Looks like no one added any tags here yet for you.

Account

Records of increases or decreases in a specific value (asset, liability or owner’s equity)

Double-entry accounting system

Each transaction must affect two or more accounts to keep the basic accounting equation in balance.

Recording done by debiting at least one account and crediting another account.

DEBITS must equal CREDITS.

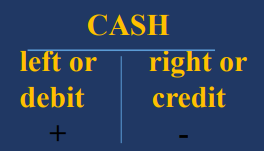

T-Account

It is the simplest form of an account

It gives you another way of analyzing transactions with each account separately analyzed for increases and decreases in the values.

It got its name because it resembles the letter T and is convenient to use as it has two sides- the left side and the right side where the increases and decreases are separately placed.

At the center is the name or title of the account. In accounting, the left side is called the debit side and the right side is called the credit side.

Normal Balances

This is in the side of the equation where the account is increased.

The accounts’ _______ _______ is as follows:

Assets - Debit

Liabilities - Credit

Owner’s Equity - Credit

Investment - Credit

Drawing - Debit

Revenues - Credit

Expenses - Debit

Chart of Accounts

It is simply a listing of all account titles, the number and nature of which depend on the type of business operation.

The accounts are properly arranged with the assets followed by the liabilities and the owner's equity.

Account numbers are assigned for easy reference usually with an allowance for accounts to be added.

Business Documents

Source documents evidencing transactions of a business.

General Journal

Book of original entry

Transactions are recorded in chronological order.

The simplest form is called a 2 column _________ _________.

Benefits of the recording process:

Discloses the complete effects of a transaction.

Provides a chronological record of transactions.

Helps to prevent or locate errors because the debit and credit amounts can be easily compared.

Journalizing

It is the process of entering transaction data in the journal.

There are 2 types of it, namely:

Simple Entry

Compound Entry

Simple Entry

[Journalizing]

Consists of 2 accounts, one debit and one credit.

Compound Entry

[Journalizing]

Consists of 3 or more accounts.

General Ledger

Book of final entry.

It contains the entire group of accounts maintained by a company.

It includes all the asset, liability, owner’s equity, revenue and expense accounts.

Ledger

Device used to record increase and decrease affecting assets, liabilities and owner’s equity.

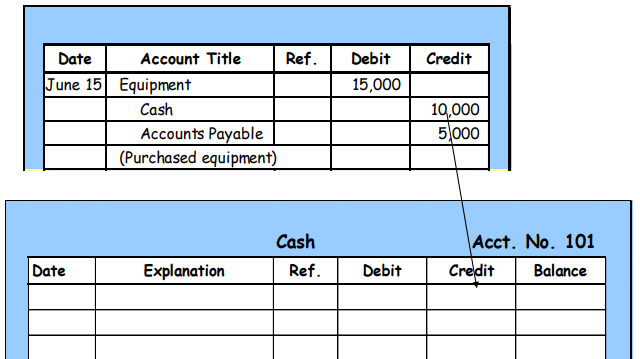

Posting

This is a process of transferring amounts or debits and credits from the journal to the ledger. Each account has a separate ledger page, such as the cash ledger shown.

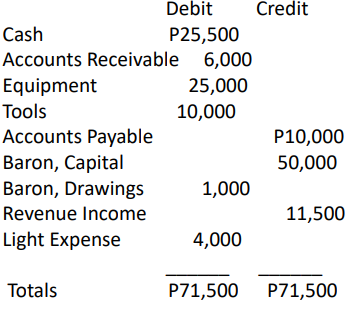

Trial Balance

A list of accounts and their balances at a given time.

Purpose is to prove that debits equal credits.

Subsidiary Ledger

It is a detailed record of individual accounts that support and provide more detailed information than the general ledger, typically for accounts like accounts receivable or accounts payable.

It helps in tracking specific transactions and balances for each customer or supplier.

Control Accounts

It is a general ledger account that summarizes the total balances of a subsidiary ledger, ensuring accuracy and simplifying financial reporting.

It provides a summary of detailed transactions without cluttering the general ledger.

Examples of these are:

Accounts Receivable

Accounts Payable

Invoice

Issued when service or merchandise is given to a customer.

Official Receipt

Issued when cash is received by the entity.

Check or Cheque

A negotiable instrument used as substitute for cash, the payment of which is drawing against the entity’s or individual’s current account.

Statement of Account

A bill presented to a customer for service rendered or merchandise given for which payment is demandable.