BUDGETING

1/25

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

26 Terms

It is a forecasting tool to determine future sources and uses of resources

Budgeting

It is a quantitative expression of what management wants to attain. It also serves as a guideline to attain desired outcomes or objectives.

Planning

Budget Cycle

Planning

Negotiation and Approval

Implementation

Review

Advantages and Uses of Budgets

Define goals and objectives

Think about and plan for the future

Means of allocating resources

Uncover potential bottlenecks

Coordinate activities

Communicate plans

Sources of Information for Preparing Budgets

Past company records

Benchmark with industry competitors

Standards developed by company

It is carefully predetermined price, cost, or quantity based on efficient operations and usually expressed on a per unit basis

Standard

These standards allow allowance for down-time and rest periods

Attainable (Practical)

These standards assume 100% efficiency

Theoretical (Ideal)

Budgets are determined based on standard costs and usually stated on a per unit basis (T/F)

False (total amount)

It is the understatement of revenues and overstatement of expenses making the budget targets easily attainable

Budgetary Slack

It is the sum total of all divisional budgets that is prepared by all the divisions.

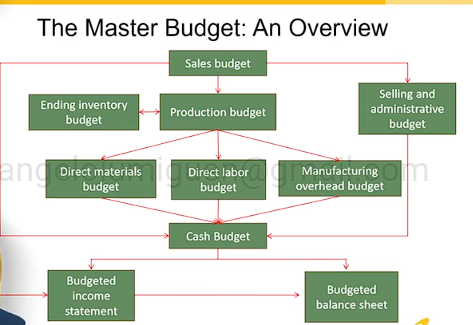

Master Budget

Two Major Composition of Master Budget

Financial Budgets (Balance Sheet Budget)

Operating Budgets (Income Statement Budget)

In preparing the Master Budget what is the first budget that is being prepared?

Sales Budget

The last budget that being prepared

Budgeted Statement of Cashflow

It includes (1) cash, (2) capital expenditures, (3) balance sheet, and (4) cash flows

Financial Budget

Steps in Preparing the Operating Budget

Step 1: Revenues budget, in units to determine production budget then converted to money for the Sales budget

Step 2: Production budget (in units)

Step 3: Direct materials usage and purchase budgets

Step 4: Direct labor budget

Step 5: Manufacturing overhead budget

Step 6: Ending inventories budget

Step 7: Cost of Goods Sold budget

Step 8: Non-manufacturing costs budget

Step 9: Budgeted Income Statement

Major Components of Budget Committee

Marketing Manager

Production Manager / Industrial Engineer

Purchasing

Human Resource

Treasurer / Cash Budget

Controller - head

It is the budget that supports Total Quality Management. It is defined as a budgeting technique focusing on continuous improvement from a service or product perspective.

Kaizen

It is a planning system under which costs are associated with activities, and expenditures are then budgeted based on the expected activity level.

Activity-based budgeting

Common in both Kaizen Budgeting and Activity-based Budgeting

Increase in quality, efficiency, and speed, while decreasing the cost

This budget is prepared for a single level of output (normal capacity)

Static (Fixed) Budget

A Master Budget is an example of what type of budget?

Static Budget

This is the only budget that is adjusted to actual level of output

Flexible Budget

It is a budget that starts from zero regardless if there is a prior budget or actual operations from the prior year

Zero-based Budget

This budget is prepared on a monthly or quarterly basis

Continuous/Sliding/Rolling/Perpetual Budget

It is a budget that is prepared with the full cooperation and participation of the managers at all levels.

Participative Budget