AP Microeconomics Exam Review

1/196

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

197 Terms

Economics

The study of how people, firms, and societies use their scarce productive resources to best satisfy their unlimited wants

Factors of Production

Labor, Land, Capital, Entrepreneurial ability

Physical capital

Manmade equipment like machinery, but also buildings, roads, vehicles, and computers

Entrepreneurial Ability

The effort and know how to put the other resources (Factors of Production) together in a productive venture

Scarcity

The difference between unlimited wants and limited economic resources

Trade-offs

The fact that we are faced with scarce resources implies that individuals, firms, and governments are constantly faced with trade-offs

Opportunity Cost

The opportunity cost of doing something is what you sacrifice to do it (i.e. if you use a scarce resource to pursue activity X, the opportunity cost of activity X is activity Y, the next best use of that resource)

Marginal Analysis

Rational individuals and firms weigh the additional benefits against the additional costs (They think at the margin)

Marginal

"the next one" or "additional" or "incremental"

Marginal Cost

The additional cost incurred from the consumption of the next unit of a good or service

Marginal Benefit

The additional benefit received from the consumption of the next unit of a good or service

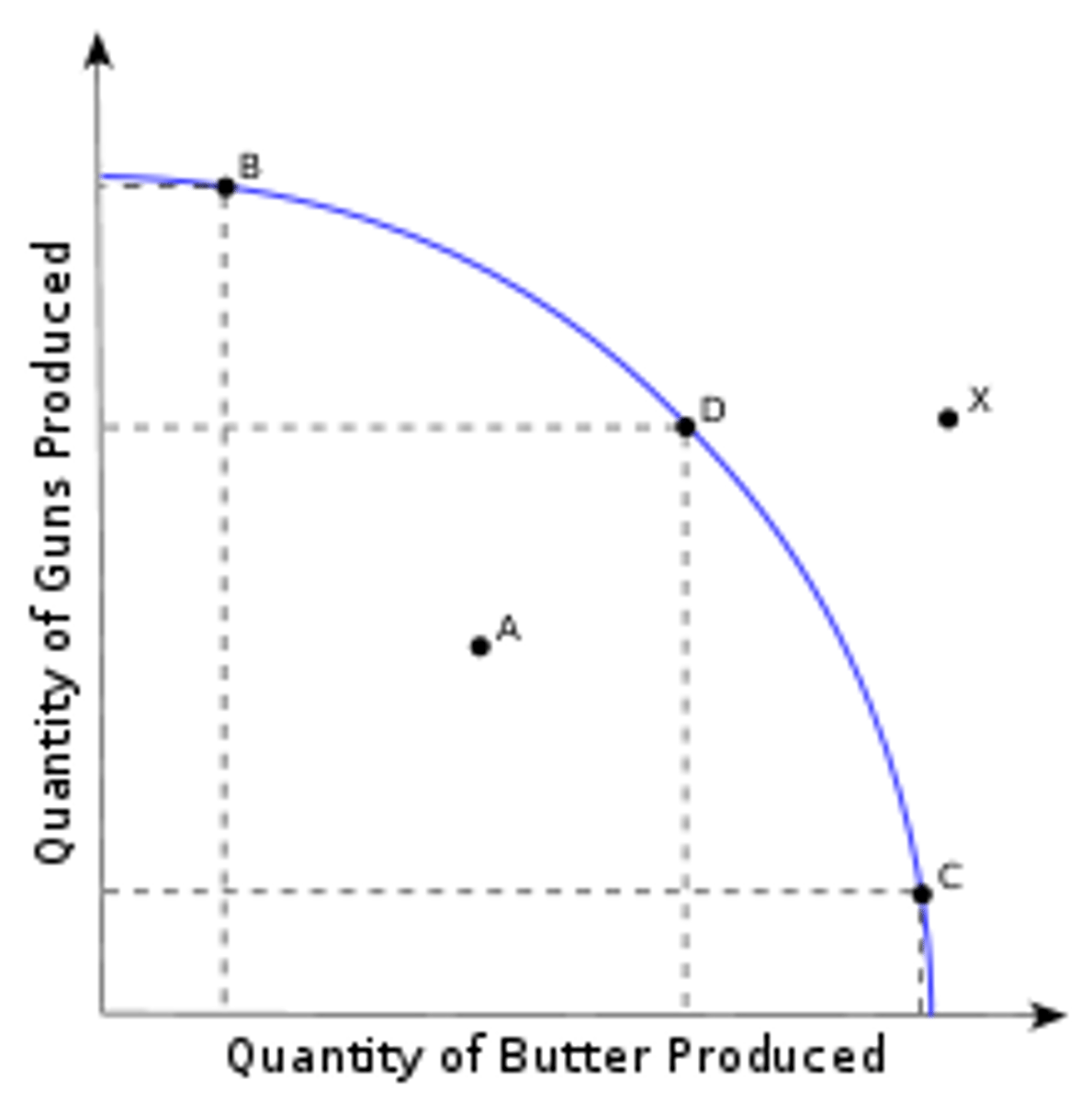

Production Possibilities Curve

A model of an individual or a nation that can choose to allocate its scarce resources between the production of two goods or services, it is assumed that those resources are being fully employed and used efficiently

Points outside of the Production Possibilities Curve

Any point outside the frontier is currently unattainable

The slope of the PPF

The slope of the curve measures the opportunity cost of the good on the x axis

The inverse of the slope measures the opportunity cost of the good on the y axis

Shape of a realistic PPF

Concave or bowed outward

Comparative Advantage

The ability to produce goods at a lower opportunity cost that another individual/firm/nation

Specialization

Individuals/firms/nations produce the goods in which they have a comparative advantage

Productive efficiency

The economy is producing the maximum output for a given level of technology and resources (all points on the PPF are productively efficient)

Allocative efficiency

The economy is producing the optimal mix of goods and services (the combination of goods and services that provides the most net benefit to society; the best point on the PPF)

Substitution effect

The change in quantity demanded resulting from a change in the price of one good relative to the price of other goods

Income effect

The change in quantity demanded resulting from a change in the consumer purchasing power (real income)

Determinants of Demand

-Consumer income

-The price of a substitute good

-The price of a complimentary good

-Consumer tastes and preferences for the good

-Consumer expectations about the future price of the good

-The number of buyers in the market for that specific good

Normal Good

A good for which higher income increases demand

Inferior Good

A good for which higher income decreases demand

Substitute Goods

Two goods are substitute goods if the consumer can use either to satisfy the same essential function, therefore experiencing the same degree of happiness (utility)

Price of Complementary Goods

If any two goods are compliments and the price of one good X falls (rises), the consumer demand for the complement good Y increases (decreases)

Determinants of Supply

-The cost of an input

-Technology and productivity

-Taxes and subsidies on a good

-Producer expectations about future prices

-The price of other goods that could be produced

-The number of producers in the industry

Taxes and Subsidies

A per unit tax is treated by firms as an additional cost of production and would therefore decrease the supply cure, or shift it leftward

A per unit subsidy lowers the per unit cost of production and therefore shifts the supply curve rightward

Market Equilibrium

The market is in this state when the quantity supplied equals the quantity demanded at a given price

Shortage

this exists at a market price when the quantity demanded exceeds the quantity supplied, can be the result of a price ceiling

Surplus

this exists at a market price when the quantity supplied exceeds the quantity demanded, this can be the result of a price floor(such as setting a minimum wage)

Simultaneous Changes in Demand and Supply

When both demand and supply are changing, one of the equilibrium outcomes (price or quantity) is predictable and one is indeterminant

Consumer Surplus

The difference between your willingness to pay and the price you actually pay

Producer Surplus

The difference between the price received and the marginal cost of producing the good

Consumer Surplus on the Graph

The area under the demand curve and above the market price is equal to total consumer surplus

Producer Surplus on the Graph

The area above the supply curve and below the market price is equal to total producer surplus

Elasticity

Measures the sensitivity, or responsiveness, of a choice to a change in an external factor

Price Elasticity of Demand

Measures the sensitivity of consumer quantity demanded for good X when the price of good X changes

Price Elasticity Formula

Ed= (%change in quantity demanded of good X)/(%change in the price of good X)

A good is price elastic if...

If Ed > 1

A good is unit price elastic if...

If Ed = 1

A good is price inelastic if...

If Ed < 1

Elasticity on the Demand Curve

Above the midpoint demand is price elastic

At the midpoint demand is unit elastic

Below the midpoint the demand is price inelastic

Delta Percentage

Delta Percentage = [final cost - initial cost]/initial cost

Perfectly Inelastic

Any increase in the price results in no decrease in the quantity demanded

Perfectly Elastic

A decrease in the price causes the quantity demanded to increase without limits

As the demand curve becomes more vertical

The price elasticity falls and consumers become more price inelastic

As the demand curve becomes more horizontal

The price elasticity increases and consumers become more price elastic

Determinants of Elasticity

-Number of Good Substitutes

-Proportion of Income

-Time

Number of Good Substitutes

If the price of good X increase, and many (few) substitutes exist, the decrease in quantity demanded can be quite elastic (inelastic)

Proportion of Income

If the price of a good increases, the consumer loses purchasing power. If that good takes up a large (small) portion of the consumers income his responsiveness will be significant (insignificant), or elastic (inelastic)

Time

it is expected that price elasticity increases (decreases) as more (less) time passes after the initial increase in price

Total Revenue

TR = Price * Quantity Demanded

Total Revenue and Elasticity

If demand is inelastic TR increases with a price increase

If demand is elastic TR decreases with a price increases

If demand is unit elastic TR stays the same

Income Elasticity

A measure of how sensitive consumption of good X is to a change in a consumer's income

Income Elasticity Formula

Ei = (%change Qd good X) / (%change income)

Luxury vs. Necessity vs. Inferior goods

If Ei > 1, the good is normal and income elastic (luxury)

If 1 > Ei > 0, the good is normal but income inelastic (a necessity)

If Ei < 0, the good is inferior

Cross-Price Elasticity of Demand

The sensitivity of consumption of good X to a change in the price of good Y

Cross-Price Elasticity of Demand Formula

Ex,y = (%change Qd good X) / (%change Price good Y)

Compliments vs. Substitutes

A cross-price elasticity of demand less than zero identifies a complementary good

A cross-price elasticity of demand greater than zero identifies a substitute good

Price Elasticity of Supply

Measures the sensitivity of quantity supplied for good X when the price of good X changes

Price Elasticity of Supply Formula

Es = (%change in quantity supplied of good X) / (%change in the price of good X)

Price Elasticity of Supply over time

Because suppliers, once the price of a good has changed, usually cannot quickly change the quantity supplied, economists predict that the price elasticity of supply increase as time passes

Excise Taxes

A per-unit tax on production results in a vertical shift in the supply curve by the amount of the tax

Incidence of Tax

The proportion of the tax paid by consumers in the form of a higher price for the taxed good is greater if demand for the good is inelastic and supply is elastic

Dead weight loss

The lost net benefit to society caused by a movement away from the competitive market equilibrium. Policies like excise taxes create lost welfare to society

Deadweight loss and Elasticity

Deadweight loss increases as the demand or supply curves become more elastic

Subsidies

Has the opposite effect of an excise tax, as it lowers the marginal cost of production, resulting in a downward vertical shift in the supply curve for good X

Price Floors

A legal minimum price below which the product cannot be sold. If a floor is installed at some level above the equilibrium, it creates a permanent surplus

Price Ceilings

A legal maximum price above which the product cannot be sold. If a ceiling is installed at a level below the equilibrium price, it creates a permanent shortage

Utility

Happiness, benefit, satisfaction, or enjoyment gained from consumption

Total Utility

The total amount of happiness received from the consumption od a certain amount of a good

Marginal Utility

The additional utility received (or sometimes lost) from the consumption of the next unit of a good

Marginal Utility Formula

Mu = (%change Total Utility) / (%change Quantity)

Utils

A unit of measurement often used to quantify utility

Utility and Rational Decisions

Even if the monetary price of good X is zero, the rational consumer stops consuming good X at the pint where total utility is maximized

Law of Diminishing Marginal Utility

States that in a given time period, the marginal utility from consumption of one more of that item falls

Constrained Utility Maximization

For a one-good case. Constrained by prices and income, a consumer stops consuming a good when the price paid for the next unit is equal to the marginal benefit received

Utility Maximizing Rule

The consumer maximizes utility when they choose amounts of goods X and Y, with their limited income, so that the marginal utility per dollar spent is equal for both goods

Utility Maximizing Rule Formula

MUx/Px = MUy/Py or MUx/MUy = Px/Py

Deriving the Demand Curve from Utility

Utility maximizing behavior of individuals creates individual demand curves

Summing the quantity demanded by individuals at each price creates market demand curves

Firm

An organization that employs factors of production to produce a good or service that it hopes to profitably sell

Explicit Costs

direct, purchased, out-of-pocket costs paid to resource suppliers outside the firm (Also called accounting costs)

Implicit Costs

Indirect, non purchased, or opportunity costs of resources provided by the entrepreneur (Also called economic costs)

Accounting Profits

The difference between total revenue and total explicit costs

Economic Profits

The difference between total revenue and total explicit and implicit costs

Short-run

A period of time too short to change the size of the plant, but many other, more variable resources can be adjusted to meet demand

Long-run

A period of time long enough to alter the plant size. New firms can enter the industry and existing firms can liquidate and exit

Characteristics of Firms in the Short-run

Plant size: Fixed

Fixed Cost: Some

Variable Costs: Some

Entry/Exit of Firms: None

Characteristics of Firms in the Long-run

Plant size: Variable

Fixed Cost: None

Variable Costs: All

Entry/Exit of Firms: Yes

Production Function

The mechanism for combining production resources, with existing technology, into finished goods and services, Inputs are turned into outputs

Fixed Inputs

Production inputs cannot be changed in the short run. Usually this is the plant size or capital

Variable Inputs

Production inputs that the firm can adjust in the short run to meet changes in demand for their output. Often this is labor and/or raw materials

Total Product (of Labor)

The total quantity, or total output, of a good produced at each quantity of labor employed

Marginal Product (of Labor)

The change in the total product resulting from a change in the labor input. MP = change in TP / change in Labor. If labor is changing one unit at a time, MP = change in TP

Average Product (of Labor)

Total product divided by the amount of labor employed. AP = TP / L

Law of Diminishing Returns

As successive units of a variable resource are added to a fixed resource, beyond some point marginal product falls

Increasing Marginal Returns

MP is increasing as Labor increases

Diminishing Marginal Returns

MP decreases as Labor increases

Negative Marginal Returns

MP becomes negative as Labor increases