ISEN FINAL

1/118

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

119 Terms

Amortization Schedule

A record of your loan payments that shows the principal amounts and the interest included in each (equal) payment

Capital Recovery

Refers primarily to recovering initial funds put into an investment through returns from that investment, making it a break-even measure.

Caveat Emptor (Buyer Beware)

Is the principle that the buyer alone is responsible for checking the quality and suitability of goods before a purchase is made.

In Present Worth Analysis resolved alternatives

1. Equivalent Net Present Worth

2. Present Worth Cost

3. Present Worth Benefit

In Annual Cash Flow Analysis, we compare alternativesbased on:

1. Equivalent Uniform Annual Benefit (EUAB)

2. Equivalent Uniform Annual Cost (EUAC)

3. Or their difference, Equivalent Uniform Annual Worth(EUAW)

EUAW = ?

EUAB - EUAC

End-of-year convention

This makes "A" a series of end-of-period receipts or disbursements

Do Sunk Costs have bearing on decisions?

Events/expenditures that have occurred in the past do not affect what we should do in the future

Borrowed Money Viewpoint

Standard assumption is that the money needed will beobtained from a bank or firm at interest rate "i"(borrowed

Financing:

obtaining money at interest rate = borrowed frombank or firm

Investment:

spending of money considering lifecycle costs &benefits

What to do if neither input or output is fixed?

Maximize EUAW (Equivalent Uniform Annual Worth)

EUAW = EUAB − EUAC

Fixed input: amount of money or other inputs are fixed

Maximize EUAB (Equivalent Uniform Annual Benefits)

Fixed output: fixed task, benefit or other outputs

Minimize EUAC (Equivalent Uniform Annual Costs)

Infinite analysis period

Under the assumption of identical replacement, economic study is based on the alternatives' own lives

Some other analysis period

Need to estimate the terminal values for all alternatives atthe end of the analysis period

What is the most frequently used measure in industry?

ROR

Advantages of ROR

Calculating rate of return is independent from minimum attractive rate of return (MARR)

What does IRR mean?

Interest rate at which PW = 0 = EUAW

IRR on a loan?

It is interest rate paid on unpaid balance so balance = 0 after final payment.

IRR on an investment?

It is interest rate earned on the un-recovered investment so un-recovered investment = 0 after last cash flow Internal Rate of Return.

IRR

IRR is a discount rate that. makes the net present value (NPV) of all cash flows equal to zero.

What does IRR measure?

Metric used to estimate the profitability of potential investments.

Do you want IRR higher or lower?

Higher

IRR For Borrowing?

The IRR is the interest rate paid on the unpaid balance of a loan, such that the payment schedule makes the unpaid loan balance equal to 0 when the final payment is made.

IRR For Investment?

The IRR is the interest rate earned onthe unrecovered investment, such that the paymentschedule makes the unrecovered investment equal to 0 atthe end of the investment life.

Calculating Rate of Return

1. Convert various consequences of investment into acash flow

2. You can use interpolation to calculate the IRR

3. Use one of the following equations to find theunknown value of the internal rate of return (IRR)

Equations to find the unknown value of the internal rate of return (IRR)

PW of benefits - PW of costs = 0

PW of benefits/PW of costs = 1

Net Present Worth = 0

EUAW = EUAB - EUAC = 0

PW of costs = PW of benfits

What does a positive cash flow in the beginning year mean?

You are borrowing money

What does a negative cash flow in the beginning year mean?

You are investing money

Nominal interest rate

does not take into account the compounding period.

Effective interest rate

does take the compounding period into account and thus is a more accurate measure of interest charges.

Discount Rate (Hurdle Rate)

The discount rate is the interestrate used to calculate the presentvalue of future cash flows from aproject or investment.

If IRR >= MARR

Choose the higher-cost alternative

If IRR <= MARR

Choose the lower-cost alternative

What does incremental analysis focus on?

Focuses on thedifferences between two or more courses ofaction.

What is incremental analysis used for?

to decide whether to accept additional business, make or buy products, sell or process products further, eliminate a product or service, and decide how to allocate resources.

Why do we have inconsistent in rankings?

We have two different reinvestment assumptions.

Interpretation of ROR and MARR?

If the ROR of the incremental cash flowequals or exceeds the MARR, thealternative associated with the extrainvestment should be selected.

Simple Investments:

A cash flow diagram withonly one down arrow at time = 0, and the rest of the arrows need to go up. Theypositive arrows don't necessarily have to be an annuity.

What does Mutually Exclusive mean?

Only one alternative may be implemented.

What is Monotonically Increasing or Decreasing?

A function is said to be monotonically increasing if its graph is only increasing with increasing values of equation.

What does ROR analysis not require?

Does not require a Minimum Attractive Rate of Return in calculation.

What does Present Worth or Annual Cash Flow Analysis require?

Require a known Minimum Attractive Rate of Return in calculation?

If MARR known

PW or equivalent annual easier than incremental IR

If MARR not known or known approximate

Graphical approach to "choice table" is often enough

Spreadsheets for intersections that define limits

Engineering Economics

Centers on the “Time Value of Money” based on interest rates and time periods, and how the value changes as time passes.

Ethics

The concept of distinguishing between right and wrong in decision making.

Integrity

The foundation for long-term career success.

Key Elements of Money

Time, Value, Interest Rate

Time Value of Money

The value of a given sum of money depends on interest rate, the amount of money and the point in time when the money is received or paid.

Discounted Cash Flow

A valuation method that estimates the value of an investment using its expected future cash flows.

4 Rules of Discounted Cash Flow

1. Money has a time value.

2. Quantities of money cannot be added or subtracted unless they occur at the same point in time.

3. To move money forward one time unit, multiply by 1 plus the discount or interest rate.

4. To move money backward one time unit, divide by 1 plus the discount or interest rate.

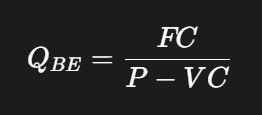

Fixed Cost

Constant, unchanging, regardless of the level of output or activity. (Property taxes, insurance, Management & administrative salaries, License fees, Rent or lease)

Variable Cost

Vary with output or activity level. (Direct labor cost - # of workers & # of hours, Direct materials)

Marginal Cost

Variable cost for producing 1 more unit. (Used as basis for last-minute pricing)

Average Cost

total cost / # units. (Basis for normal pricing)

Breakeven Point

The point where your output = to your input, or where your profit is = 0.

Sunk Cost

Money already spent due to past decision, therefore not used in decision making.

Opportunity Cost

Cost of the foregone opportunity, often hidden or implied.

Recurring Cost

Repetitive to produce similar goods & services. (Office space rental, Material cost for a product)

Non-recurring costs

Not repetitive; one time. (Purchase cost for real estate, Construction costs of the plant)

Incremental Cost

Difference in costs between two alternatives.

Cash Cost

Money from one owner to another: cash flow. (This month’s car loan payment, Money paid or received)

Book Cost

Transaction cost as recorded in an accounting book. (Depreciation cost calculated this year for an existing asset, per accounting department, Book value of your office equipment)

Life Cycle Cost

All costs over its entire life of a product, structure, system, or service.

Life Cycle Costing

Design products, projects, & services recognizing all costs & benefits over the entire life cycle.

Design Changes and Cost Impacts

Design changes implemented later in the cycle the more difficult and costly it becomes; when designers try to save money early in the design stage the result is often poor design and change orders during construction

Internal Cost

(materials, labor, overhead, etc.) used to calculate product/service cost.

External Cost

Not directly incurred by the firm and not easily predictable. (ex. Effects on wildlife & environment)

Benefits

Often more difficult to estimate than costs, optimism is common and is usually overestimated. (Sales of products, Revenues, Cost reduction from reduced material or labor costs, Reduced risk)

Cost Estimating Model (Per Unit Model)

ex. Construction cost per square foot (building), Capital cost of power plant per kW of capacity, Revenue / maintenance cost per mile (hwy).

Cost Estimating Model (Segmenting Model)

Estimate is decomposed into individual components, Estimates are made at component level, Individual estimates are aggregated back together.

Nominal Interest Rate

Also known as Annual Percentage Rate, is the annual interest rate (r) without considering the effect of any compounding.

Effective Interest Rate

The annual interest rate taking into account the effect of compounding during the year. [ i = (1+r/m)^n - 1 ]

Annuities

End-of-period cash flow.

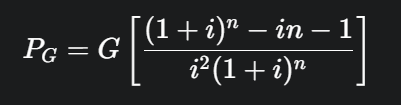

Arithmetic Gradient Repeated Cash Flow

When a cash flow is not a constant amount “A”, but is a uniformly increasing series “G”. It is expressed as (A/G, i%, n) or (G/A, i %, n).

Geometric Gradient Repeated Cash Flow

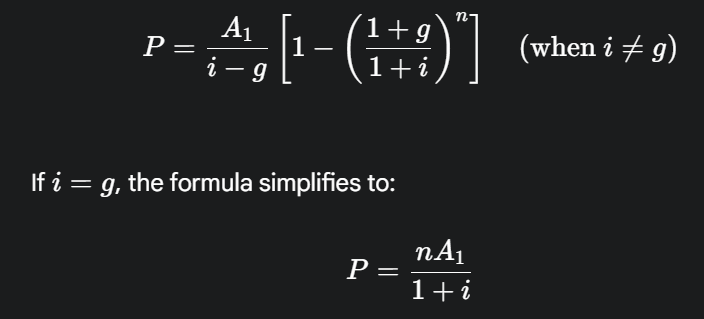

When the period to period cash flow change is a uniform rate “g” (% increase)

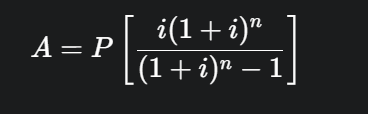

Capital Recovery Factor

Ratio used to determine the present value of a series of equal annual cash payments.

Uniform Series Sinking Fund Factor

Ratio used to determine the future value of a series of equal annual cash payments.

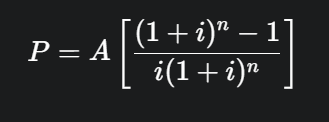

Present and Future Money

F = P(1+i)^n

Benefit Cost Ratio (BCR)

A method to evaluate the financial viability of a project by comparing the present value of projected benefits to the present value of associated costs. It is used to determine if a project delivers a positive net present value to a firm and its investors. It is also used to compare alternatives.

Payback Period

The time required for a project's profit and benefits to equal the project's cost. It is used as an approximate economic analysis method (though it ignores the time value of money and cash flows after payback). It is commonly used by start-up enterprises short of capital or to communicate financial information when other measures might cause confusion.

Depreciation

The decline in an asset's market value due to deterioration or obsolescence, or the decline in value to the owner. It is the systematic allocation of an asset's cost over its depreciable life. The purpose is to reduce taxable income; depreciation charges are business costs that are written off over time, reducing income taxes.

Straight-Line Method

What was used before declining balance?

Depreciable Assets

These are capital assets used for business purposes to produce income with a useful life longer than one year.

They lose value gradually over time (wear out, decay, become obsolete).

Examples include buildings, plants, machines, and vehicles.

Deductible (Expensed) Items

These are expenses consumed over a short period (less than one year) and are part of regular business operations.

They are subtracted from business revenues (written off) immediately as they occur.

Examples include labor, utilities, materials, and insurance.

MACRS

What does not take salvage value into consideration?

Straight-Line (SL)

Sum-of-the-Years'-Digits (SOYD)

Declining Balance (Classic)

MACRS (GDS)

U.S. Corporate Tax Rate

21%

Tax Cuts & Jobs Act of December 2017(effective 2018)

When was the corporate tax rate established?

One Big Beautiful Bill Act of July 2025

When was the corporate tax rate made permanent?

Cost Basis (B)

The dollar amount being depreciated, including the asset's purchase price and any costs necessary to make the asset ready for use.

Capitalized Costs/Expenditures

These are expenses added to the cost basis of an asset (rather than expensed immediately). They are recovered over a period of time via depreciation or amortization. Examples include fees and charges to obtain and place the asset in service.

Taxable Income Formula

Taxable Income = Gross Income - All expenditures (except capital expenditures) - Depreciation & Depletion charges

Generally Accepted Accounting Principles (GAAP)

A common set of accounting rules, standards, and procedures issued by the Financial Accounting Standards Board (FASB). Public companies in the U.S. must follow this when compiling their financial statements. Allows four methods for valuation: Straight-line, Declining Balance, Units of Production, and Sum-of-Years' Digits.

Tangible Property

Property that can be seen, touched, and felt. It includes Real property (land, buildings) and Personal property (equipment, vehicles). Tangible property (except land and inventory) is depreciated

Intangible Property

Property that has value but cannot be directly seen or touched, such as patents, copyrights, and goodwill. Intangible property can generally be depreciated (amortized).

Expensed Assets

Items that are not property (capital assets) but are operating expenses (labor, materials) are expensed.

Book Value (Valuation)

The remaining cost of a product after depreciation.

Book Value Formula

BVt = Cost Basis (B) - (Sum of depreciation charges made to date)