Microeconomics

1/36

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

37 Terms

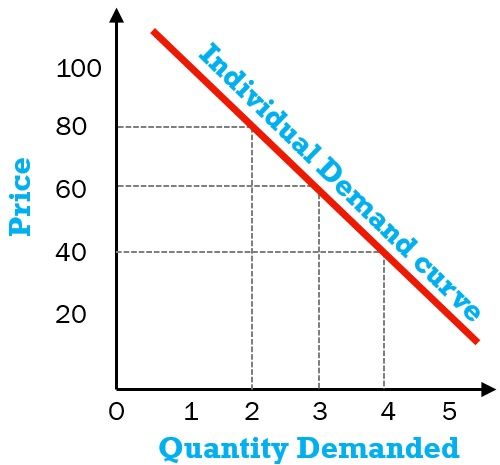

Individual Demand curve

graph plotting the quantity of an item that some plans to buy at each price

Interdependence principle

concept that individuals, businesses, and nations rely on one another to produce and consumer goods and services

Law of demand

tendency for quantity demanded to be higher when price is lower

Marginal principle

rule for making decisions by comparing extra benefit (marginal benefit) of one or more units of something against the extra cost (marginal cost) of the same unit

marginal benefit

the additional benefit arising from a unit increase in a particular activity.

marginal cost

the cost added by producing one additional unit of a product or service.

cost-benefit principle

action should only be taken if benefit ≥ cost

,

opportunity cost principle

tru cost of a decision is value of next best alternative

rational rule for buyers

buy more of an item if the marginal benefit is ≥ cost

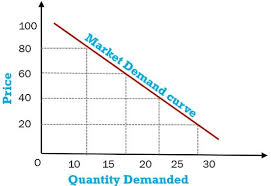

market demand curve

graph plotting the total quantity of an item demanded by the entire market, at each price

factors that shift demand curves

Income

Preferences

Expectations

Price of related goods

Congestion and network affects

Typer and number of buyers

Normal good

product for which demand increases when consumer income rises

Inferior good

good which income decrease in demand- something you stop buying when you earn more money EX instant noodles

Complementary good

goods that go together. demand for a good will increase if price of complementary good inceases

substitute good

goods that replace each other. demand for a good will increase if a price of a substitute good rises, and fall is substitute falls

Network effects

good becomes more useful because other people are using it

Congestion effect

good becomes less valuable because of other people using it

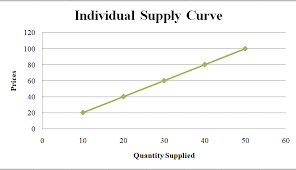

Individual supply curve

graph plotting the quantity of an item that a business plans to sell at each price

Law of supply

tendency for the quantity supplied to be higher when price is higher

Perfect competition

markets in which all firms in an industry sell an identical good

there are many buyers and sellers, each of who are small relative to the size of the market

Price takers

someone who decides to charge the prevailing price and whose actions do not affect the prevailing price → follow market price

Variable costs

those costs-labor and raw materials- that vary with the quantity of output you produce

fixed costs

those costs that don”t vary when you change the quantity of output you produce

Rational rule for sellers in competitive markets

sell one more unit if the price is ≥ the marginal costs

marginal product

the increase in output that arises from an addition unit of input example : labor

Diminishing marginal product

an economic principle where adding more of one input (like labor) to a fixed input (like a factory) eventually leads to smaller increases in total output, eventually falling

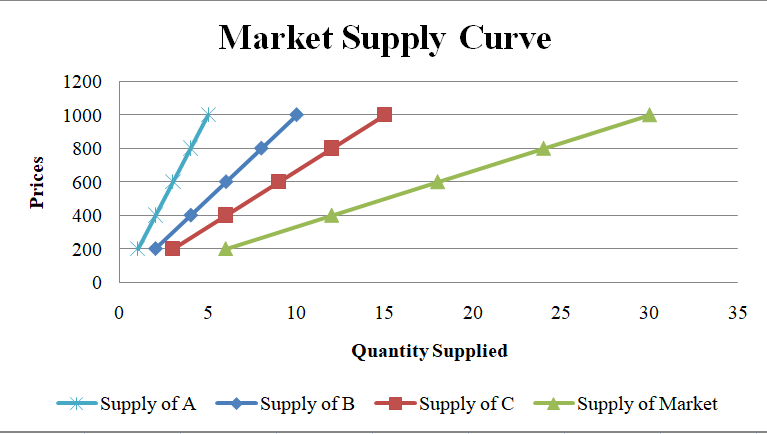

market supply curve

graph plotting the total quantity of an item supplied by the entire market at each price

substitute- in -production

alternative use of your resources. your supply of a good will decrease if the price of substitute- in -production increases ex: gas and diesel

complements- in- production

goods that are made together. your supply of a good will increase if complements- in- production rises

Price elasticity demand

measure of how responsive buyers are to price changes. measures the percent change in quantity demanded that follows from a 1% price change

Inelastic demand

buyers are not responsive to price. quantity demand rises very little

Elastic demand

buyers are responsive to the price. quantity demand increases a lot

price elasticity of supply

measure of how responsive sellers are to price changes. measure percent change in quantity supplied that follows a 1% in price change

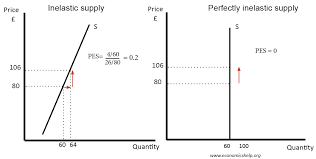

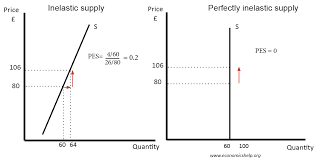

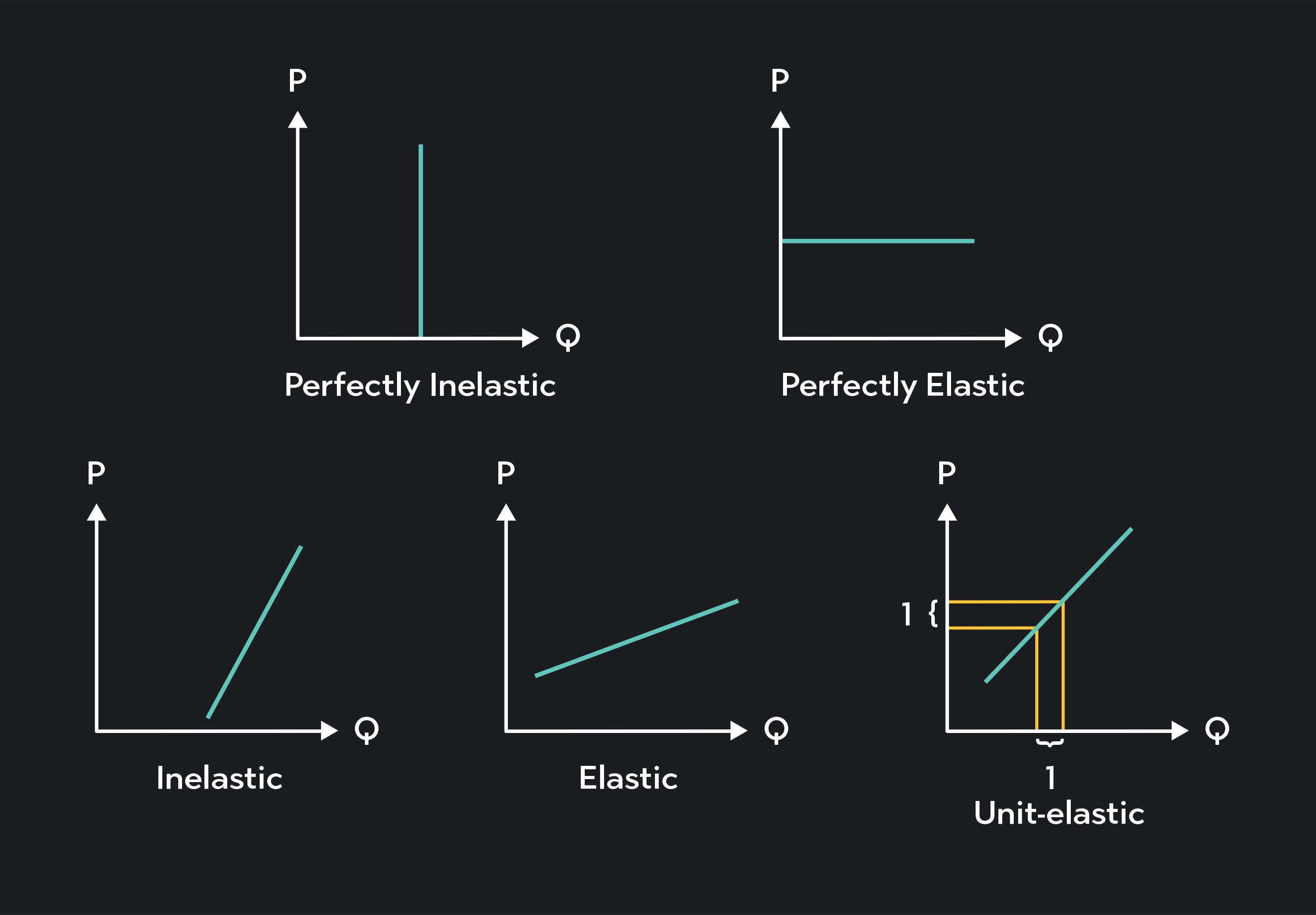

Perfectly inelastic supply

the quantity supplied of a good or service doesn't change, no matter the price, resulting in a vertical supply curve, where sellers are completely unresponsive to price changes

Inelastic supply

occurs when the quantity of a good or service supplied changes very little in response to price fluctuations

elastic supply

quantity supplied of a good or service is highly responsive to price changes

Perfectly elastic supply

an extreme case where the supply curve is a horizontal line, indicating that suppliers are willing to sell any quantity at the prevailing market price.