Bond Terms

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

20 Terms

F

Face value (also known as par value or principal), is the fixed amount of money an issuer agrees to repay the bondholder upon the bond’s maturity.

r

Coupon rate per coupon period, the interest rate applied each payment period to determine the coupon payment.

Coupon Amount

The periodic payment made to bondholders, calculated as F⋅r

n

Total number of coupon payments made over the life of the bond.

m

Number of coupon payments made per year.

N

Number of years until the bond matures.

Relationship (n, m, N)

The total number of coupons is given by n=mN

α (alpha)

nominal coupon rate convertible m times per year, representing the annual stated rate before adjusting for compounding.

Relationship (r, α, m)

The coupon rate per period is r=α/m

Total Coupon Payments per Year

The total annual coupon payment is F⋅α

C

Redemption amount, the amount paid to the bondholder at maturity (often equal to face value).

K

Value of the redemption amount C at the time of issue (present value of C)

P

Price of the bond, the amount investors pay to purchase the bond, determined by the market.

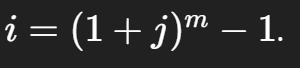

j

Yield per coupon period, the rate of return earned each payment period.

i

Annual effective yield, the actual yearly return accounting for compounding.

I

Nominal yield convertible mmm times per year, the annual yield stated without compounding adjustment.

Relationship (j, m, i)

annual effective yield is

Relationship (j, m, I)

the nominal yield is I=mj

g

Modified coupon rate, calculated as the coupon amount divided by the redemption amount

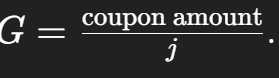

Base amount, equal to the present value of all coupon payments as a perpetuity