bus 102 exam 2

1/87

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

88 Terms

sole proprietorship

the business is owned by a single individual

partnership

two or more people serve as co-owners of the business

corporation

the business is a separate legal entity

limited liability company

a hybrid with characteristics of both a corporation and partnership

business ownership options

sole proprietorship (72.4%), partnership(10.7%), corporation(16.9%), limited liability company

advantages of sole propietorships

•Ease of formation

•Retention of control

•Pride of ownership

•Retention of profits

•Possible tax advantage

disadvantages of sole proprietorships

•Limited financial resources

•Unlimited liability

•Limited ability to attract and maintain talented employees

•Heavy workload and responsibilities

•Lack of permanence

advantages of partnerships

•Ability to pool financial resources

•Ability to share responsibilities and capitalize on complementary skills

•Ease of formation

•Possible tax advantages

disadvantages of partnerships

•Unlimited liability

•Potential for disagreements

•Lack of continuity

•Difficulty in withdrawing from a partnership

advantages of corporation

•Limited liability

•Permanence

•Ease of transfer of ownership

•Ability to raise financial capital

•Ability to make use of specialized management

disadvantages of corporations

•Expense and complexity of formation and operation

•Complications when operating in multiple states

•Double taxation of earnings and additional taxes

•More paperwork and regulation and less secrecy

•Possible conflicts of interest

ownership of corporations

ownership is represented by shares of stock

stockholder

an owner of a corporation

board of directors in corpotations

•The individuals who are elected by stockholders of a corporation to represent their interests

•Establishes the corporation’s mission and sets its broad objectives

•Appoints officers, such as CEO and CFO, for day-to-day management of the corporation

corporate restructuring

acquisition and merger

acquisition

one firm buys another firm

merger

Two formerly independent business entities combine to form a new organization

types of mergers

Horizontal merger, vertical merger, and conglomerate merger

horizontal merger

definition: a combination of firms in the same industry (airlines or pharmacy)

common objectives:

•increases size and market power within the industry

•improves effeciency by eliminating duplication of facilities and personnel.

vertical merger

definition: Combination of firms that are at different stages in the production of a good or service, creating a buyer-seller relationship (IKEA)

common objective: Provides tighter integration of production and increased control over the supply of crucial inputs.

conglomerate merger

definition: A combination of firms in unrelated industries (Clorox).

common objective: Reduce risk by making the firm less vulnerable to adverse conditions in any single market.

Franchise

A licensing arrangement under which a franchisor allows franchisees to use its name, trademark, products, business methods, and other property in exchange for monetary payments and other considerations.

advantages of franchising

•Less risk

•Training and support

•Brand recognition

•Easier access to funding

disadvantages of franchising

•Costs

•Lack of control

•Negative halo effect

•Growth challenges

•Restrictions on sale

•Poor execution

reasons to launch a small business

greater financial success, independence, flexibility, challenge, survival.

entrepreneurs

People who risk their time, money, and other resources to start and manage a business

necessity entrepreneurs

They launch businesses because they believe it is their only economic option.

entrepreneurial characteristics

vision, self-reliance, energy, confidence, tolerance of uncertainty, tolerance of failure

funding options for small business

personal resources, loans, crowdfunding, angel investors and venture capital.

personal resources

friends, family and personal credit cards

loans

Sources include commercial banks, U.S. Small Business Administration (SBA), and peer-to-peer lending

crowdfunding

Process of funding ventures by raising money from a large number of investors via the internet

angel investors

Individuals who invest in start-up companies with high growth potential in exchange for a share of ownership

venture capital

Companies that invest in start-up businesses with high growth potential in exchange for a share of ownership

small business opportunities

•Market niches

•Personal customer service

•Lower overhead costs

•Technology

small business threats

•High risk of failure

•Lack of knowledge and experience

•Less money and more regulatory burden

•High health insurance costs

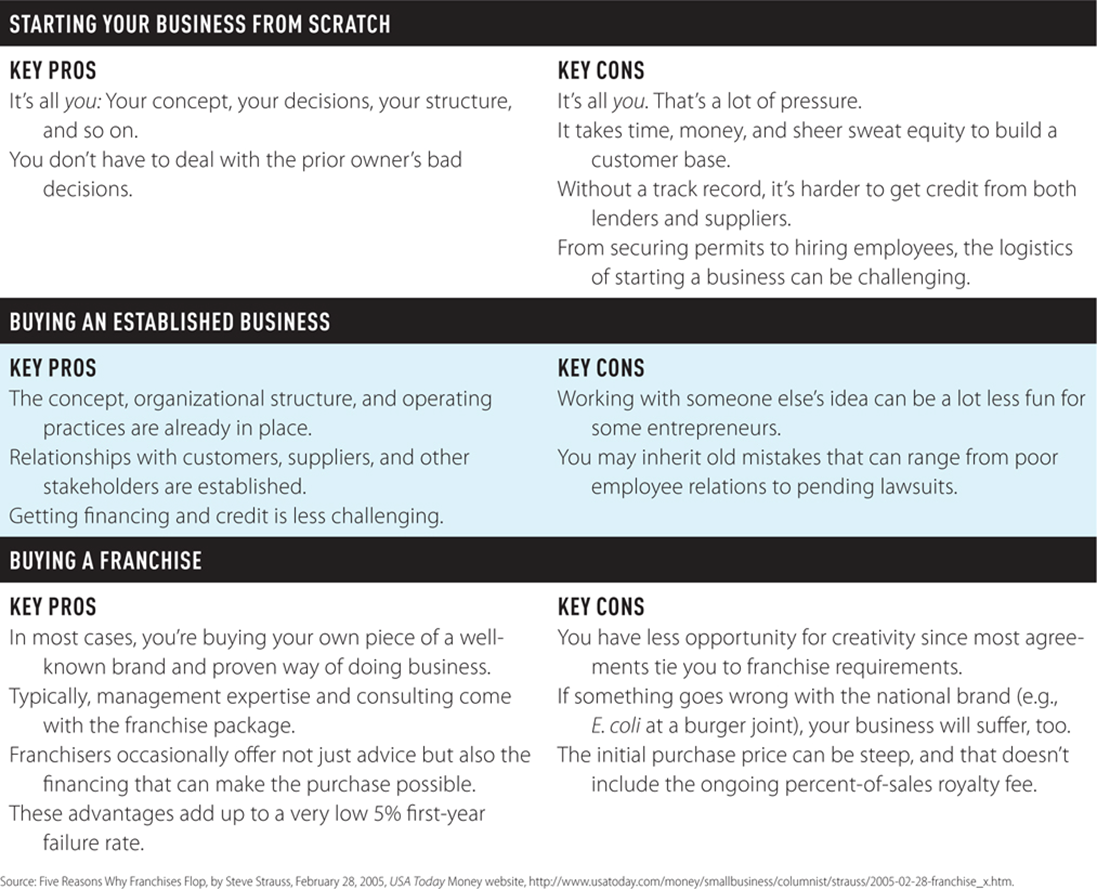

pros and cons of starting a business from scratch vs buying an established business

small business administration

•An agency of the federal government designed to maintain and strengthen the nation’s economy by aiding, counseling, assisting, and protecting the interests of small businesses

•Provides resources to small business owners

business plan

A formal document that describes a business concept, outlines core business objectives, and details strategies and timelines for achieving those objectives

business plan includes:

executive summary, descriptions of business, complete financial data and plan.

Small businesses play a vital role in the U.S. economy

• Comprise 99.9% of all U.S. businesses and 47.1% of private sector employees

• Create new jobs

• Fuel innovation

• Vitalize inner cities

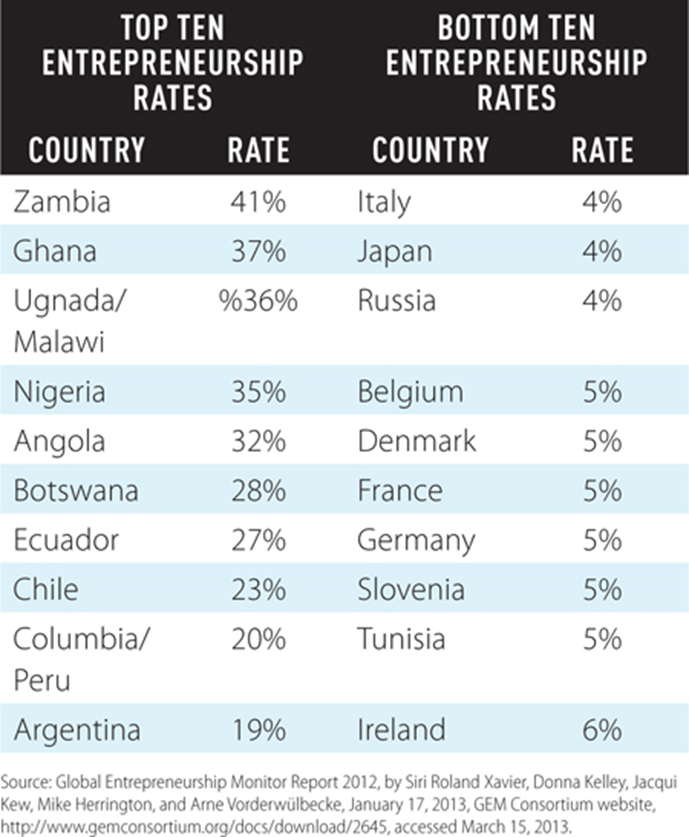

Entrepreneurship around the world

•Societies need entrepreneurs to ensure:

−New ideas actualize

−People are able to self-employ when their economy does not provide for their basic needs

•Current entrepreneurship rates vary from country to country

entrepreneurship around the world

Accounting

“language of business”

A system for recognizing, organizing, analyzing, and reporting information about the financial transactions that affect an organization.

accounting’s goal

To provide users with relevant, timely information that can help them make better economic decisions

who uses accounting?

managers, stockholders, employees, creditors, suppliers, government agencies, news media, competitors, unions.

who does accounting?

public accountants, management accountants, government accountants

public accountants

Provide services such as tax preparation, external auditing, and management consulting to clients on a fee basis

management accountants

Work within a company and provide analysis, prepare reports and financial statements, and assist managers

government accountants

Perform accounting functions for local, state, or federal government agencies

financial accounting

The branch of accounting that prepares financial statements for use by owners, creditors, suppliers, and other external stakeholders

−Stakeholders need this information to analyze the financial condition of the firm through a period of time

−Investors compare a company’s financial results to other firms in the same industry

−The major output of financial accounting—balance sheets, income statements, and cash flows—provides fundamental information about a company’s past and future financial performance

GAAP

Generally Accepted Accounting Principles

A set of accounting standards that is used in the preparation of financial statements

FASB

Financial Accounting Standards Board

The private board that establishes the generally accepted accounting principles used in the practice of financial accounting

GAAP and FASB ensures that financial statements are:

• Relevant

• Reliable

• Consistent

• Comparable

three basic financial statements:

balance sheet, income statement and statement of cash flows

financial statements

• Provide external stakeholders with a view of an organization’s financial condition

• Must appear in publicly traded companies’ annual report

• Part of companies’ quarterly and annual filings with the Securities and Exchange Commission (SEC)

Balance sheet

A financial statement that reports the financial position of a firm by identifying and reporting the value of the firm’s assets, liabilities, and owners’ equity

accounting equation

Assets = Liabilities + Owners’ Equity

assets

resources owned by a firm

liabilities

Claims that outsiders have against a firm’s assets

owners’ equity

The claims a firm’s owners have against their company’s assets (often called “stockholders’ equity” on balance sheets of corporations)

income statement

The financial statement that reports the revenues, expenses, and net income that resulted from a firm’s operations over an accounting period

revenue

Increases in a firm’s assets that result from the sale of goods, provision of services, or other activities intended to earn income

expenses

Resources that are used up as the result of business operations

net income

The difference between the revenue a firm earns and the expenses it incurs in a given time period

statement of cash flows

The financial statement that identifies a firm’s sources and uses of cash in a given accounting period

Cash flows from operating activities, investing activities, and financing activities.

Statement of retained earnings

Shows how retained earnings have changed from one accounting period to the next

stockholders’ equity statement

−Shows how net income and dividends affect retained earnings

−Shows changes in stockholders’ equity, such as changes that arise from the issuance of additional shares of stock

The independent auditor’s report: getting a stamp of approval

•Prepared after conducting an annual external audit of the financial statements

•Verifies that financial statements:

−Are prepared in accordance with generally accepted accounting principles

−Fairly present the firm’s financial condition

•Included in the annual report that a firm sends its stockholders

fine print of financial statements

•Disclose additional information about a firm’s operations, accounting practices, and special conditions

•Explain the specific accounting methods used to recognize revenue, value inventory, and depreciate fixed assets

•Disclose changes in accounting methods or any risks that a firm may face

comparative statements

•Comparative statements put the balance sheet, income statement, and statement of cash flows of two or more years side by side

−Trace what happened to key assets and liabilities through several time periods

−Show increases or decreases in revenues or expenses

horizontal analysis

Analysis of financial statements that compares account values reported on these statements through two or more years to identify changes and trends

budgeting

A management tool that explicitly shows how a firm will acquire and use the resources needed to achieve its goals over a specific time period

-Facilitates planning by requiring managers to:

• Translate goals into measurable quantities

• Identify the specific resources needed to achieve goals

advantages of budgeting

• Helps managers specify how they intend to achieve goals set during the planning process

• Encourages communication and coordination among managers and employees

• Serves as a motivational tool

• Helps managers evaluate progress and performance

Managerial (or management) accounting

The branch of accounting that provides reports and analysis to managers (internal) to help them make informed business decisions

−A firm’s performance depends on the accuracy and reliability of this information

−Management accounting systems may be a source of competitive advantage

financial capital

The funds a firm uses to acquire its assets and finance its operations

finance

•The functional area of business that is concerned with finding the best sources and uses of financial capital

•Goal of financial management is to maximize the value of the firm to its owners

socially responsible firm

A socially responsible firm has an obligation to respect the needs of all stakeholders

•Being socially responsible requires a long-term commitment to the needs of different stakeholders

fiduciary duty of financial managers

Managers should make decisions that are most consistent with the interests of ownership when conflicts arise

Risk

The degree of uncertainty regarding the outcome of a decision

Risk and return trade-off

The observation that financial opportunities that offer high rates of return are generally riskier than opportunities that offer lower rates of return

financial ratio analysis

Computing ratios that compare values of key accounts listed on a firm’s financial statements

financial leverage

The use of debt in a firm’s capital structure

id financial needs

Ratio name | Type | How it is computed |

Current | Liquidity •Measures ability to pay short-term liabilities as they come due | Current Assets/Current Liabilities |

Inventory turnover | Asset management •Measures how effectively a firm is using its assets to generate revenue | Cost of Goods Sold/Average Inventory |

Average collection period | Asset management •Measures how effectively a firm is using its assets to generate revenue | Accounts Receivable/(Annual Credit Sales/365) |

id financial needs pt 2

Ratio name | Type | How it is computed |

Debt-to-assets | Leverage •Measures the extent to which a firm relies on debt to meet its financing needs | Total Debts/Total Assets |

Return on equity | Profitability •Compares the amount of profit to some measure of resources invested | Net Income – Preferred Dividend/Average Common Stockholders Equity |

Earnings per share | Profitability •Compares the amount of profit to some measure of resources invested | Net Income – Preferred Dividend/Average Number of Common Shares Outstanding |

equity financing

acquired from owners

debt financing

acquired from lenders