L1 Stationary point Econmetric

1/20

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

21 Terms

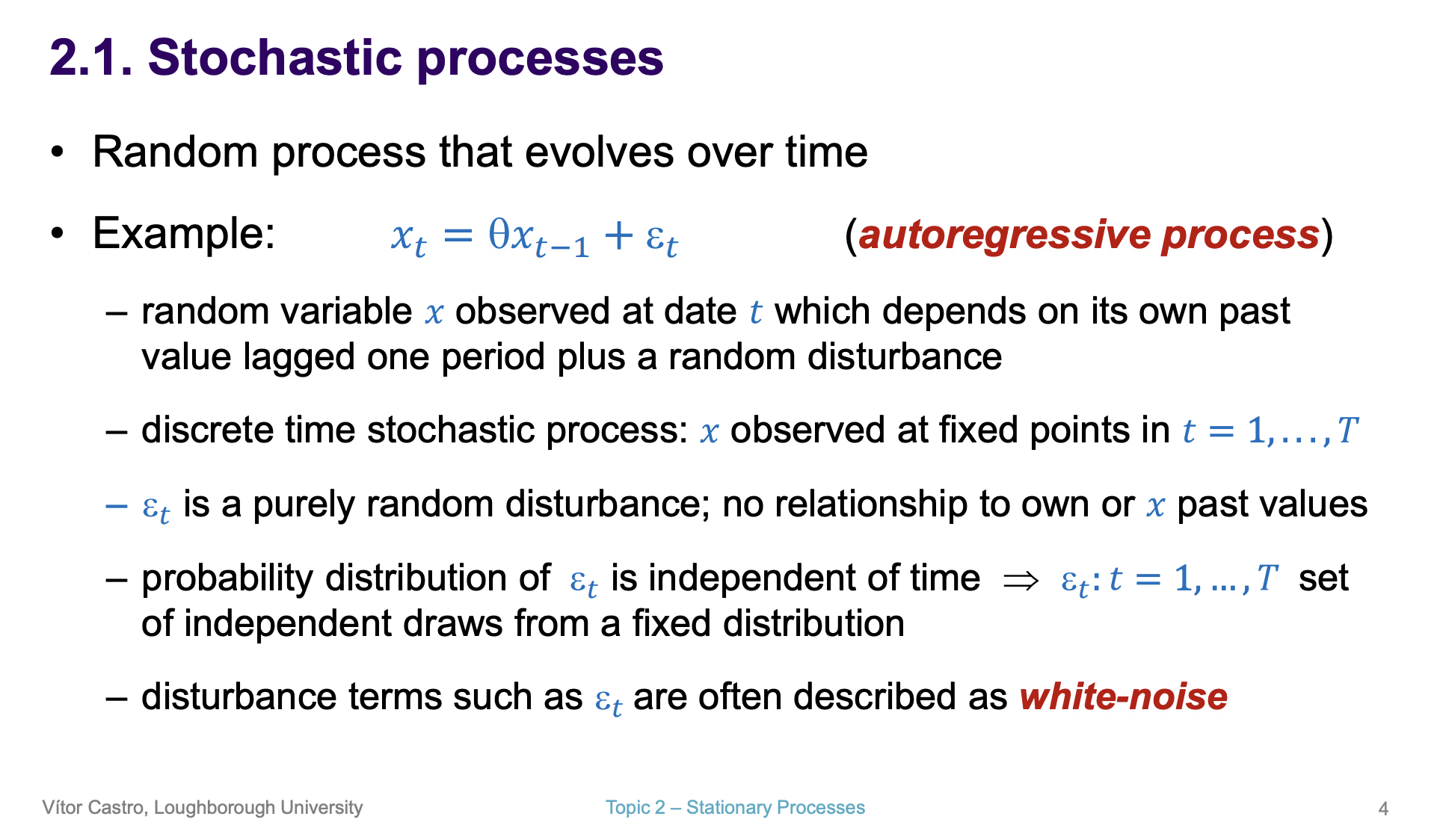

What is a stochastic process

What is a Auto regressive function and what do we use to identify its order in ACF and PACF

Use PACF to find its order of AR model, if the ACF converses to 0

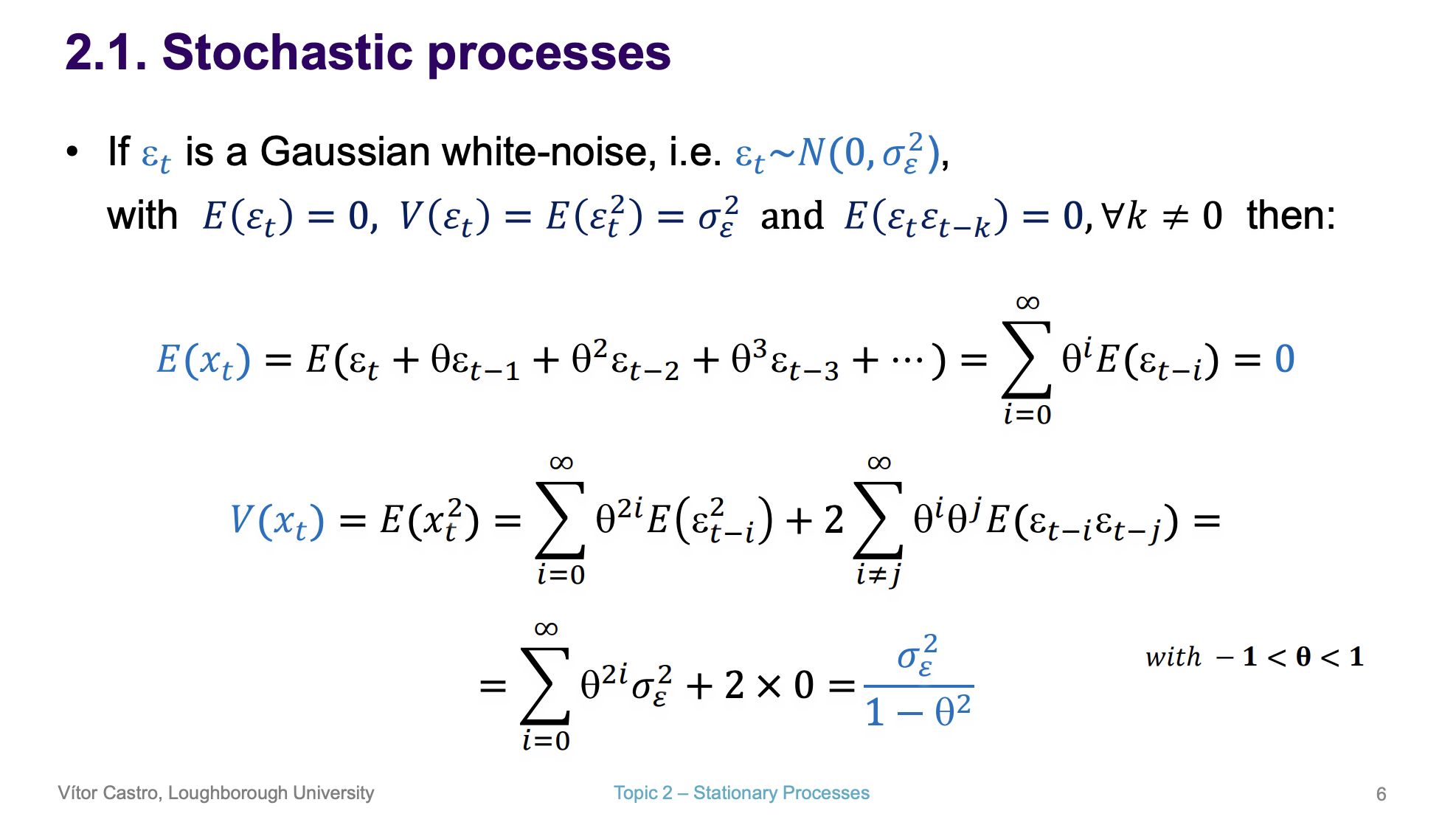

If we have the error term as white noise, what is the Mean and Variance equal to

Expected value and variance is constant from the idea of stationarity

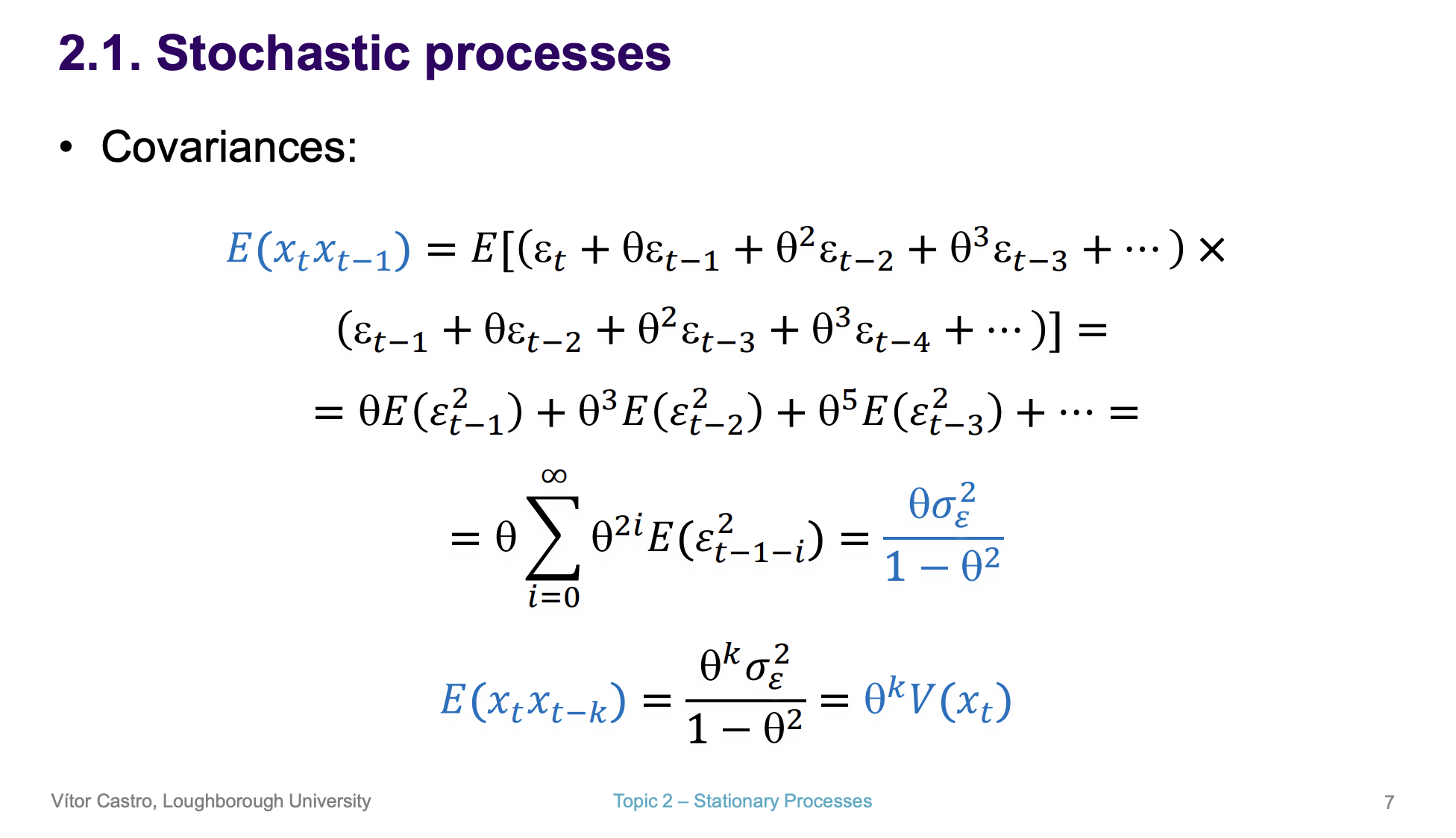

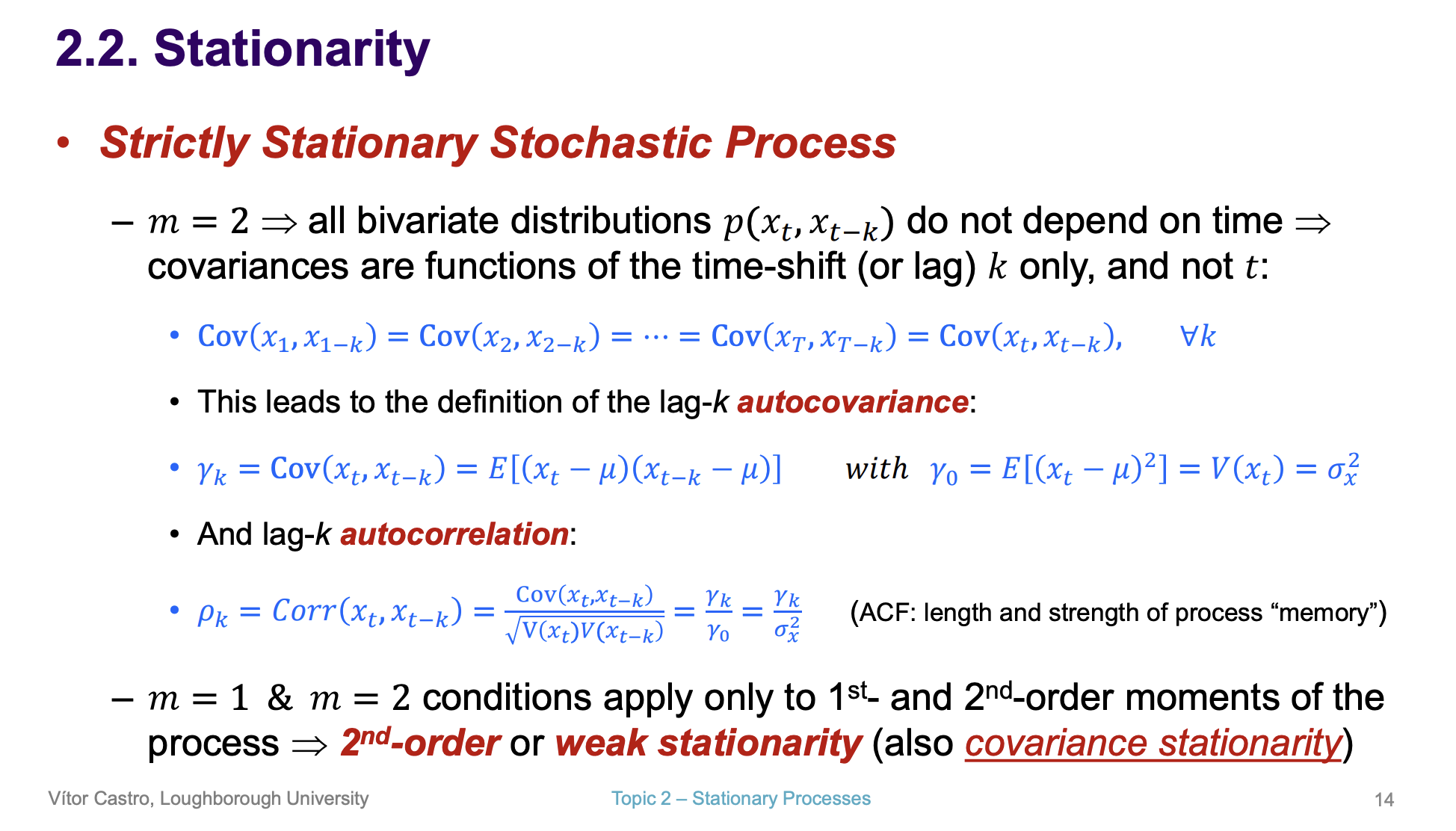

What is the equation for CO variance

What defines the auto correlation of a function?

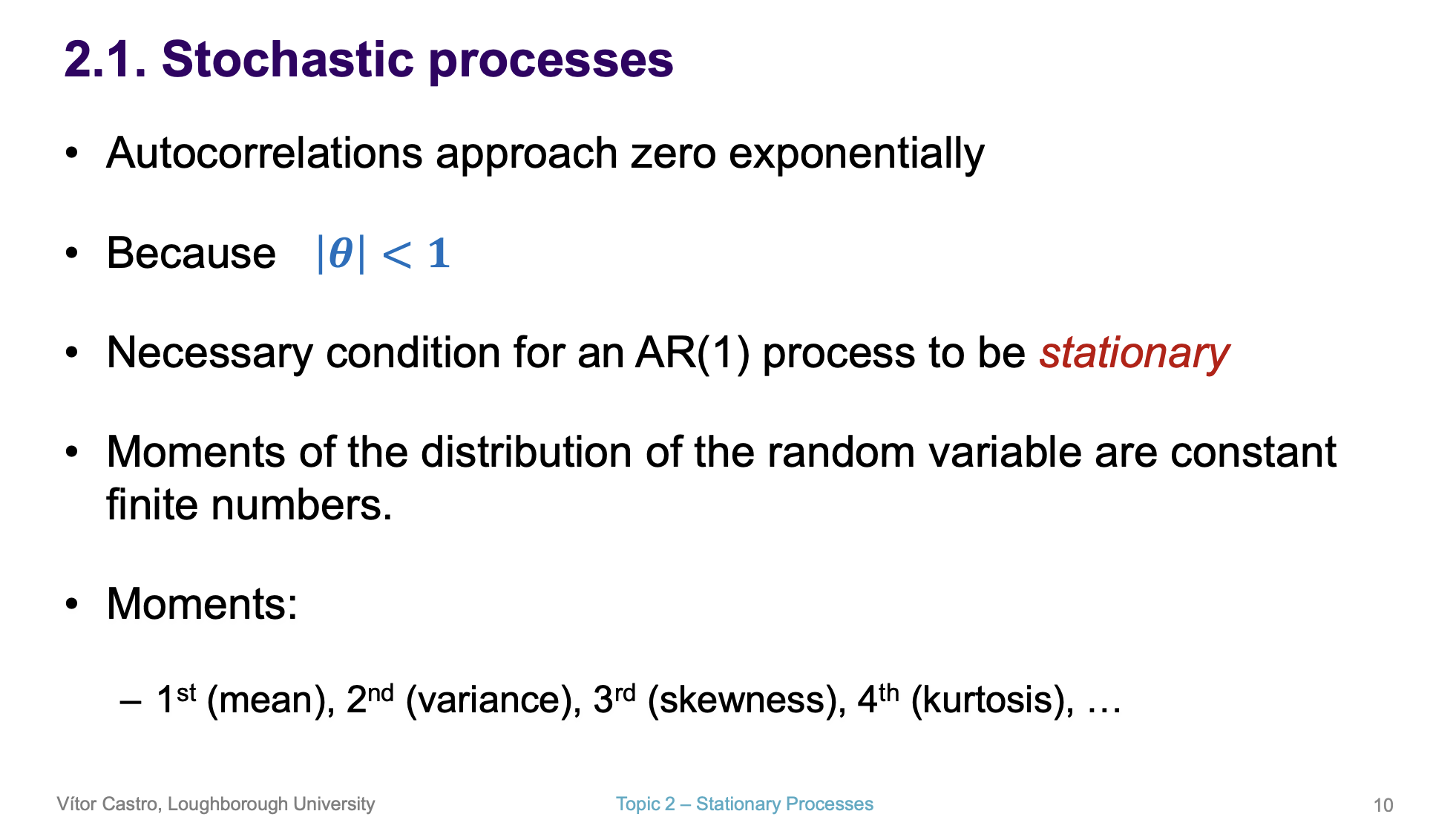

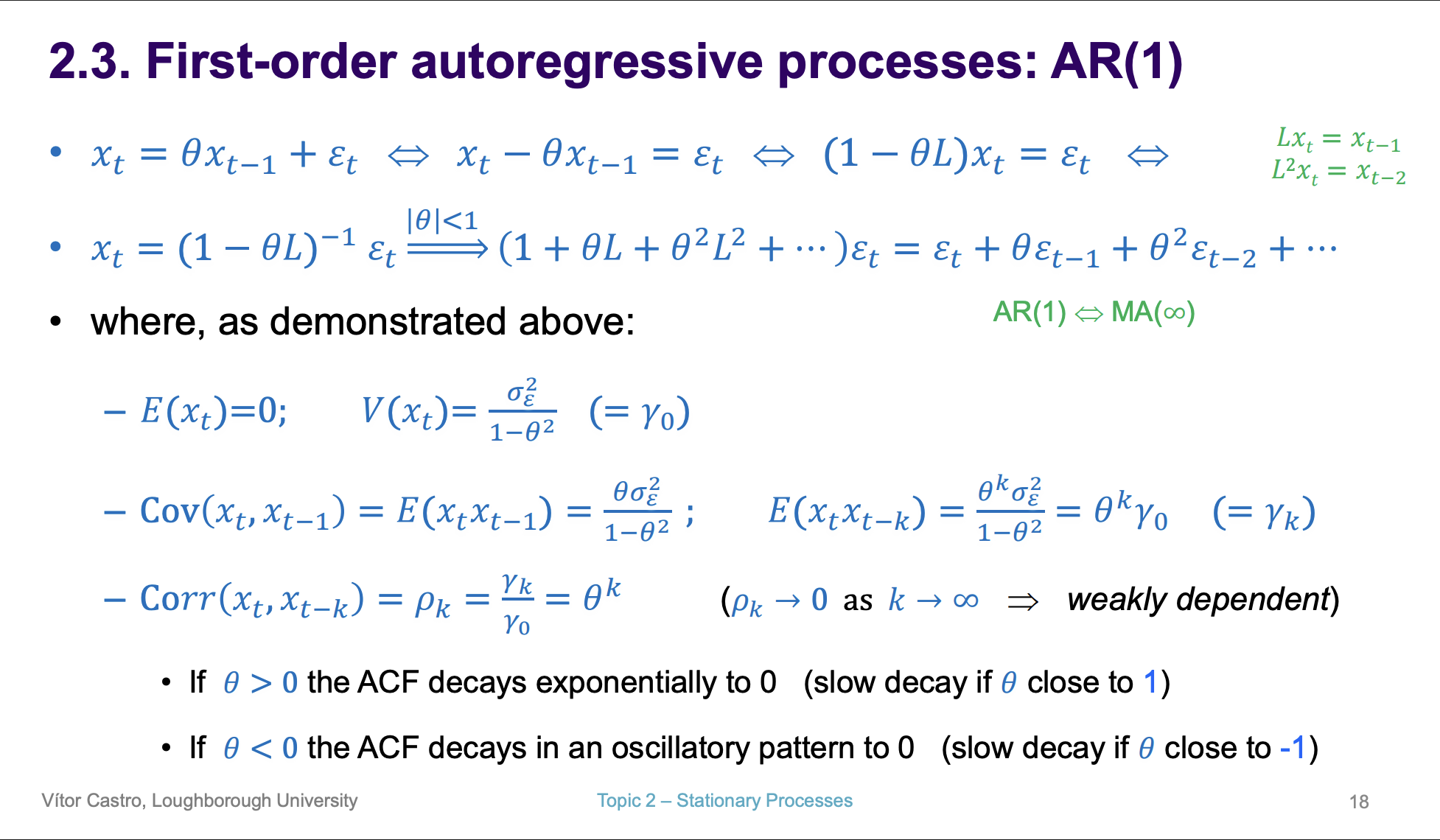

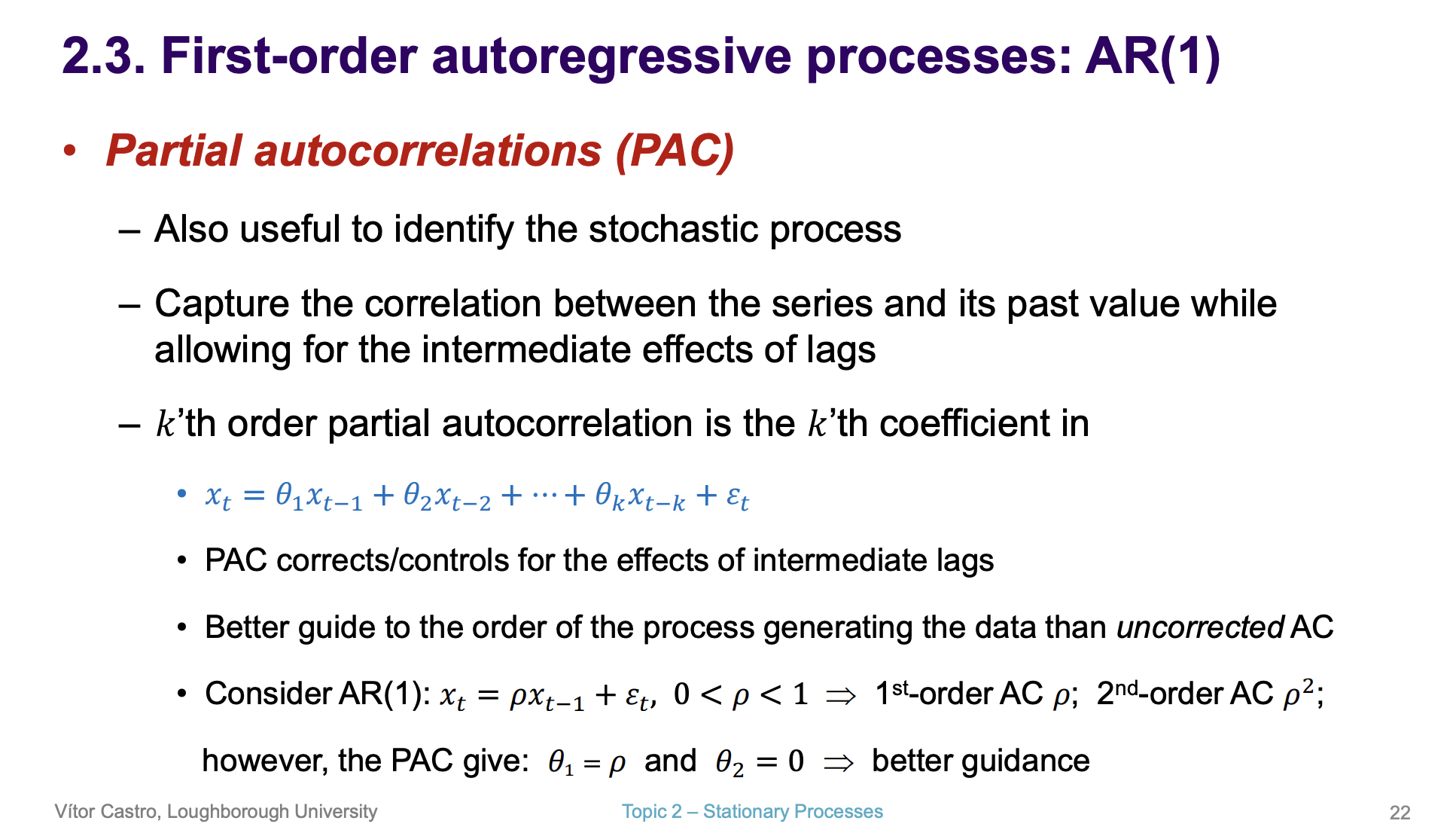

What is the necessary conditionn for AR(1) to be stationary

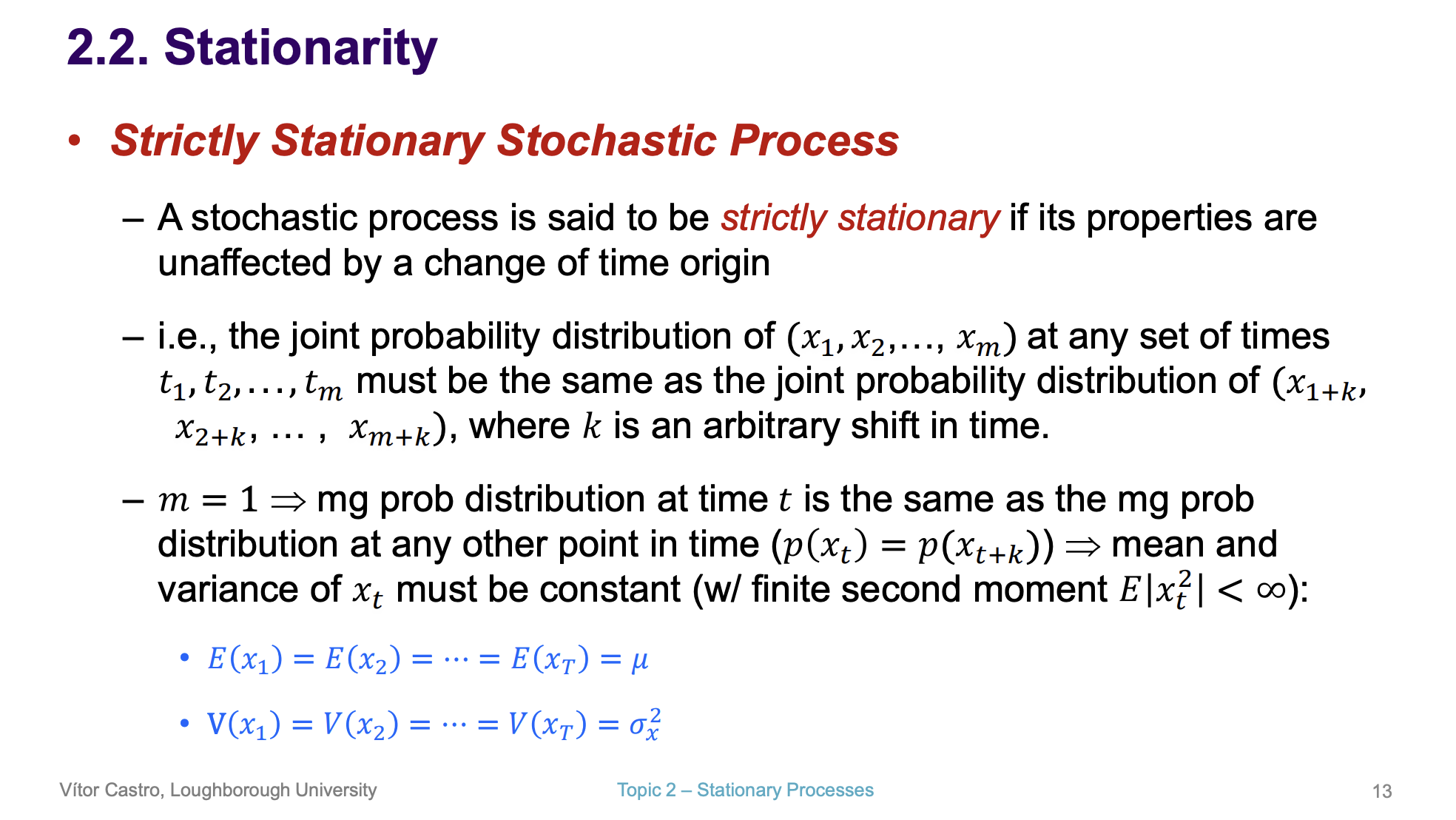

define what strictly stationary means

define what strictly stationary means v2

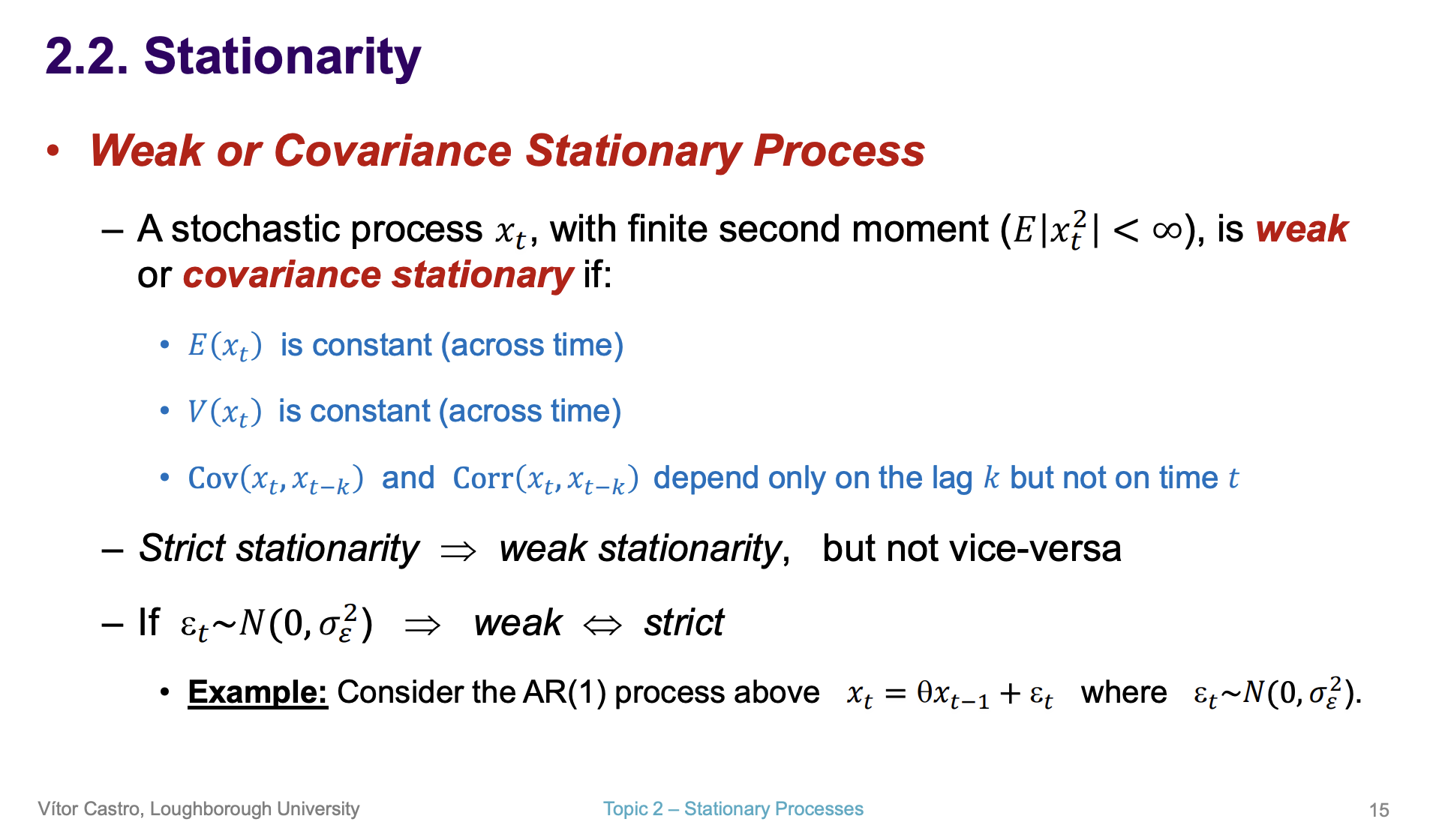

Define what weak or covariance stationary process means

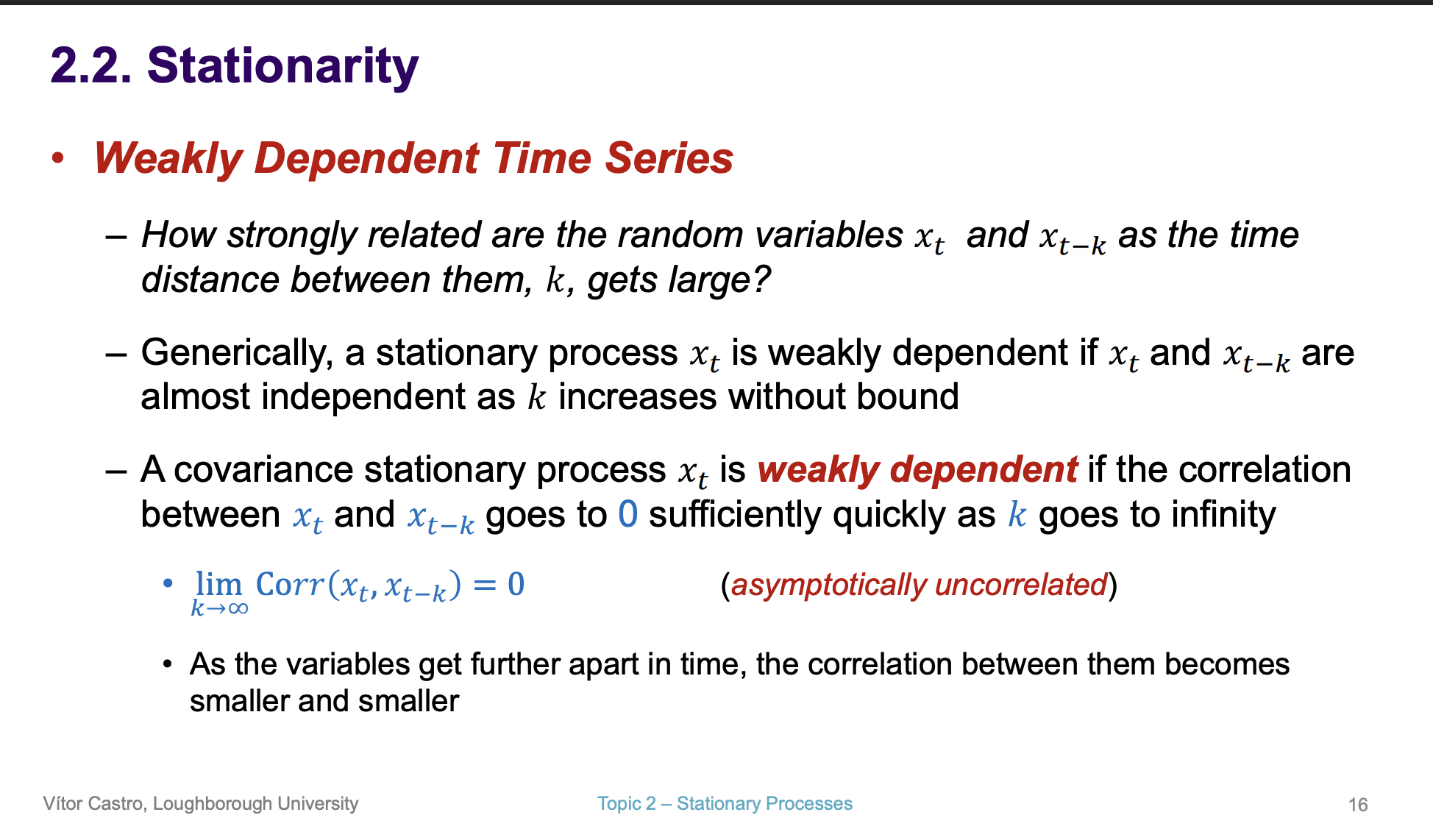

Define a wealky dependent time series

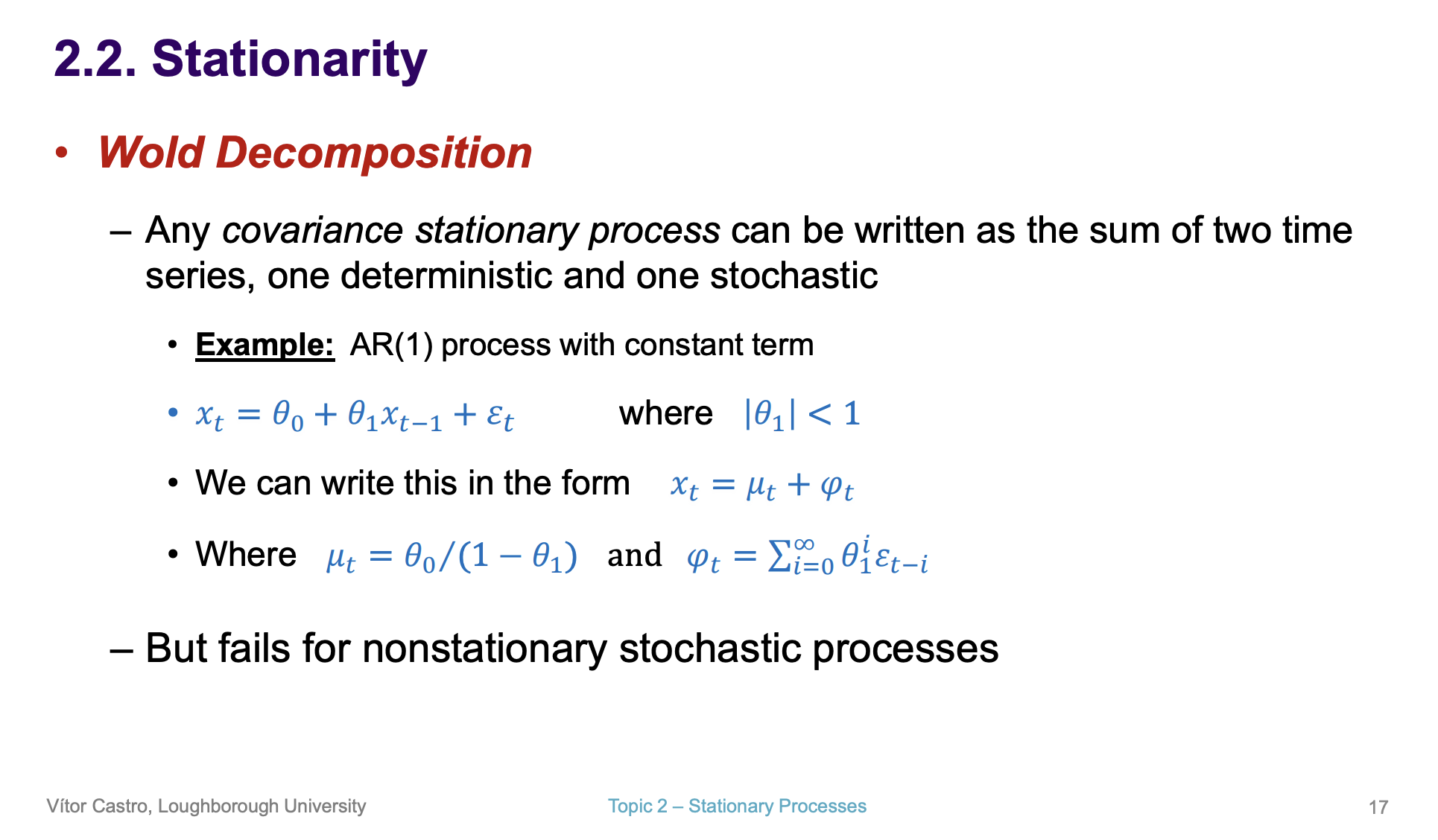

Define Wold Decomposition

What are some of the equation for AR(1)

What is a PAC

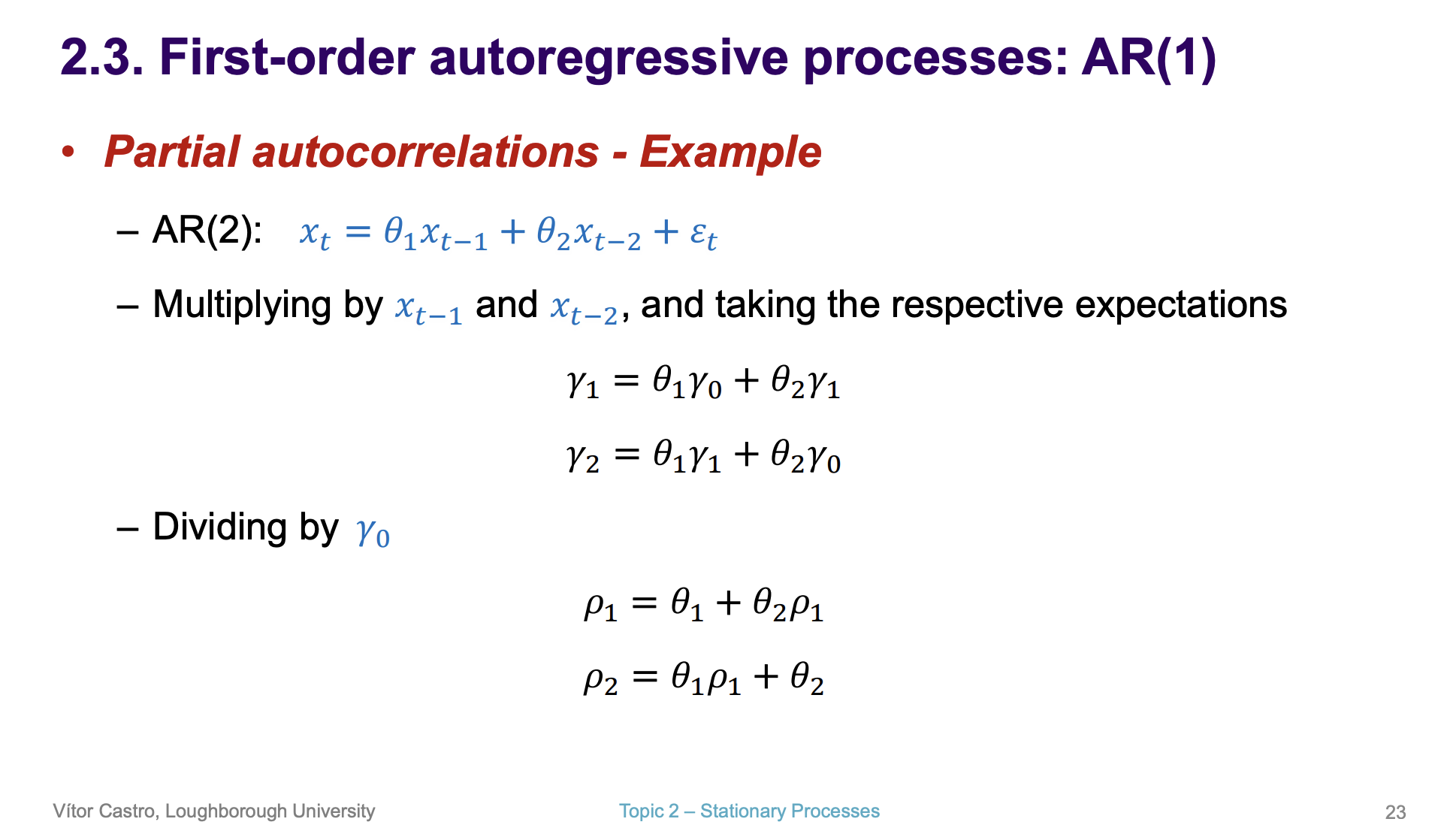

What equation do we use to find partial auto correlations in AR(2) models

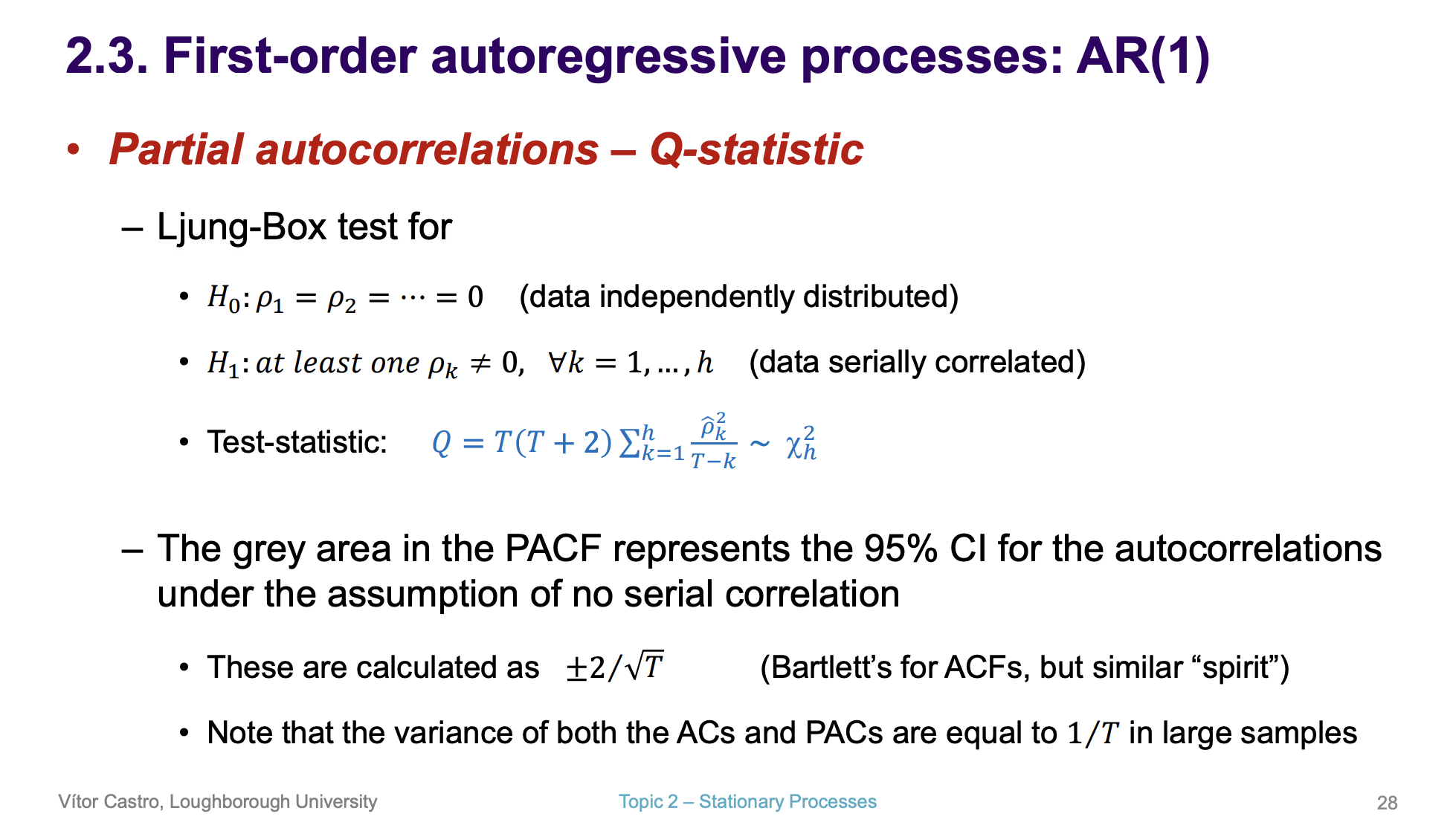

Q stat in the PAC, what is it used for

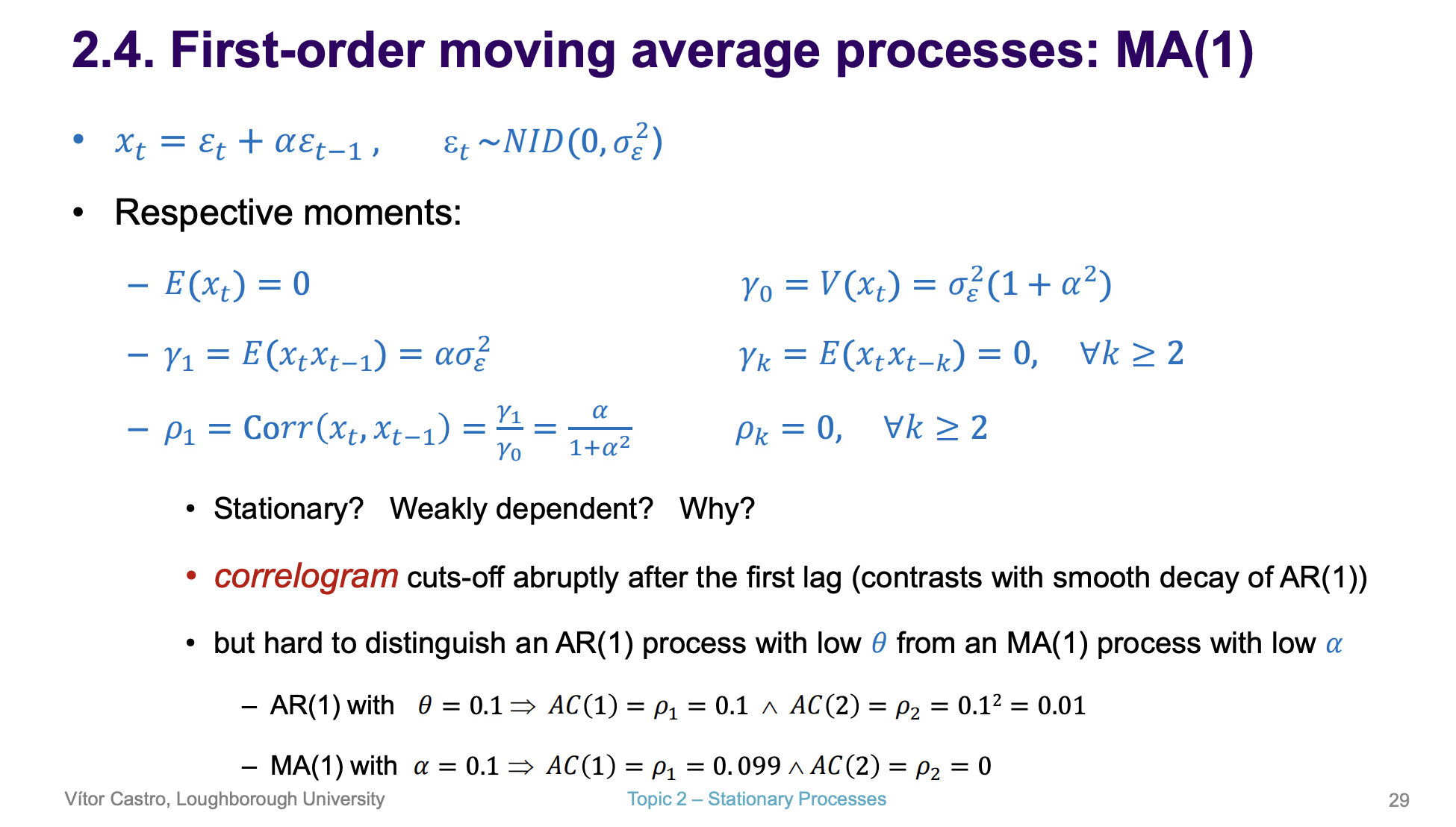

What are the respective moment in a MA(1) model

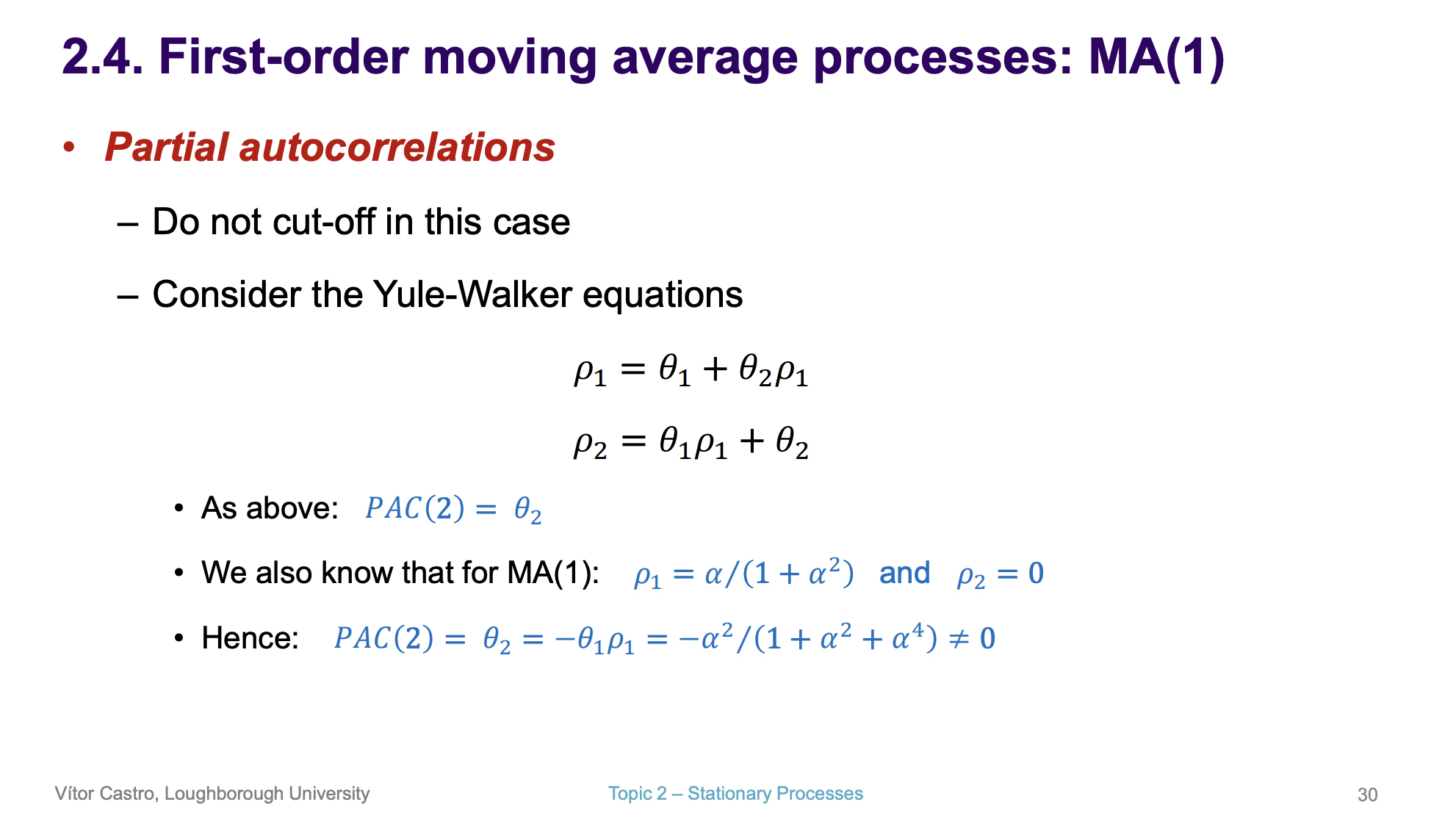

What do PAC show in a MA(1) model

Cut off after the first lag

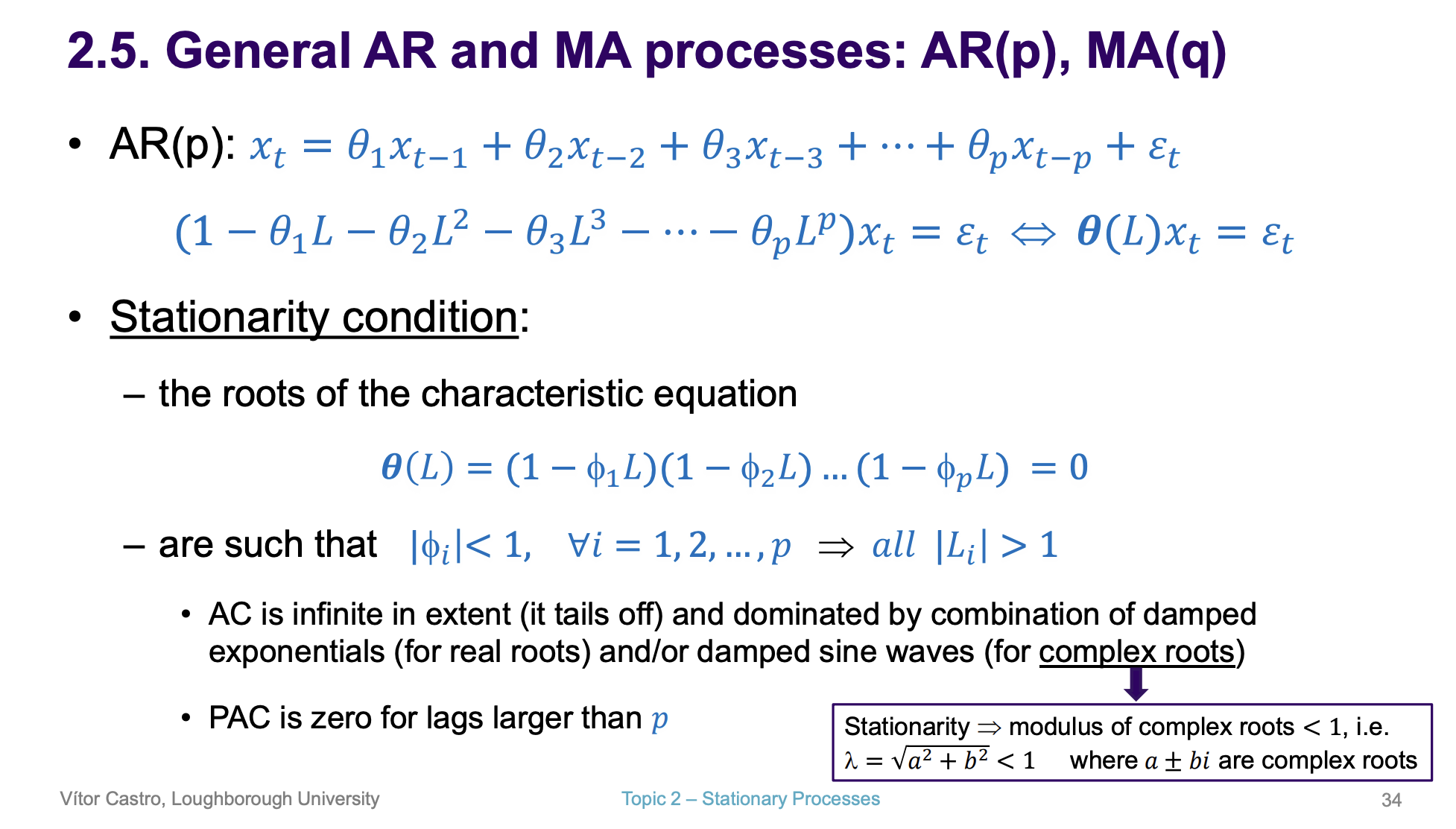

How to take roots in the AR model

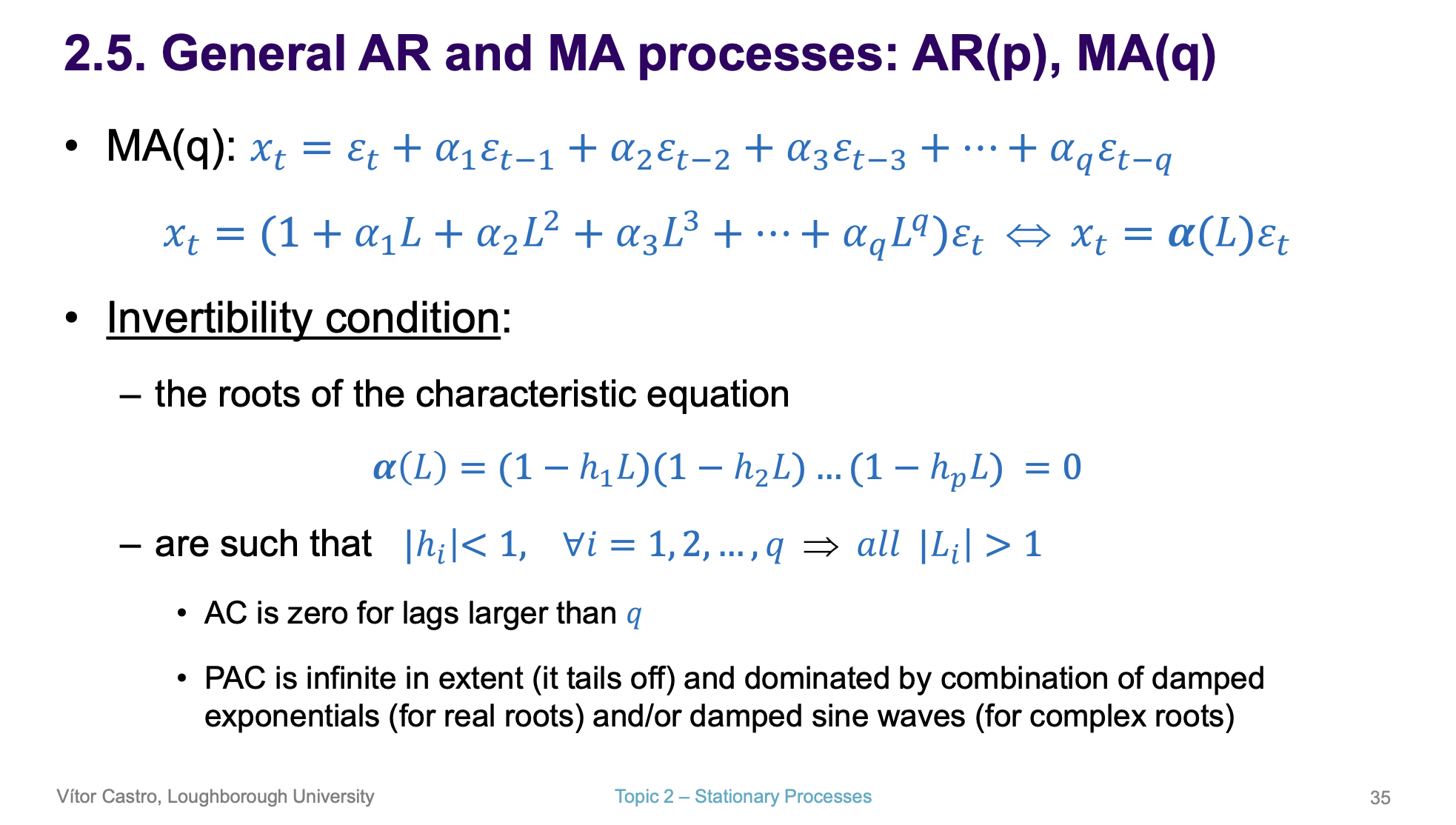

How to take roots in the MA model

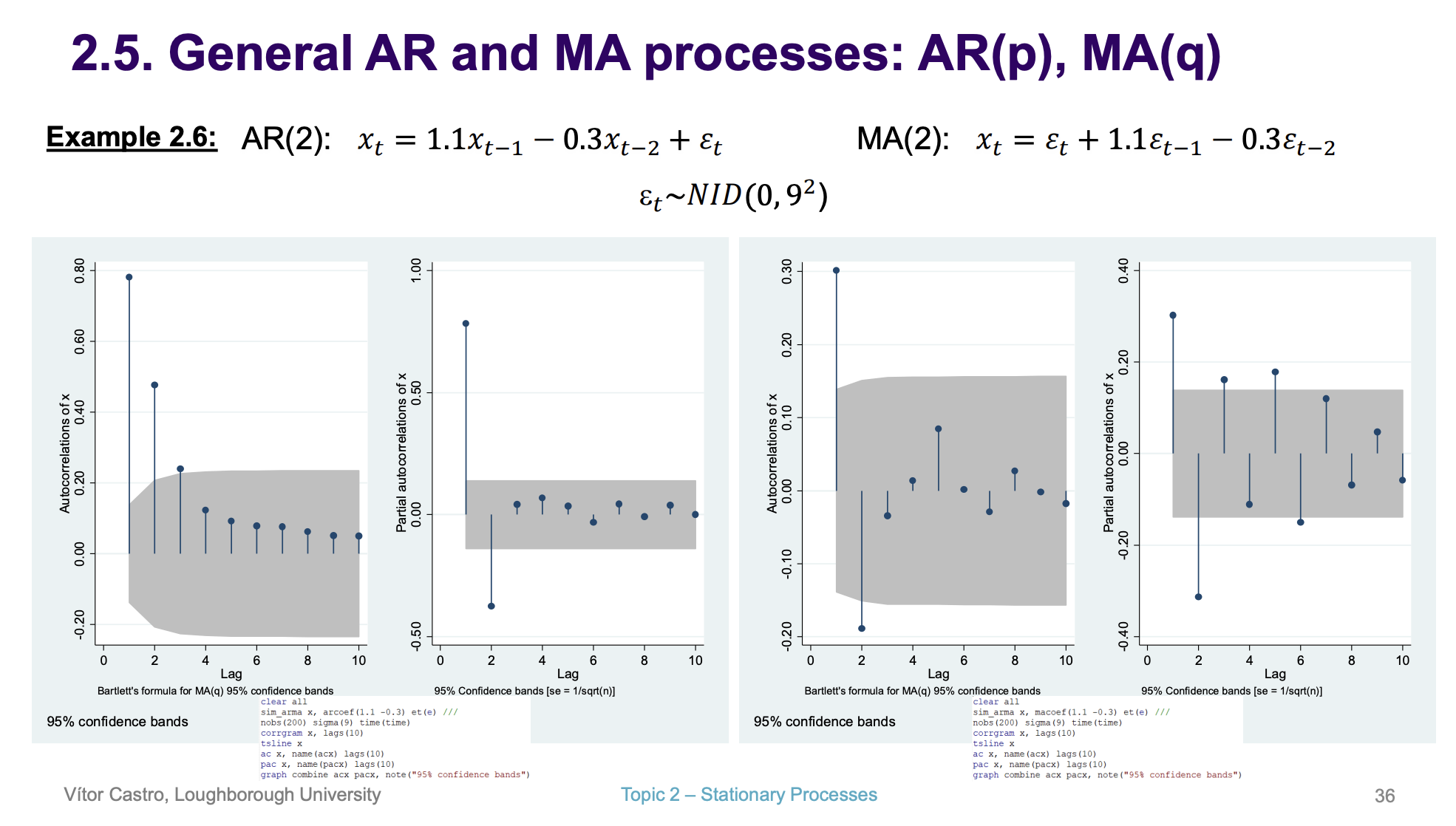

What models are these and why

AR (2) - high AR, PAC two very high and then all cut off to 0 after 2 lags

MR (2) - 2 high ar , then cuts off, while the PAC converges more slowly

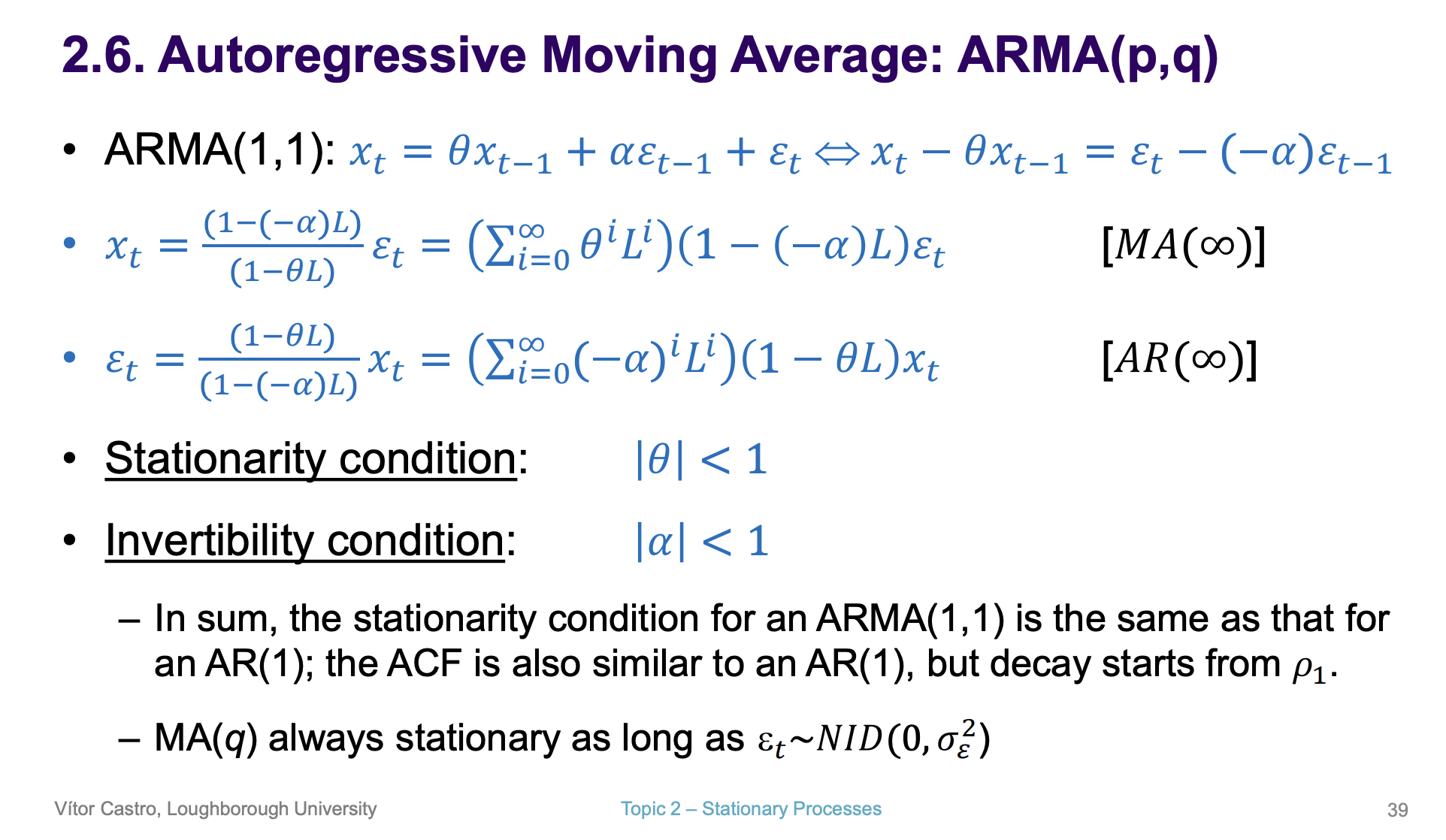

What is the condition for stationary and Invertibility in an ARIMA model