ACCA_F8_General theory

1/40

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

41 Terms

Components of internal control system

control environment

entity's risk assessment

entity's process to monitor the system of internal control

information system and communication

control activities

control environment

include: governance and management functions

focus on the attitude, awareness and actions

influence the control consciousness of people and provide the overall foundation for the operation of other components

entity’s risk assessment

risk assessment process

for how managemen

entity's process to monitor the system of internal control

information system and communication

control activities

audit engagement letter

outline the nature of the contract bwt audit firm and audit client

purpose of audit engagement letter

minimize the risk of misunderstanding

confirm acceptance of the engagement

set out the terms + conditions of engagement + responsibility of management & auditors

what is included in audit engagement letter?

objective & scope of the audit

auditor & management ’s responsibilities

the applicable of financial reporting framework for preparation of FS

the form of any communication of results of audit engagement

the fact that some material misstatement may not be detected

the expectation that management’ ll provide written presentations & access to all relevant information

What does it mean ‘impraticable’ for an auditor to attand physical inventory counting?

near impossible = cause threat to auditor’s safety # inconvenience

existence vs completeness

book to floor vs floor to book

Which factors must be considered before the internal audit engagement should be accepted?

If the assignments relate to internal controls over financial reporting

If management will accept responsibility for implementing appropriate recommendations

external confirmation on trade receivables- IAS 505

bằng chứng kiểm toán được thu thập dưới dạng phản hồi trực tiếp từ bên thứ 3 cho KTV dưới dạng chứng từ giấy hoặc điện tử hoặc phương thức khác.

External confirmation is usually achieved by how?

director contact with customers

method of of confirmation

negative

positive

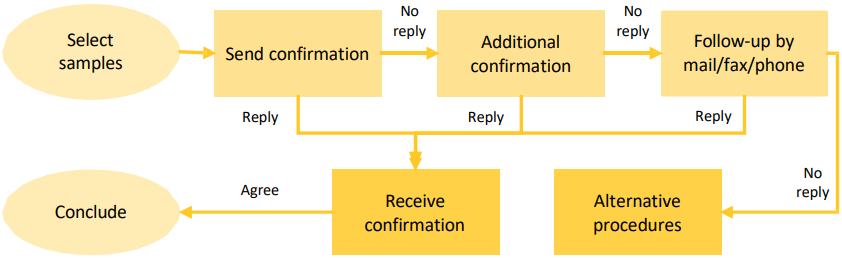

what is the purpose of this flow?

obtain external confirmation of trade receivables

which one is the most reliable?

positive confirmation

negative confirmation

positive confirmation

positive confirmation

Yêu cầu bên thứ 3 xác nhận trực tiếp về việc có đồng ý hoặc không đồng ý với các thông tin được xác nhận

current audit file

hồ sơ kiểm toán năm

negative confirmation

Yêu cầu bên thứ 3 trực tiếp xác nhận chỉ khi họ không đồng ý với thông tin được xác nhận

why should choose positive confirmation?

Khi rủi ro tiềm tàng và rủi ro kiểm soát cao

Toàn bộ hoặc một số số dư các khoản phải thu cao

when using negative confirmation?

Sai sót trọng yếu thấp

Khi rủi ro tiềm tàng và rủi rõ kiểm soát thấp hơn

Số dư của các khoản phải thu nhỏ

benefits of external confirmation

it provides evidence from an independent external source

it improves the reliability of audit evidence as the process is under the control of the auditor

adjusting events - IAS 10

those that provide evidence of conditions that existed at the end of the reporting period

non-adjusting events - IAS 10

those that are indicative of conditions that arose after the reporting period

which subsequent events should be amended in FS?

only material adjusting events would require an amendment to the figures within the financial statements

Does the auditor need to actively look for subsequent events after the auditor's report is issued

no

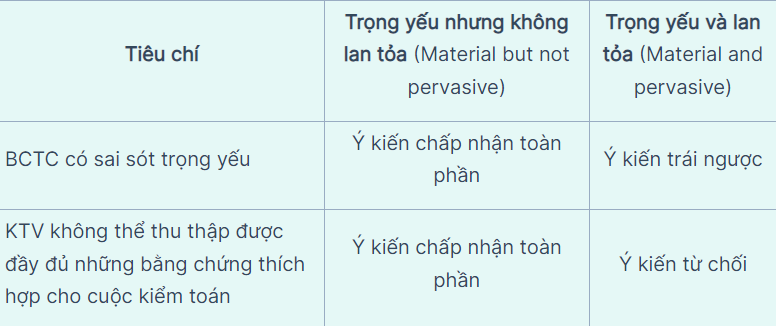

persasive

the possible effects on the financial statements of misstatements or detected misstatements

key audit matter (KAM) factors to consider:

communicate with those charged with governance

risk assessment

effect on audit

emphasis of matter paragraph

Vấn đề cần nhấn mạnh

for what

audit opinion

emphasis of matter paragraph được trình bày ở đâu?

ngay sau đoạn ý kiến của KTV trong BCKT

Sử dụng tiêu đề “Vấn đề cần nhấn mạnh”

what action need to have before disclose the matter paragraph

discuss and confirm with the director

audit risk

the risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated

inherent risk

risk of errors or misstatements due to the nature of the company and its transaction

control risk

the risk that a misstatement which could occur in an assertion about a class of transaction, account balance or disclosure and which could be material, either individually or when aggregated with other misstatements, will not be prevented, detected, or corrected on a timely basis by the entity’s internal control

detection risk

the risk that the procedures performed by the auditor to reduce audit risk to an acceptably low level will not detect a misstatement which exists and which could be material

stage of an audit engagement

planning

test of controls

substantive tests

completion

what are the actions in the planning stage?

engagement acceptance

obtain an understanding of the clients and its environment, including internal control

risk assessment

audit planning

content in key audit matter (KAM)

issue description

why determine KAM

how addressed in audit

is it a must to disclose KAM in audit report for listed company?

for listed company, it’s required to have KAM section