Life Insurance - C6-C7

1/45

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

46 Terms

Premium Calculation

Gross & Net Premium

Premium Calculation

Payment Rules

Premium Calculation

Pricing Methods

Chapter 6: Premium Calculation

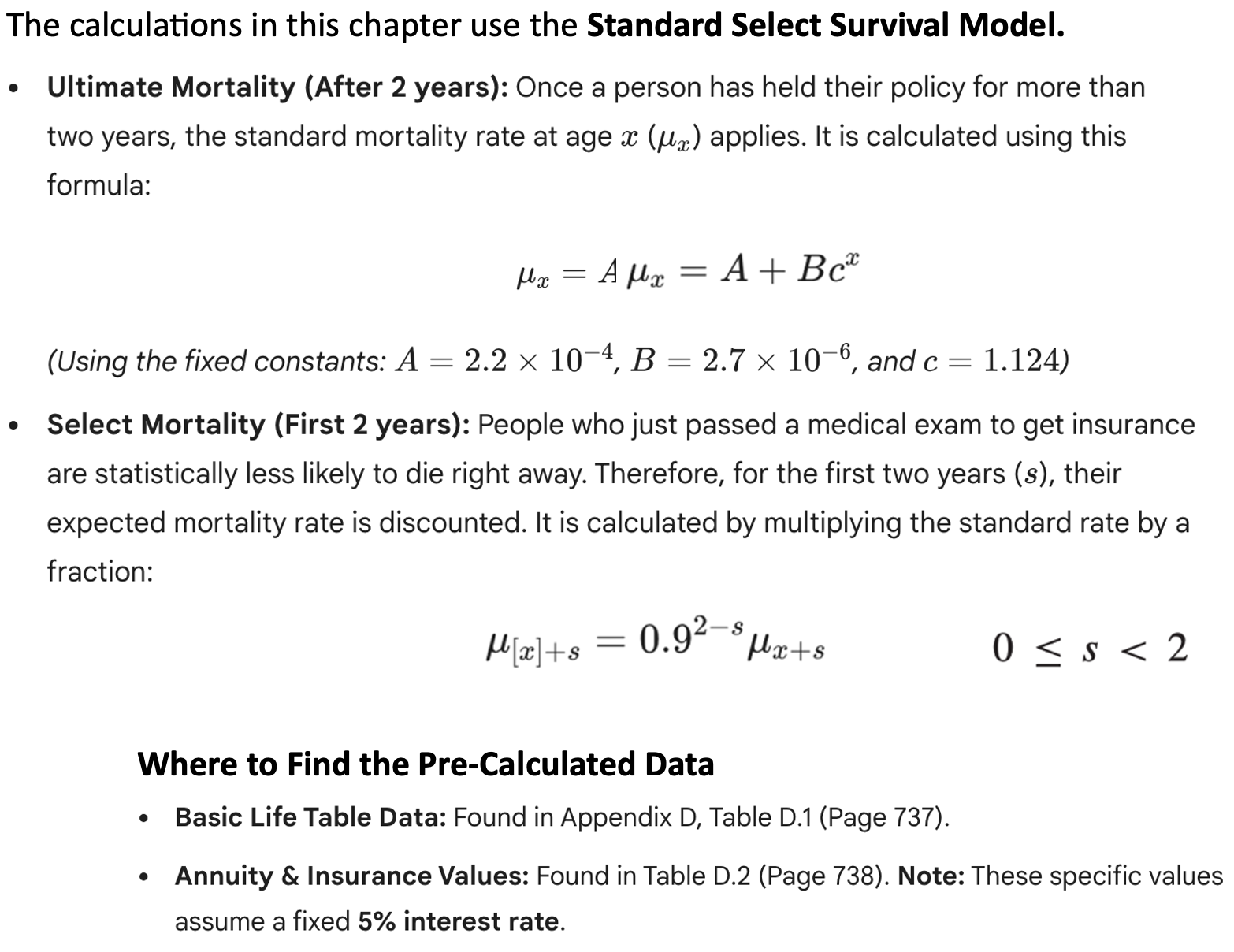

Assumptions

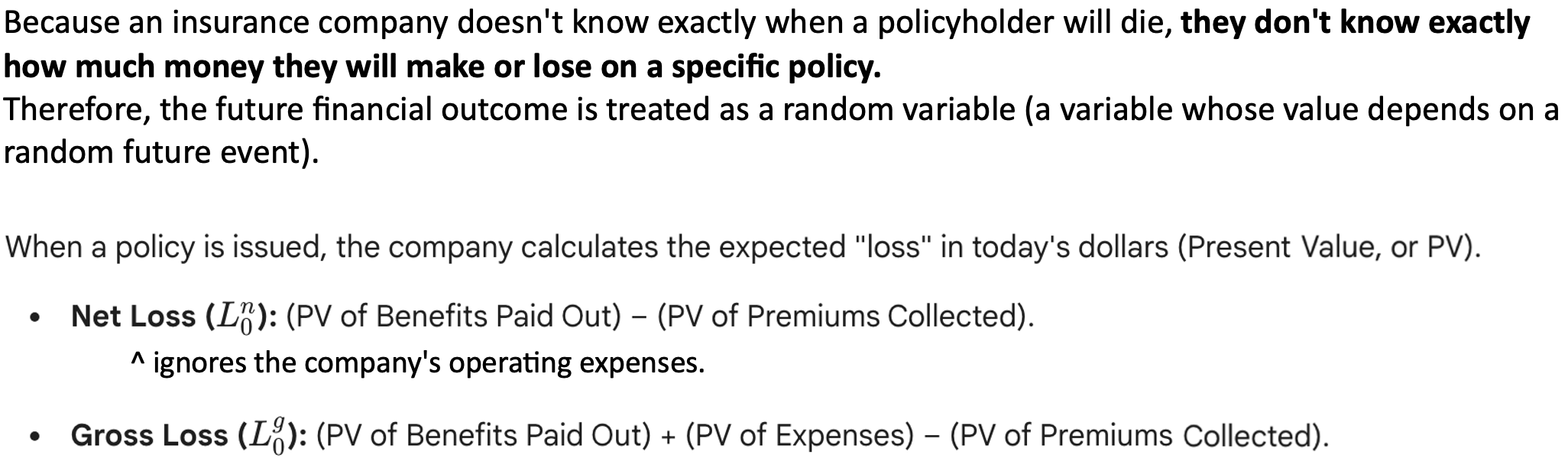

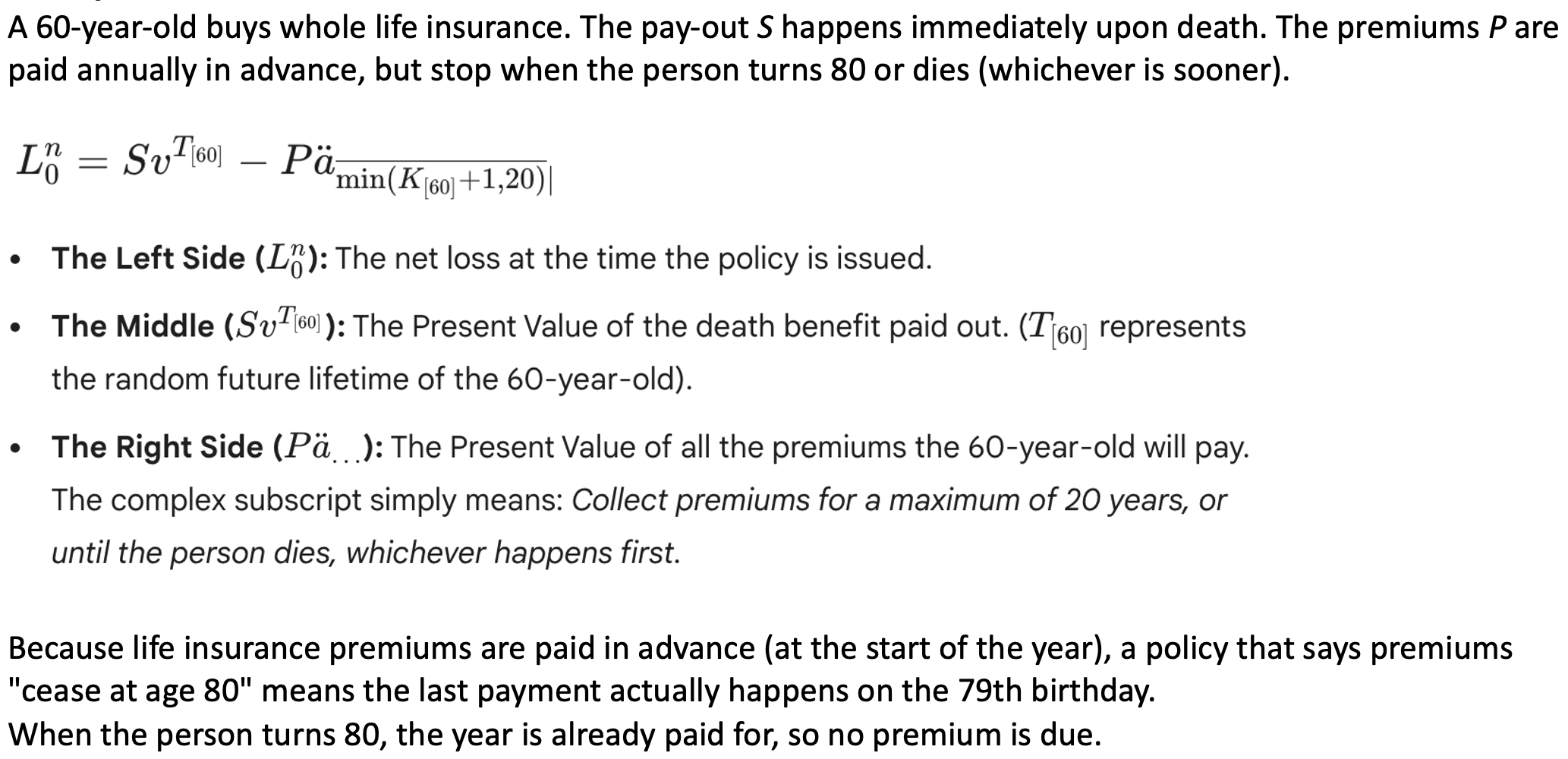

The loss at issue random variable

The loss at issue random variable

Example

Premium Principle

Once the insurer calculates all the different possible ways they could lose or make money on a policy (the "loss distribution"), they need a formalized rule to decide exactly how much to charge the customer = Premium Principle

The Equivalence Principle Premium

The Equivalence Principle Premium

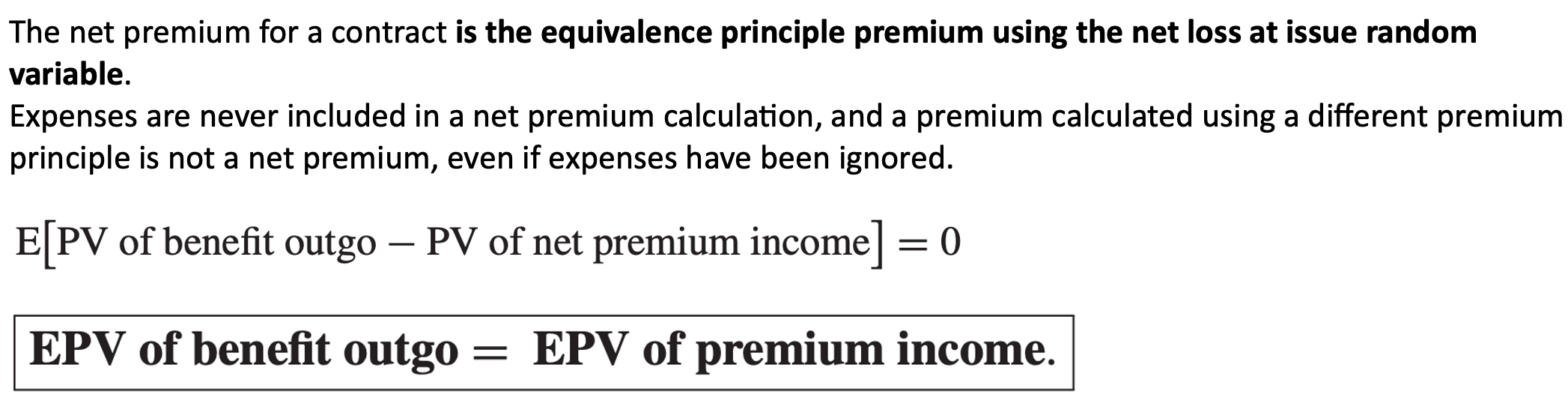

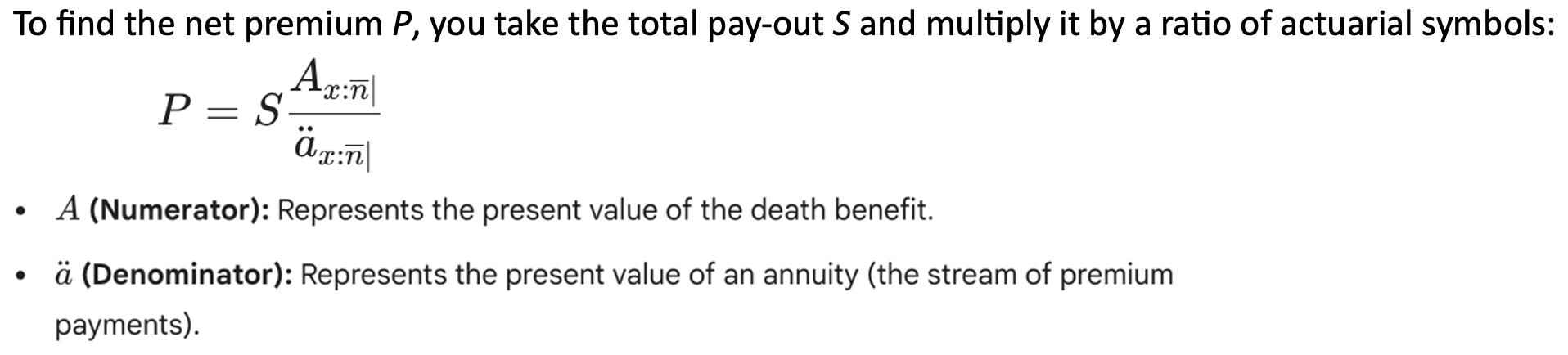

Net Premiums

The Equivalence Principle Premium

Net Premiums

The Standard Premium Formula

The Equivalence Principle Premium

Net Premiums

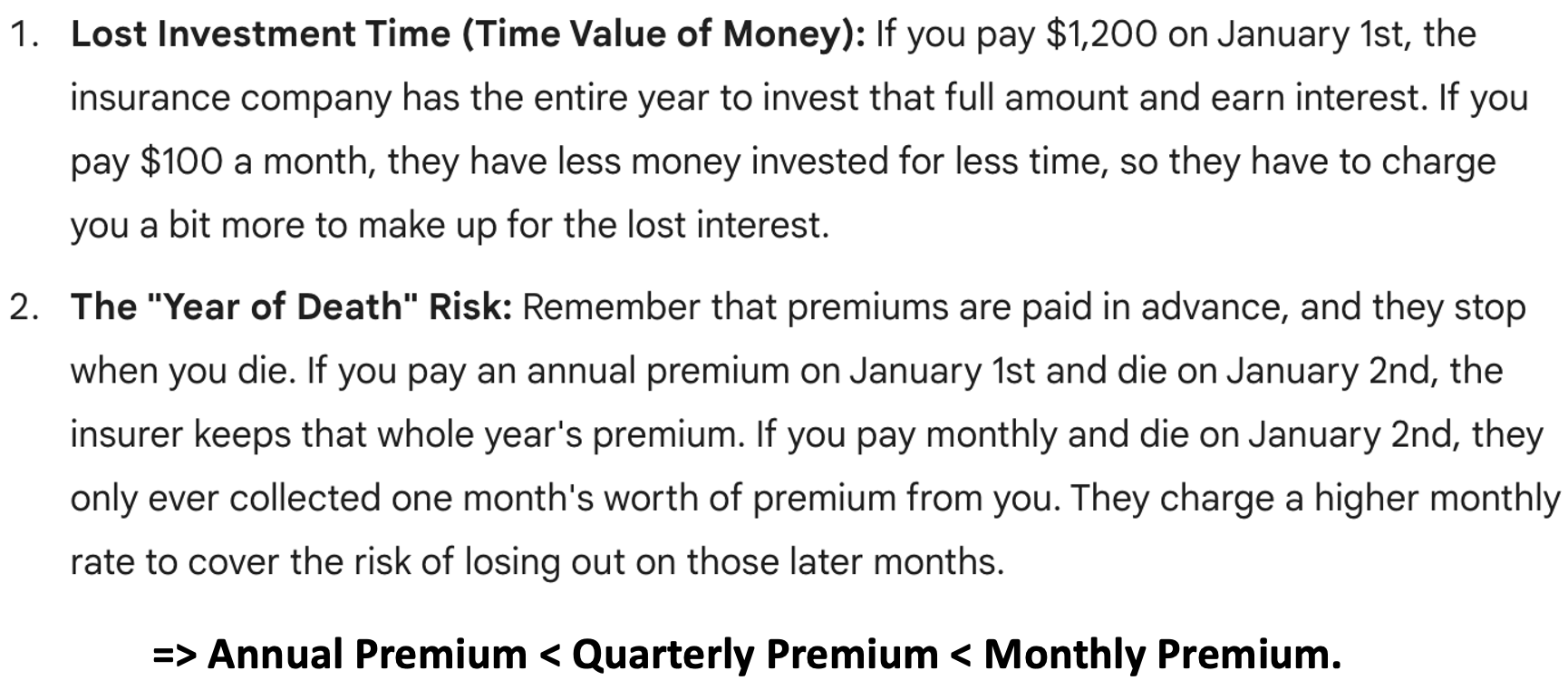

Why Monthly Premiums Cost More

The Equivalence Principle Premium

Gross Premiums

The Equivalence Principle Premium

Gross Premiums

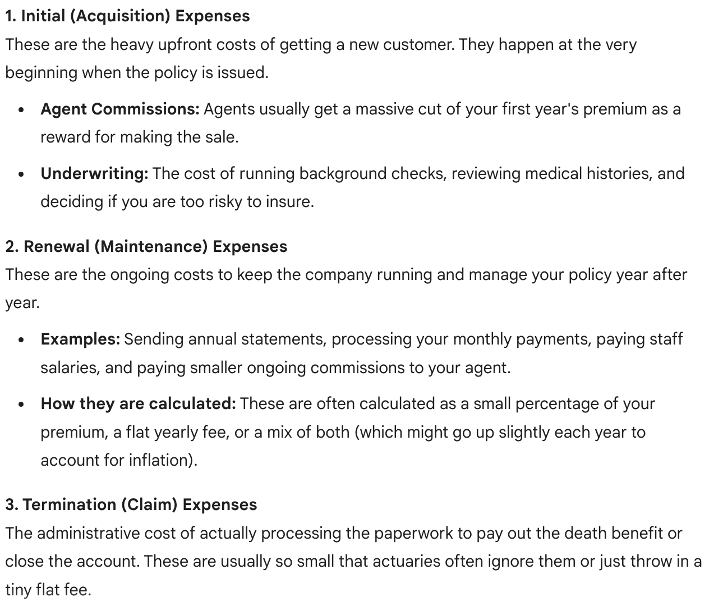

These company expenses are three categories:

The Equivalence Principle Premium

Gross Premiums

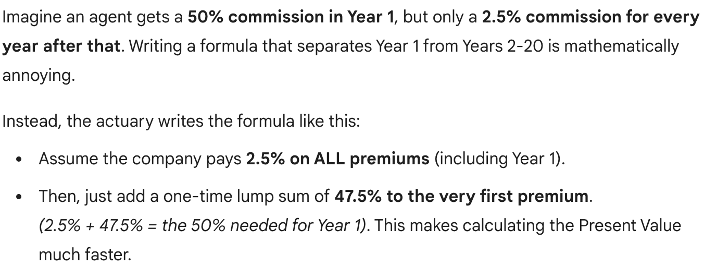

The Actuary's Math Shortcut

The Equivalence Principle Premium

Gross Premiums

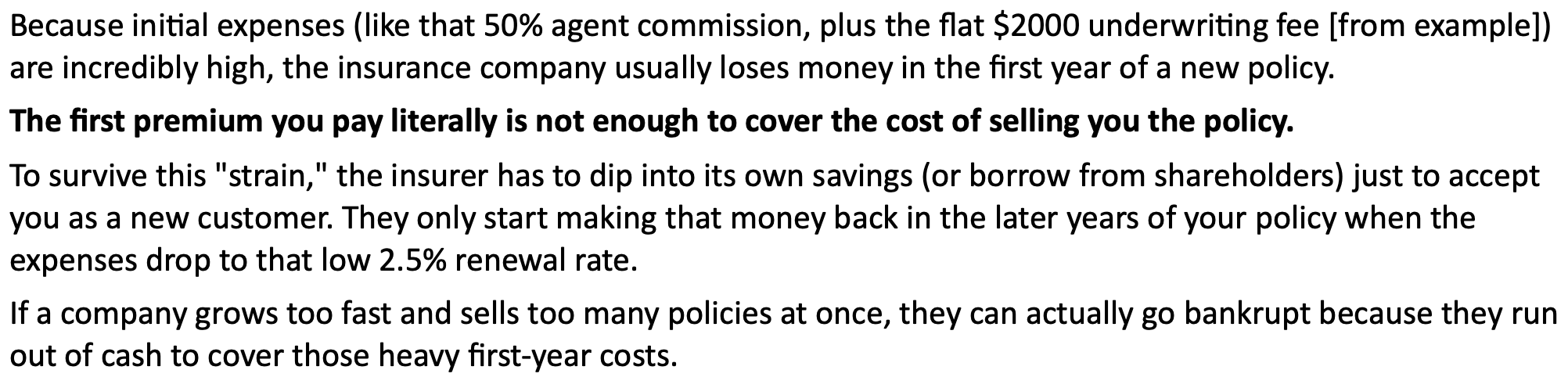

New Business Strain

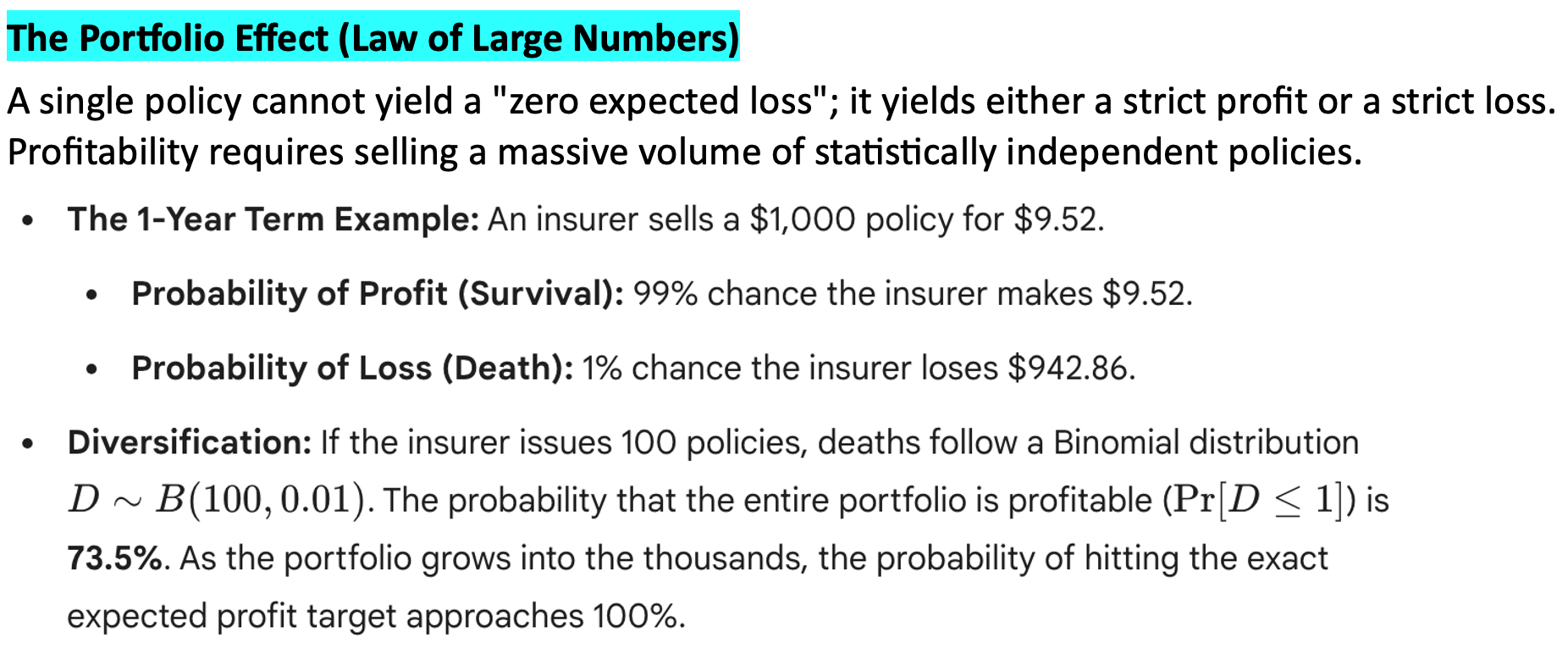

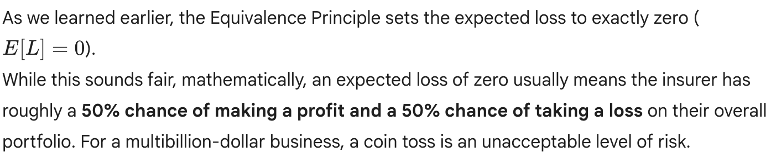

If the Equivalence Principle sets the expected profit exactly to zero, how do insurance companies actually make money?

The Portfolio Effect

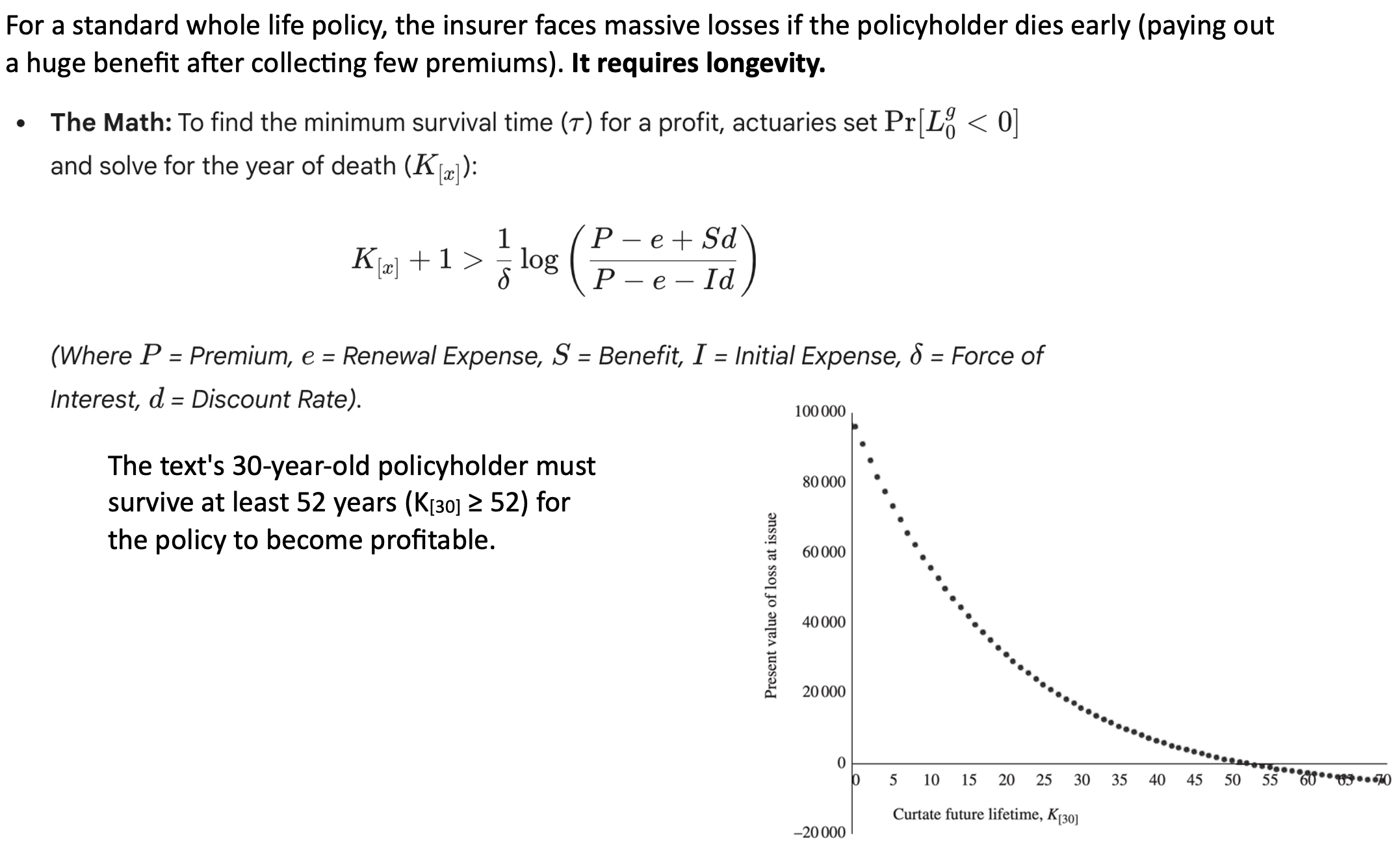

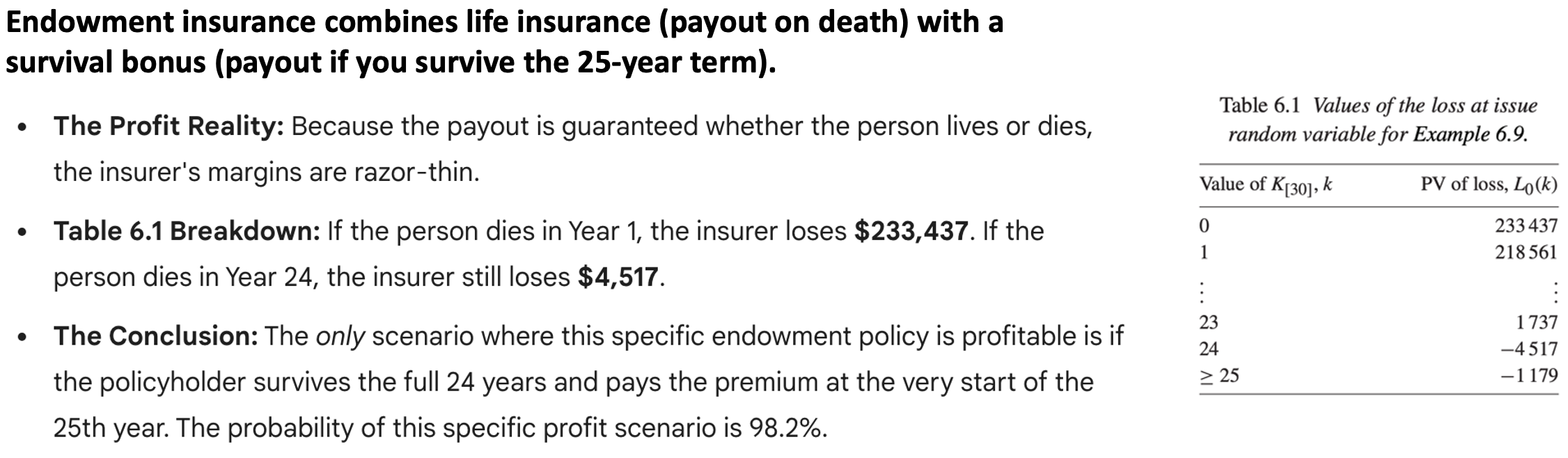

Calculating the "Tipping Point" of Profitability

Calculating the "Tipping Point" of Profitability

Life Insurance

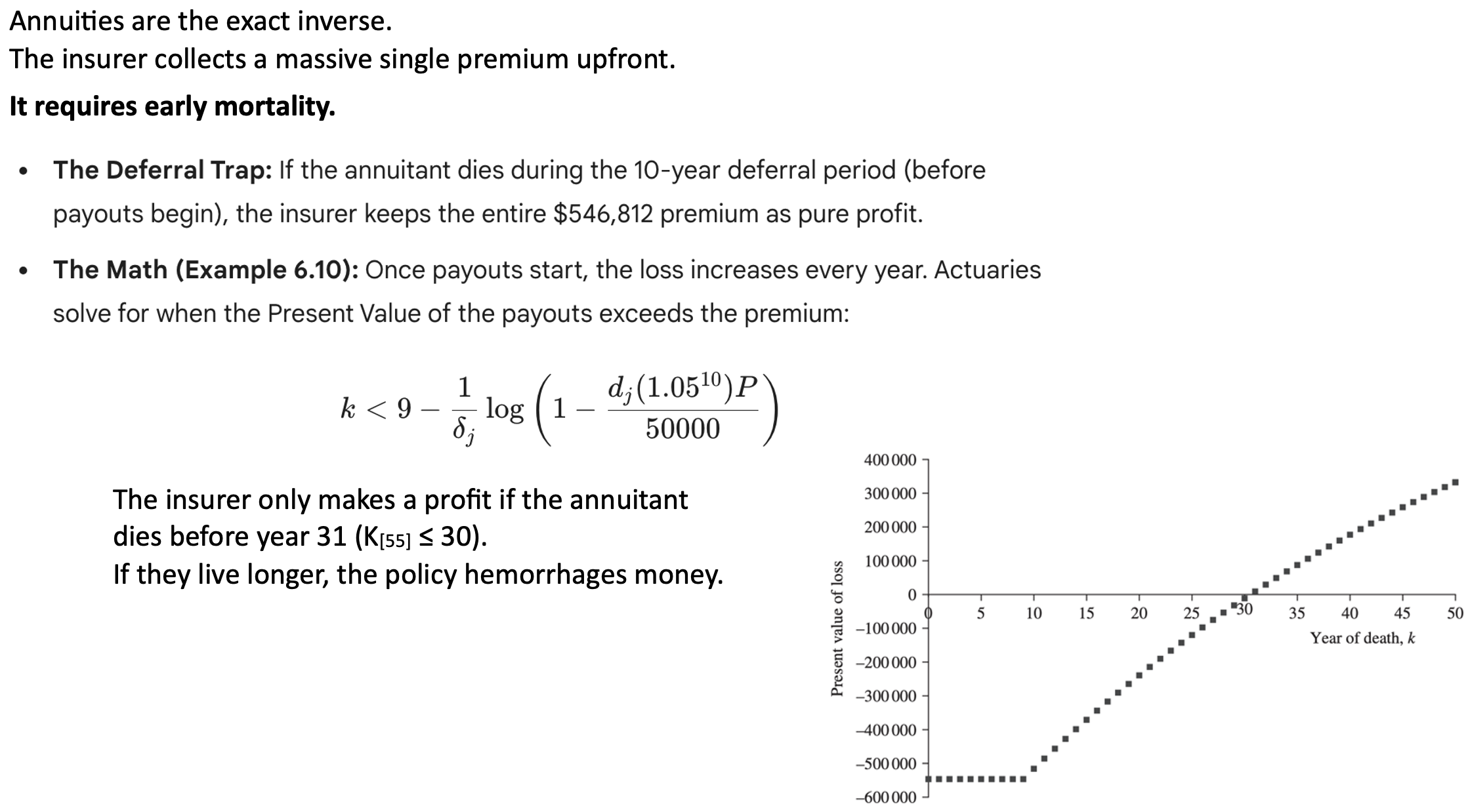

Calculating the "Tipping Point" of Profitability

Annuities

Calculating the "Tipping Point" of Profitability

Hybrid Policies: Endowment Insurance

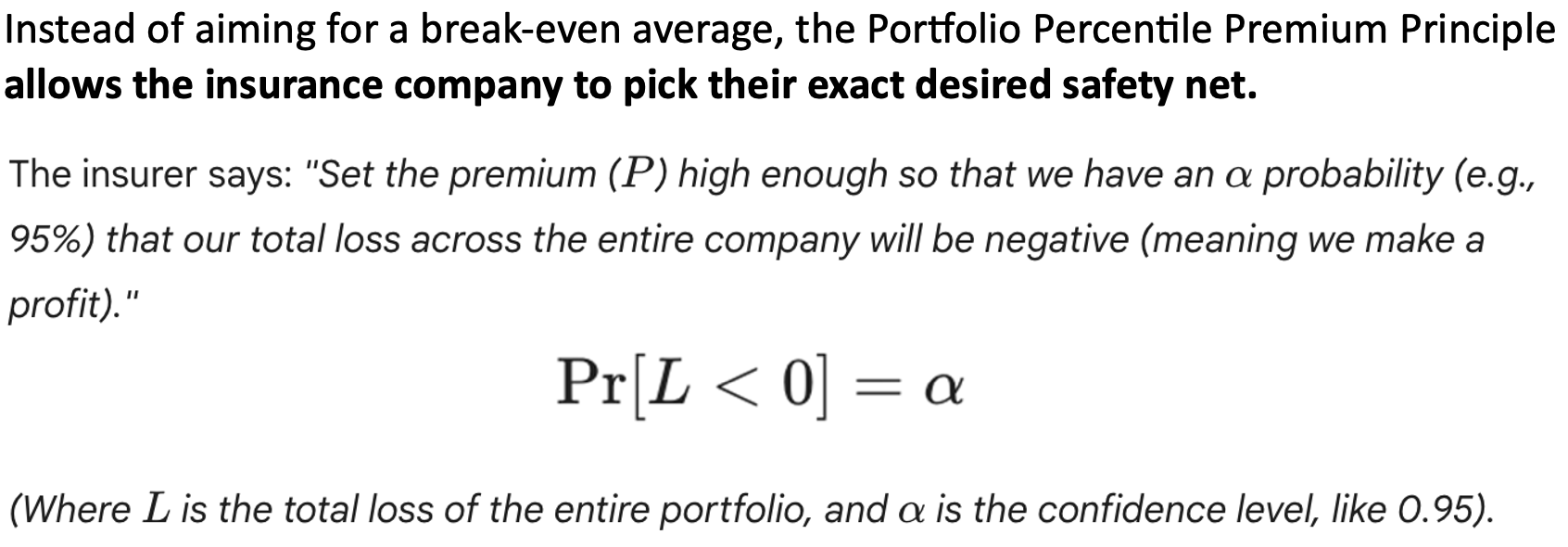

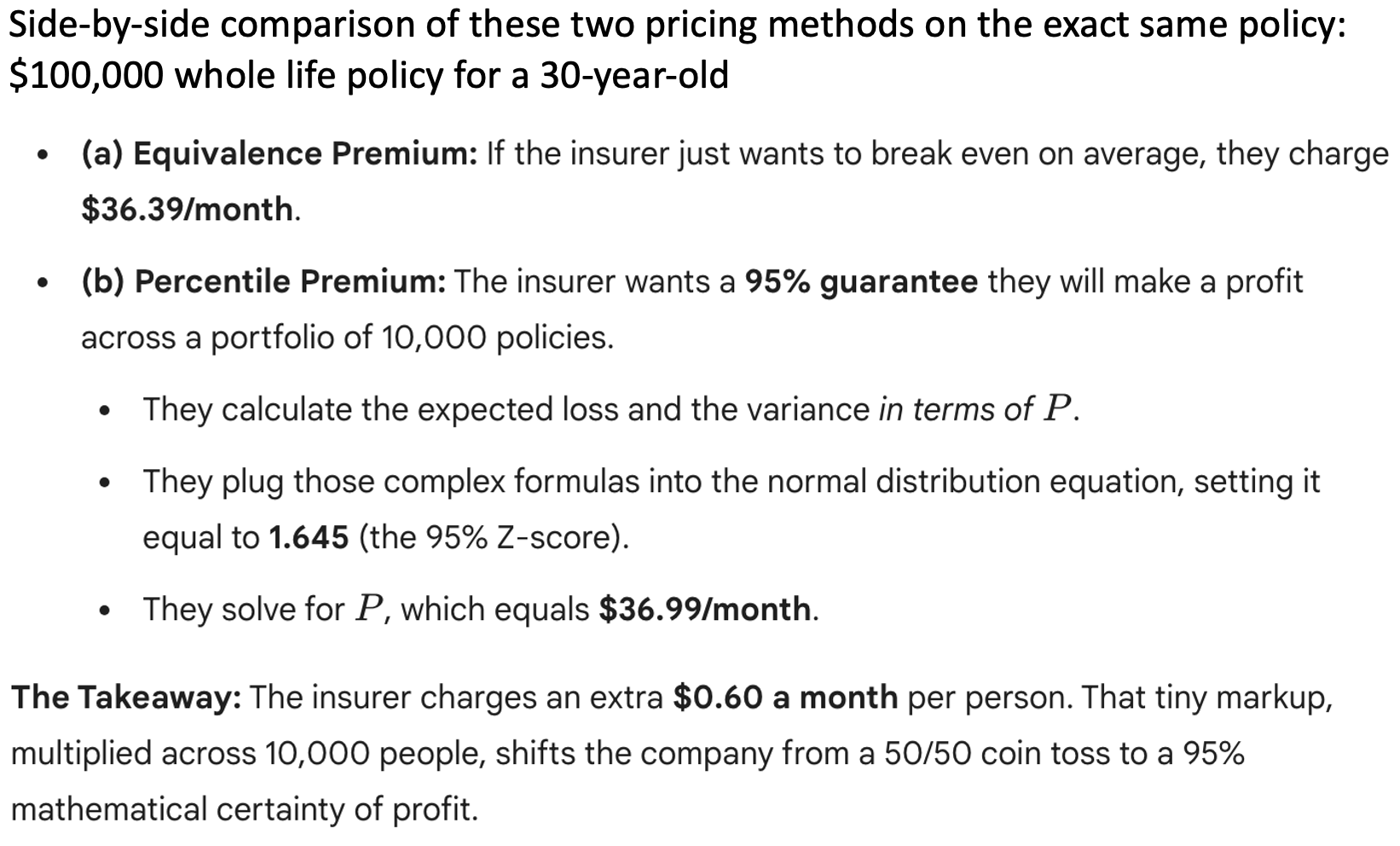

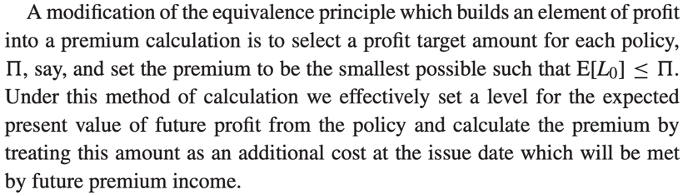

The Portfolio Percentile Premium Principle

This section answers a massive real-world flaw in the Equivalence Principle and introduces how insurers use statistics to virtually guarantee they won't go bankrupt.

The Flaw of the Equivalence Principle

The Solution: The Percentile Principle

The Percentile Principle

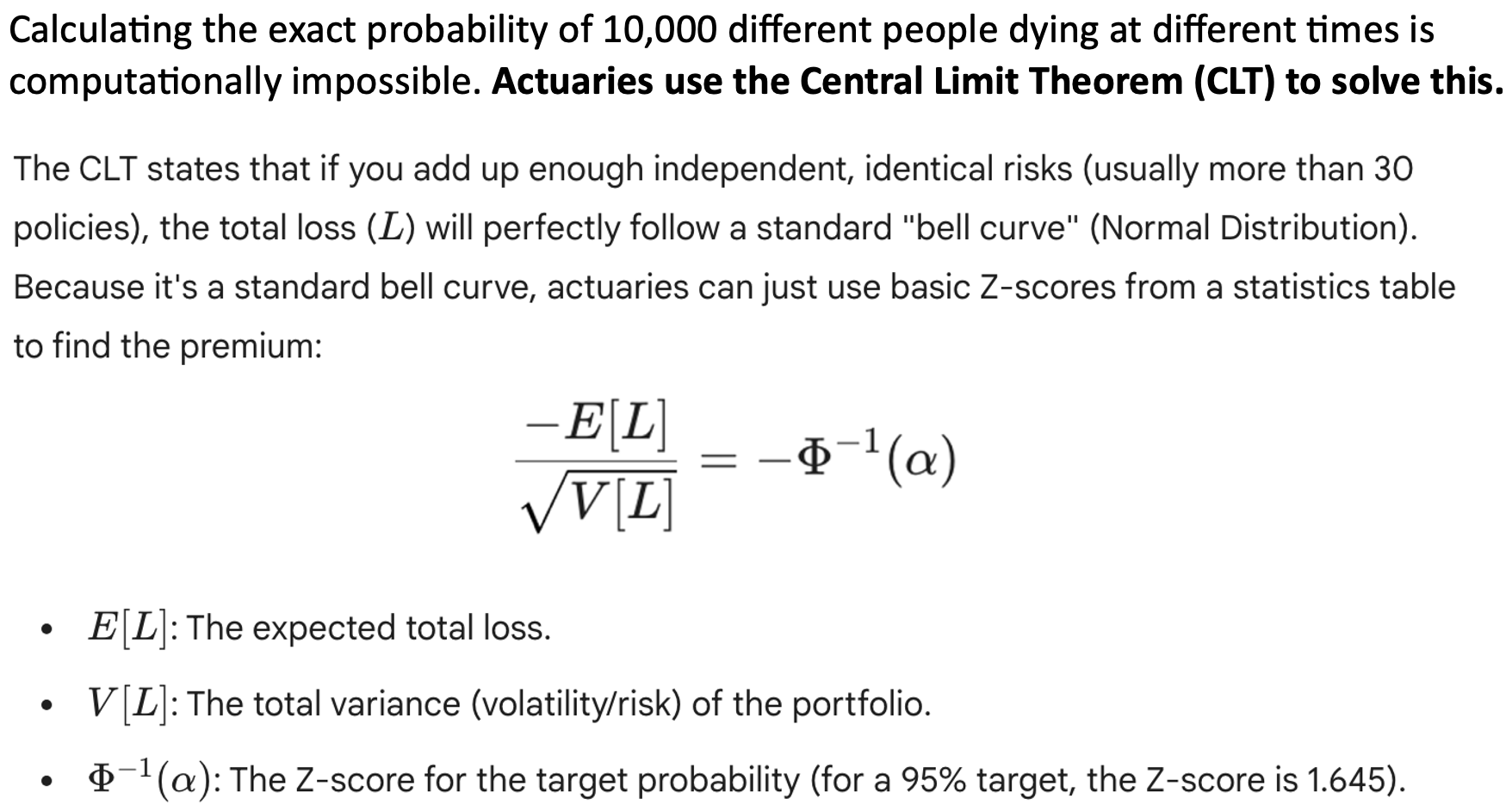

Math Shortcut

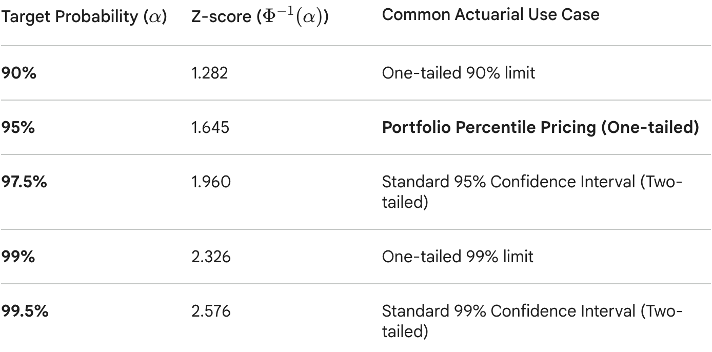

Most common Z-scores

The Percentile Principle

Example

Risk Diversification

How can actuaries deal with people who don't fit the "perfectly healthy" mold?

In the insurance world, this is known as handling substandard lives or extra risks.

Two main scenarios:

- The Underwriting Penalty (Life Insurance)

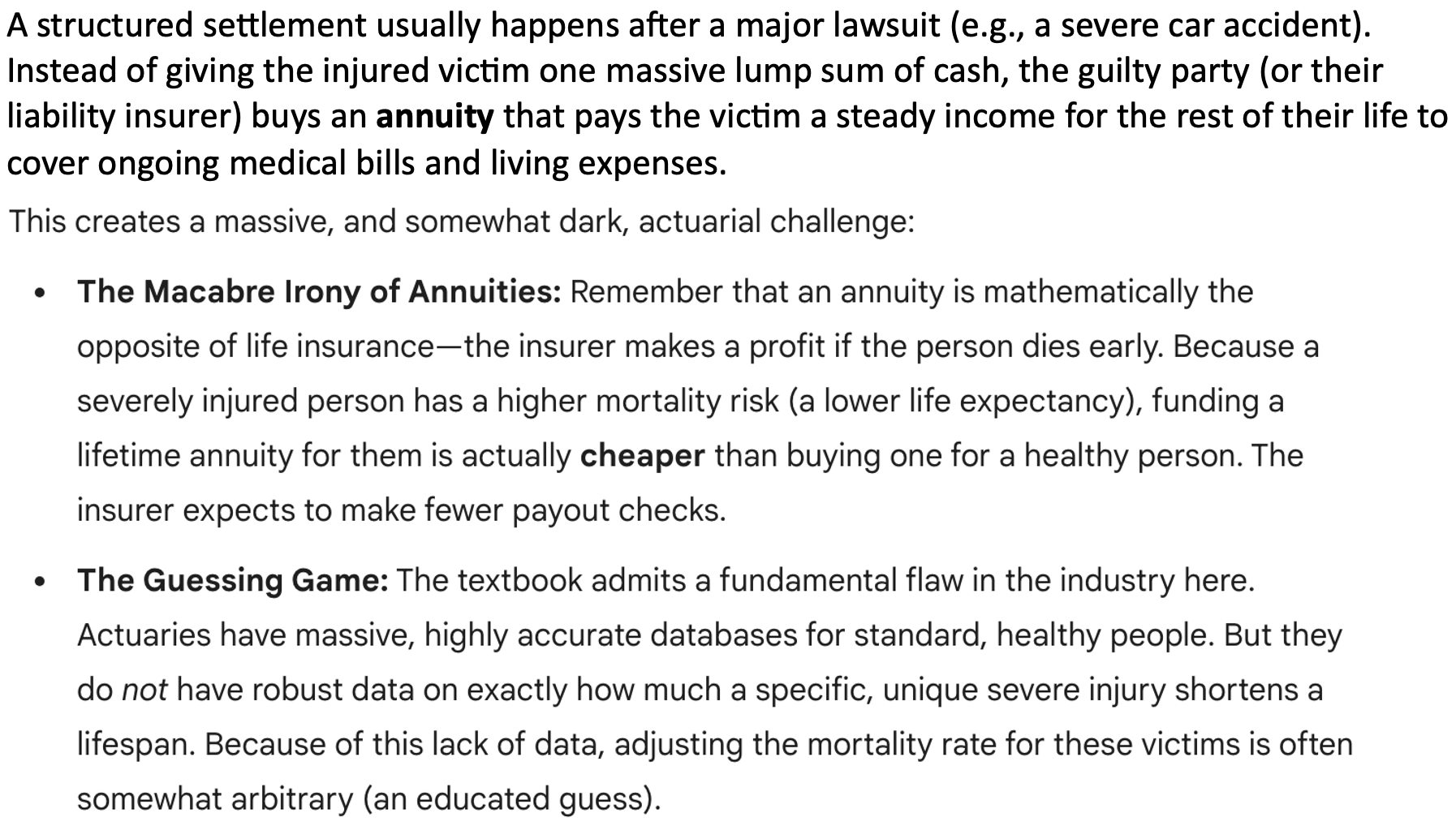

- The Structured Settlement Challenge (Annuities)

The Underwriting Penalty (Life Insurance)

The Structured Settlement Challenge (Annuities)

To model this "extra risk" in EPV calculations, one of three methods are usually used:

Extra Risk Modelling

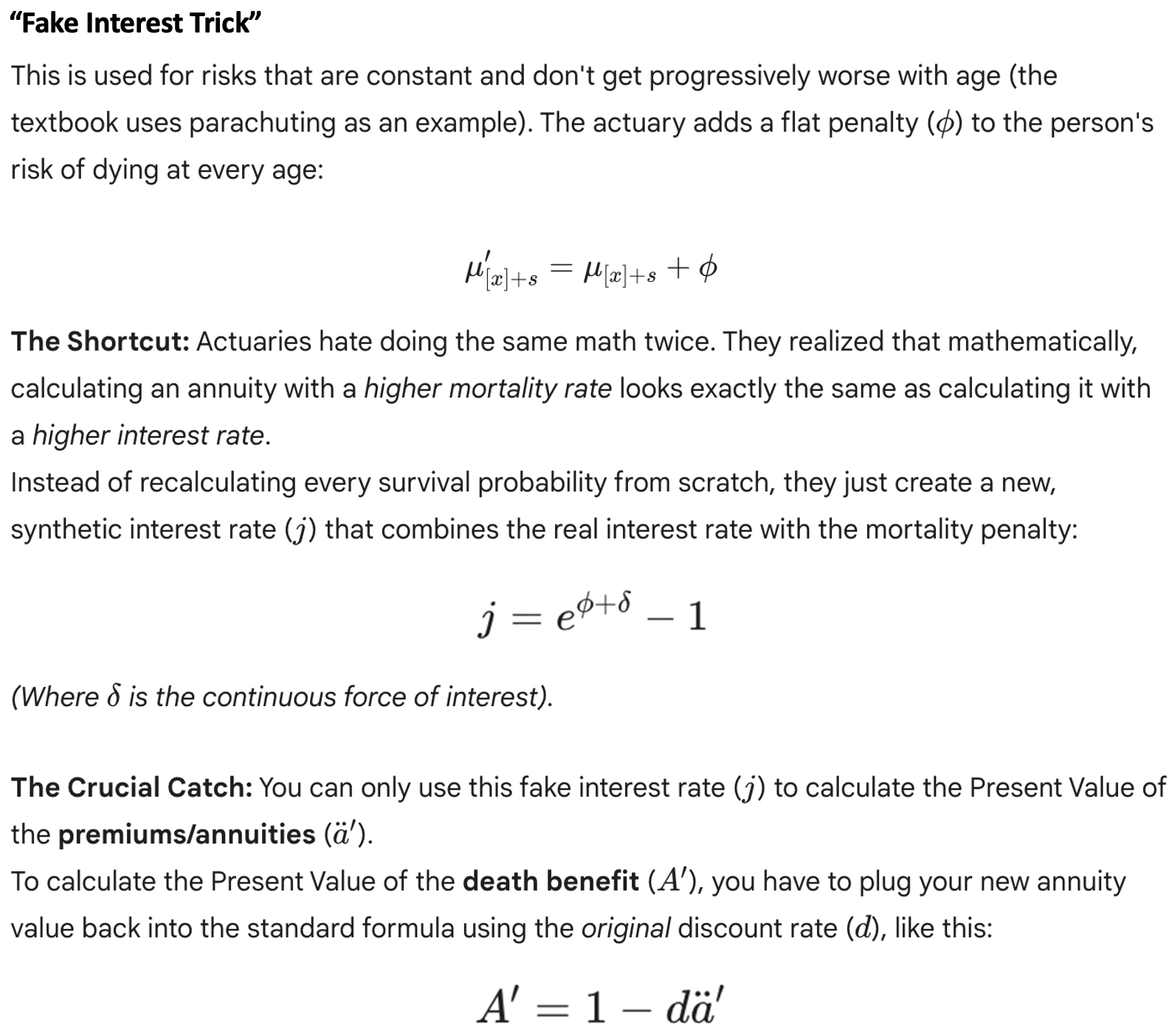

Age Rating

Extra Risk Modelling

Constant Addition

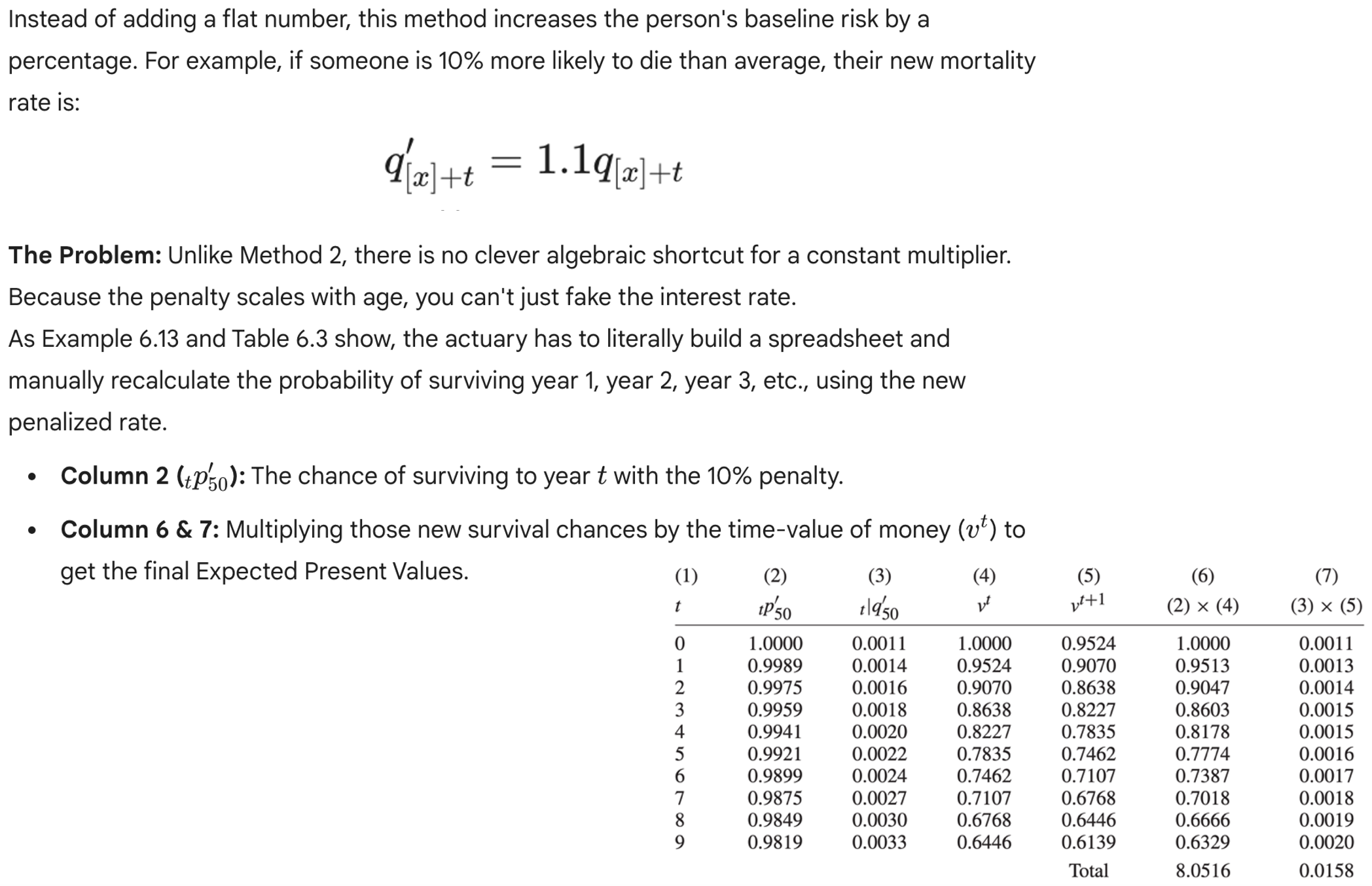

Extra Risk Modelling

Percentage Multiplier

The equivalence principle is the traditional approach to premium calculation.

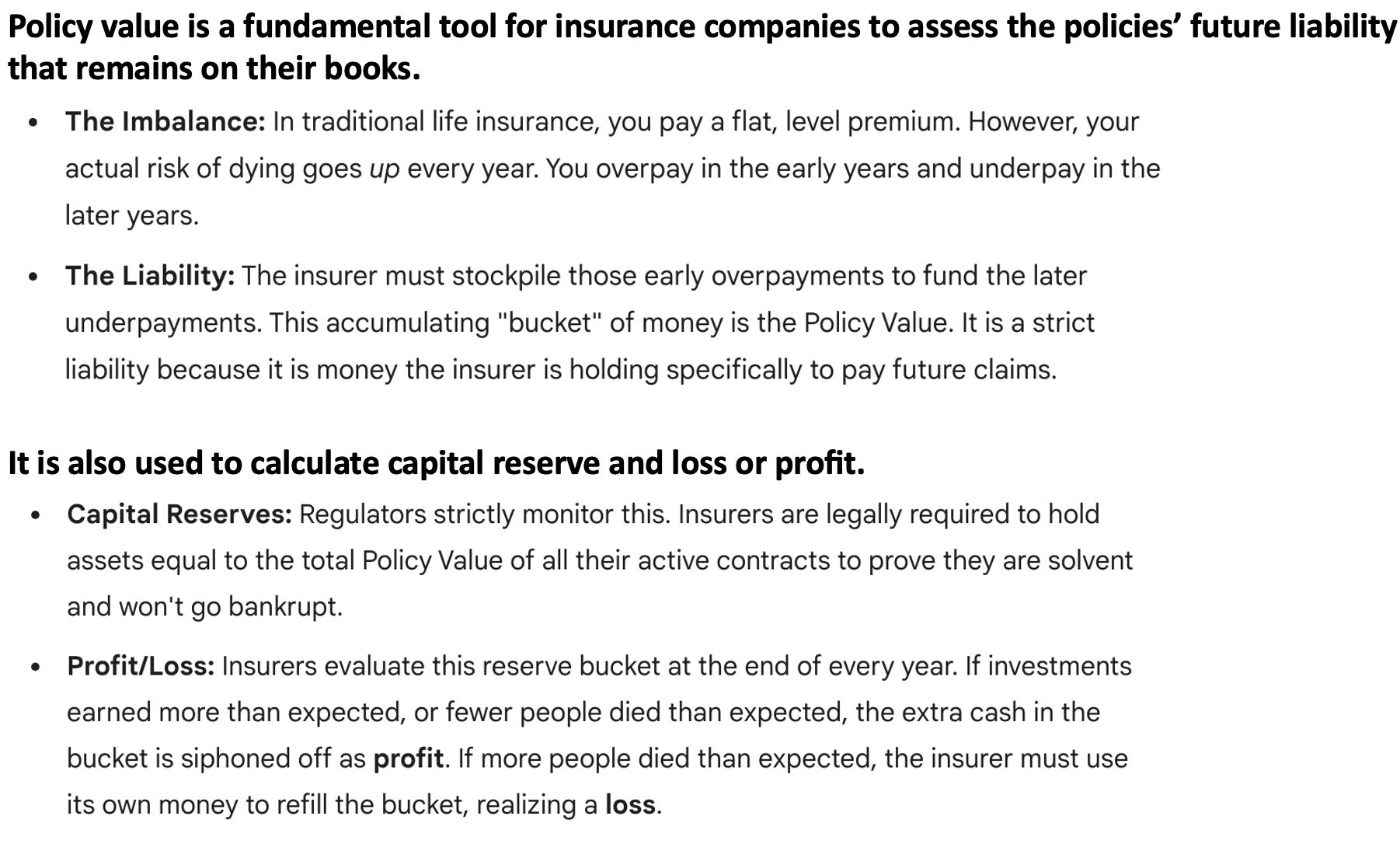

Policy value is a fundamental tool for insurance companies to assess the …

Mathematically speaking, the most important change is that we are moving away from assessing the cash flow at issue in the previous three chapters and changing our point of view to other times on the timeline.

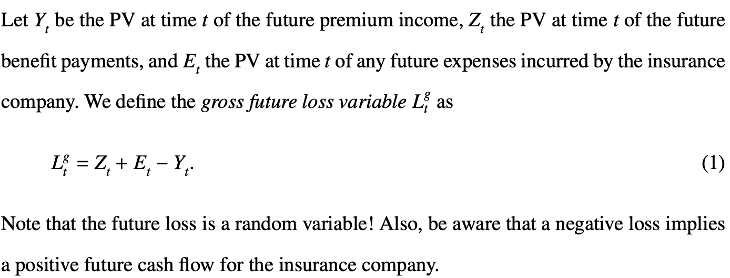

The Future Loss Random Variable

The Future Loss Random Variable

Note

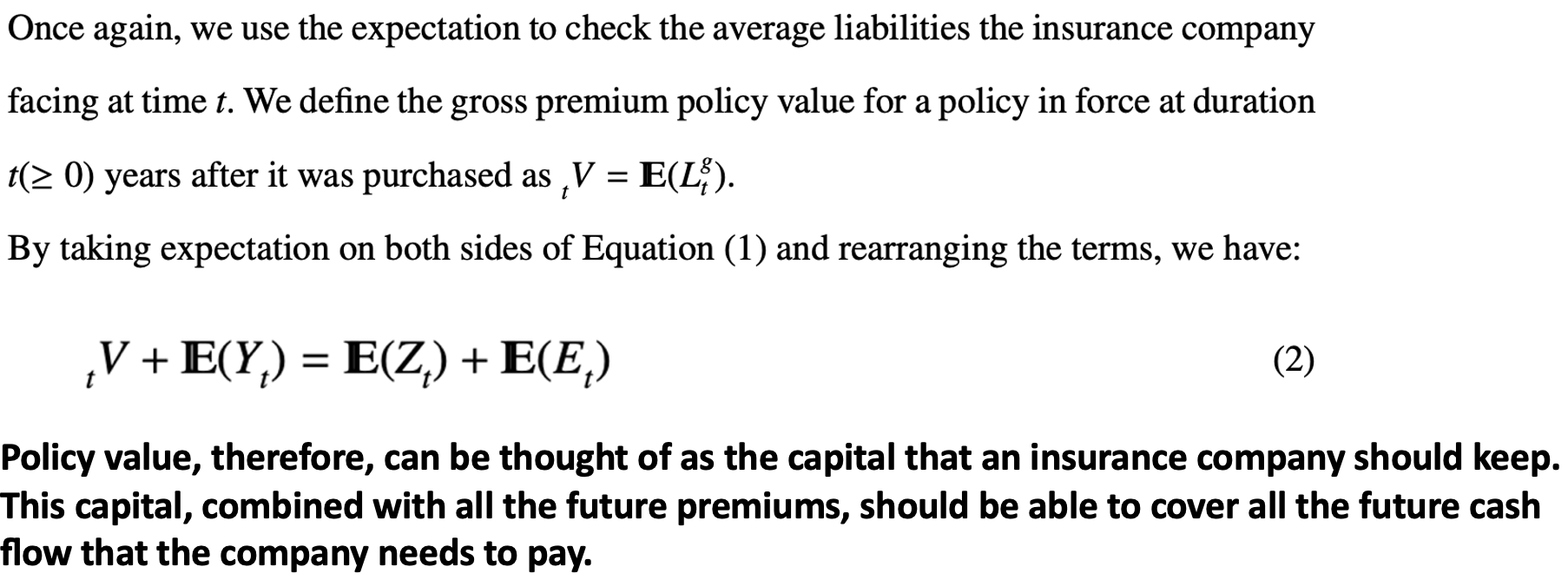

Policy Values

Instead of just saying "Liabilities - Income," the book frames it as

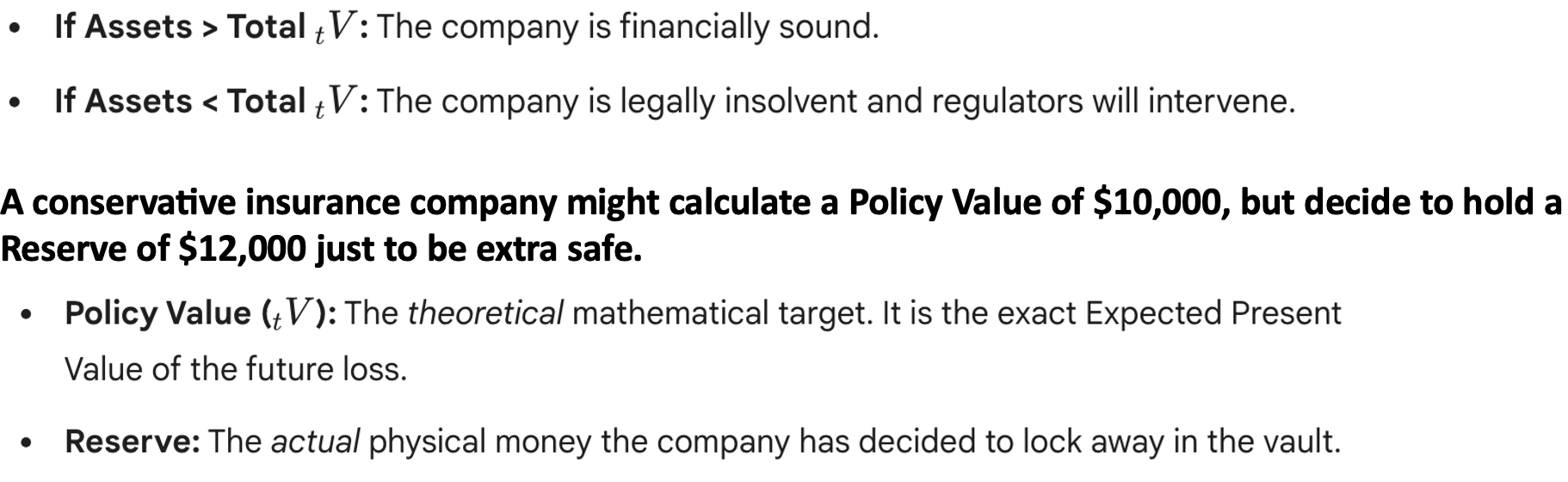

Valuation of Company

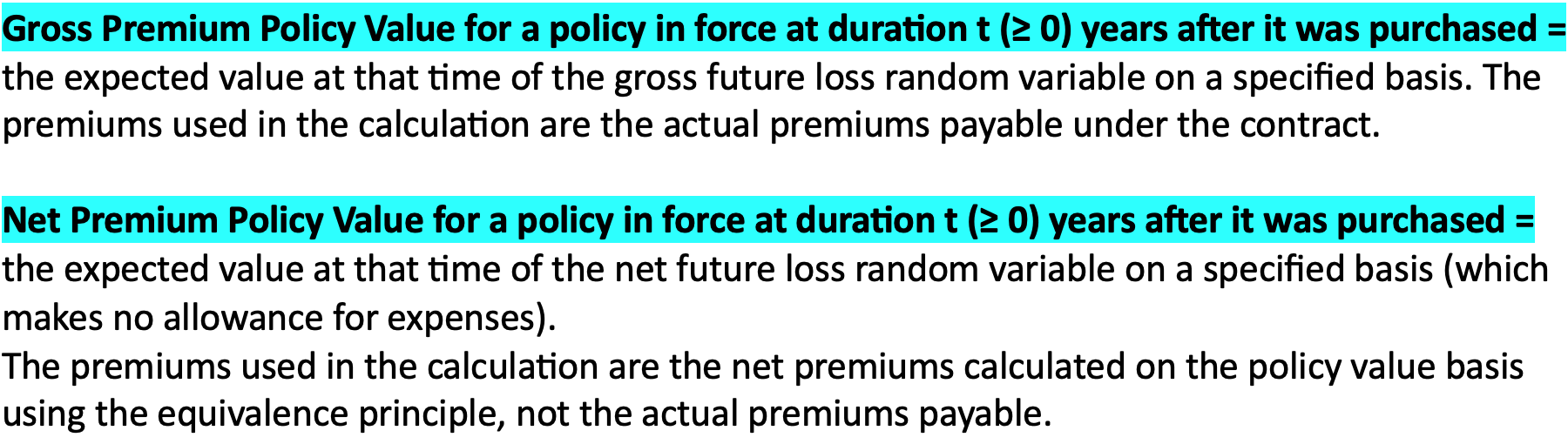

Gross and Net Premium Policy Value

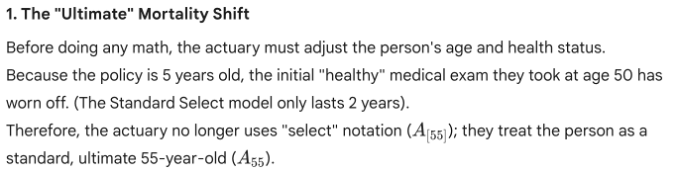

Mortality Shift

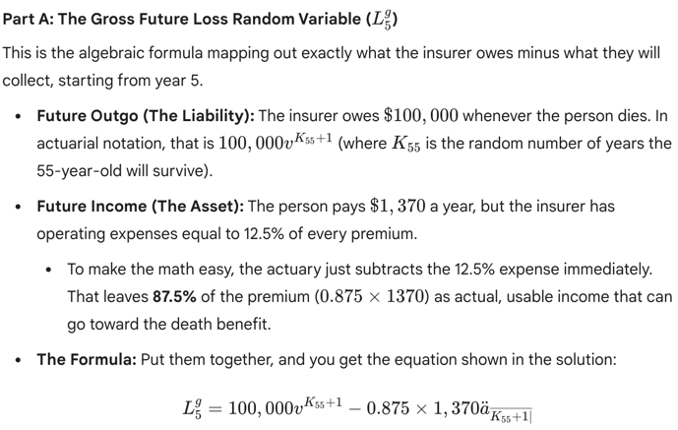

Gross Future Loss r.v.

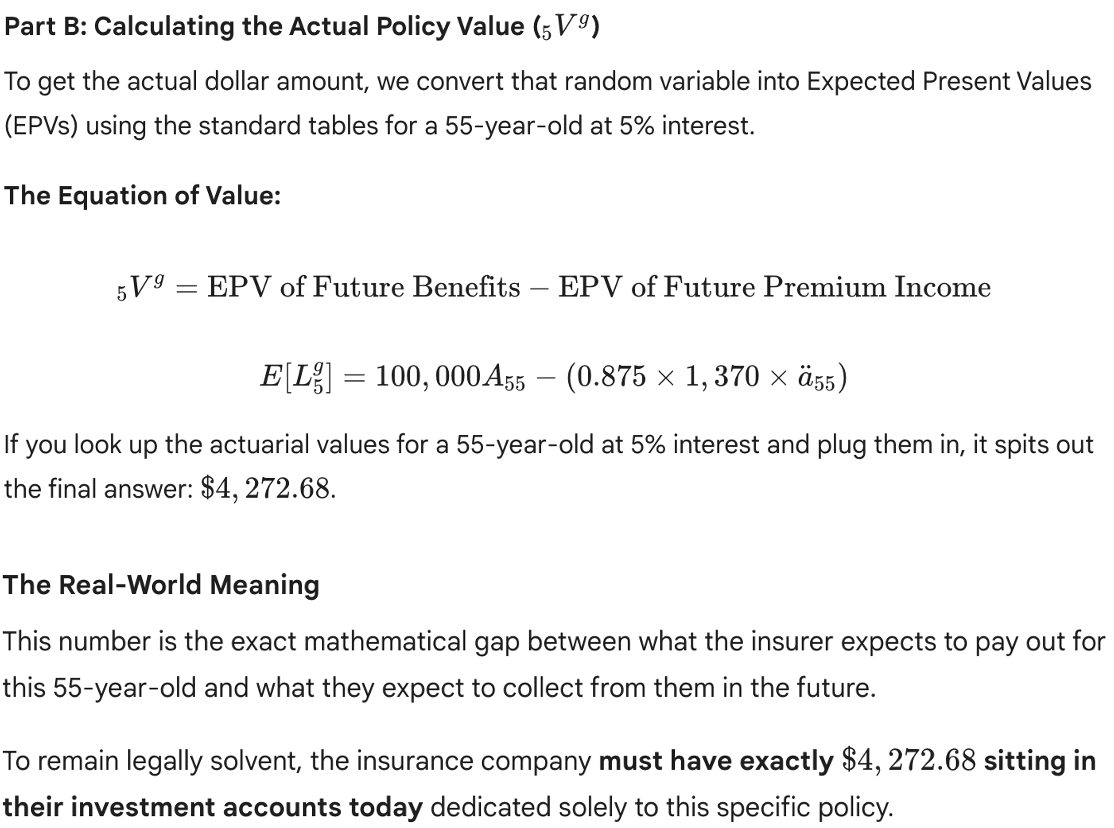

Calculating actual Policy Value