Econ 202 Exam 3

1/53

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

54 Terms

Private Enterprise

The ownership of businesses, resources, production technologies, profit,etc. by private individuals.

Production

The process of combining inputs to produce outputs.

Economic Cost

The total cost of production and distribution, including opportunity costs of resources.

Explicit Costs

Out-of-Pocket costs, financial expenditures.

Implicit Costs

The opportunity cost of using resources that the firm already owns, even when no direct payment is made (i.e. wages/rent).

Total Revenue

Price times quantity (PxQ), earnings or income for the firm.

Firm

An organization that combines inputs of labor, capitol, land, and raw or finished component materials to produce final goods and services.

Accounting Profit

The difference between dollars brought in and dollars paid out.

Accounting Profit

Accounting Profit= Total Revenue - explicit costs

Economic Profit

Includes both explicit and implicit costs.

Economic Profit

Economic Profit = Total Revenue - explicit costs - implicit costs

Technology

The method of how inputs are converted to the final product.

Production Funciton

The relationship between the type of land quantity inputs to the level of production for a good or service.

Short Run

Period of time during which at least some factors of production are fixed.

Long Run

Period of time during which all factors are variable.

Fixed Inputs

Factors of production that cannot be easily increased or decreased in a given period of time.

Variable Inputs

Factors of production that a firm can easily increase or decrease in a given period of time.

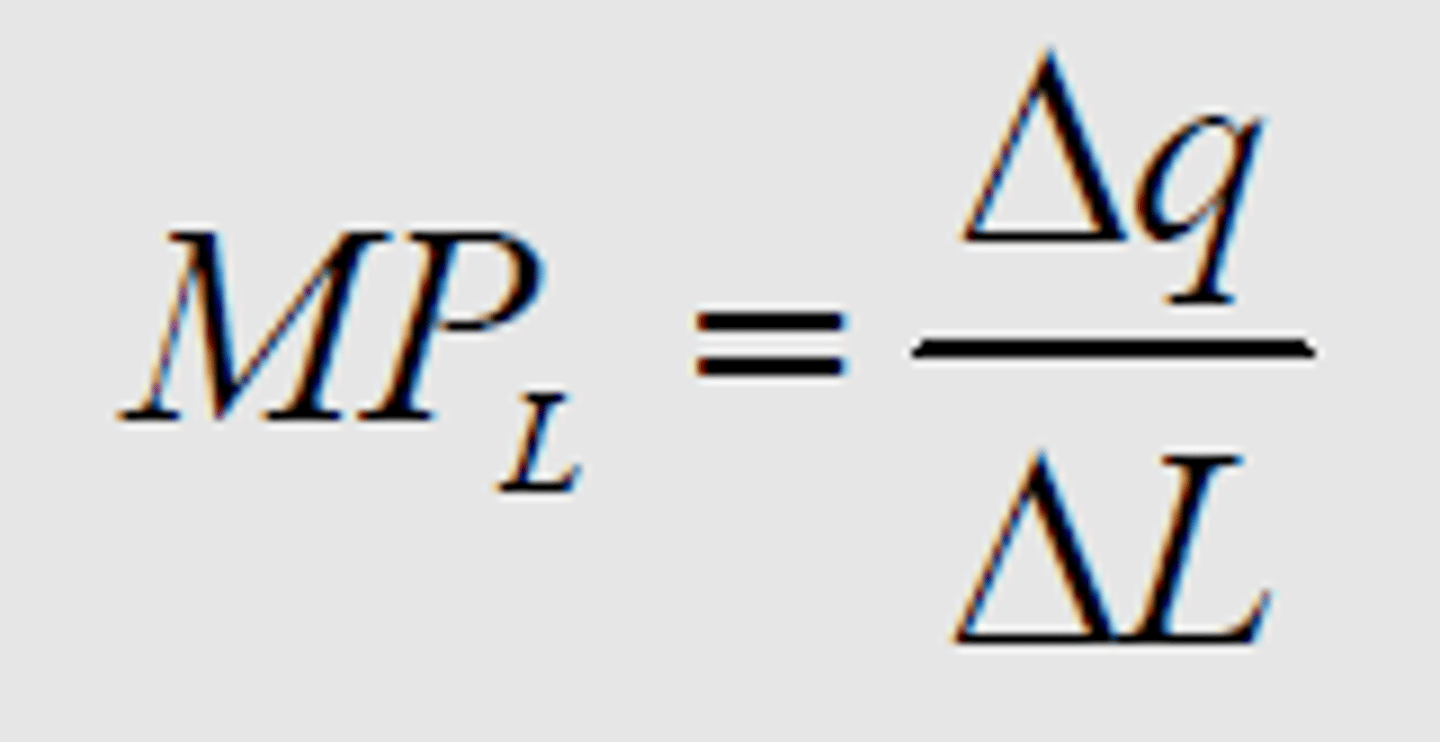

Marginal Product of Labor (MPL)

The additional output of one more worker.

MPL

change in Q/change in L (Q2-Q1/L2-L1)

Law of Diminishing Productivity

General rule that as a firm employs more labor, eventually the amount of additional output produced declines. As more/less labor is hired, labor becomes more/less productive

Fixed Reesources

Cannot be adjusted in a given time period. It will still be employed with no production.

Variable Resources

Can be adjusted, either increased or decreased. It will cause the level of output to change.

Total Cost

The economic value of all resources used to produce output level q.

Fixed Cost

Costs of fixed inputs of fixed resources. Costs of production don't change when output is altered.

Variable Costs

Cost of variable inputs or variable resources. Costs of production that change when output is altered.

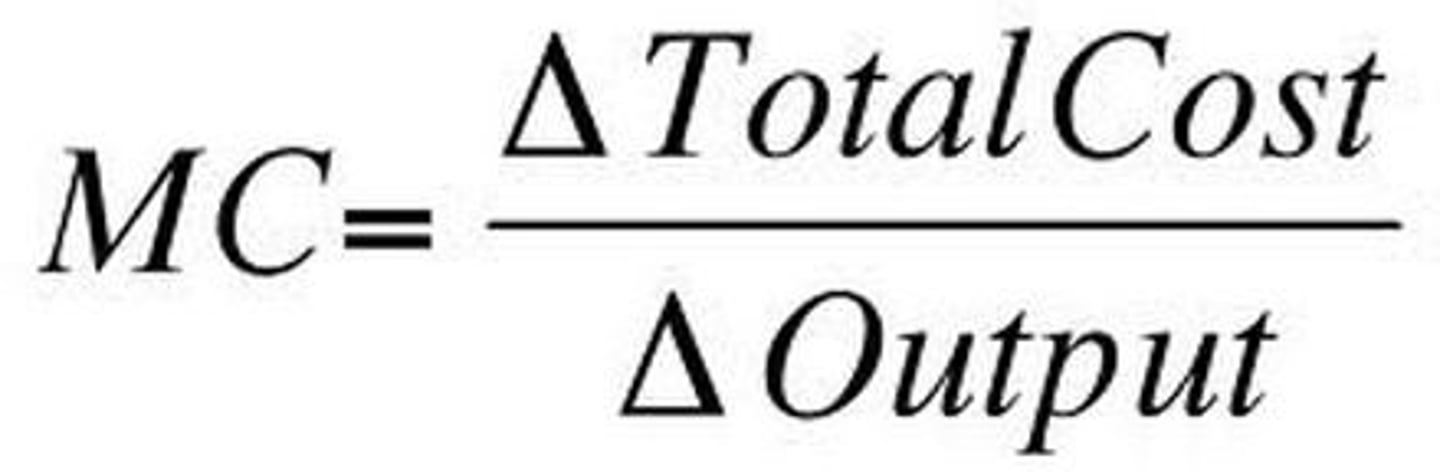

Marginal Costs

The additional cost of producing one more unit of output.

Marginal Cost

change in TC/change in Q (TC2-TC1/Q2-Q1)

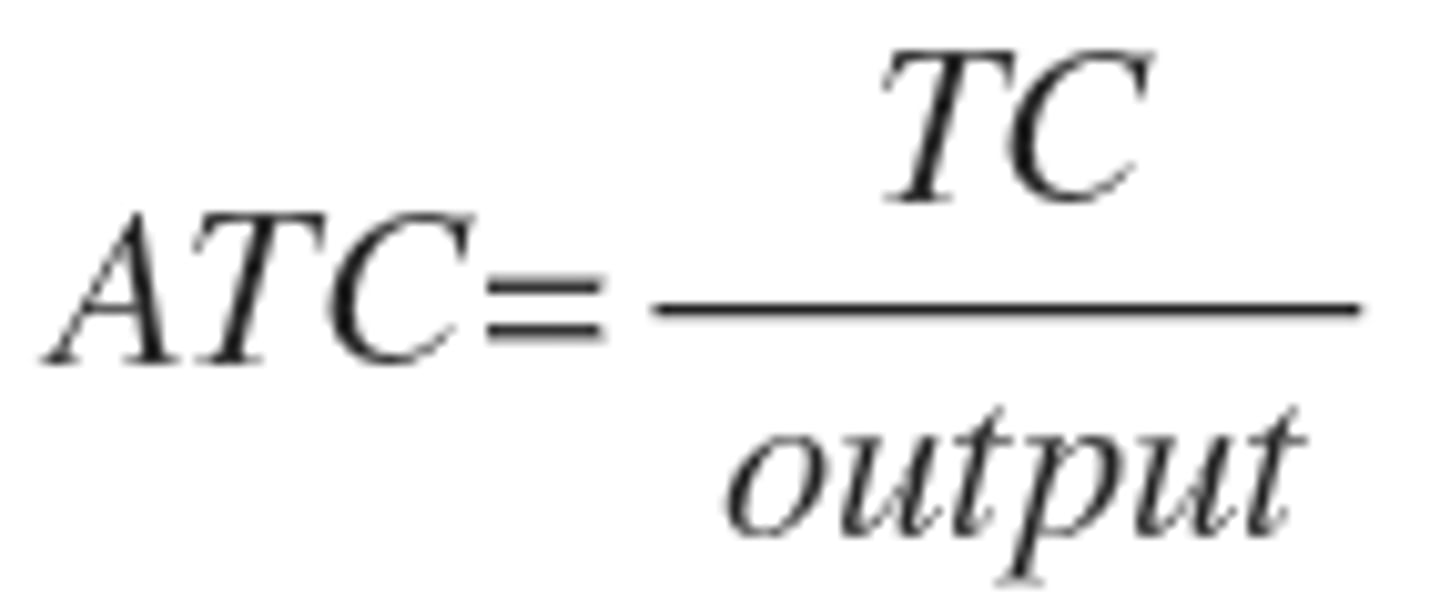

Average Total Cost (ATC)

Total cost divided by the total output in a given time period.

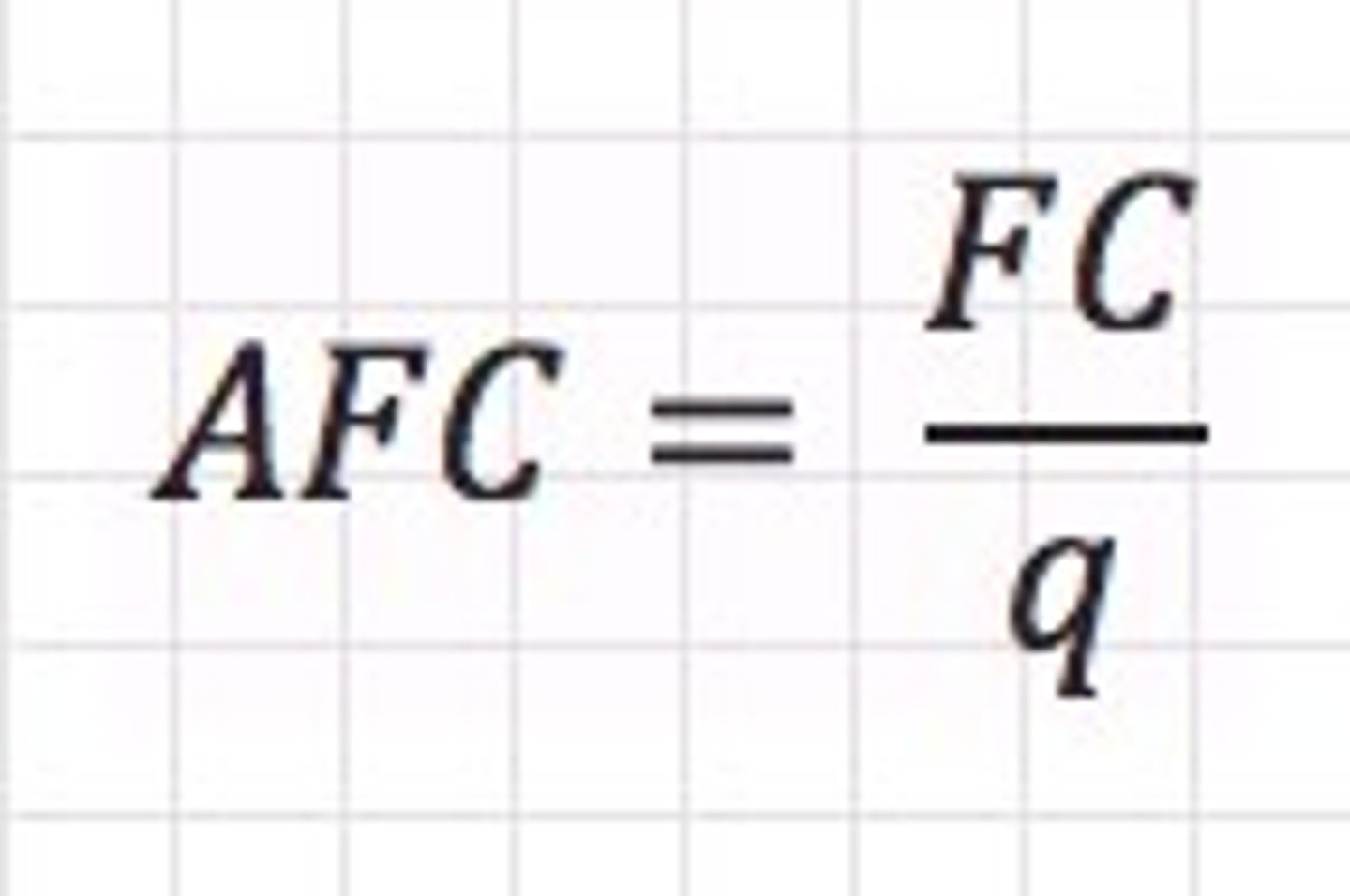

Average Fixed Cost (AFC)

Total fixed cost divided by the total output in a given time period.

Average Variable Cost (AVC)

Total variable cost divided by the total output in a given time period.

Returns to Scale

If you double your input, your output will more than double.

Constant Return to Scale

The company has maxed out their gains from getting bigger, so their costs are remaining constant.

Perfectly competitive market

A market that meets the conditions of (1) many buyers and sellers, (2) all firms selling identical products, and (3) no barriers to new firms entering the market.

Profit Maxmizing Output (Perfect Competition)

MC=MR

Profit Maximizing Output (Monoploy)

P=MR

MC=MR

Profit is not increasing nor decreasing, this is where profit is mazimizing.

MR>MC

Profit is increasing so profit is not yet maximizied.

MR

Profit is decreasing so profit is no longer maximizing.

Shut-Down Rule

A firm should shut down if the price falls below the ninimum AVC.

Total Cost

FC/Q + VC/Q

Zero Profits

Means at the market price, the firm is covering all of its costs including enough to pay labor and capital their orinary oppourtunity cost.

Entry and Exit Costs

e.g., Entry means drilling an oil well

Costs of drilling an oil well are sunk costs

Sunk Costs

A cost that once incurred can never be recovered

Entering Markets

P>AC, incentive to enter

Exiting Markets

P

Pure Monopoly

A market controlled by one seller with a good or service that has no close substitutes.

Oligopoly

When a few firms have a large majority of market share. (i.e. car industry)

Barriers to Entry

Obstacles that make it harder to join the industry.

Natural Monopoly

When it is more cost effective to have one large producer rather than several smaller competing firms.

Market Power

The power to raise price above marginal cost without fear that other firms will enter the market. Comes from selling a unique good with barriers to enter.

Differentiated Products

Goods that are not identical, and firms are able to capture a piece of the market by making unique goods.

Game Theory

Even if the people or companies rationally follow their own self-intrest, the best outcome is hard to reach when they can't or don't cooperate.

Cartel

Split consumers 50/50 and improve prices illegally.

Price Leadership

When the company changes its prices, and its competitors have to decide if their going to follow suit.