Economics

The study of how “households” make decisions when facing scarce resources (NOT the study of money)

Principles of economics

People face trade-offs

Opportunity cost (what you give up to get something else)

Rational people think at the margins

People respond to incentives

Equality vs. Efficiency

Equality- focuses on equal distribution of resources (more liberal view)

Efficiency- focuses on what works best for society as a whole (more conservative view)

Thinking like an economist

Putting yourself in the person’s shoes, thinking logically, and imagining what they would do

Trade

Works best when countries specialize in producing goods in which they have the comparative advantage (makes everyone better off)

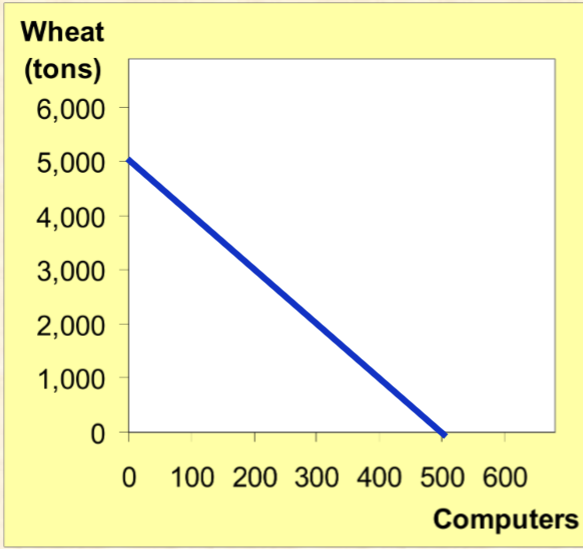

Production possibilities frontier

Depicts the most efficient production of goods/services for a country

Absolute advantage

Ability to produce a good using fewer inputs than another country

Ex- Chinese worker can produce 4 shirts or 1 computer in a day. US worker can product 3 shirts or 2 computers in a day.

Shirt AA- China

Computer AA- USA

Comparative advantage

Ability to produce a good at a lower OPPORTUNITY COST than another country

Ex- Chinese worker can produce 4 shirts or 1 computer in a day. US worker can produce 3 shirts or 2 computers in a day.

Shirt CA- China (S=1/4C)

Computer CA- USA (C=1.5S)

Terms of trade

In order for trade to be beneficial for both countries, they must trade…

what they have the comparative advantage in

trade in between their opportunity costs

Ex- Chinese worker can produce 4 shirts or 1 computer in a day. US worker can produce 3 shirts or 2 computers in a day.

Chinese CA- C=4S

USA CA- C=1.5S

Best trade would be… C=(1.5 , 4)S —> C= 2 2/3 S

Competitive market

A market with many buyers/sellers who have negligible control over price (ex- car dealerships)

Perfectly competitive market

All goods are exactly the same, so many buyers/sellers that none have an effect on market price (price takers) (ex- fast food hamburgers)

Demand

Relationship between price and quantity demanded

Quantity demanded

The amount of a good that buyers are willing/able to purchase

Law of demand

Claims that as quantity demanded falls, price rises

Demand curve shifters

Number of buyers (buyer increase=QD increase)

Income levels (income decrease= QD decrease)

Price of related goods (increase= QD increase)

Tastes (preference increase= QD increase)

NOT PRICE!! (That moves ALONG the demand curve)

Normal good

A good is a “normal good” if it’s positively related to income (quantity demanded increases after income increases)

Ex- Luxury handbags

Inferior good

Negatively related to income (quantity demanded goes down after income increases)

Ex- ramen packets (cheap and gross)

Substitute goods

If price increases for one good, demand increases for the other

Ex- hot dogs and hamburgers (if hot dog prices increase, demand for hamburgers will increase instead)

Complement goods

If price increases for one good, demand decreases for the other

Ex.- bagels and cream cheese (if bagel price increases, cream cheese demand decreases)

Supply

Relationship between price and quantity supplied

Quantity supplied

The amount of a good that sellers are willing/able to sell

Law of supply

As quantity supplied increases, price increases too

Supply curve shifters

Input prices (if input prices decrease, supply will increase)

Technology (as technology improves, supply increases)

Number of sellers (as sellers increase, supply increases)

NOT PRICE (moves ALONG supply curve)

Equilibrium

Reached when price of quantity supplied and quantity demanded are equal

Surplus vs shortage

Surplus- when quantity supplied is greater than quantity demanded (price will decrease)

Shortage- when quantity supplied is less than quantity demanded (price will increase)

Adam Smith’s invisible hand

Equilibrium will naturally be reached when we allow the market to function naturally

Reaching equilibrium after shock (3 steps)

Decide if quantity supply or demand (or both) were affected

Decide what direction it shifted (left=less, right=more)

Use diagram to show the equilibrium shift