econ part two :(

1/60

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

61 Terms

quota rent

extra profit someone receives from limit on supply. Example: shoes were 30 dollars at world price, but quota limited the imports. therefore, domestic prices can be raised

three benefits of international trade

lower-priced goods, increased variety of products, access to scarce resources

Autarky

situation in which a country is closed to international trade

Absolute Advantage

ability to produce more output given similar resources than another producer

hint: consumption with trade will be a dot outside of the ppf line

hint: specialization is based on comparative advantage, so always check that to see if they should trade

terms of trade

the price of one g/s in terms of another

Hints: looking at opportunity costs, if someone is selling something, the trade must be greater than the opportunity cost. if someone is buying something, the trade must be less than the opportunity cost

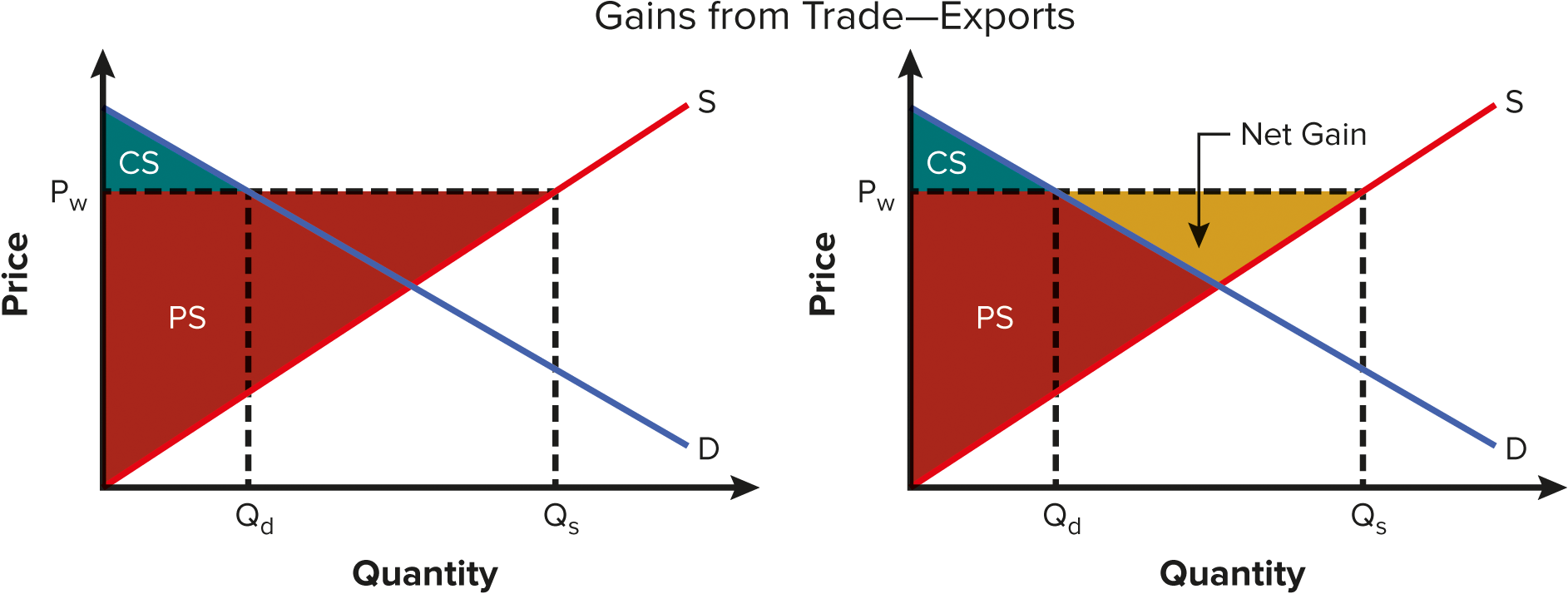

Gains from trade

Benefit or wealth to buyer or seller as a result of trade- this picture is exports

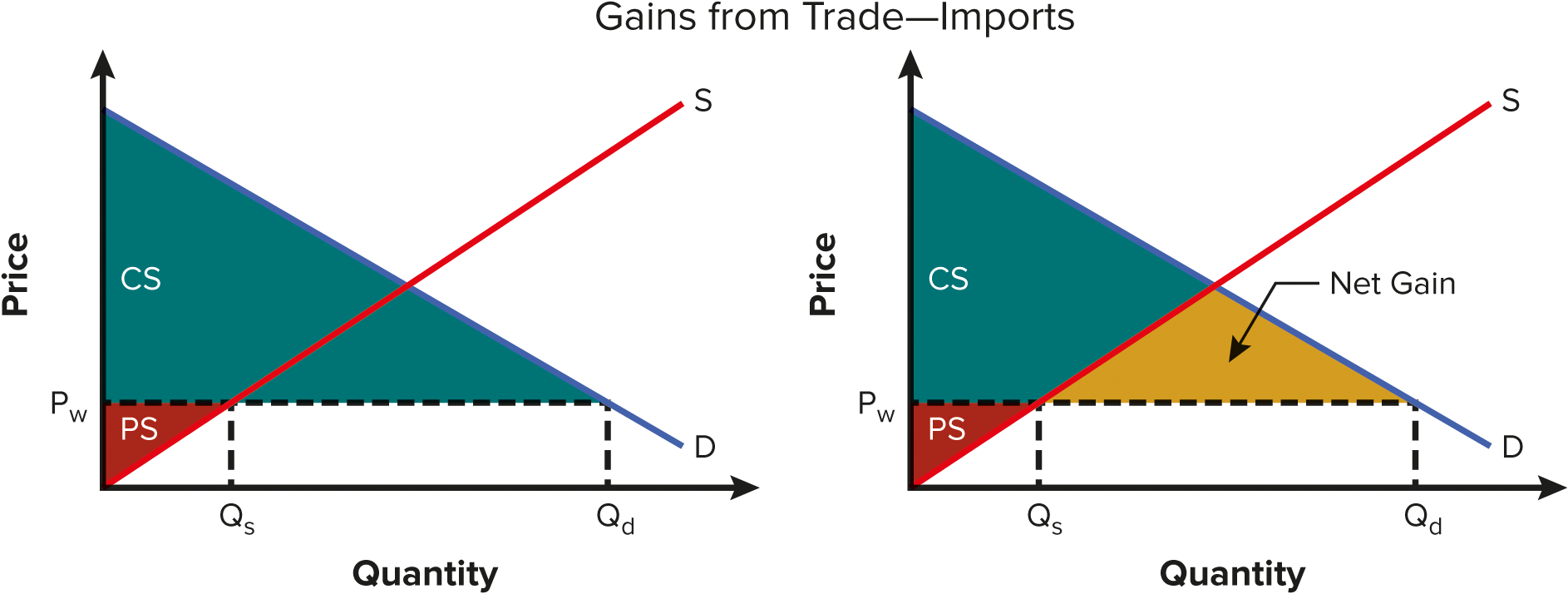

gains from trade imports

hint: numbers dont equal wealth. just because someone numerically is getting a better trade, they could really like and value the item they are trading and end up being more “wealthy" than the other person

Hint: the country that benefits more is the one that trades closer to the other persons opportunity cost

small country market

a country so small it just has to accept the world price of a good

price takers

firms that take market price and have no ability to influence that price

Hint: whether the world price is below or above the domestic price, when a country opens to international trade, the total amount of product traded globally will increase

welfare effects

effects that change in market conditions, usually price, has on welfare or ecnonomic wellbeing of market participants

welfare effects of exports

consumer surplus falls, producer surplus rises, overall society is better off

welfare effects of imports

consumer surplus rises, producer surplus falls, overall society is better off

hint: international trade can reduce jobs in domestic markets

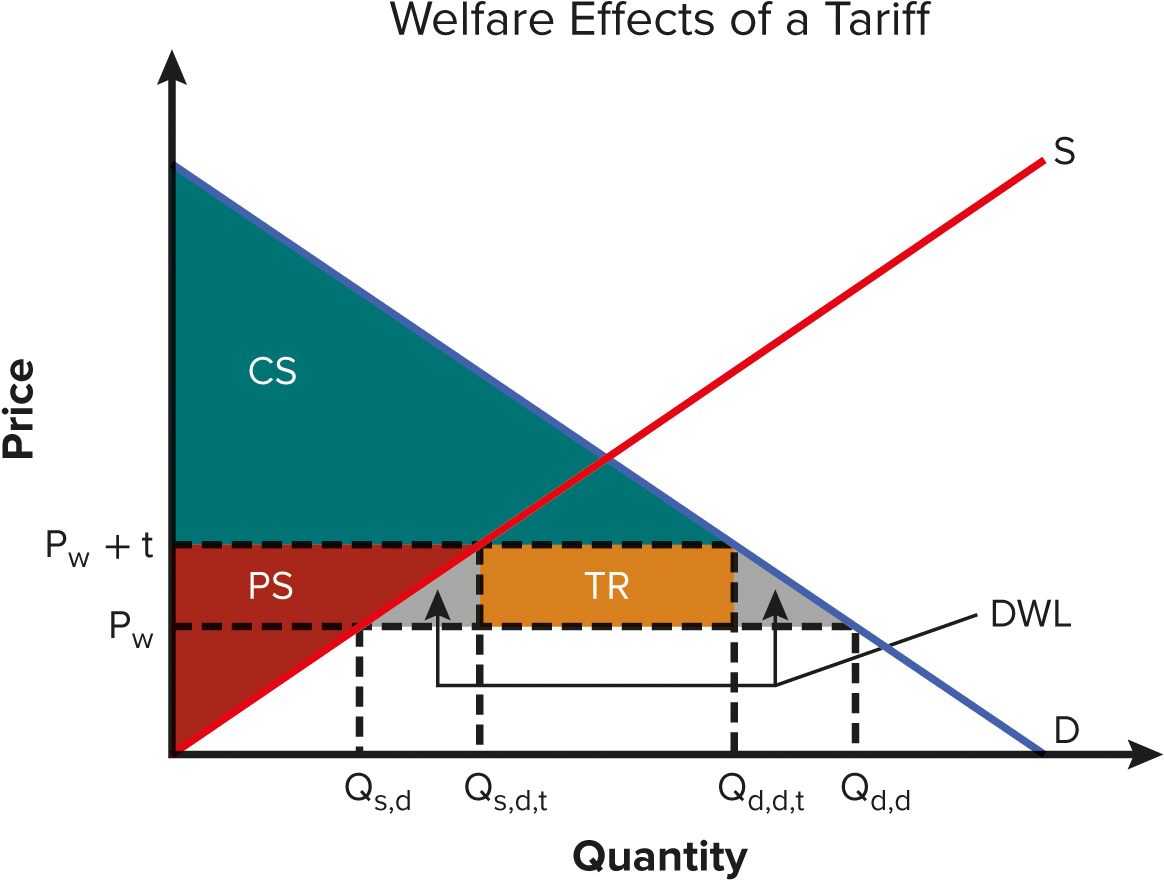

tariff

a barrier to trade, reduces imports, a tax or fee that must be paid to export

tariff welfare effects

consumer surplus falls, producer surplus rises, government collects tariff revenue, overall society is worse off

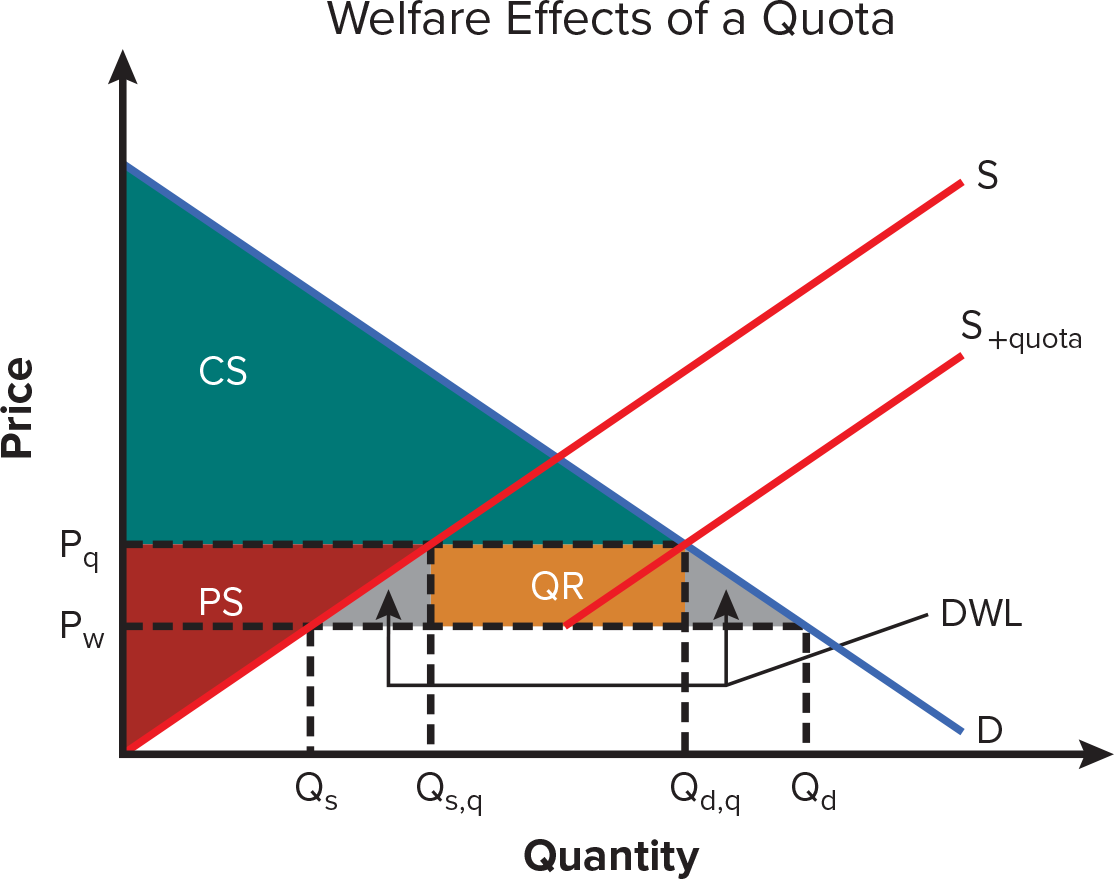

quota

numerical limit on import

quota welfare effects

consumer surplus falls, producer surplus rises, owners of quota rights gain, overall soceity is worse off

quota rent

income from quota

utility

satisfaction or happiness from consumption of goods or services

total utility

total satisfaction from consumption of good/service or combo of g/s

marginal utility

additional satisfaction from consumption of additional unit of g/s

decision making factors

rational,ranked preferences, limited incomes, prices

equal marginal principle

consumers maximize utility when they allocate their incomes in a way that marginal utility per dollar spent on each choice in the bundle is equal

equal marginal utility how to solve:

divide marginal utility by dollar

go down the list, seeing which one gives you higher marginal utility

start at 1, then 2, and if the other item’s “1” is higher than the other item’s “2”, then you get that one instead

total utility equals?

sum of marginal utilities

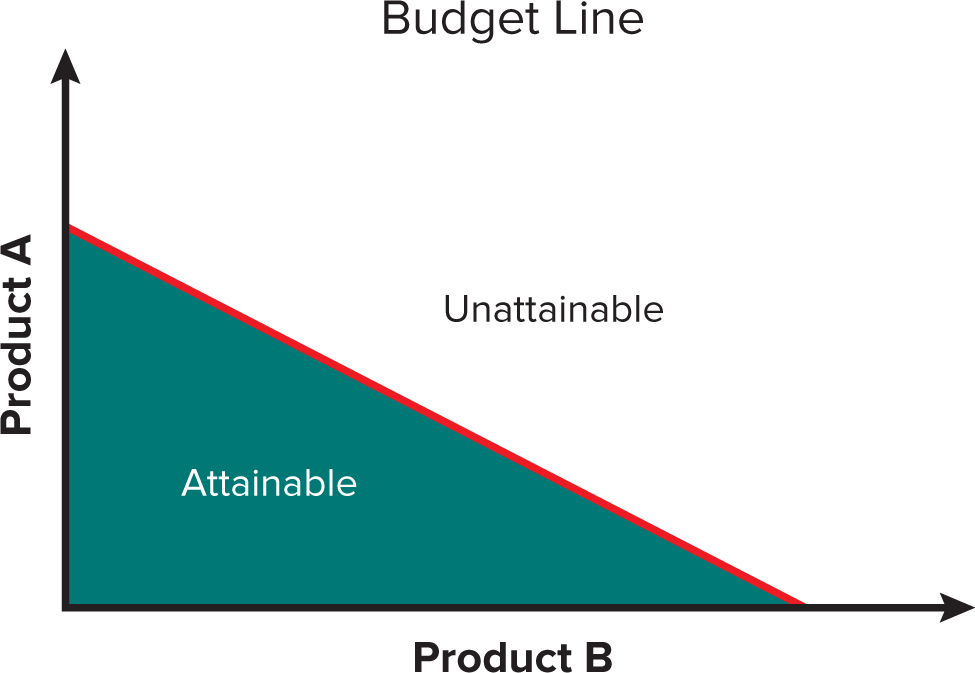

budget line

line showing different combos of two products that can be purchased with given budget and with known prices

indifference curves

curve showing the combos of two products that generate the same amount of utility

indifference curves qualities

downward sloping, curves farther from the origin are preffered, indifference curves cannot cfross

hint: when budget line and indifference curves cross, maximize

economic costs

sum of explicit and implicit costs, costs associated w/ use of resources

explicit costs

monetary costs

implicit costs

costs associated w/ opportunity costs of using owned resources

accounting profit

total revenue minus explicit costs

ecnonomic profit

total revenue- economic costs (explicit and implicit)

hint: zero accounting profit isnt good, means economic profit is zero. Zero economic cost however is okay, means youre doing just as well as your next best option

short run

time period which one variable stays the same the others can change

total product

total output w/ given resources

marginal product

addtional output produced in result of of utilizing one more unit of a variable resource

average product

average product produced per unit of chosen resource

increased marginal returns

marginal product w/ next unit of variable resource is greater than that of previous vriable resource

diminishing marginal returns

hints: average fixed cost always declines with more output produced

average variable and fixed cost declines then increases

avt and atc are not parallel

three types of average costs

fixed afc, variable avc, total atc divide all of those by total output

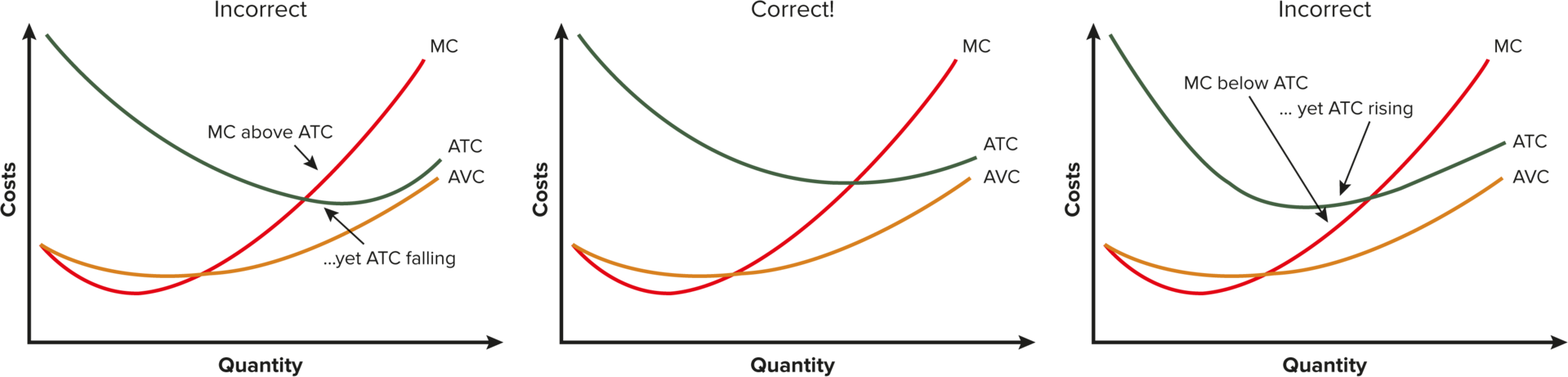

Hint: if marginal cost is above average, it increases. if it is below average, it decreases

curves of mc avc and afc

rememeber MC intersects at the minimum point of their curves

short run average total cost (ATC)

curve showing average total cost for different levels of output when at least on input is fixed, usally plant capacity

long run average total costs curve

curve showing lowest average total cost for any given level of output when all inputs in production are variable

price elasticity of demand

a measure of how responsive quantity demanded is to price change. percent change in quantity. percent change in price. Always negative, price increase= quantity demand decrease, price decrease= quantity demand increase

price elasticity of demand midpoint formula

midpoint percent change in demand/ midpoint percent change in price

calculate by product 2-product 1/ (p2+P1)/2 times 100 do this for quantity and price then divide the two

inelastic

less sensitive to change, less than one

elastic

greater than one, sensitive to change in price

unit elastic

equal to one

perfectly elastic

any change makes 0 demand immediately

perfectly ineqlastic

ends up equaling zero, any change in price leaves quantity demanded unchanged

Hint: elastic is flatter, inelastic is steeper

hint: in a line of an elasticity curve, unit elastic is max, top of the line is elastic, bottom of the line is inelastic

Hint: more substitutes equals more elasticity