Equity Securities & Indexes. Primary Market and Market Indexes

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

15 Terms

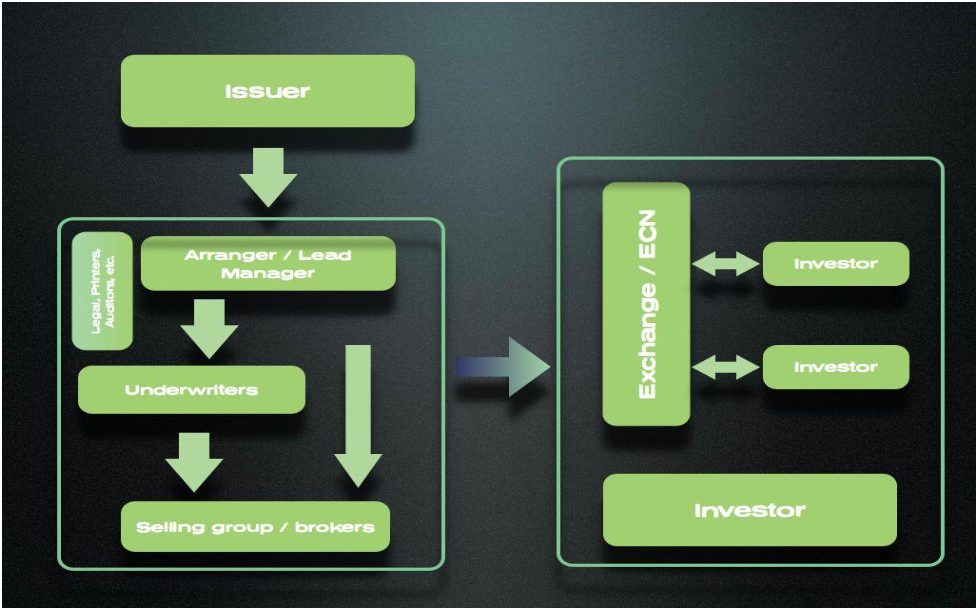

Initial Public offerings (IPO)

The process of selling stock to the public for the first time.

* Advantages:

Greater liquidity: Private investors get the ability to diversify.

Better access to capital: Public companies typically have access to much larger amounts of capital through the public markets.

* Disadvantages:

The equity holders become more widely dispersed, which makes it difficult to monitor the management.

The firm must satisfy all of the requirements of public companies (such as quarterly reports) which increase compliance costs, but also reveal too much information to potential competitor

Best Efforts Basis

For smaller IPOs, the underwriter does not guarantee that the stock will be sold, but instead tries to sell the stock for the best possible price.

Often such deals have an all-or-none clause: either all of the shares are sold on the IPO or the deal is called off.

Firm commitment

An agreement between an underwriter and an issuing firm in which the underwriter guarantees that it will sell all of the stock at the offer price.

Auction IPO

A method of selling new issues directly to the public: the underwriter in an auction IPO takes bids from investors and then sets the price that clears the market.

Road show and Book building

In a firm commitment deal, the underwriter promotes the IPO and tests investors’ demand.

Road show

During an IPO, when a company’s senior management and its underwriters travel around promoting the company and explaining their rationale for an offer price to the underwriters’ largest customers, mainly institutional investors such as mutual funds and pension funds.

Book Building

A process used by underwriters for coming up with an offer price based on

their valuation, as well as customers’ interest.

Private Offering

Disclosures about risks are fewer than in a public offering

Only for sophisticated investors (money management firms or wealthy individuals)

Usually cannot be re-sold in the public markets for a specified period of time

Secondary offerings

The firm´ s shares are already trading

The selling of additional shares

Large shareholders want liquidity (one single large investor offers its shares to the market)

Proceeds of the sale go to the sellers, not to the company

No dilution of existing shareholders (no more capital issued)

Direct listing

Alternative to IPO´s. (Spotify or Slack). Direct Listings use an electronic auction by the Stock Exchange to get startups a fairer price for their shares than investment bankers might. But they don't allow firms to raise new money. Only for cash rich firms.

Special Purpose Acquisition Company (SPACS)

“Shell firm” that go public promising to buy one or more unlisted private businesses with the proceeds from the listing. These companies then fill the “shell”. Deals faster and more predictable. In 2020 70 SPACS went public raising 25 bn.

Mergers & Acquisitions

Market for corporate control

* Acquirer (or bidder) – the buyer of the firm

* Target – the seller of the firm

The global takeover market is highly active, averaging more than $1 trillion per year in transaction value.

Merger Waves:

Peaks of heavy activity followed by quiet throughs of few transactions in the takeover market.

=> Usually there is more activity during economic expansions

Value creation through mergers

Acquirers usually add economic value that an individual investor cannot add.

Most of this value comes from synergies in the form of cost reduction or revenue enhancement.

Economies of scale and scope

Vertical integration

Expertise

Monopoly gains

Efficiency gains

Tax saving from operating losses

Diversification (risk reduction, borrowing capacity, liquidity)

Earnings growth

Stock Market Indexes

Definition: “Proxy” of the markets.

“Exposure” to a given market or types of equity.

Exposure in terms of: geography, type of stocks (“value”, “growth”, “size”, “volatility” risk).

Bet on a group of stocks rather than doing so individually.

“Benchmarks” for investors´ investment portfolios. “Beat the market” (active management) vs “Tracking the market” (passive)

Construction: Equally weighted indices or “market cap” weighted.

Free float

the real amount of stock available to trade on a given market