ACC 403 Chapter 7

1/54

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

55 Terms

What are the typical activities in the revenue and collection cycle for a manufacturing company?

Receiving orders, delivering goods, billing customers, collecting cash.

What is a bill of lading?

A contract between the shipper and the carrier, including shipping information.

What is a packing slip?

A document included with a shipment showing the description and quantity of goods.

What is a sales invoice?

A bill sent to customers for payment showing the amount due and payment terms.

What is the purpose of the customer master file?

To list approved customers and their credit limits.

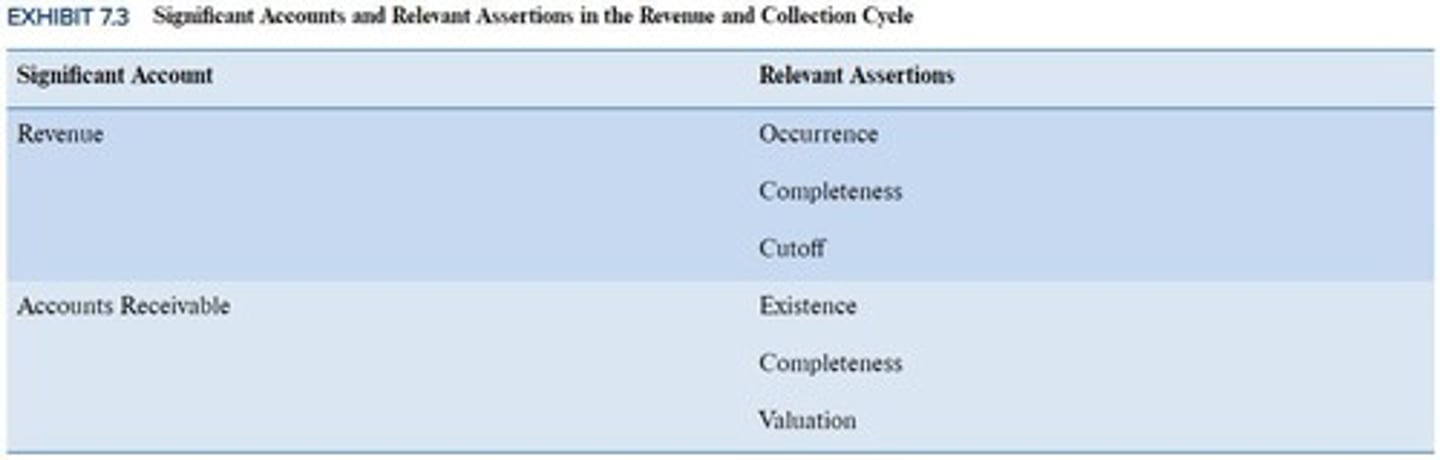

What is the significance of the accounts receivable listing?

It lists customer balances owed and how long receivables have been outstanding.

What are the three primary concerns regarding the risk of material misstatement in the revenue cycle?

Revenue recognition, possibility of returns, collectibility of accounts receivable.

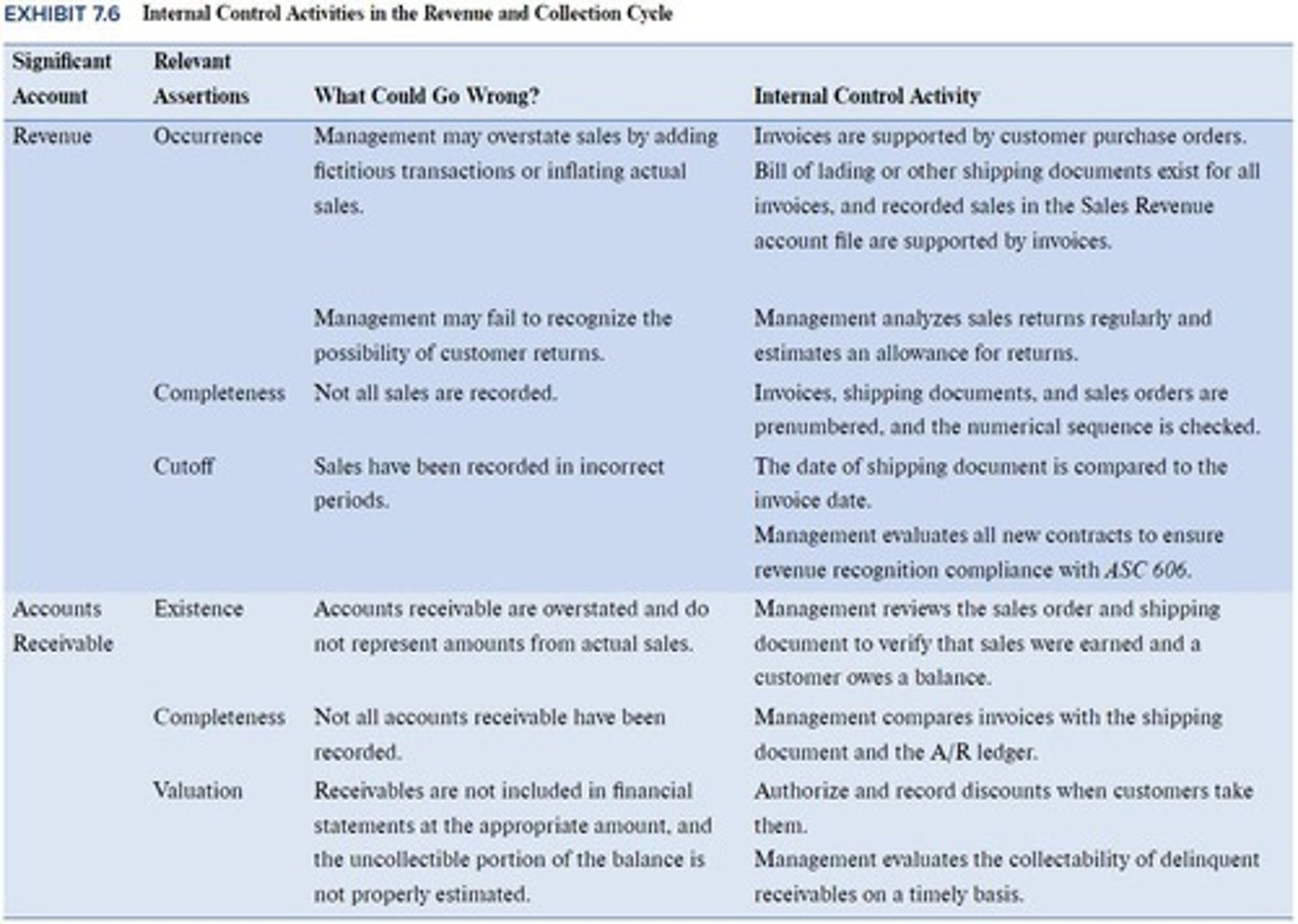

What internal control measure helps prevent sales to fictitious customers?

Authorization of credit sales.

What is the role of prenumbered sales documents?

To ensure completeness and prevent duplicate transactions.

What is the ending balance in Accounts Receivable for Shamrock Corporation at the end of 2025?

To be determined based on sales, collections, and write-offs.

What is the net realizable value of receivables?

The amount expected to be collected from accounts receivable.

What must revenues be for recognition?

Revenues must be realized or realizable and earned.

What are the SEC criteria for revenue recognition?

1. Persuasive evidence of an arrangement exists. 2. Delivery has occurred or services have been rendered. 3. The seller's price to the buyer is fixed or determinable. 4. Collectability is reasonably ensured.

What is the first step in the FASB ASC 606 revenue recognition process?

Identify the contract(s) with a customer.

What is the second step in the FASB ASC 606 revenue recognition process?

Identify the performance obligations in the contract.

What is the third step in the FASB ASC 606 revenue recognition process?

Determine the transaction price.

What is the fourth step in the FASB ASC 606 revenue recognition process?

Allocate the transaction price to the performance obligations in the contract.

What is the fifth step in the FASB ASC 606 revenue recognition process?

Recognize revenue when (or as) the entity satisfies a performance obligation.

What estimates must be made regarding revenue recognition?

Estimates regarding collectability of accounts receivable and customer returns and allowances.

What does the risk of material misstatement equal?

Risk of material misstatement = Inherent Risk (IR) x Control Risk (CR).

What should internal control activities align with?

Internal control activities should align with the 'what could go wrong?' for relevant assertion(s).

What is assessed via the walkthrough in internal control evaluation?

Whether the audit client has designed and implemented a control that would mitigate the identified risk of material misstatement.

What are entity-level controls?

Pervasive controls that are not specific to the revenue cycle, such as audit committee oversight and overall performance reviews by management.

Why is separation of duties critical in the revenue cycle?

It helps prevent or detect material misstatements.

What is a three-way match in the revenue cycle?

A control activity that provides evidence that a sale has been completed and revenue has been earned, involving a purchase order, shipping documents, and invoices.

What does the three-way match ensure?

It ensures the existence of accounts receivable and the occurrence of revenue.

What is the purpose of prenumbering sales invoices?

To provide evidence that sales transactions have not been missed, ensuring completeness of accounts receivable (AR) and revenue.

Why is it important to compare ship dates to invoice dates?

To provide evidence that sales transactions have been recorded in the correct period, ensuring completeness of AR and revenue (cutoff).

What is a three-way match in the context of internal controls?

An automated control that compares purchase orders, receiving reports, and invoices to ensure accuracy in transactions.

What is one important control activity in the revenue cycle regarding credit sales?

Credit sales are authorized based on the credit limit in the customer master file, affecting the valuation of AR.

How is the collectability of delinquent receivables evaluated?

Regular evaluations are conducted to assess the collectability of delinquent receivables, impacting the valuation of AR.

What does management regularly evaluate in relation to accounts receivable?

The adequacy of allowances for doubtful accounts.

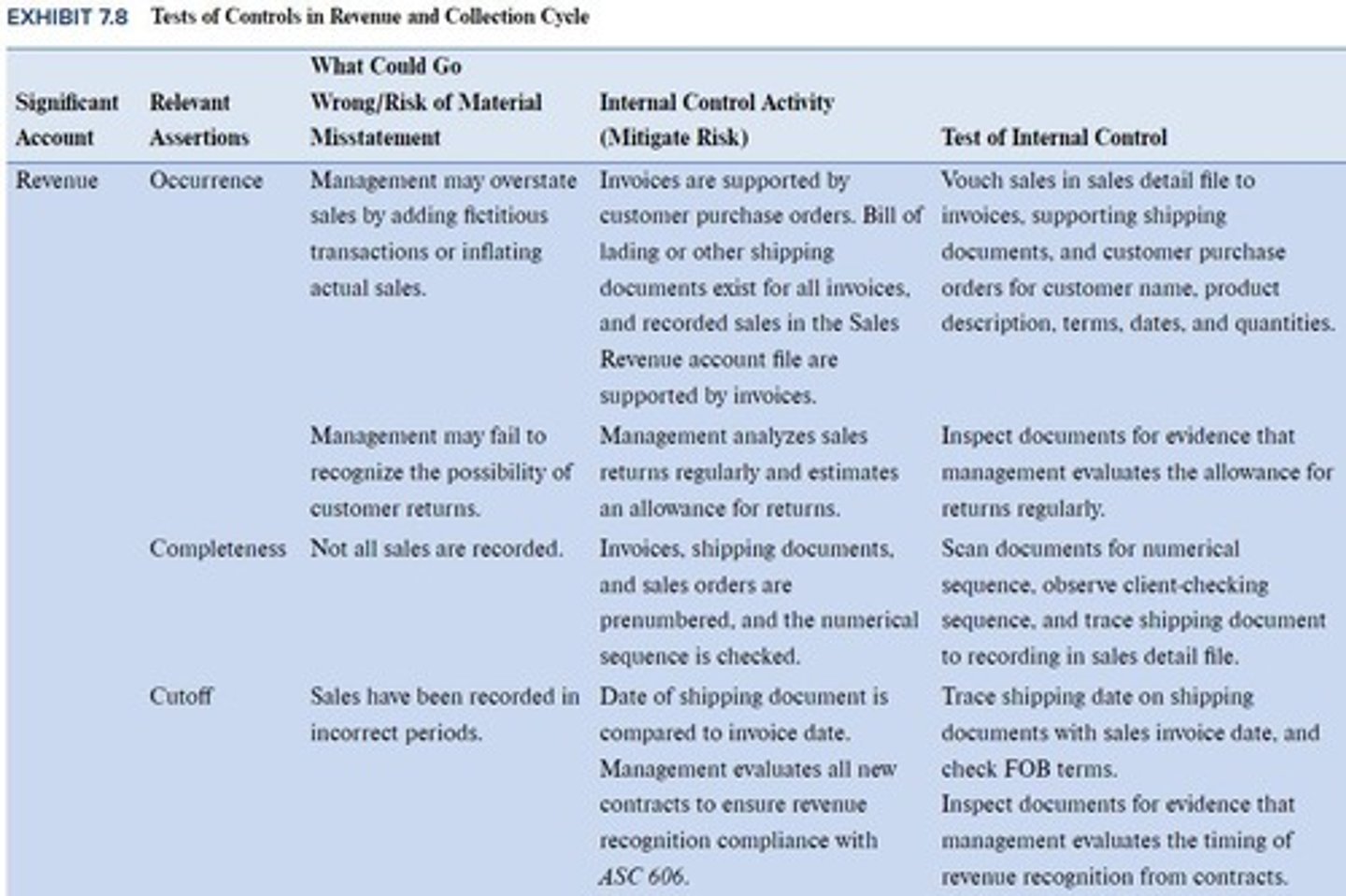

What must an auditor determine to rely on internal controls?

Whether the controls operate as designed.

What are the components of operating effectiveness testing?

Inquiry, observation, inspection of documents, and reperformance.

What is a dual-purpose procedure in auditing?

An audit procedure that serves both the substantive purpose and the test of controls purpose.

What should be done after testing internal controls is complete?

Reassess control risk based on whether controls are functioning as described.

What happens if controls are functioning as described?

Control risk is consistent with the preliminary level, and planned substantive procedures can proceed.

What should be adjusted if controls are not functioning as described?

The planned nature, timing, and/or extent of substantive testing should be adjusted to obtain more persuasive evidence.

What is the focus of the internal controls exercise in the revenue cycle?

To test the boxed controls by selecting a sample of sales invoices.

What is the formula for Accounts Receivable (AR)?

AR = IR x CR x DR (Inherent Risk x Control Risk x Detection Risk)

What are the two types of substantive procedures in the revenue cycle?

Analytical procedures and tests of detail.

What is the purpose of substantive analytical procedures?

To substantiate an account or disclosure by developing an independent estimate and comparing it to the recorded balance.

What are the steps involved in substantive analytical procedures?

1. Develop an independent expectation; 2. Determine the threshold for investigation; 3. Calculate the variance; 4. Investigate variances above the established threshold.

What types of comparisons are made in substantive analytical procedures?

Comparisons of asset and revenue balances with recent history, calculations/ratios to historical data and industry statistics, and account interrelationships.

What must auditors ensure regarding the data used in developing an independent expectation?

Auditors must be comfortable with all data used.

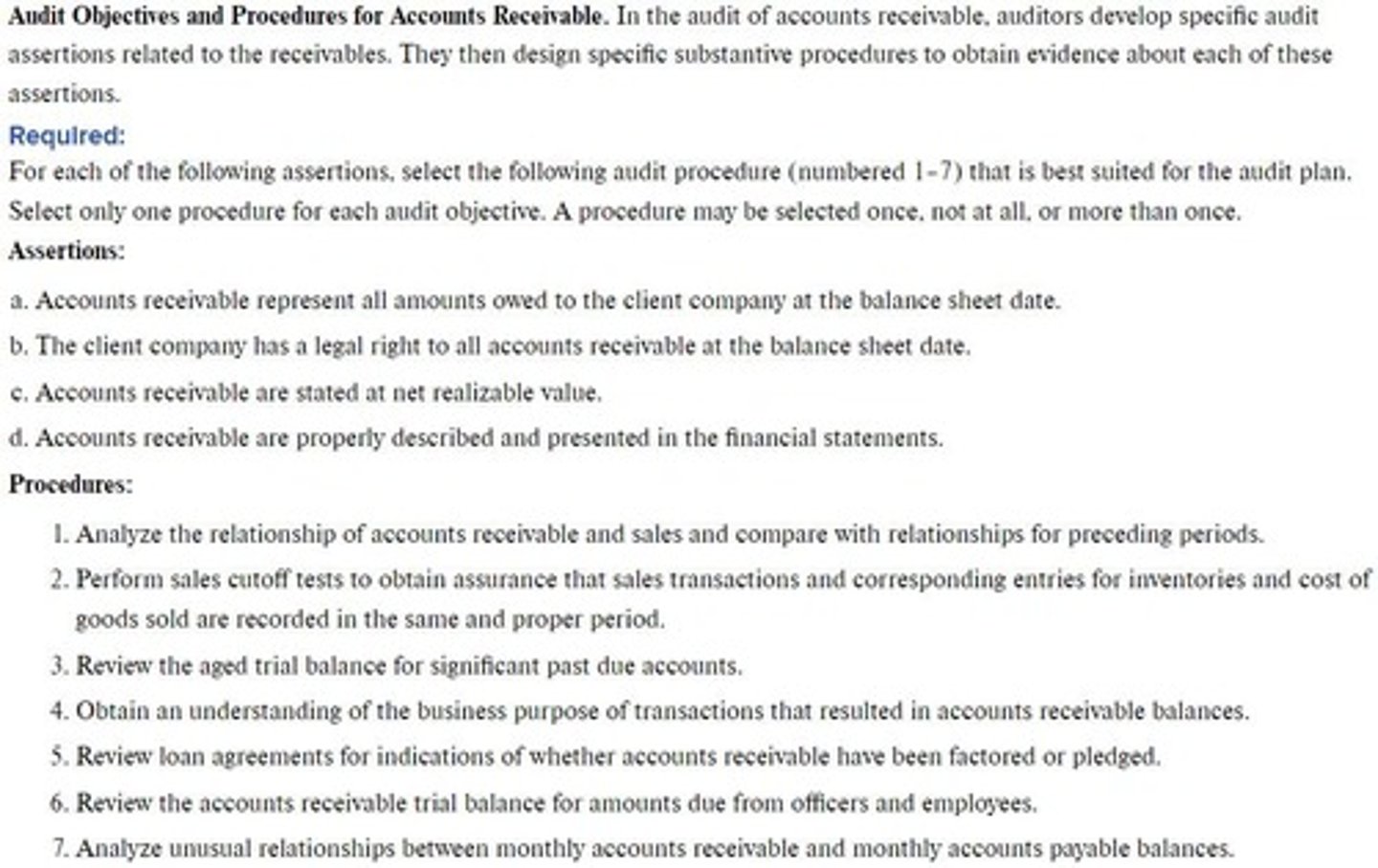

What is the purpose of tests of detail in auditing?

To substantiate an account or disclosure by directly testing the transactions that make up the account.

What is the focus of occurrence tests in revenue?

To vouch details per the sales journal to invoices, shipping documents, and customer purchase orders.

What does completeness testing involve for revenue?

Tracing details per shipping documents to the sales journal and ensuring sales were recorded in the correct period.

What is the existence test for Accounts Receivable?

Confirm accounts receivable with customers, generally required per GAAS.

What does valuation testing for Accounts Receivable assess?

Company policy for the allowance for doubtful accounts and potential collectability issues.

What are the two types of confirmations in auditing?

Positive confirmation (response requested regardless of balance correctness) and negative confirmation (response requested only if balance is incorrect).

What is a key note regarding AR confirmations?

AR confirmations are mostly manual and auditors must control the entire confirmation process.

What should auditors do if they receive non-responses to confirmations?

Follow up with second and third requests and perform alternative procedures, such as reviewing subsequent cash receipts.

What is the significance of the presumptive risk of fraud in revenue recognition?

It is considered a significant risk that requires careful substantive testing.

What is the next topic to be covered in the auditing class?

Audit Sampling.