2.1 - demand and supply, surplus, traditional economic theory

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

23 Terms

demand

quantity of a good/ service that consumers are willing and able to purchase at various prices during a specific period.

demand curve

relationship between the price of a good or service and the quantity demanded by consumers.

law of demand

price ↑= quality demanded ↓

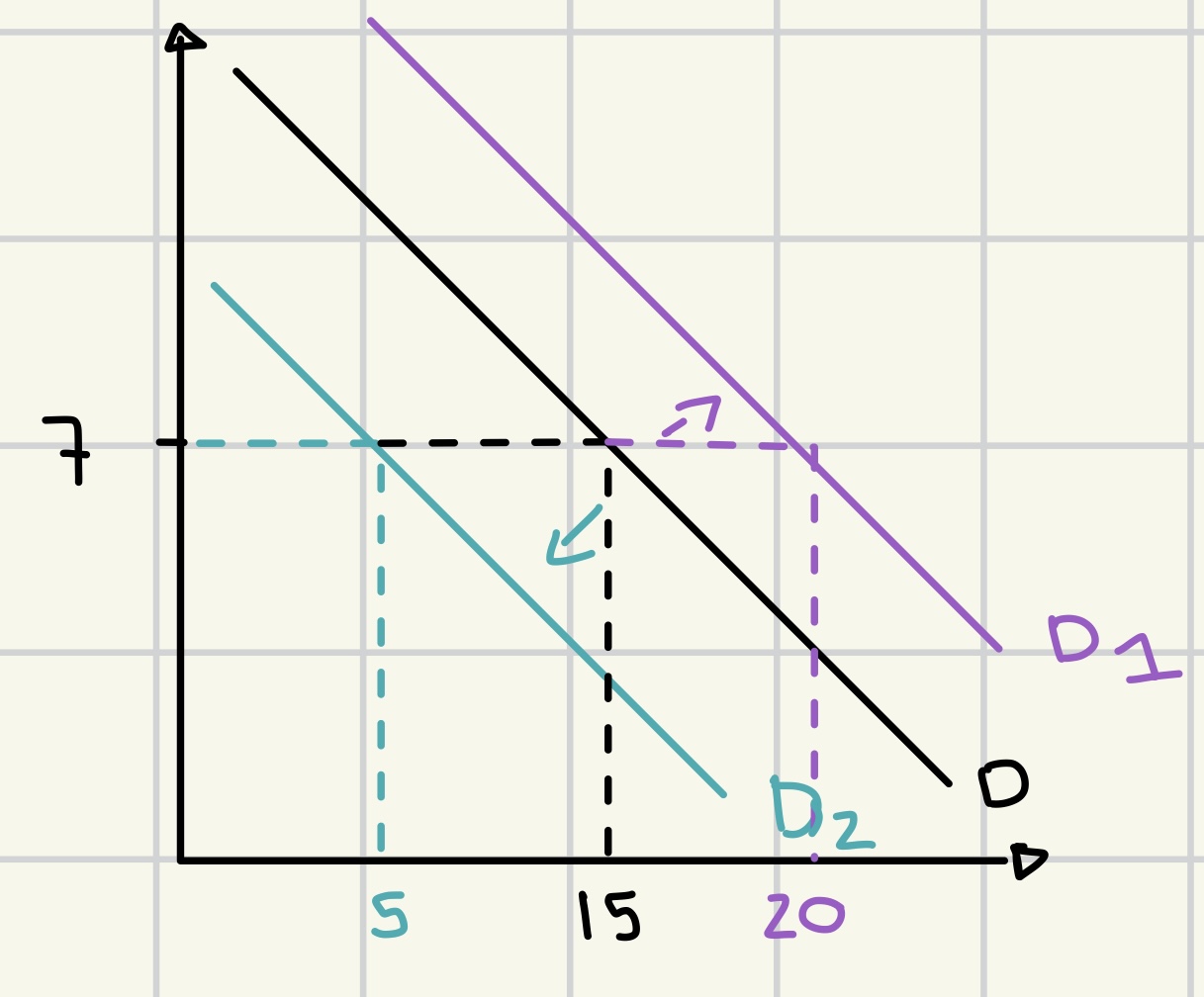

non-price determinants of demand

income ↑ = quality demanded ↑ (D → D1)

good preference ↑ = quantity demanded ↑ (D → D1)

price of substitute ↑ = quantity demanded↑ (D → D1)

number of consumers ↑ = quantity demanded ↑ (D→ D1)

price of complementary goods ↑ = quantity demanded ↓ (D → D2)

supply

amount of a good or service that producers are willing and able to sell at various prices over a specific time period.

supply curve

relationship between quantity supplied and price

law of supply

market price ↑ = quantity supplied ↑

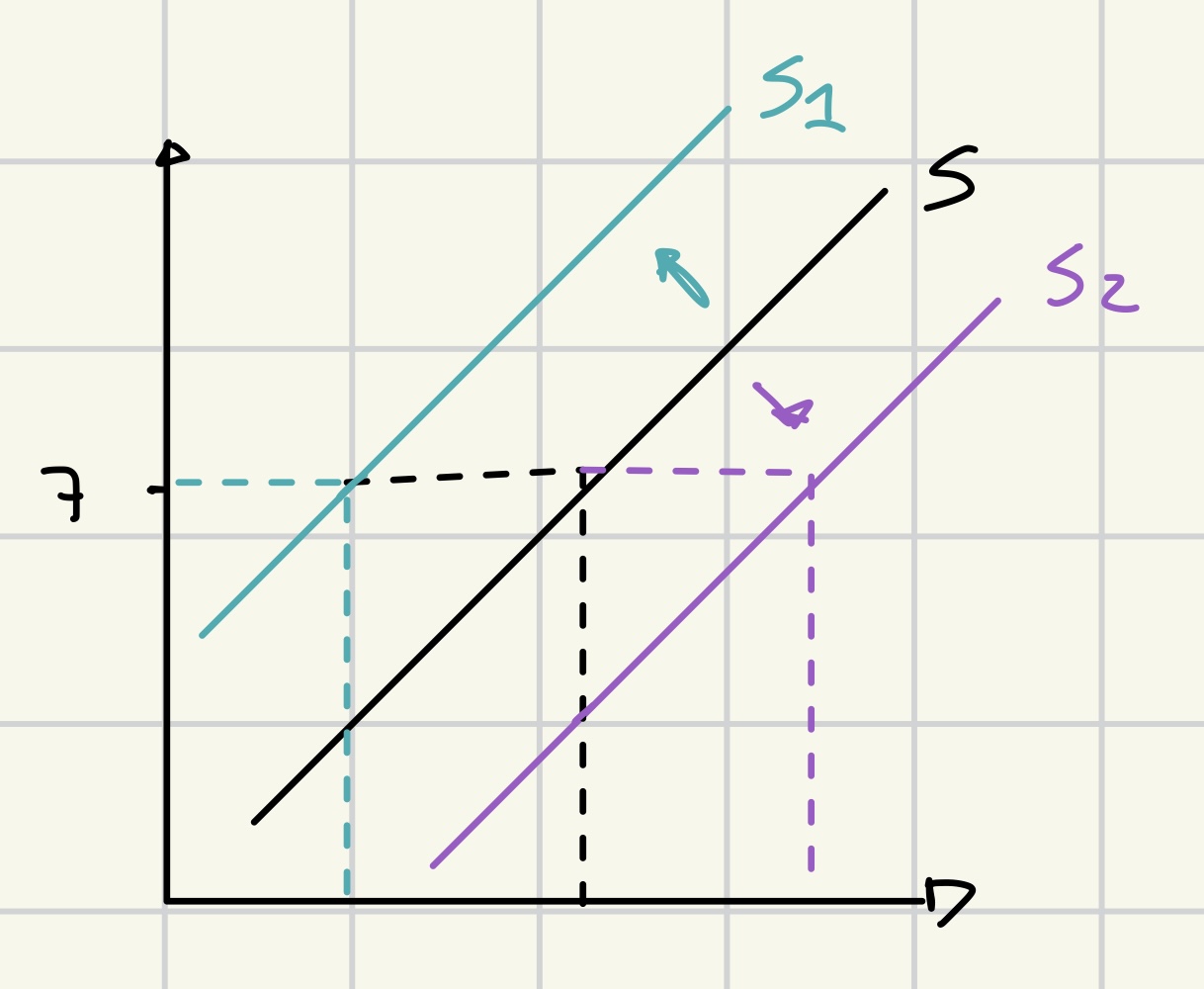

non price determinants of supply

subsidies ↑ = supply ↑ (S→ S2)

new technology ↑ = supply ↑ (S→ S2)

competitors ↑ = supply ↑ (S→ S2)

cost of production ↑ = supply ↓ (S→ S1)

taxes ↑ = supply ↓ (S→ S1)

weather disaster = supply ↓ (S→ S1)

opportunity cost of related products ↑ = supply ↓ (S→ S1)

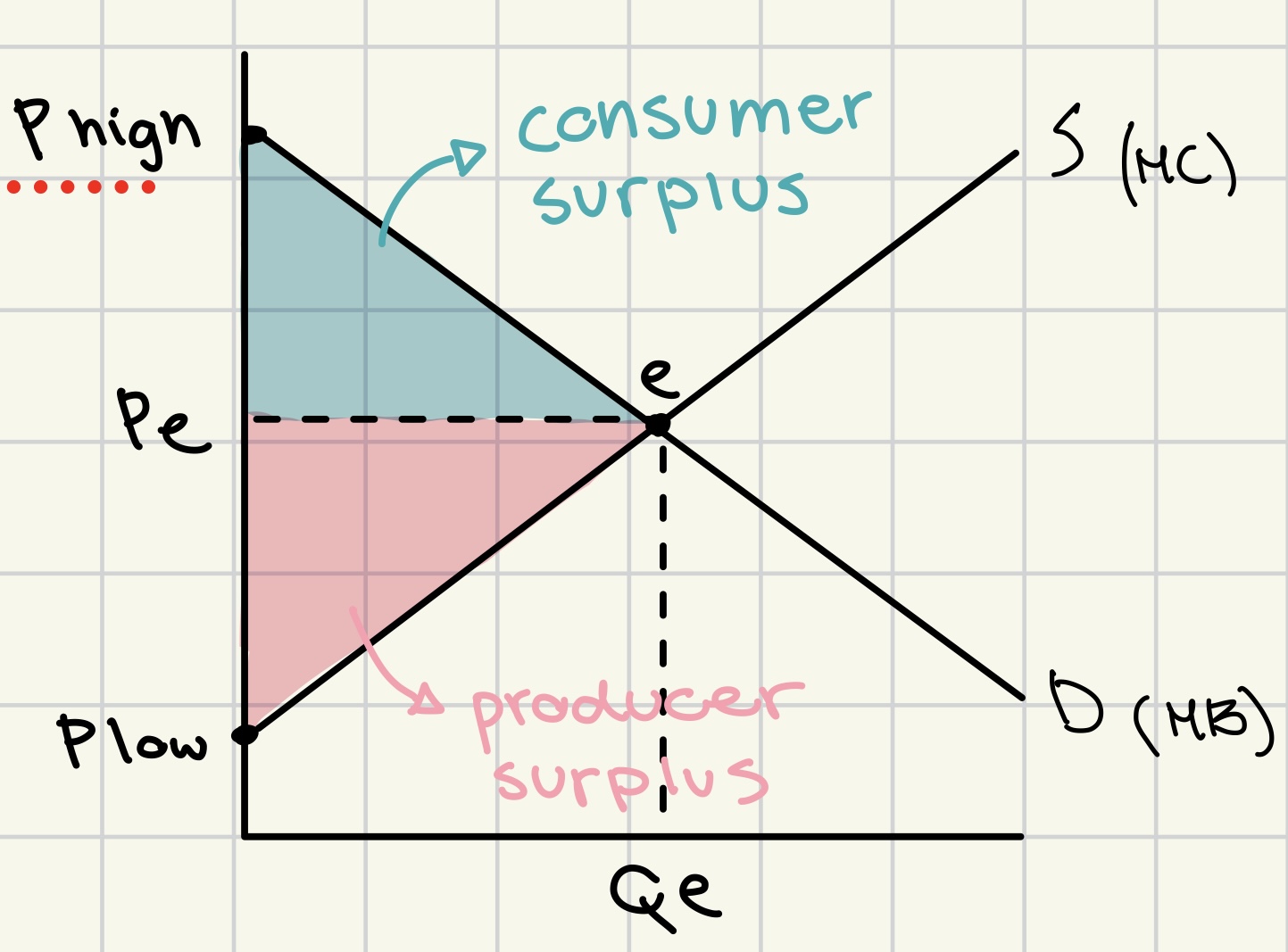

consumer surplus

difference between the amount the consumer is willing to pay for a product and the price they have actually paid

benefit gained by the consumer for purchasing the product at a lower price.

producer surplus

difference between the price producer is willing to sell a product for and the price they actually do

benefit to producers from selling at a higher price than their minimum acceptable price.

producer and consumer surplus graph

supply ↑ = producer/consumer surplus ↑

demand ↑ = producer/consumer surplus ↑

allocative efficiency/ equilibrium

resources are distributed in a way that maximizes total societal welfare

quantity of a good produced is equal to the quantity demanded.

productive efficiency

at minimum average total cost

all resources are utilized effectively.

traditional economic theory

consumer rationality

utility maximization

perfect information

limitations on rational consumer choice

biases

bounded rationality

bounded self-control

bounded selfishness

imperfect information

forms of biases

based on experience

framing ‘20% fat vs 80% fat free’

anchoring (seller suggest a higher price than the real value)

availability bias

bounded rationality theory

individuals make decisions based on the limited information available to them, leading to less-than-optimal choices.

bounded self control

the tendency to struggle with making choices that align with long-term goals due to immediate temptations and distractions.

bounded selfishness

the tendency of individuals to prioritize their own interests over the collective good, often leading to suboptimal outcomes for the group.

imperfect information

the situation where all relevant information is not available to consumers or producers, leading to suboptimal decision-making in markets.

types of choice

default

restricted

mandated

nudge theory EAST

using reinforcement and suggestions to influence decision-making of individuals.

E - easy → simplify

A - attractive → gain people’s attention

S - social → individuals may be influenced by others doing said thing

T - timely → identify when people are most responsive

advantages of nudge theory

cost effective

preserves freedom of choice

improves decision making

encourages positive behavior change.