IFinance FINAL EXAM PREP (L4-L9)

1/12

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

13 Terms

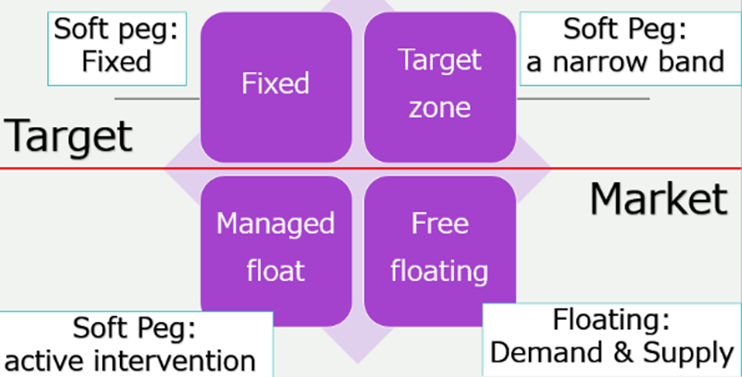

4 main types of exchange rate regimes definitions

Fixed Exchange Rate Regime

Currency is pegged to a major currency (e.g., USD) or basket of currencies

Fluctuates only within a very narrow margin (around ±1%)

Government/central bank maintains the peg

Free Floating Exchange Rate Regime

Exchange rate is fully market-determined by supply & demand

No central bank intervention

Currency can fluctuate widely

Target Zone Exchange Rate Arrangement

Currency allowed to move within a narrow band (e.g., ±1%)

Band/central rate is adjusted periodically to reflect economic fundamentals

Managed Float (Dirty Float) Exchange Rate Arrangement

Exchange rate mostly market-driven

But central bank intervenes actively to influence the currency

Not fixed, not fully free - a hybrid

L4: difference between long and short currency forwards

Long forward contract- agreeing to buy foreign currency in future

Short forward contract- agreeing to sell foreign currency in future

Definition of foreign currency OPTION & 2 types

A foreign currency option is a contract giving the option buyer the right, but not the obligation, to buy or sell a given amount of foreign exchange at a fixed price per unit for a specified time period

•There are two basic types of options:

•A call is an option to buy foreign currency

•A put is an option to sell foreign currency

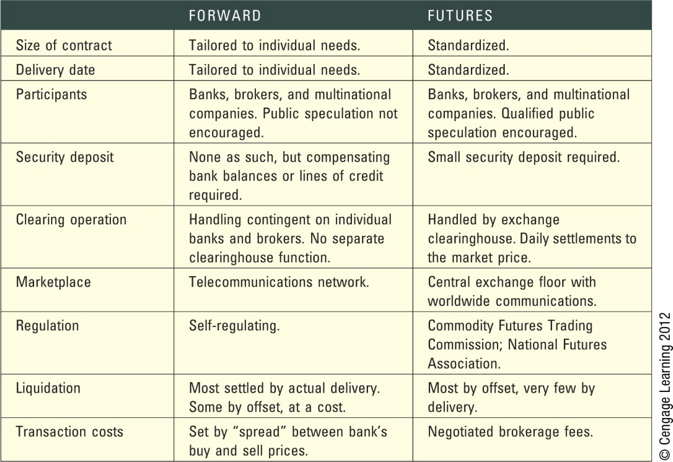

Forward and Futures Market COMPARISON (just in case)

Forward Contract

A private agreement between two parties to exchange currency at a fixed rate on a future date.

Customized

Not traded on an exchange

Very common for hedging

Futures Contract

Similar to a forward, but:

Standardized

Traded on an exchange

FEE

L5 EXPLAIN:

a) fixed exchange rate regime

b) free floating exchange rate regime

c) target zone exchange rate arrangement

d) managed float exchange rate arrangement

1. Fixed Exchange Rate Regime

Currency pegged to another currency (hard or soft peg)

Government actively intervenes

Example: Saudi Arabia

2. Free Floating Exchange Rate Regime

Exchange rate determined by demand & supply

No government intervention

High volatility

Example: UK, USD

3. Target Zone Exchange Rate Arrangement

Exchange rate allowed to fluctuate within a narrow band

Central bank intervenes when limits are approached

A soft peg

4. Managed Float Exchange Rate Arrangement

Exchange rate mostly market-determined

Government occasionally intervenes

Example: India, Singapore

📌 Memory ladder:

Fixed → Target Zone → Managed Float → Free Float

IMPORTANT: explain Free-Floating Exchange Rate Regime:

What it is

Why Malaysia uses it

Pros & cons

Definition

A free-floating exchange rate is determined by market supply and demand with no government intervention.

Advantages

No need for huge reserves

Can absorb economic shocks

Monetary policy is independent

Disadvantages

Exchange rate volatility

Uncertainty for businesses

Malaysia

Malaysia moved to a float after the 1997 Asian crisis so it could control interest rates and inflation.Malaysia prefers free floating because it allows independent monetary policy and absorbs economic shocks, but it creates exchange-rate volatility which increases business risk for MNCs.

TO UNDERSTAND/MEMORIZE THIS ESSAY MODEL ANSWER:

Free-Floating Exchange Rate Regime

A free-floating exchange rate regime is one in which the value of a currency is determined by market forces of demand and supply without direct government intervention. Under this system, exchange rates fluctuate freely in response to changes in economic conditions such as inflation, interest rates, trade balances, and investor confidence. Many countries adopt this regime to allow their currencies to reflect true market conditions.

One major advantage of a free-floating regime is that it allows a country to maintain independent monetary policy, enabling the central bank to adjust interest rates to control inflation or stimulate economic growth. It also reduces the need for large foreign exchange reserves and allows the economy to absorb external shocks more smoothly. However, the main disadvantage is exchange rate volatility, which creates uncertainty for firms involved in international trade and investment.

Malaysia adopts a free-floating exchange rate regime to maintain monetary independence and flexibility, especially after experiencing the Asian Financial Crisis in 1997. While this regime exposes firms to exchange rate risk, it provides long-term macroeconomic stability and policy autonomy.

IMPORTANT: explain Economic (Operating) Exposure with examples

Economic exposure refers to the impact of exchange-rate changes on a firm’s future operating cash flows and competitiveness. Unlike transaction exposure, it affects the entire business. For example, a strong US dollar makes Apple’s products more expensive overseas, reducing demand. Firms manage economic exposure through operational strategies such as matching currency cash flows, diversifying production, and using currency swaps.

its about how exchange rates change a firm’s competitiveness and future cash flows by measuring it

Example from slides:

Toyota → weak yen = more profit

Apple → strong USD = overseas sales fall

TO UNDERSTAND/MEMORIZE THIS ESSAY MODEL ANSWER:

Economic exposure, also known as operating exposure, refers to the extent to which a firm’s future cash flows and overall market value are affected by unexpected changes in exchange rates. Unlike transaction exposure, economic exposure focuses on the long-term impact of exchange rate movements on a firm’s competitiveness, pricing strategy, and demand for its products in global markets.

For example, a strong domestic currency can make a firm’s exports more expensive abroad, reducing sales and market share, while a weaker currency can enhance competitiveness. Companies such as Toyota benefit from a weaker yen, which increases overseas revenue when converted back to yen, whereas firms like Apple face reduced international revenues when the US dollar strengthens.

Firms manage economic exposure through strategic decisions rather than financial contracts. These strategies include diversifying production locations, matching costs and revenues in the same currency, sourcing inputs globally, and adjusting pricing strategies to remain competitive in different markets.

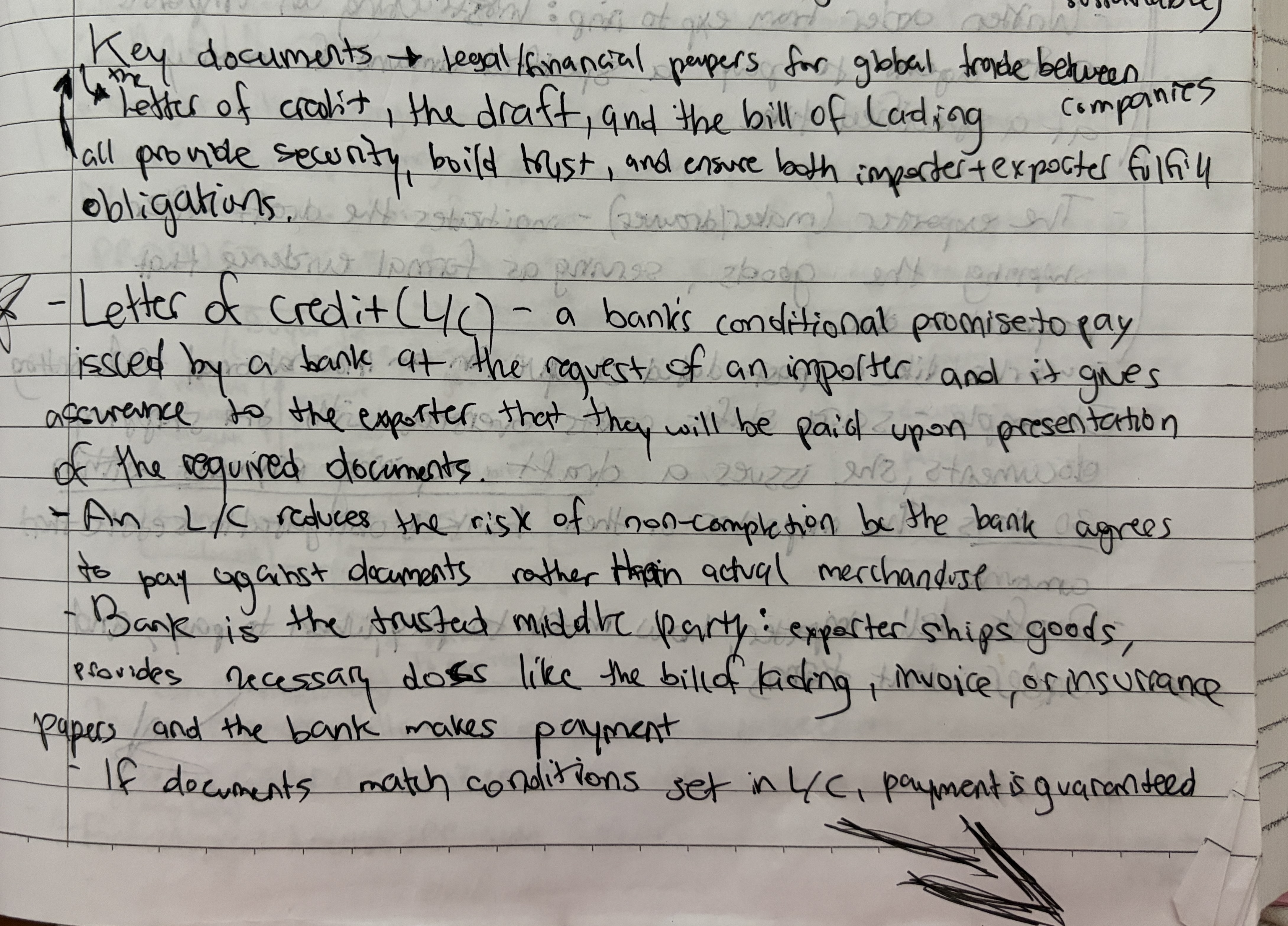

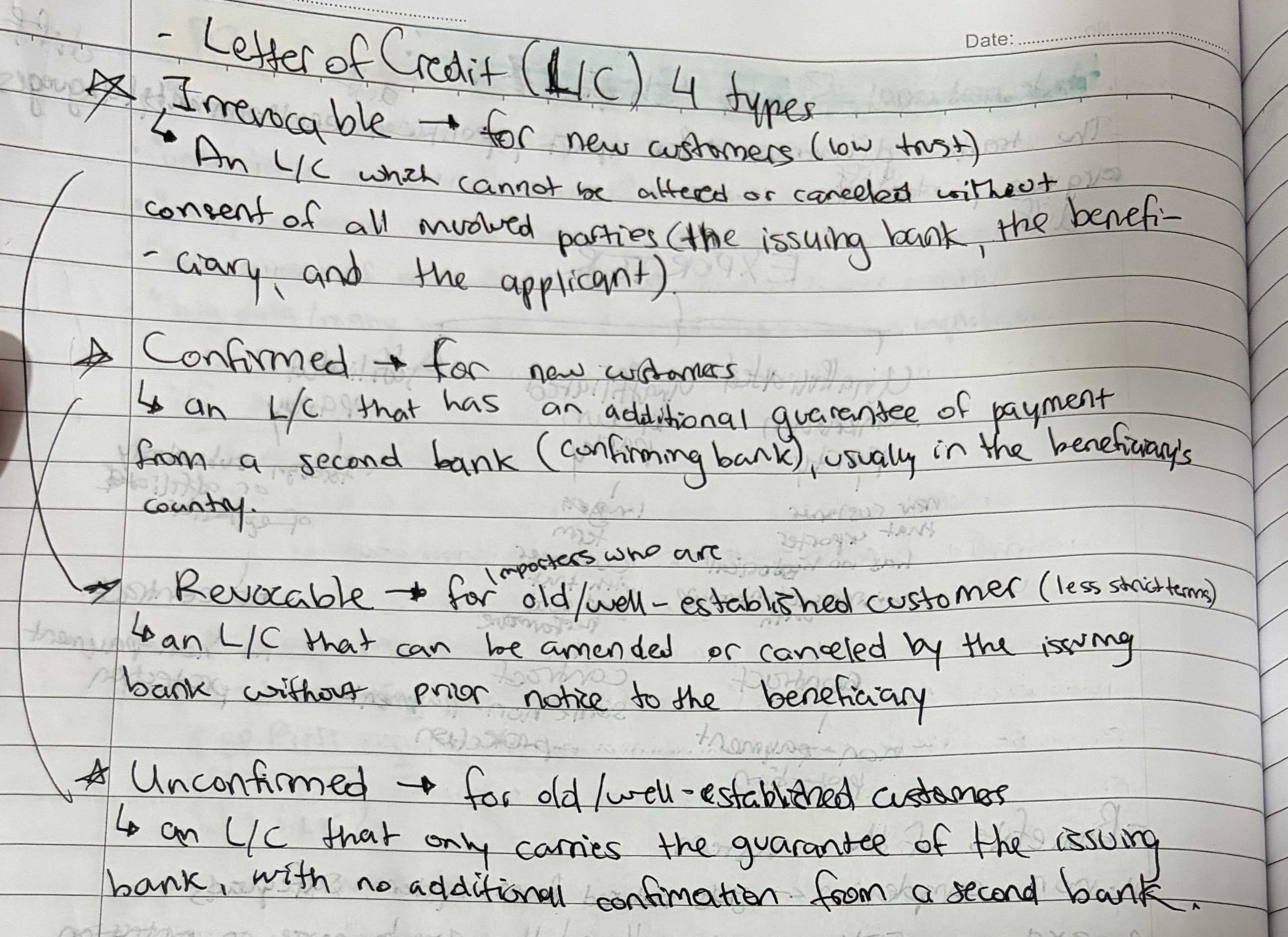

IMPORTANT: explain about the Letter of Credit

Problem

Importer and exporter don’t trust each other.

Solution

A bank issues a Letter of Credit promising to pay the exporter if documents are correct.

Key documents

Letter of Credit

Draft

Bill of Lading

Why it reduces risk

Exporter relies on bank, not buyer

Importer pays only when documents are received

TO UNDERSTAND/MEMORIZE THIS ESSAY MODEL ANSWER:

A Letter of Credit (L/C) is a bank’s conditional promise to pay an exporter on behalf of an importer, provided that the exporter presents documents that comply with the terms specified in the credit. It is widely used in international trade to reduce the risk of non-payment caused by distance, lack of trust, and differences in legal and business systems between trading partners.

The key feature of a Letter of Credit is that payment is made against documents rather than the actual goods. The three main documents involved are the Letter of Credit itself, the draft (bill of exchange), and the bill of lading. This system protects the exporter by ensuring payment from a reputable bank, while the importer is protected because payment is only made when shipping documents are properly presented.

Letters of Credit are especially important for transactions involving new or unfamiliar trading partners. By transferring credit risk from the importer to the bank, the L/C facilitates international trade, improves financing opportunities, and reduces uncertainty for both parties.

IMPORTANT: UNDESTAND THE Subprime Crisis 2008

TO UNDERSTAND/ THIS MODEL explanation:

Subprime Crisis 2008

The Subprime Crisis of 2008 was a global financial crisis that originated in the United States due to excessive lending to high-risk borrowers with poor creditworthiness. Banks issued subprime mortgages and then securitized these loans into complex financial instruments, which were sold to investors worldwide under the assumption that housing prices would continue to rise.

When interest rates increased and borrowers began defaulting on their mortgage payments, housing prices collapsed and the value of mortgage-backed securities fell sharply. This led to severe losses for banks and financial institutions, causing liquidity shortages, bank failures, and a collapse in investor confidence. Major institutions faced bankruptcy, triggering a global financial panic.

The crisis spread internationally because financial markets were highly interconnected, with global investors holding US mortgage-related assets. The Subprime Crisis highlighted the dangers of excessive risk-taking, weak regulation, and lack of transparency in financial systems, leading to significant reforms in banking and financial supervision worldwide.

TUTORIAL 4- steps of calculating options & forwards (fx derivatives)

for regular questions:

step 1- calculate premium x total units

step 2- do S-E if call or E-S if put. EX : 1.46-1.45= 0.01 IV

step 3- calculate profit/loss per unit (IV-Premium=net prof per unit)

step 4- calculate prof/loss per OPTION (Q x net profit per unit)

basically:

step 1- premium x total units

step 2- e-s or s-e which = iv

step 3- prof/loss unit (iv-premium)

step 4- prof/loss option (Q x net prof per unit)

also calculate premium paid if U DONT exercise option (premium x total)

for rise and fall of call and put option calculations:

call - rise : s-e

call - rise : prof/loss (IV-Premium)

call - fall : s-e

call - fall : prof/loss (IV-Premium)

AND

put - rise : s-e

put - rise : prof/loss (IV-Premium)

put - fall : s-e

put - fall : prof/loss (IV-Premium)

TUTORIAL 6- steps of calculating Hedging strats (forward, money market)

FORWARD RATE

step 1: forward rate based on IRP

s x ( 1+ i home/ 1+ i foreign) = spot forward (SF)

step 2: Cash flow unhedged

amount x SF

MONEY MARKET

step 1: (firm can convert home currency to foreign currency and deposit it in a bank at _ %) invest amount to hedge payables

Amount/(1+i foreign)= deposit amount

step 2: (firm must borrow from home country bank for _ year to make deposit into foreign bank)

Amount borrowed in USD - deposit amount x S (spot) = borrowed amount in home currency

step 3: (later firm must repay home currency loan with home country interest %)

Loan repayment - borrowed amount in home currency x ( 1 + i home)

IF OPTION MARKET’S spot 1 year from now changes

step 1: calc quality of contract (Q) = amount/contract size (CS)

step 2: exercise value = exercise price x Q x CS

step 3: calc premium paid = premium x Q x CS

step 4: amount recieved in home currency = exercise value - premium paid

TUTORIAL 8- steps of calculating WACC, cost of equity, cost of debt

if QUESTION GIVES U We and Wd in a ratio like debt/equity = 1:2 then do this:

step 1: find total assets (D+E=A) so 1+2=3 so NOW Wd = 1/3 and We = 2/3

Calculating foreign project WACC and parent WACC:

step 1: foreign project wacc : wacc = We(Ke)+Wd(Kd)(1+T)

step 2: parent wacc : wacc = We(Ke)+Wd(Kd)(1-T)

if QUESTION GIVES U NORMAL We and Wd then do this:

step 1: find total assets (D+E=A) so if it says d 10 mill and e 20 mill : 10+20=30 total assets

step 2: divide debt by total assets and equity by total assets to find real Wd and We : d 10/30= _ and e 20/30= _

step 3: finally do the wacc = We(Ke)+Wd(Kd)(1-T)

HOWEVER IF IT ALSO ASKS to calculate wacc including exchange rate change, do:

K=(1+wacc answer)(1+e)-1

k = rate of return

e=exchange rate

IF QUESTION GIVES U BETA, RISK FREE RETURN & return on market

do Ke = Rf + B (Rm-Rf) and convert answer to percentage if u think its asked

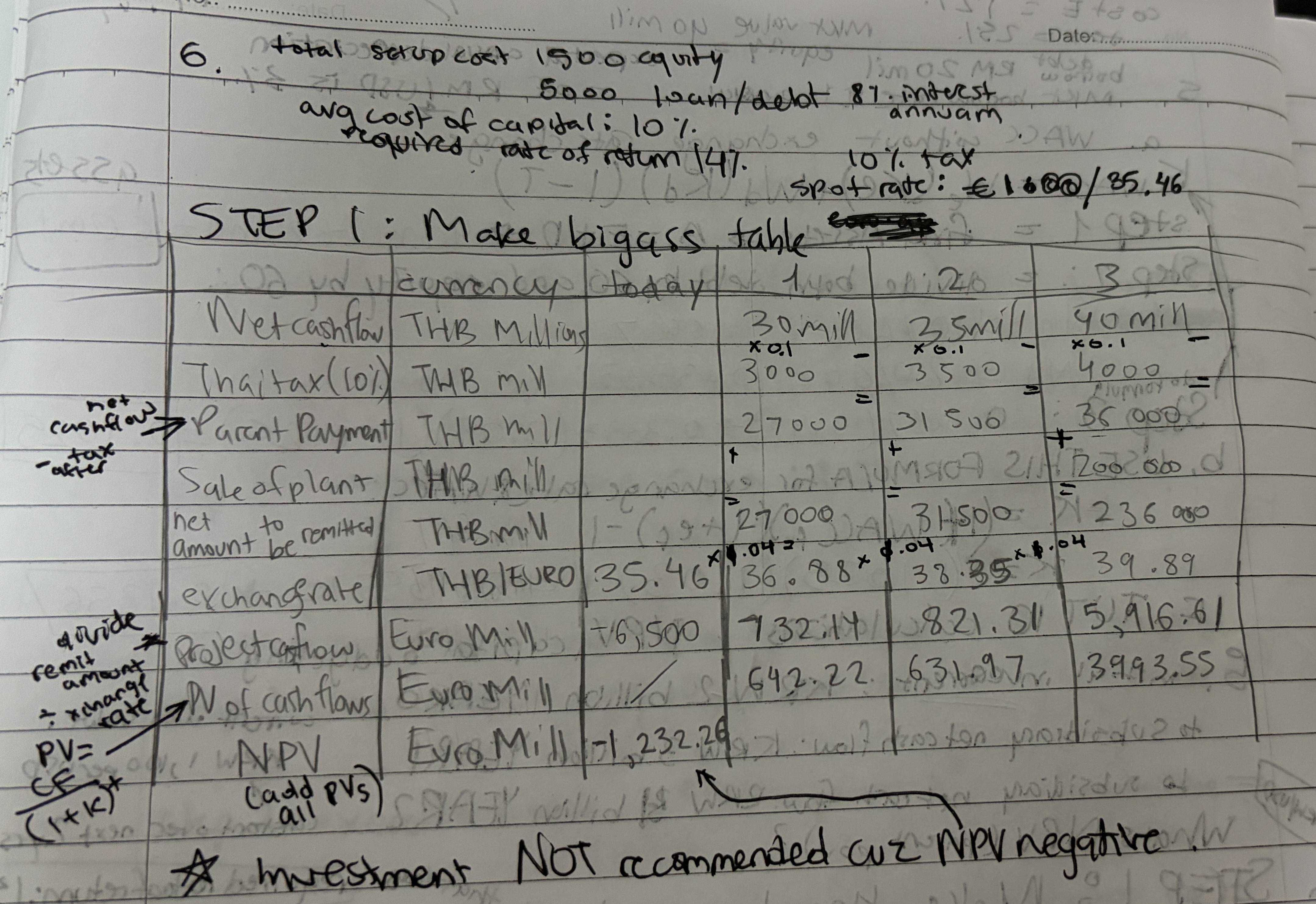

TUTORIAL 10- steps of calculating NPV, capital budgeting

to know :

k= rate of return

t= time

PV=present value

calculating tax cost = net cash flow x tax

calculating parent payment = net cash flow - tax cost

calculating net amount remitted = parent payment + sale of plant

calculating exchange rate = Y1 use og given rate then times by new rate and Y2 times that Y1 result by new rate

calculating project cashflow = remitted amount/exchange rate for every year

calculating PV = CF/(1+K)^t do for each year

calculating npv= all PV’s added

if NPV negative, investment not recommended