Ch. 8 Efficient Market Hypothesis

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

29 Terms

Random Walk

•Notion that stock price changes are random

pattern on the market where if people were rational there will always be patterns, but because scientists didn’t find any patterns this means it was a “random” generation

Efficient Markey Hypothesis (EMH)

•Prices of securities fully reflect available information

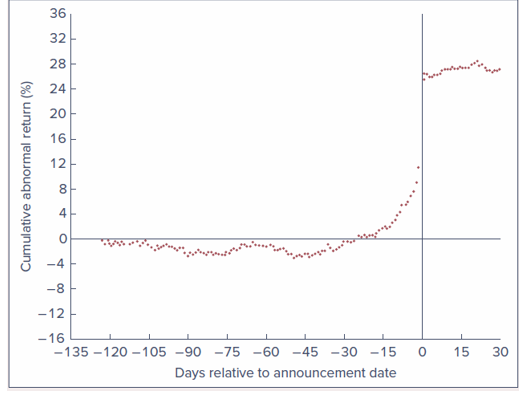

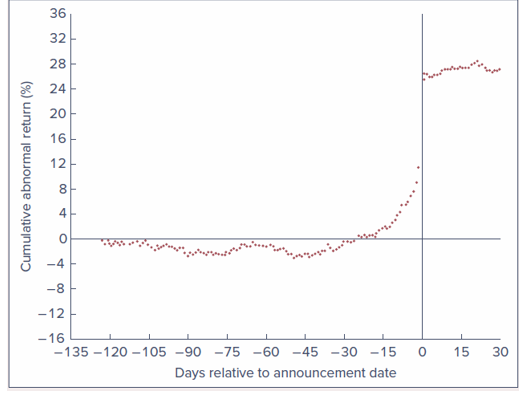

Cumulative Abnormal Returns before Takeover

target company of a takeover

becomes buyout target if the company isn’t doing well

prices will go up due to 3 assumptions

3 takeover assumptions

immediate day of affect (people react quickly to the market)

when prices rise (increase), the price stays put (indicates initial reaction is fast and accurate)

price before the announcement goes up = insider trading, assumption that people have a leverage over public info

ties into image

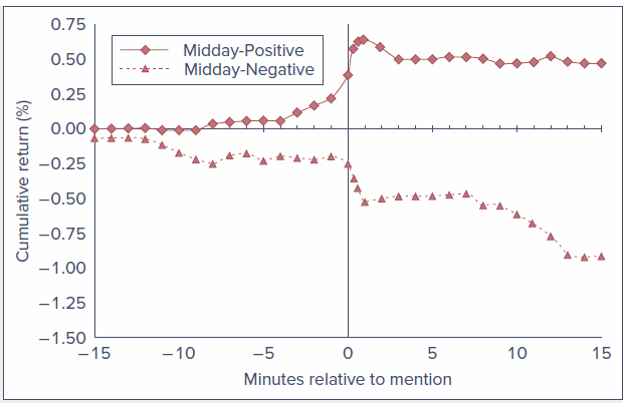

Stock Price Reaction

news announcements will come with recommendations

positive reports = quick reaction, there will be slight overreaction

negative reports = drifts initial reaction and will have slight underreaction

market reacts relatively quickly on the daily level of news

Competition as source of efficiency

•Investor competition should imply stock prices reflect available information

•Investors exploit available profit opportunities

•Competitive advantage can verge on insider trading

assumption that more people will passively invest when market is efficient, causing market to become less efficient, then balance out as people will start to actively invest

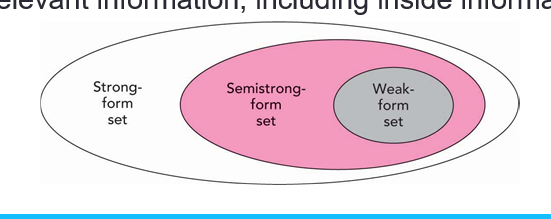

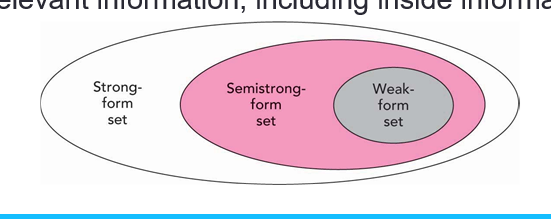

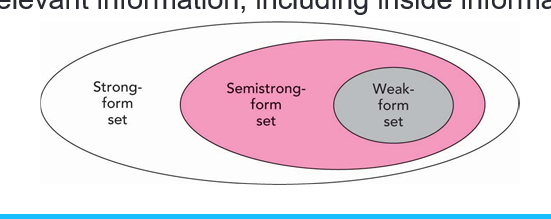

Weak-form EMH

Stock prices already reflect all information contained in history of trading

least efficient

prices already reflected in the historical data

means no advantage

Semistrong-form EMH

Stock prices already reflect all public information

trading data is available to the public

the market is relatively efficient

often means you cannot get a lead on investing

Strong-form EMH

Stock prices already reflect all relevant information, including inside information

market price = private + public information'

Technical Analysis

Research on recurrent/predictable price patterns and on proxies for buy/sell pressure in market

•Resistance Level

Unlikely for stock/index to rise above

•Support Level

Unlikely for stock/index to fall below: stock won’t drop below the lowest stock price recorded

uses historical prices and data

not commonly taught in school

gain an advantage is hard when only using historical data

Fundamental Analysis

•Research on determinants of stock value:

•Earnings, dividend prospects, future interest rate expectations and firm risk

•Assumes stock price equal to discounted value of expected future cash flow

uses financial statements and other public information

commonly taught in school

Passive investment strategy (vs active)

•Buying well-diversified portfolio without attempting to find mispriced securities

Index fund

•Mutual fund which holds shares in proportion to market index representation

Portfolio Management in Efficient Market

•Active management assumes market inefficiency

•Passive management consistent with semistrong efficiency

•Even if the market is efficient, a role exists for portfolio management: Diversification; Tax considerations; Risk profile of investor

•Inefficient market pricing leads to inefficient resource allocation

skipped over

Market Efficiency Issues

Magnitude issue: Efficiency is relative, not binary

•Selection bias issue

•Investors who find successful investment schemes are less inclined to share findings

•Observable outcomes preselected in favor of failed attempts’

•Lucky event issue: Lucky investments receive disproportionate attention

Weak Form Efficiency Tests

• Patterns in Stock Returns

•Returns over short horizons

•Momentum effect: Tendency of poorly- or well-performing stocks to continue abnormal performance in following periods

stocks perform in the short term, reversal effect in the long term

if price goes up in short term, then it’s likely to drop in long term

•Returns over long horizons

•Reversal effect: Tendency of poorly- or well-performing stocks to experience reversals in following periods

Tests indicate if market is efficient, may not be useful though due to transaction costs

Broad Market Performance

Predictors

•1988—Fama and French: Return on aggregate stock market tends to be higher when dividend yield is high

•1988—Campbell and Shiller: Earnings yield can predict market returns

•1986—Keim and Stambaugh: Bond market data (spread between yields) can predict market returns

skimmed in class

Semistrong Form efficiency tests

•Anomalies

•Patterns of returns contradicting EMH

•P/E effect: lower ratio = more valuable stock, firm w/ lower P/E = paying less for equal or better earnings

•Portfolios of low P/E stocks exhibit higher average risk-adjusted returns than high P/E stocks

looking at public data patterns

patterns = anomalies

Semistrong Tests: Market Anomalies

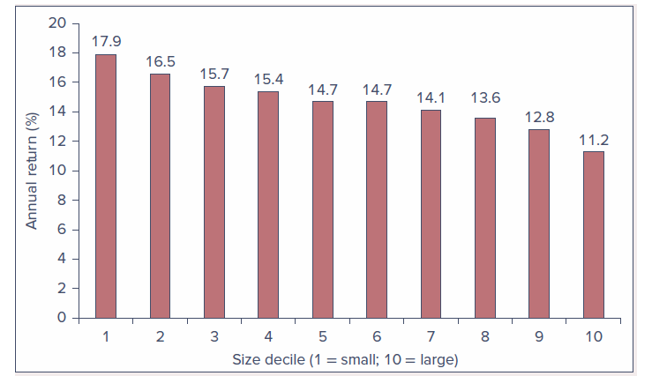

•Small-firm effect

•Stocks of small firms can earn abnormal returns, primarily in January

higher return due to more risk

tied to fama french rule 3

•Neglected-firm effect

•Stock of little-known firms can generate abnormal returns

also may have advantage similar to small firm affect

•Book-to-market effect

•Shares of high book-to-market firms can generate abnormal returns

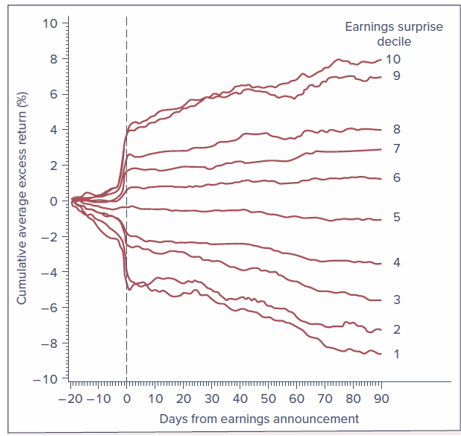

•Post-earnings announcement price drift

•Sluggish response of stock price to firm’s earnings announcement

•Abnormal return on announcement day, momentum continues past market price

continuation of anomaly tests

Abnormal Returns after Earnings Announcements

graph suggests people are still not rational and the market may be inefficient

the earnings aren’t accurate, takes about 3 months to catch up

Strong Form Efficiency Tests

•Inside Information

•The ability of insiders to trade profitability in their own stock has been documented in studies by Jaffe, Seyhun, Givoly, and Palmon

•SEC requires all insiders to register their trading activity

•Trades become public information

Predictors of Stock Returns

•Volatility

•Accruals and earnings quality

•Growth

•Profitability

•Q-factor - the ratio of the present value of an investment to it’s cost (Tobin’s q)

skipped in class

Interpreting Anomalies

•Risk premiums or inefficiencies?

•Fama and French: Market phenomena can be explained as manifestations of risk premiums

•Lakonishok, Shleifer, and Vishny: Market phenomena are evidence of inefficient markets

•Anomalies or data mining?

•Some anomalies have not shown staying power after being reported

•Small-firm effect

•Book-to-market effect: high book value, increase market

bubbles and market efficiency

•Speculative bubbles can raise prices above intrinsic value

•Even if prices are inaccurate, it can be difficult to take advantage of them

skipped in class

Stock Market Analysis

•Analysts are overly positive about firm prospects

•Womack: Positive changes associated with 5% increase, negative with 11% decrease

•Jegadeesh, Kim, Kristie, and Lee: Level of consensus is inconsistent predictor of future performance

•Barber, Lehavy, McNichols, and Trueman: Firms with most-favorable recommendations outperform firms with least-favorable recommendations; Recommendations may lead to investing strategies that are too expensive to exploit

analysts should have a hard time beating the market

alpha

the return on top of the risk premium

excess return on firm risk taken

mutual funds tend to have some of this type of return

Mutual Fund Managers

•Today’s conventional model: Fama-French factors plus momentum factor

•Wermers: Funds show positive gross alphas; negative net alphas after controlling for fees, risk

•Carhart: Minor persistence in relative performance across managers, largely due to expense/transaction costs

skipped in class

•Berk and Green: Skilled managers with abnormal performance will attract new funds until additional cost, complexity drives alphas to zero

hedge fund exclusive, doesn’t grow as much as possible due to it hurting return by requiring more diversification or transaction costs

alpha goes down as fund size goes up

Chen, Ferson, and Peters: On average, bond mutual funds outperform passive bond indexes in gross returns, underperform once fees subtracted

•Kosowski, Timmerman, Wermers, and White: Stock-pricing ability of minority of managers sufficient to cover costs; performance persists over time

•Samuelson: Records of most managers show no easy strategies for success

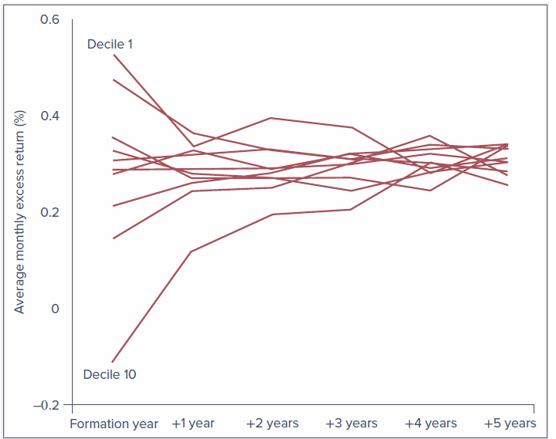

Persistence of Mutual Fund Performance

Shows the Decile formation year

over time performance

evidence of skew? no, not much evidence that good performers stay good over time

hard to stay persistent in trading

Are Markets Efficient?

•Enough that only differentially superior information will earn money

•Professional manger’s margin of superiority likely too slight for statistical significance

basically yes, to an extent