Micro Econ EXAM 1

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

36 Terms

Economics defintion

The study of how individuals in society allocate their limited resources to satisfy the practically unlimited wants.

Macro

The study of the overall aspects of the working economy

Micro

The study of the individual units that makeup the economy

5 foundations of Economics

1.) Incentives

2.) Trade offs

3.) Opportunity Cost

4.) Marginal Thinking

5.) Trade

Incentives

the factors that motivate you to act or not act

Trade offs

a balance achieved between two desirable but incompatible features; a compromise.

Opportunity Cost

value of the next best alternative not chosen, what is best value

Marginal Thinking

helping optimize choices by comparing incremental changes rather than totals

Trade

the action of buying and selling goods and services (more trade the better for everyone)

Positive Incentives vs Negative Incentives

reward system vs providing undesirable consquences

Direct Investments

obvious and immediate awards or penalties for specific action

Indirect Investments

consequences that are secondary effects or unintened consquences of a direct influence

Circular Flow

Comparative Advantage

where an individual, a business, buisness or a country can produce at a lower opportunity cost than a competitor

Economics is a…

social science

positive statements

something that can be tested and validated Ex. what is the unemployment rate?

normative statement

opinion of what should be

Econ Model definition

a simplified, abstract representation of reality. NOT SUPPOSED TO BE REALISTIC

Assumptions

a simplifying condition or initial premise used to build models, theories, and analyses, helping to make complex systems manageable by isolating key factors, even if they aren't perfectly realistic

Ceteris Peribus

all other things equal, controlling other things by holding a variable constant

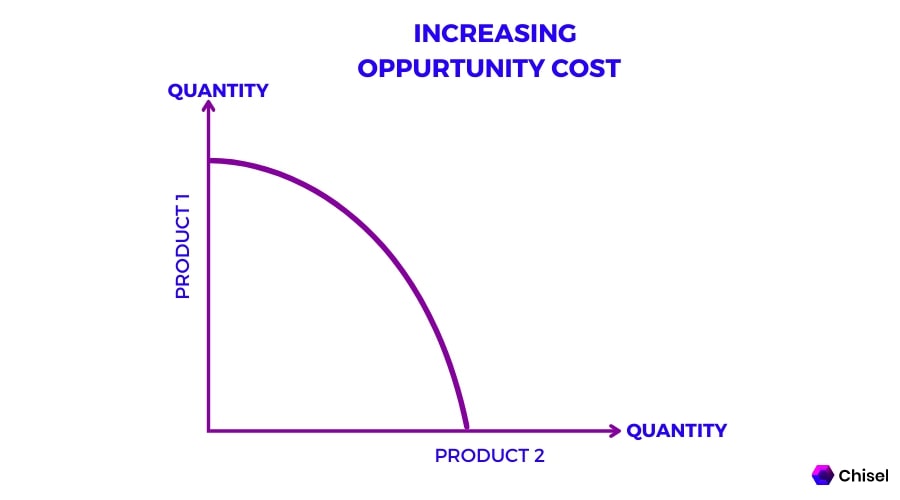

Production Possibilities Frontier (PPF)

a model that illustrates a combination of outputs that an economy produces, assumptions made = tech, resources, 2 goods.

endogenous vs exogenous

Inside our model variables vs outside our model variables.

Law of Increasing Opportunity Costs

as you produce more of one good, the cost (in terms of the other good you give up) rises because resources aren't perfectly adaptable

Specialization

limiting ones work to a particular area or areas

Absolute Advantage

When someone can produce more of something than someone else

Market Place

Consumers + firms

Supply

How many units (price) and Quantity Supply (qs) so if price goes up than products go up

Qs greater than Qd

surplus

Qd greater than Qs

shortage

Change in Supply

1.) Cost of inputs (amount of products produce)

2.) Tech (tech you pay once, people $$$)

3.) # of suppliers

4.) Price Expectations (the price you can get day by day)

Law of Supply

holding other factors constant, as the price of a good or service increases, the quantity supplied by producers also increases, and as the price decreases, the quantity supplied decreases

Demand

Consumers and relationships between 2 particular variables.

Change in Demand

1.) Income

2.) price of other goods (substitute and complement)

3.) taste

4.) price expectations

5.) # of buyers

Law of Demand

Price and quantity demanded move in opposite directions. Inverse relationships

What way does supply and demand move

right to left