Lesson 11

1/18

Earn XP

Description and Tags

Notes from slides

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

19 Terms

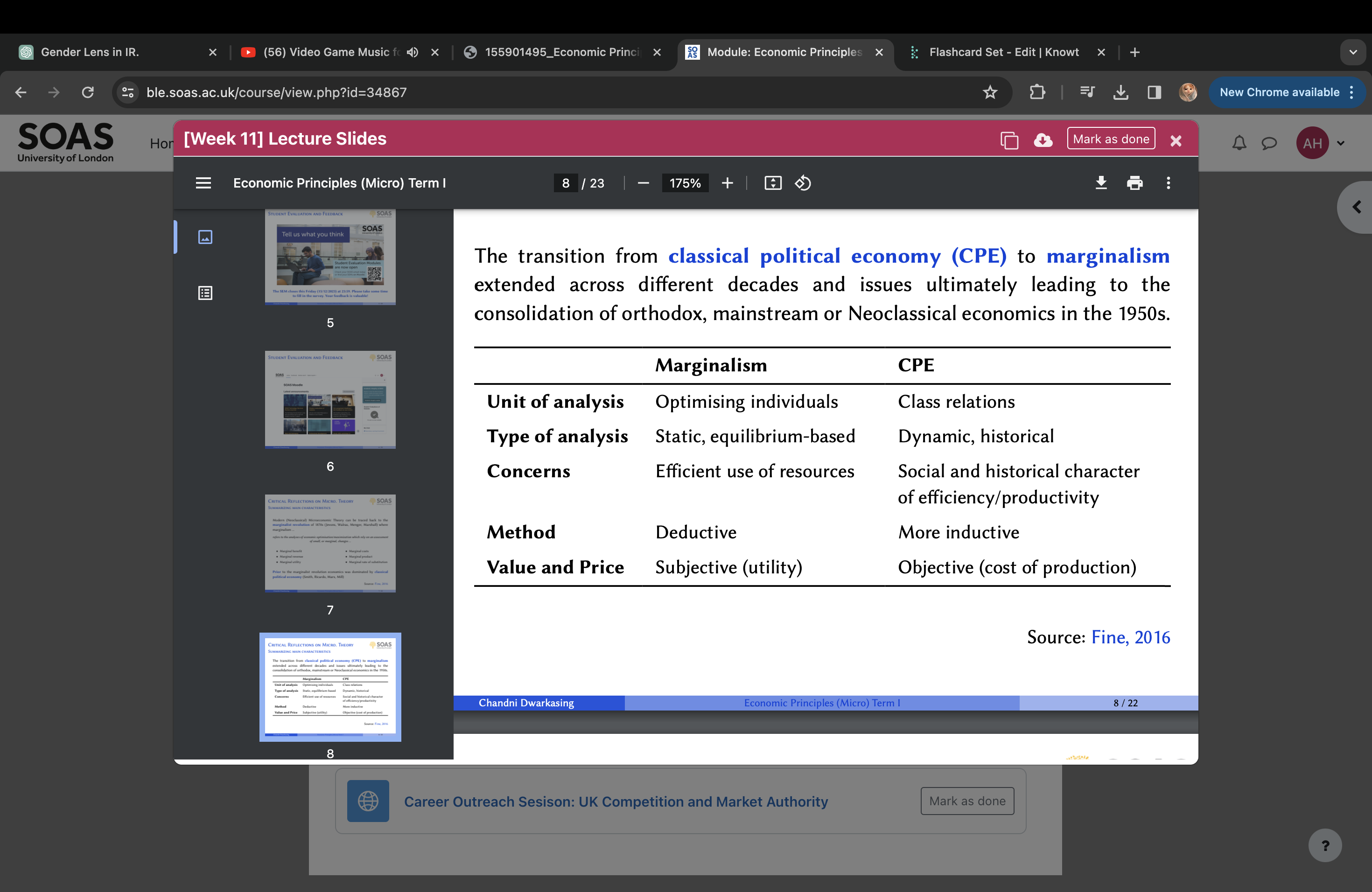

Modern (Neoclassical) Microeconomic Theory can be traced back to the marginalist revolution of 1870s (Jevons, Walras, Menger, Marshall) where marginalism ...

refers to the analyses of economic optimisation/maximization which rely on an assessment of small, or marginal, changes ...

• Marginal benefit

• Marginal revenue

• Marginal utility

• Marginal costs

• Marginal product

• Marginal rate of substitution

Prior to the marginalist revolution economics was dominated by

classical political economy (Smith, Ricardo, Marx, Mill)

The transition from classical political economy (CPE) to marginalism extended across different decades and issues ultimately leading to the consolidation of orthodox, mainstream or Neoclassical economics in the 1950s.

Inductive reasoning uses specific observations to make generalizations,

while deductive reasoning starts with a general statement to reach a specific conclusion.

Neoclassical consumer theory in a nutshell:

• An individual disposes a set of subjective preferences

• Individual preferences are represented/mapped to a utility function

• If a consumer prefers good x1 over good x2 → u(x1) > u(x2) • Consumer behaviour is a matter of maximising utility given constraints (prices & budget)

• Marginal utility is a decreasing function of consumption

Consumer preferences are thus purely subjective, personal and fixed without reference to external (or internal, self-reflecting) influences

What Neoclassical consumer theory overlooks:

Pleasure is not only derived from receiving a specific quantity of goods but the creation of pleasure and enjoyment out of those goods

• Consumption is influenced by social factors: being accepted, being unique but also cultural and social norms (advertising understands this!)

• Are consumers always autonomous, rational, selfish and perfectly aware of their own preferences?

• What about altruism, cooperation, engaging in unpaid labour?

Overlooking these aspects and treating consumers as homo-economicus allows one to flawlessly derive how much of a good will be demanded at different prices in a given economy.

What is the standard assumption on the consumer demand curve?

The standard assumption on the consumer demand curve is that all factors influencing consumer behavior, except for price, remain constant.

Down-ward sloping hence, p ↑ → D ↓

• Giffen Goods: Demand goes up when the price goes up (non-luxury, essential, inferior goods such as staple foods)

• Luxury Goods: Demand goes up when the price goes up (luxury, premium goods associated with status and conspicuous consumption)

To which goods and for what type of consumers these law-defying situations hold is not uniform. → depends on income and socio-cultural factors!

In Neoclassical economics, the aggregate demand curve for a given economy assumes that

preferences and the relationship between price and demand is uniform across every single consumer (requires an estimation of a ’representative individual/agent’).

Does it matter if the choice of the representative agent is or is not realistic?

"Its task is to provide a system of generalizations that can be used to make correct predictions about the consequences of any change in circumstances. Its performance is to be judged by the precision, scope, and conformity with experience of the predictions it yields. In short, positive economics is, or can be, an "objective" science, in precisely the same sense as any of the physical sciences" Milton Friedman, 1953

This quote is discussing the concept of positive economics, which aims to provide a set of rules or principles that help predict what will happen when circumstances change. The quote suggests that the success of positive economics should be measured by how accurate, comprehensive, and consistent its predictions are with real-life experiences. Essentially, it's saying that positive economics can be as objective and reliable as the natural sciences, like physics or chemistry, in predicting outcomes based on changes in situations.

Some alternatives to Neoclassical Consumer Theory:

• Behavioural Economics:

Committed to the testing the empirical validation of neoclassical utility theory and adjusting it on the basis of this testing process. E.g. motivations beyond maximization

• Prospect Theory:

Alternative to neoclassical decision-making under risk (expected utility theory). Two phase decision process 1) gains and losses are coded against reference point 2) evaluation of each prospect leading to choice

• Endogenous Preference Theory:

Attempts to model the evolution of preferences over time under influence of markets, institutions and cultures (challenges fixed preference assumption)

• Procedural/Bounded Rationality:

Assumes that agents lack perfect knowledge and the ability to process large amounts of data (satisfactory vs optimal decisions)

• Systems of Social Provisioning:

Focusses on items of consumption rather than individuals. Attempts to identify how levels of commodity consumption and who consumes depends on modes of production and socially determined socio-economic variables

Key Neoclassical Producer Theory assumptions:

• Production is requires inputs which each have a cost/price

• Cost-minimisation implies MPi = pi (optimal input allocation) (MPi stands for the marginal product of input i, which is the additional output produced by adding one more unit of input i while holding other inputs constant. pi represents the price of input i, which is the cost incurred to acquire one unit of input i. In other words, the firm is getting the most value out of each unit of input it purchases.)

• There are decreasing returns to the use of one factor

• Profit-maximisation implies production is determined by MC = MR (optimal output)

• When it comes costs a distinction is made between economies and diseconomies of scale

Under perfect competition:

− Industry-wide demand curve is downward-sloping

− Single-firm demand curve is horizontal

− No barriers to entry

− Normal profits made in the short-run: TR − TC > 0

− Zero profits made in the long-run: TR − LRAC = 0

− Temporary economies of scale or diseconomies of scale

Under imperfect competition

− Single-firm demand curve is down-ward sloping

− Persisting economies of scale

− Distinction between monopolistic competition, oligopolist competition and monopolies

− Above distinction determines barriers to entry and interdependence

some other notes ?

• Production is asocial

• Technology and the organization of production are taken as given

• There are decreasing returns to the use of one factor

• Market equilibrium is achieved when supply = demand

Each of these assumptions treats capitalism as a harmonious and efficient cooperation among sacrifices. Workers earns a wage which is equal to the marginal product of labour. Owner of the firm is seen as an entrepreneur and earns normal profits as a compensation based on the opportunity cost of using their money elsewhere. Production is asocial and technology and the organization of production are taken as given. In this framework, capitalism as a conflictual society where distribution refers to the division of a surplus among classes (workers, capitalists and landlords) does not hold.

Another way to frame this critique is to argue that Neoclassical Economics fails to account for power relations….

Market exchange is considered to be the central organizing principle in the economy

Individual identities and roles outside of the market are regarded as irrelevant: individuals show up on the market as owners of commodities they are willing to sell to satisfy their needs

Agents are free to choose with whom they exchange and whether they exchange at all

The capitalist economy is depicted as a set of voluntary agreements between free and equal individuals → absence of power

Some alternatives to Neoclassical Producer Theory based on the treatment of profits and distribution:

• Neo-Ricardian Approach: After all capital inputs and rent has been paid for, there’s an economic surplus which needs to be divided between capitalists (owners of the firm) and workers. Either the wage or rate of profit is taken as a given, allowing for an inverse relation between the wage and rate of profit.

• Marxist Approach: Profits are the money form of surplus value produced by labour and appropriated by capitalists. The amount of labour commanded by the wage < the amount of labour power used up in the production process. Exploitation is the source of surplus value.

• Schumpeterian Approach: Profits are driven by innovation and the superior amounts of productivity it entails. Only occurs in disequilibirum, dissipate in equilibrium.

The assumption of rational behaviour in microeconomic theory means that firms will want to grow and innovate as long as benefits > costs:

• Costs: Investment in adoption or R&D → entrepreneurial & high risk

• Benefits: Gain super profits (new products, new services), reduce costs (of labour and/or capital input)

Disruptive technologies

The introduction of new technologies often interferes with perfect competition through the generation of monopolies, monopolistic competition and positive network externalities. This is particularly apparent in Information and Communication Technologies (ICT)

Disruptive technologies: Imperfect competition

Borderline monopolies:

• Google search engine

• Windows operating system

• Meta (Facebook and Instagram social media platforms)

• Youtube

• Amazon (online shopping but also web hosting!)

Monopolistic competition

• Deliveroo, UberEats, JustEat

• Dating platforms

• The variety of small online webshops

network externalities

Network externalities/effects apply to almost every sector of the ’internet’ industry

The more people are using e.g. Facebook, the more likely new users will join → direct effect.

The more people are using Facebook, the more likely new advertisers will join → indirect effect.

Facebook is a two-sided market: 1) users, 2) advertisers → incentive to keep service free for 1) because revenue can be earned through 2). Same for Google, Twitter, etc.