Summary - C1-7

1/34

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

35 Terms

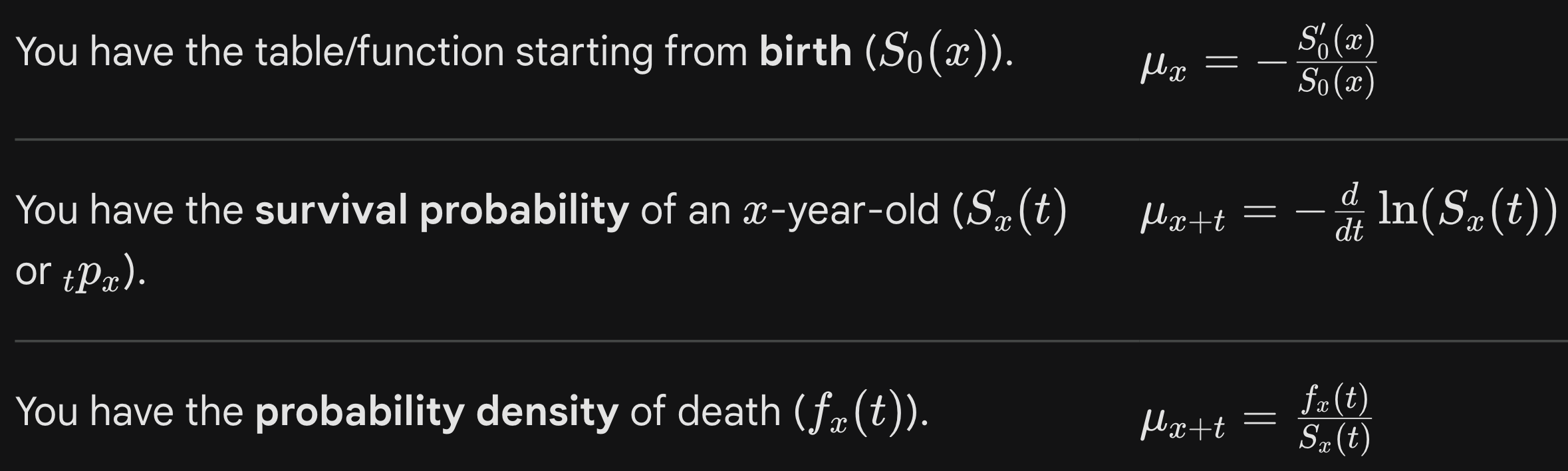

μx =

μx+t =

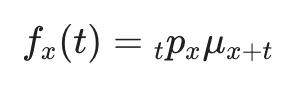

fx(t) =

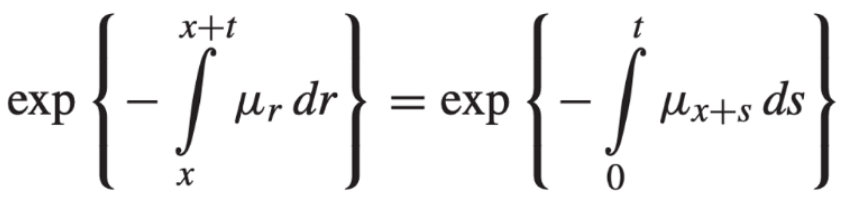

tpx =

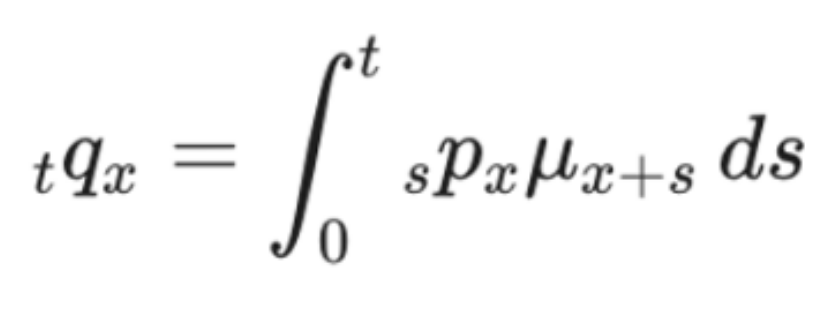

tqx =

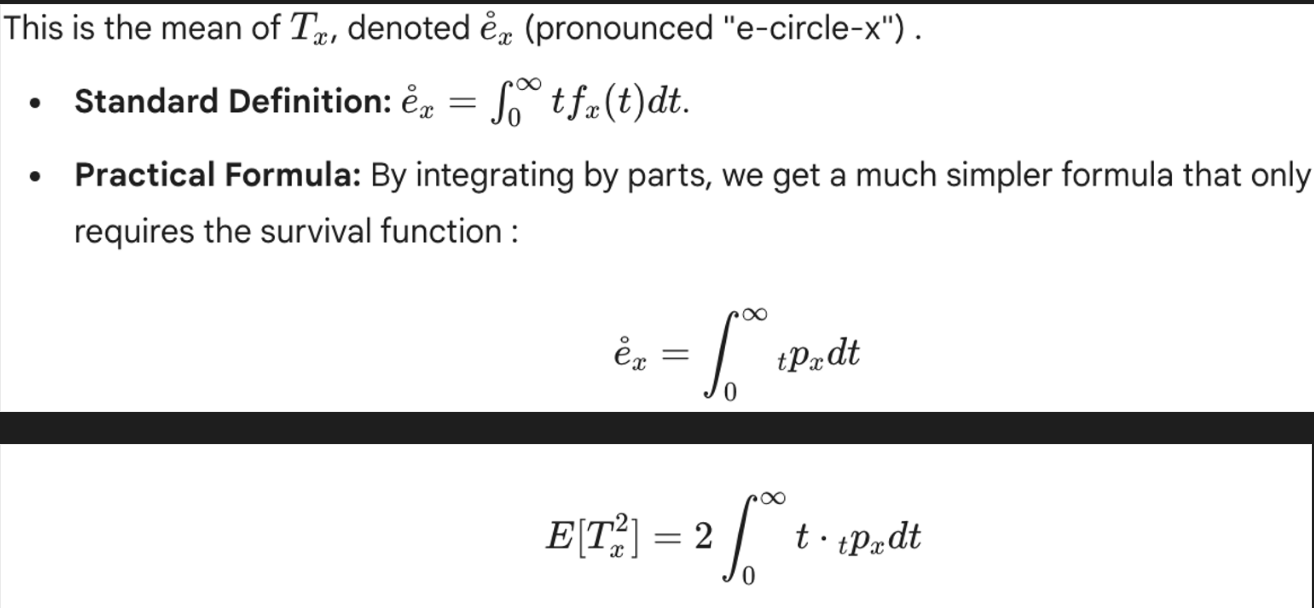

E[Tx] =

E[Tx2] =

Complete Expectation of Life

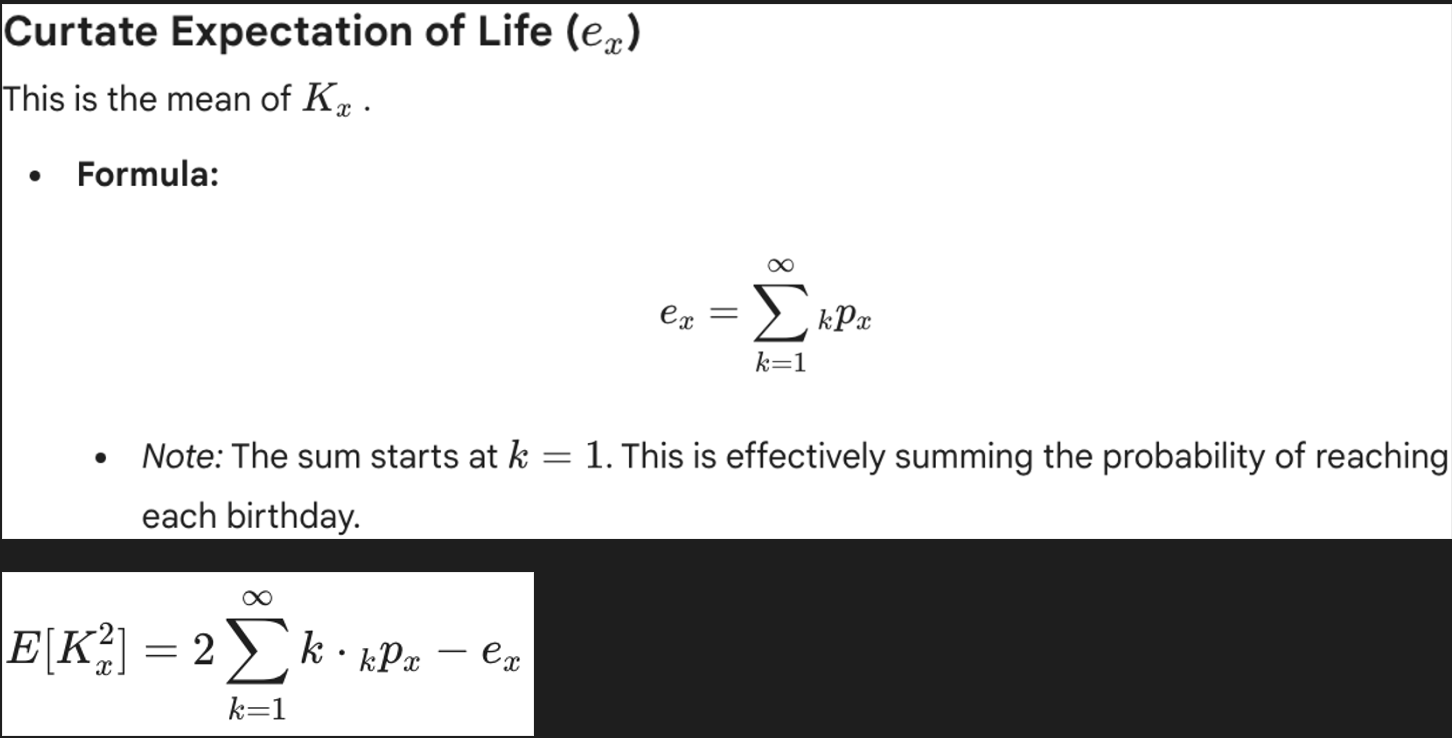

E[Kx] =

E[Kx2] =

Curtate Expectation of Life

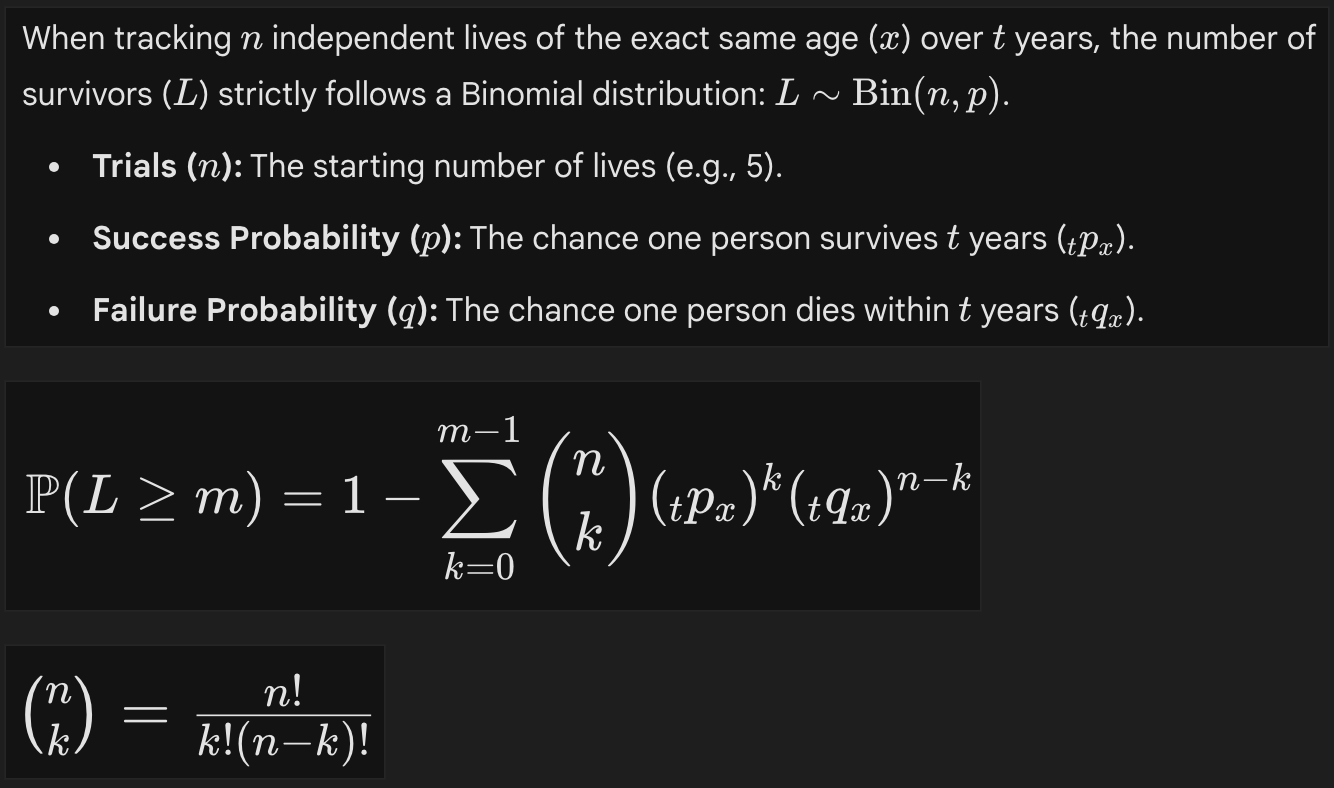

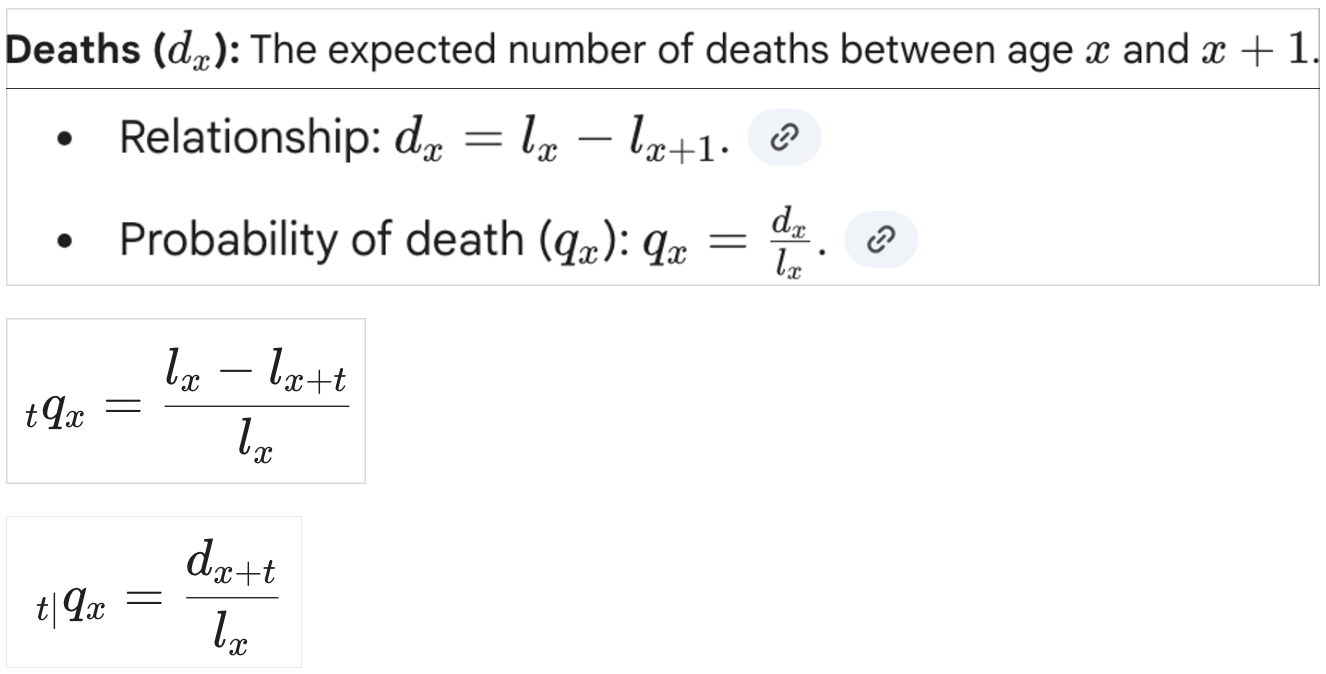

Number of survivors/death calculations

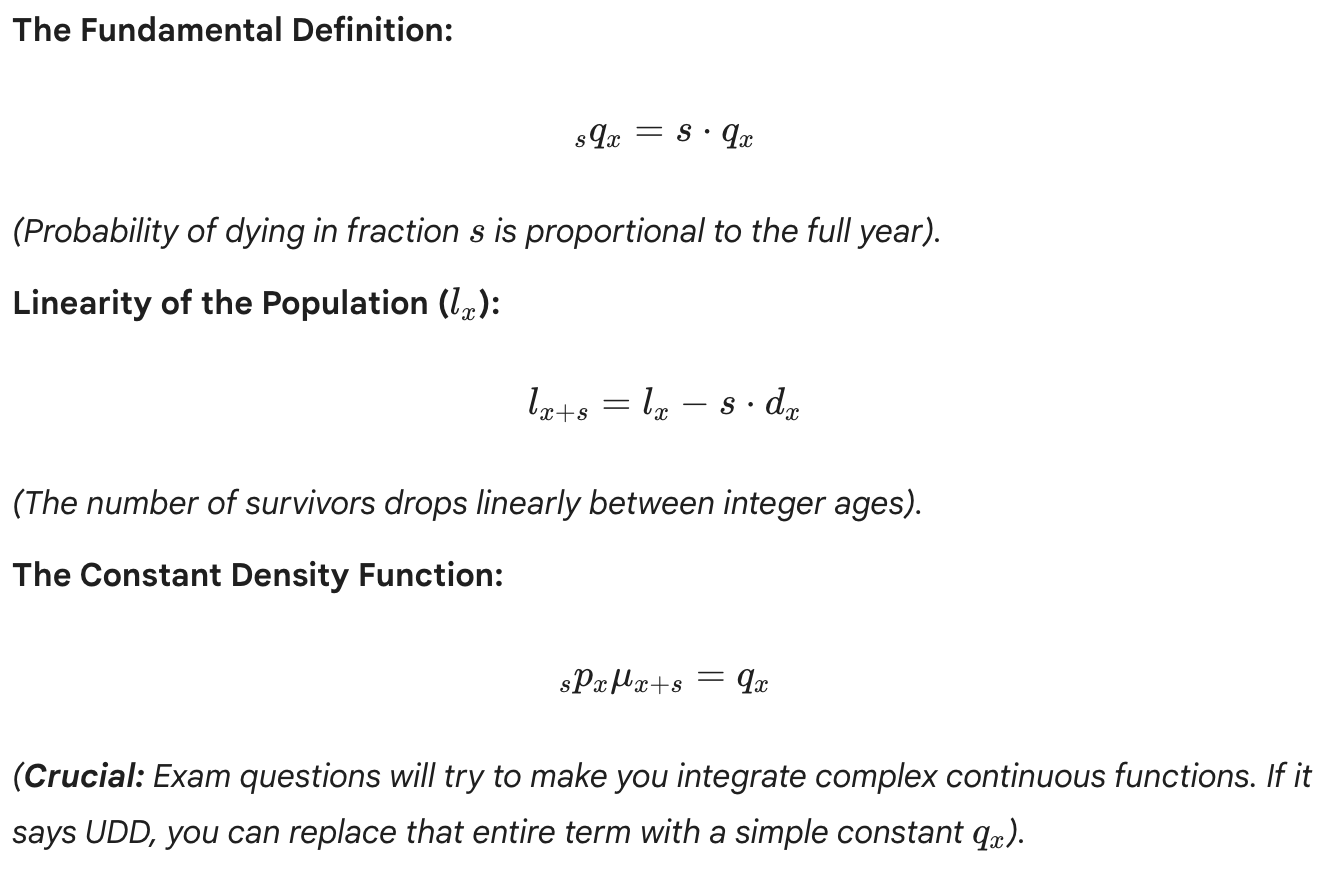

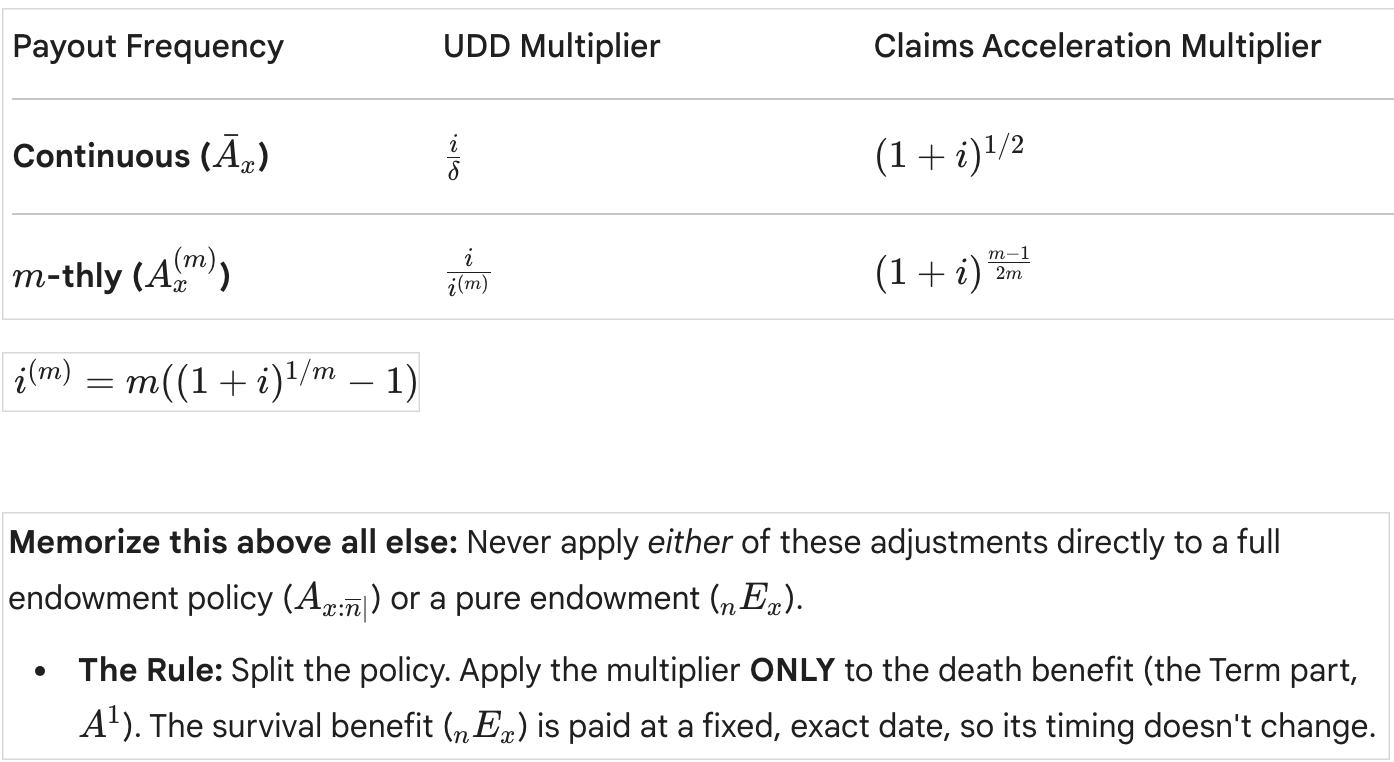

UDD

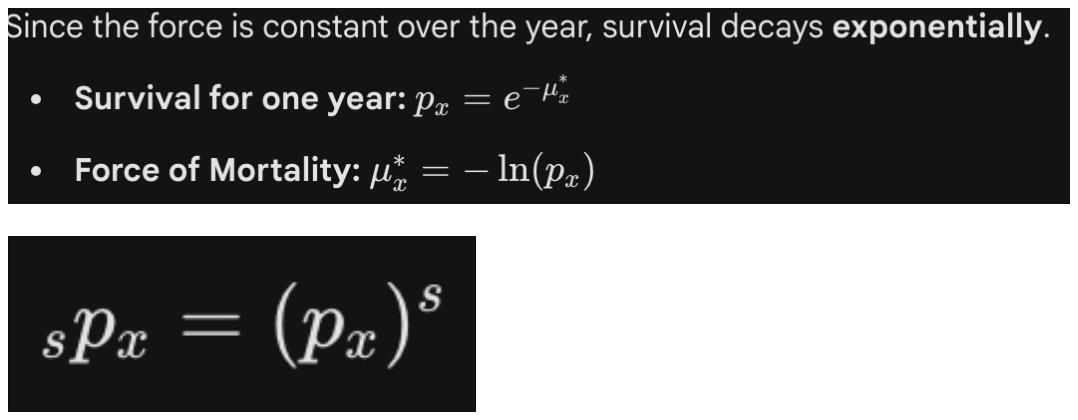

CFM

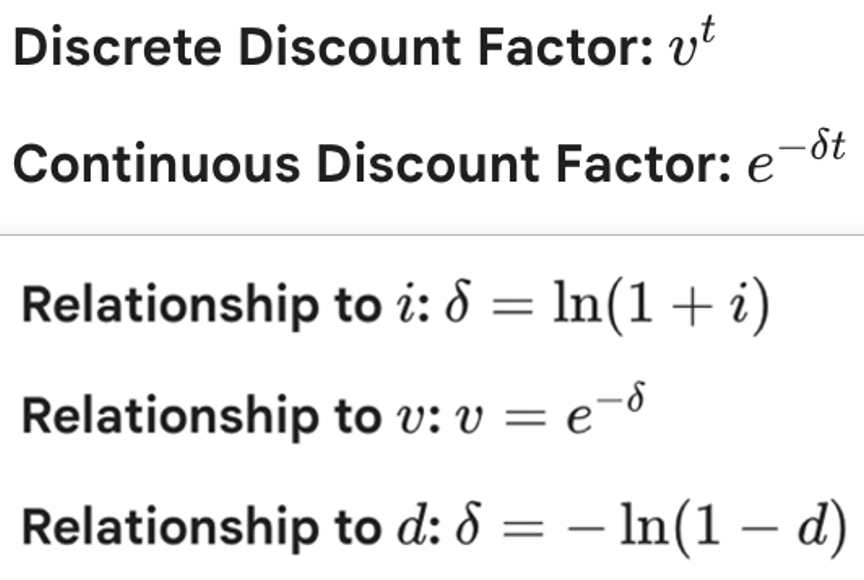

Discount Factor

Discrete vs Continuous

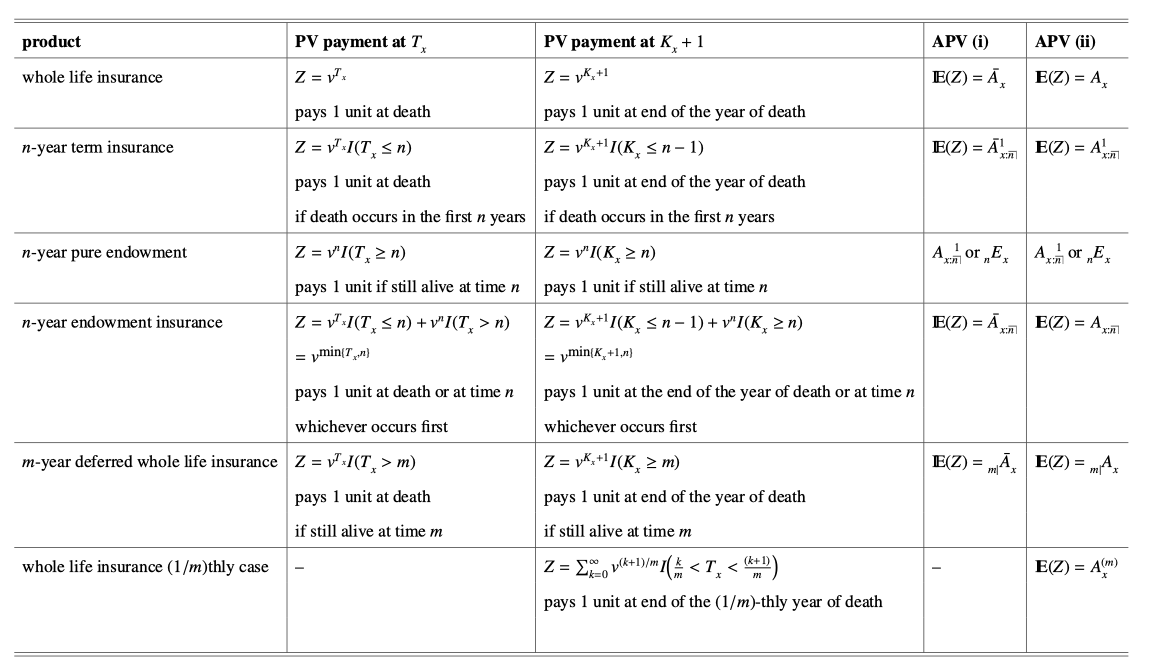

Life Insurance Overview

PV (cont, discrete) + symbol for APV

EPV

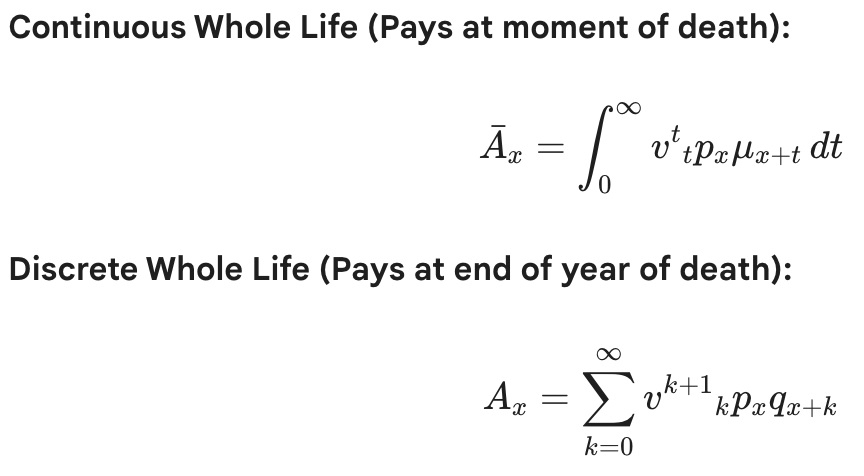

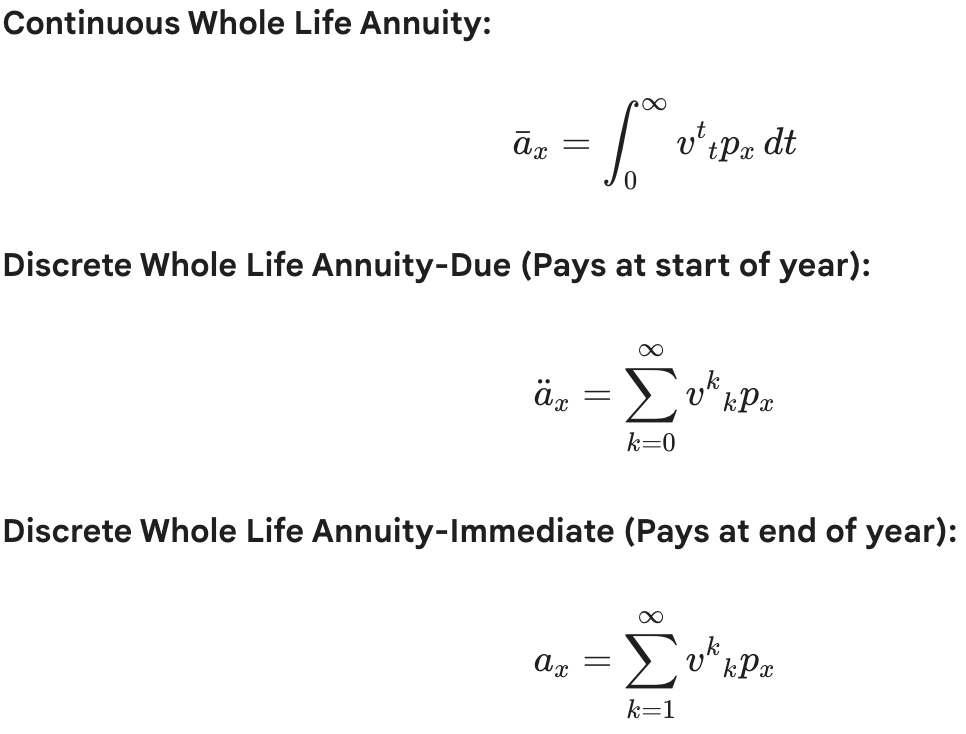

Continuous Whole Life

Discrete Whole Life

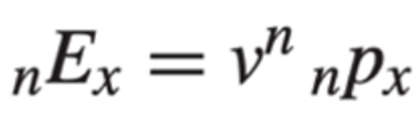

Pure Endowment

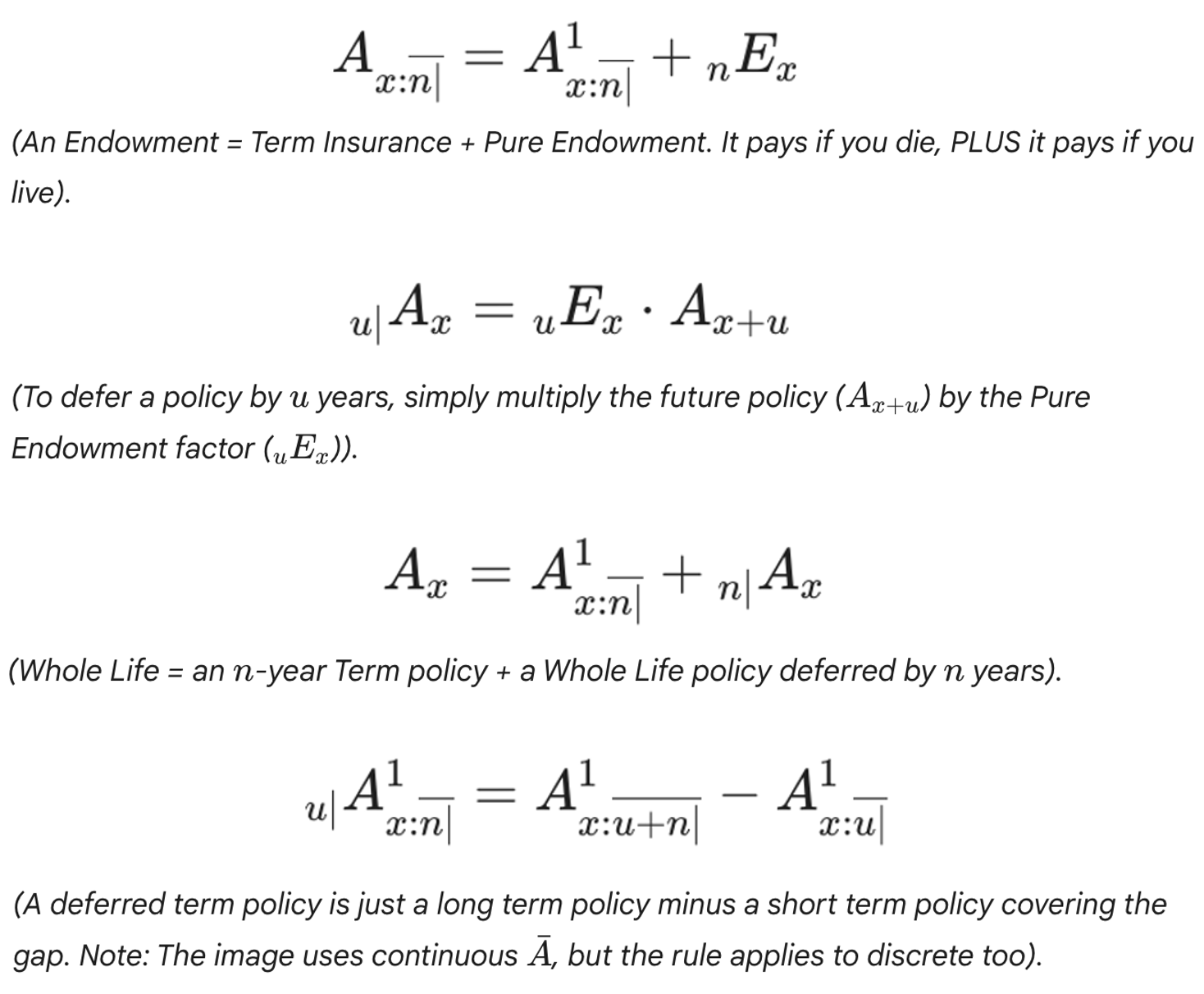

Life Insurance Relationships

UDD & CA

Life Insurances

Second Moment

EPV:

Continuous Whole Life Annuity

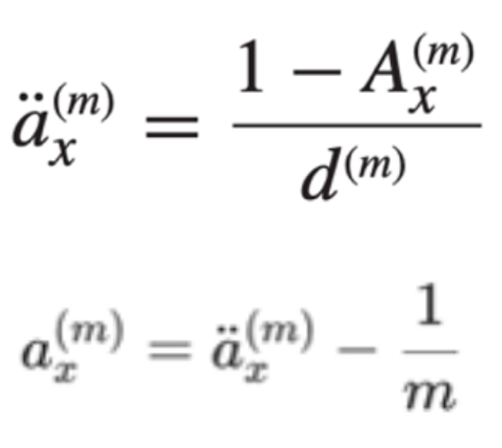

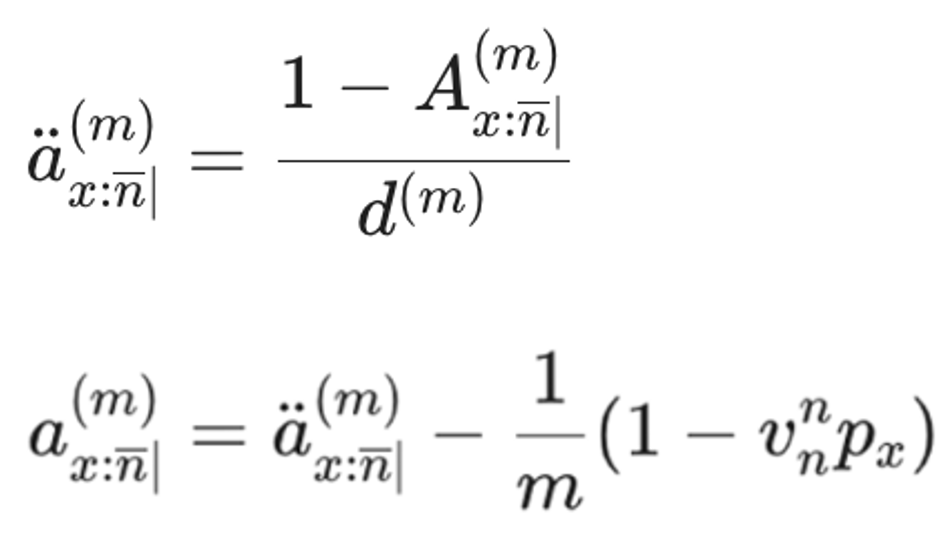

Whole Life Annuity-Due

Whole Life Annuity-Immediate

EPV:

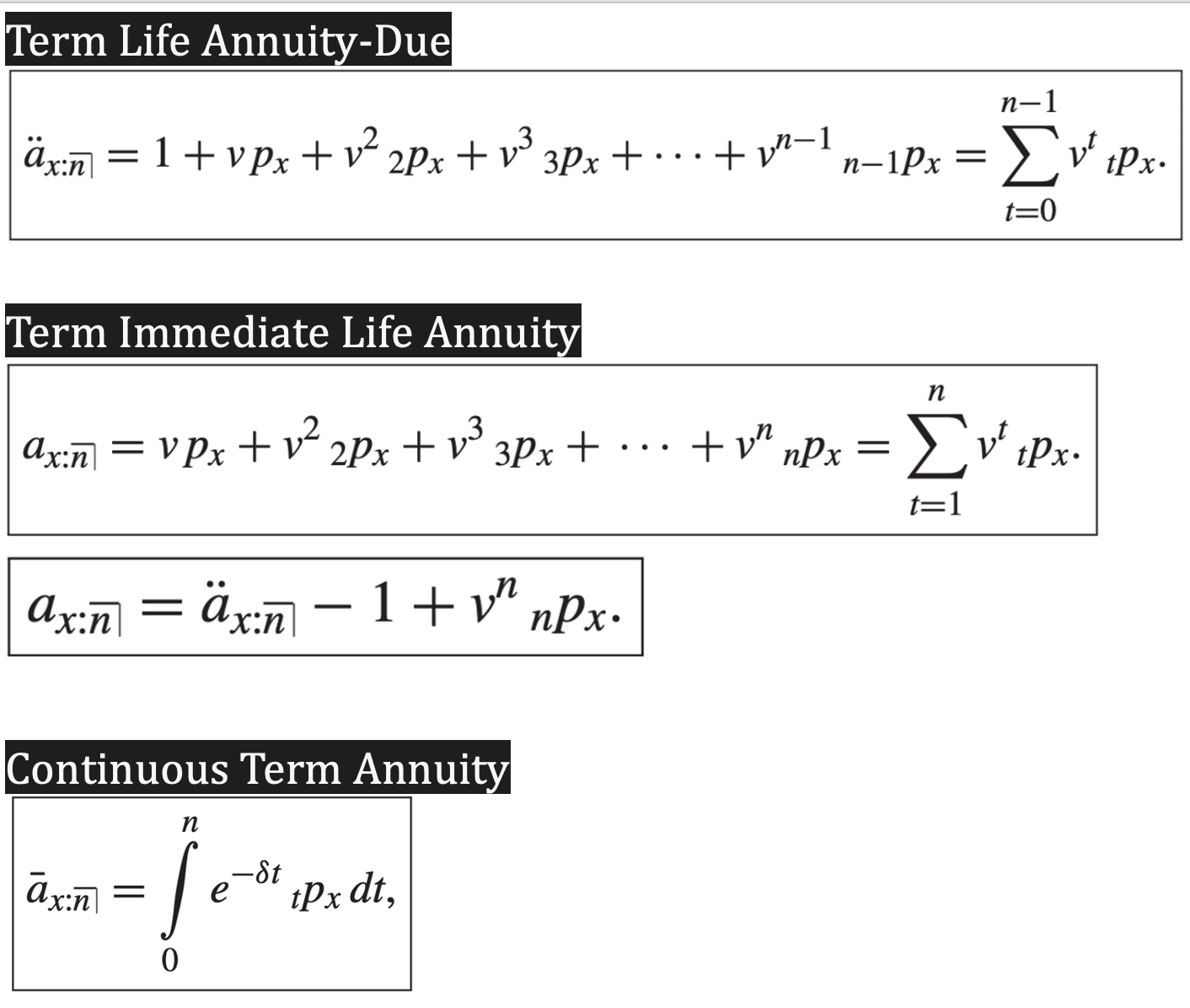

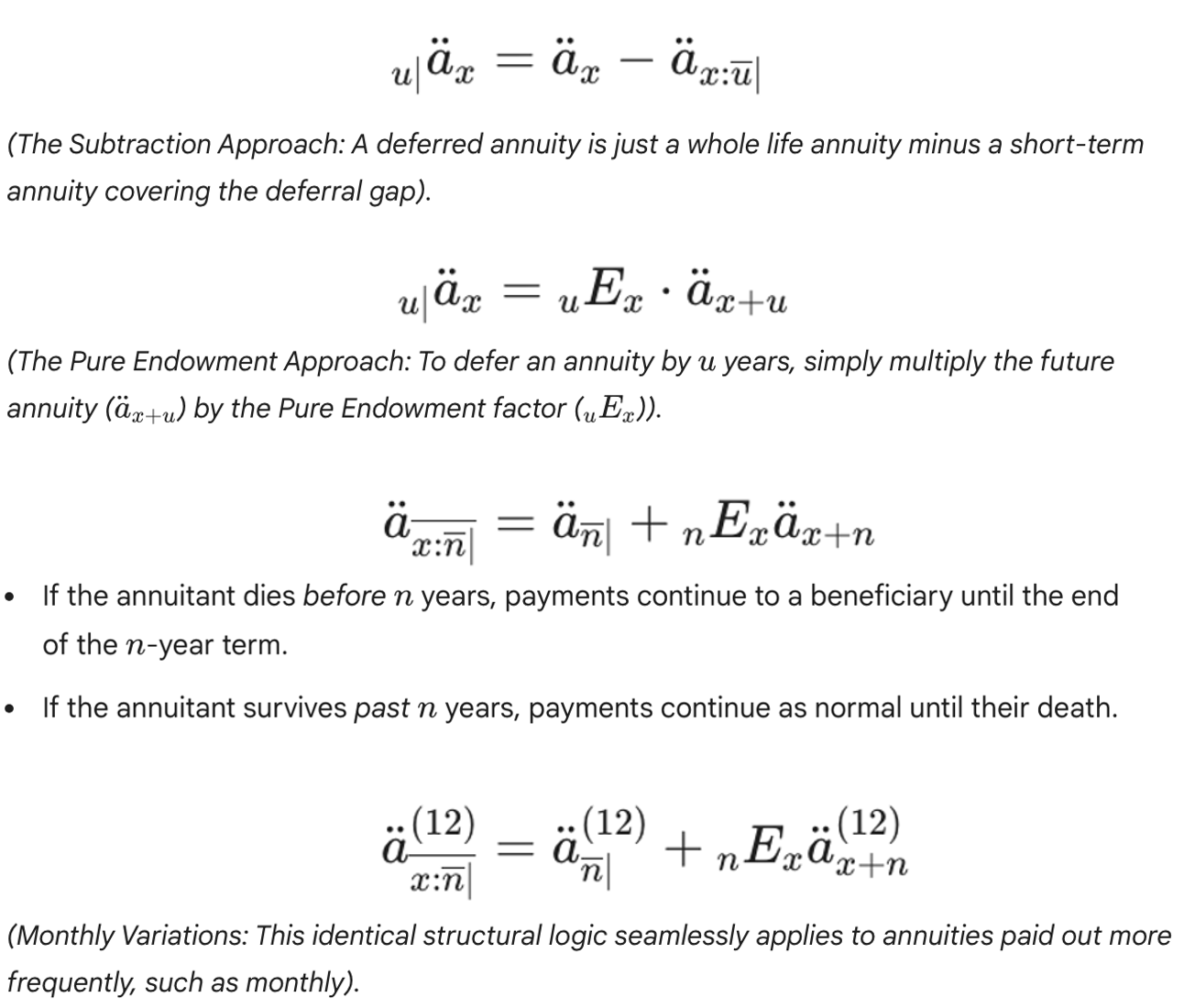

Term Life Annuity-Due

Term Life Annuity-Immediate

Continuous Term Life Annuity

Annuities

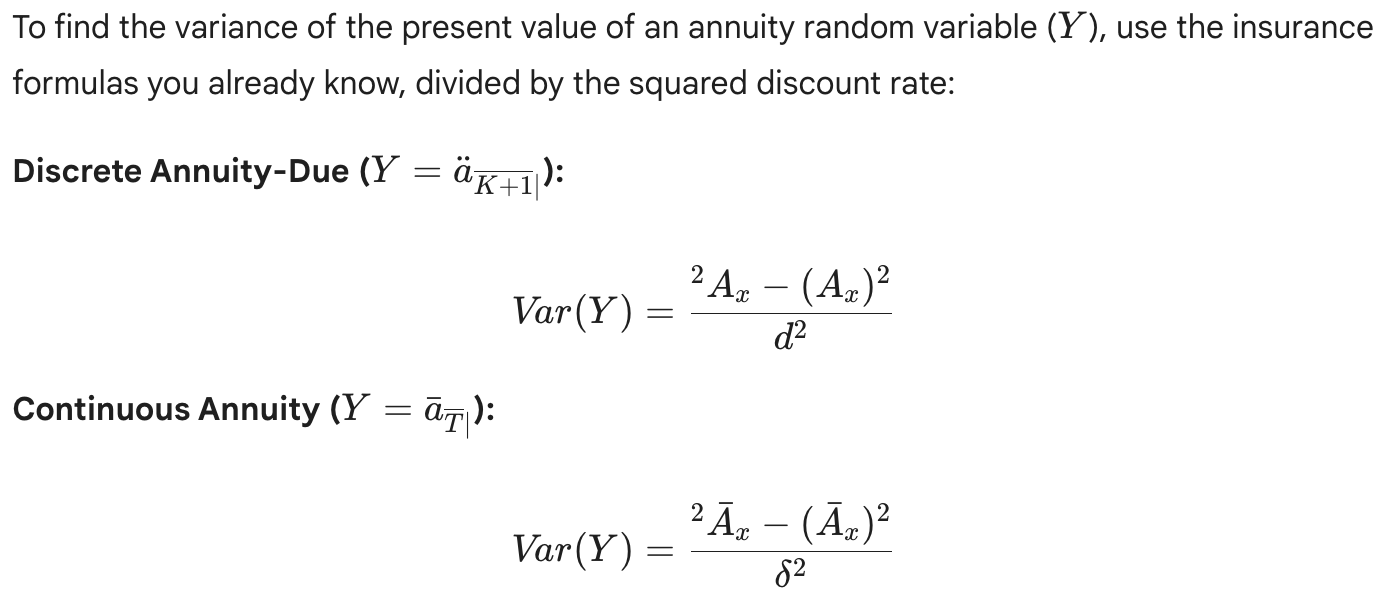

Variances

Annuities Relations

Guaranteed Annuity =

98th percentile means

98th percentile means the survival probability equals 0.98

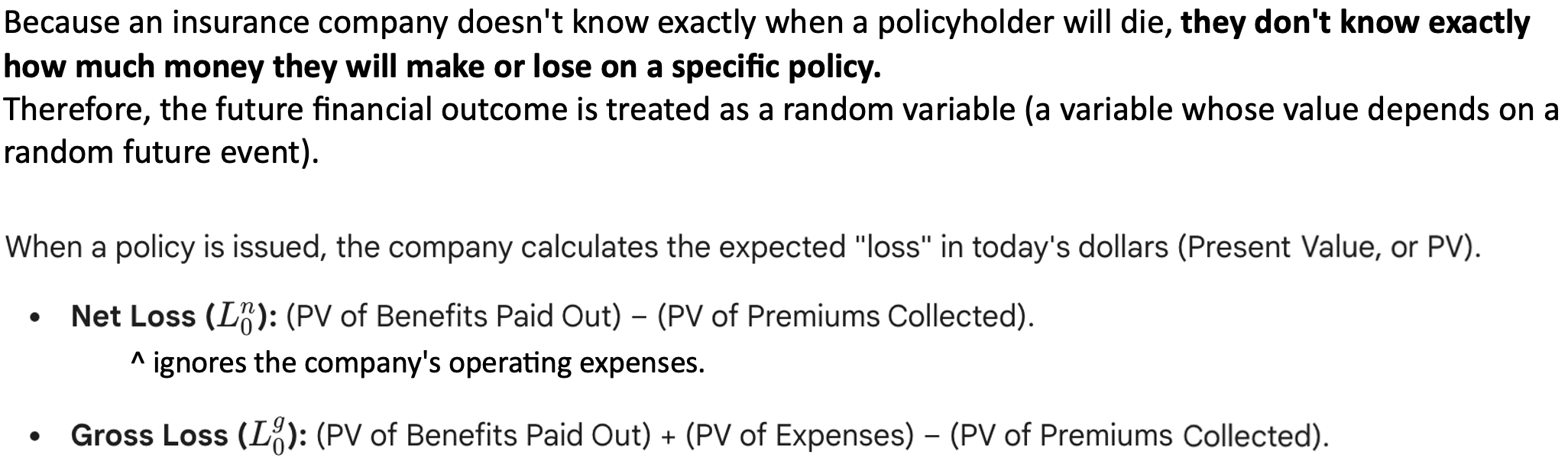

The Loss at Issue Random Variable

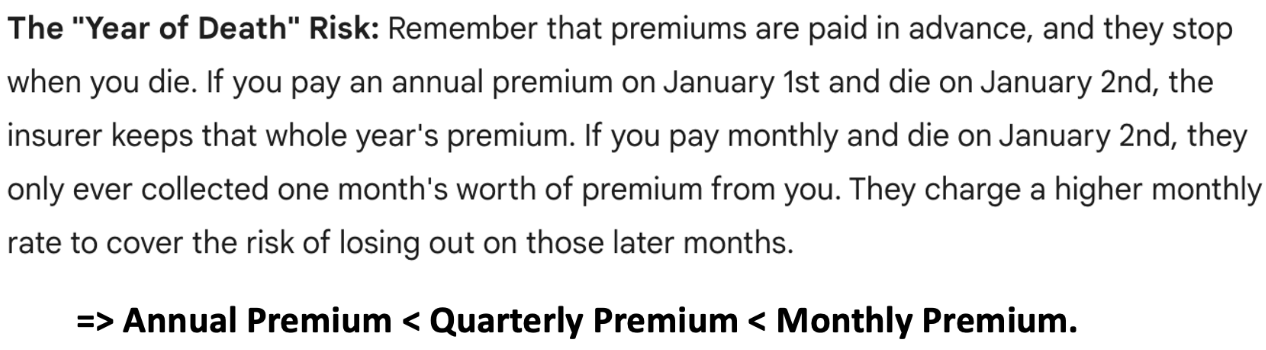

When are premiums paid?

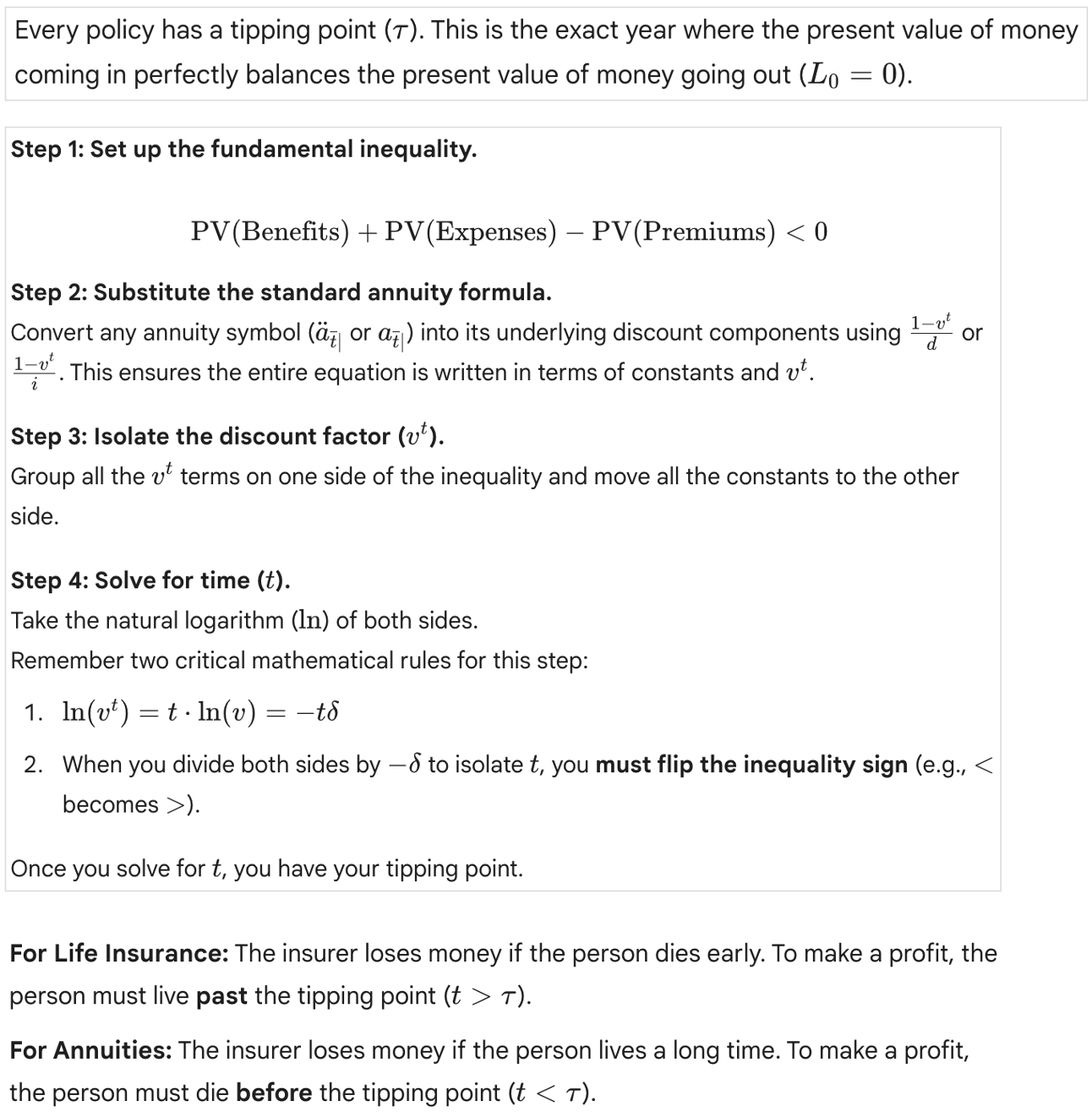

Calculating the "Tipping Point" of Profitability

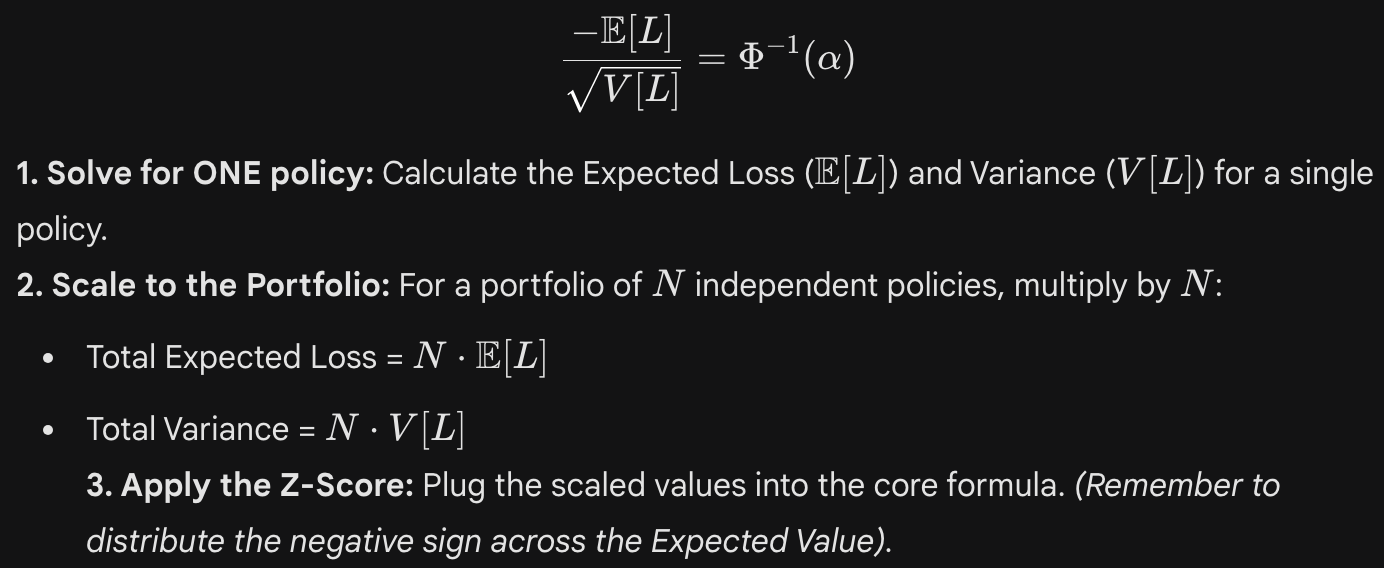

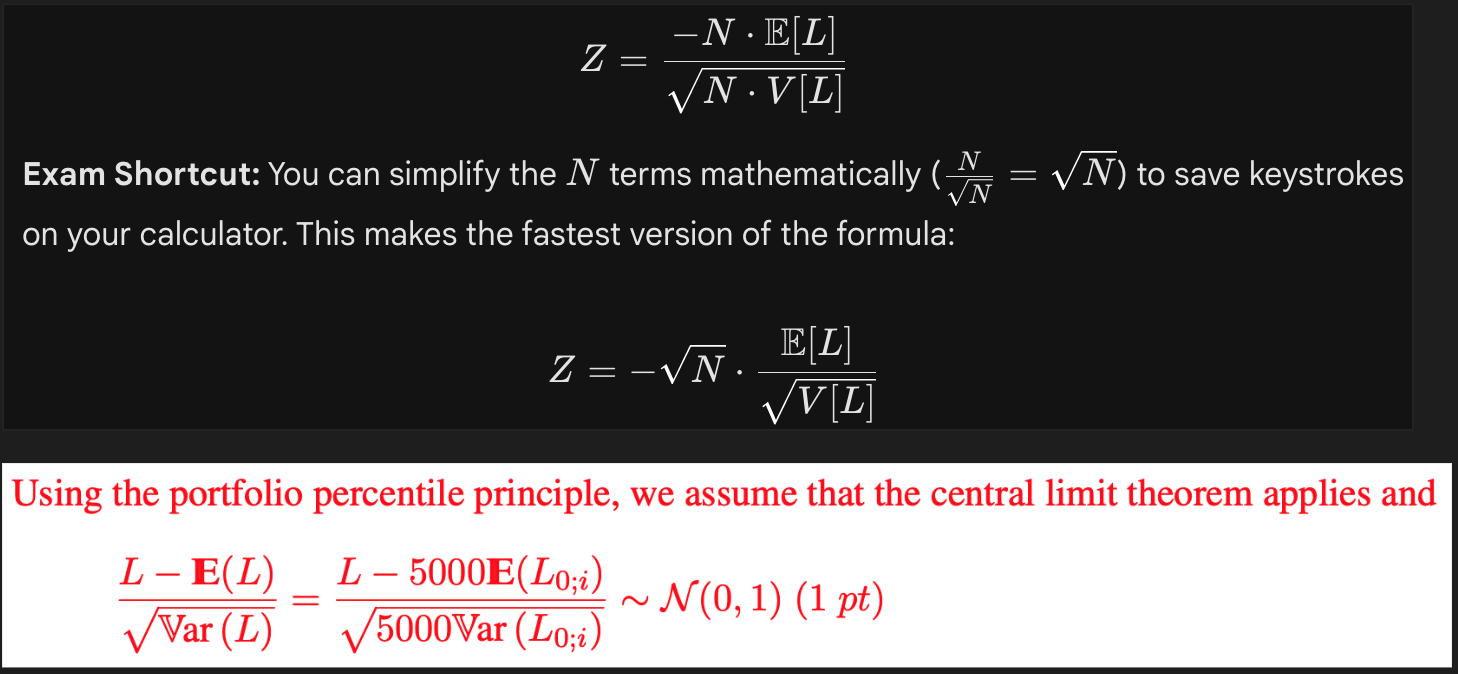

The Percentile Premium Principle

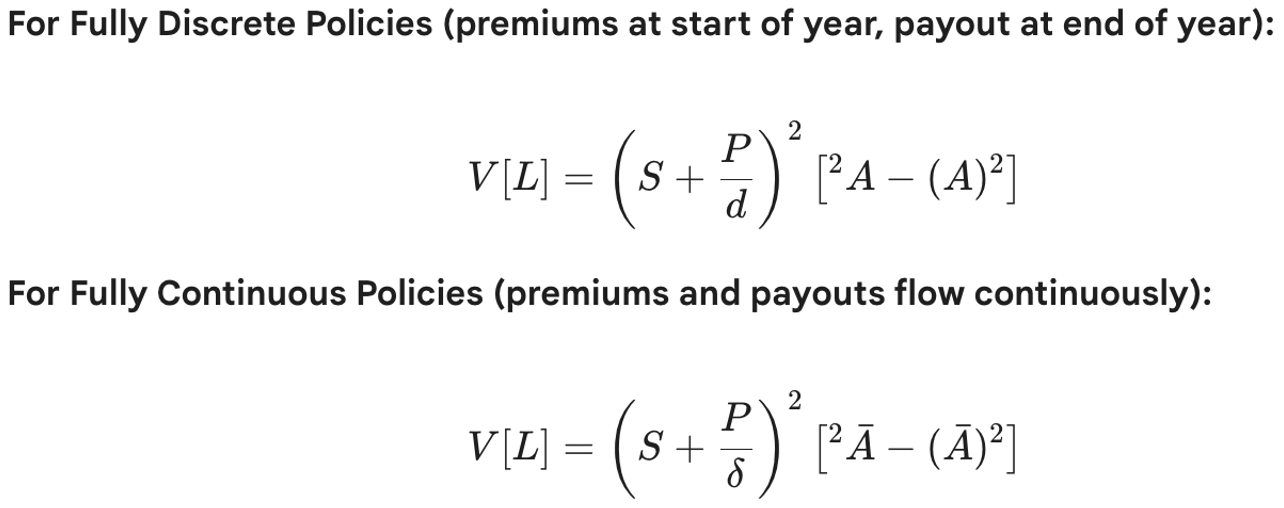

V[L] =

The Percentile Premium Principle

Shortcuts

To model this "extra risk" in EPV calculations, one of three methods are usually used:

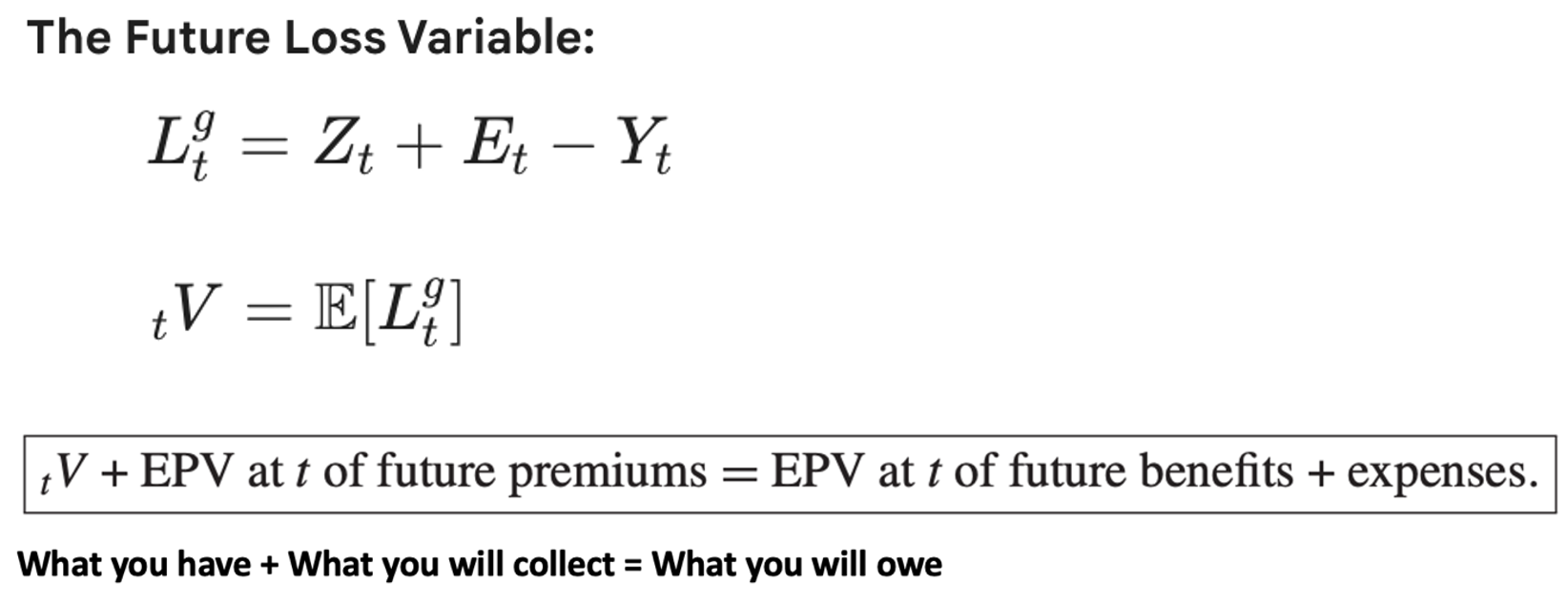

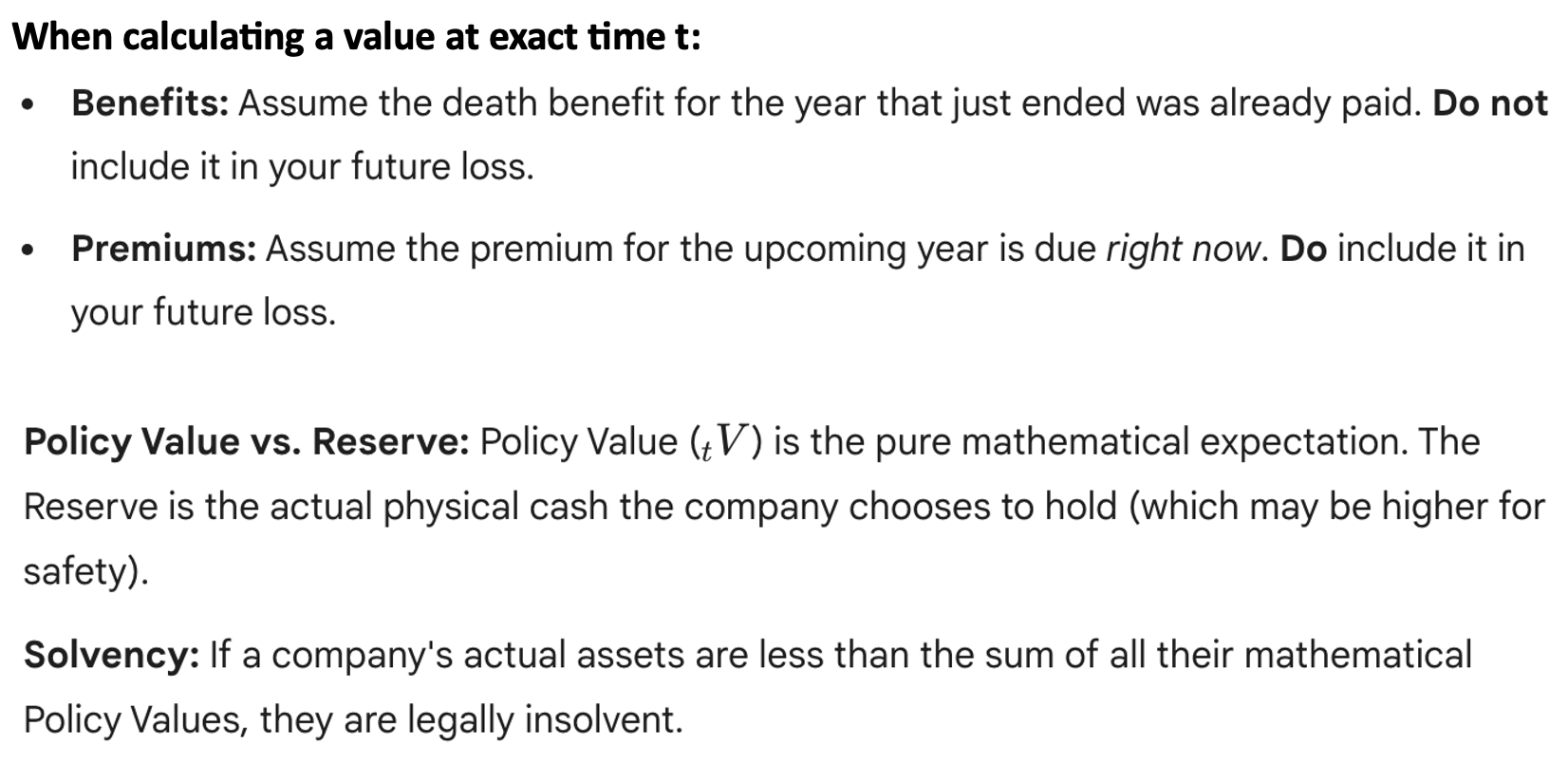

The Future Loss Random Variable

The Future Loss Random Variable

Assumptions & Company Valuation

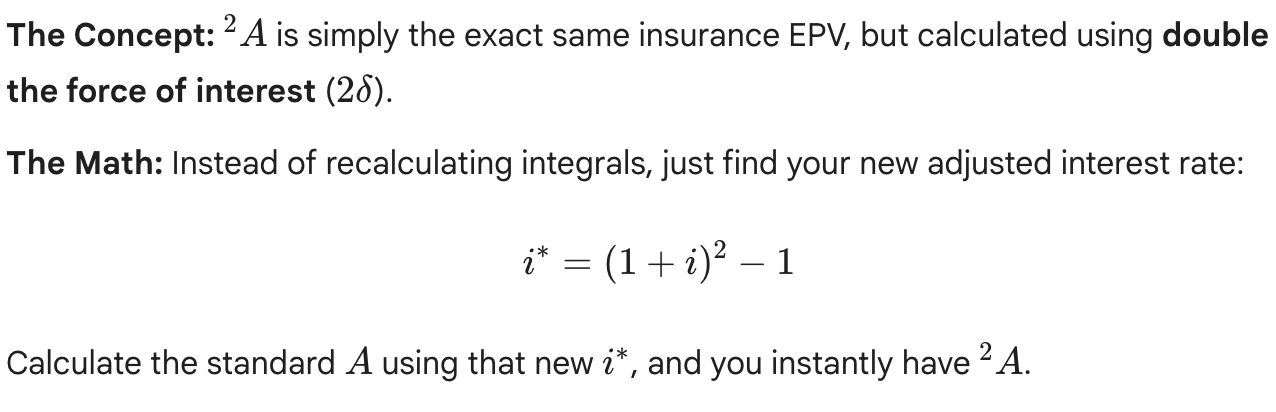

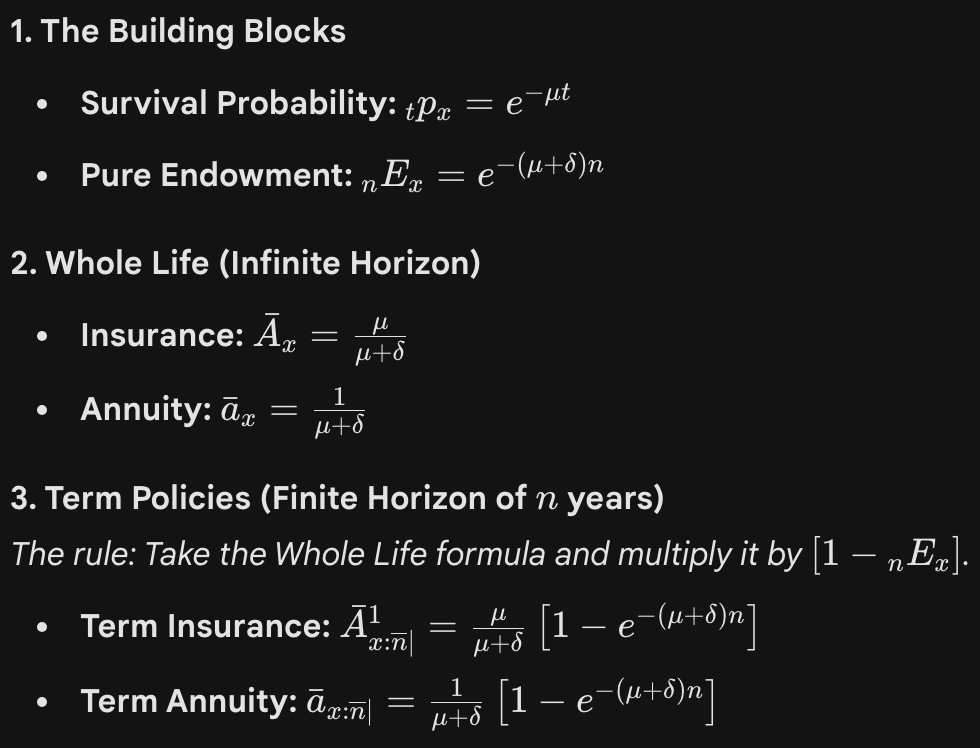

When dealing with Constant Force of Mortality / Interest

CFM distribution