Ch. 22 Statement of Cash Flows Revisited

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

28 Terms

Cash Flow Info

Helps financial stmt users assess financial performance and condition

Indicates whether a borrower will produce sufficient cash to pay its debts

Indicator of a company’s financial flexibility or ability to use cash for unexpected needs and opportunities

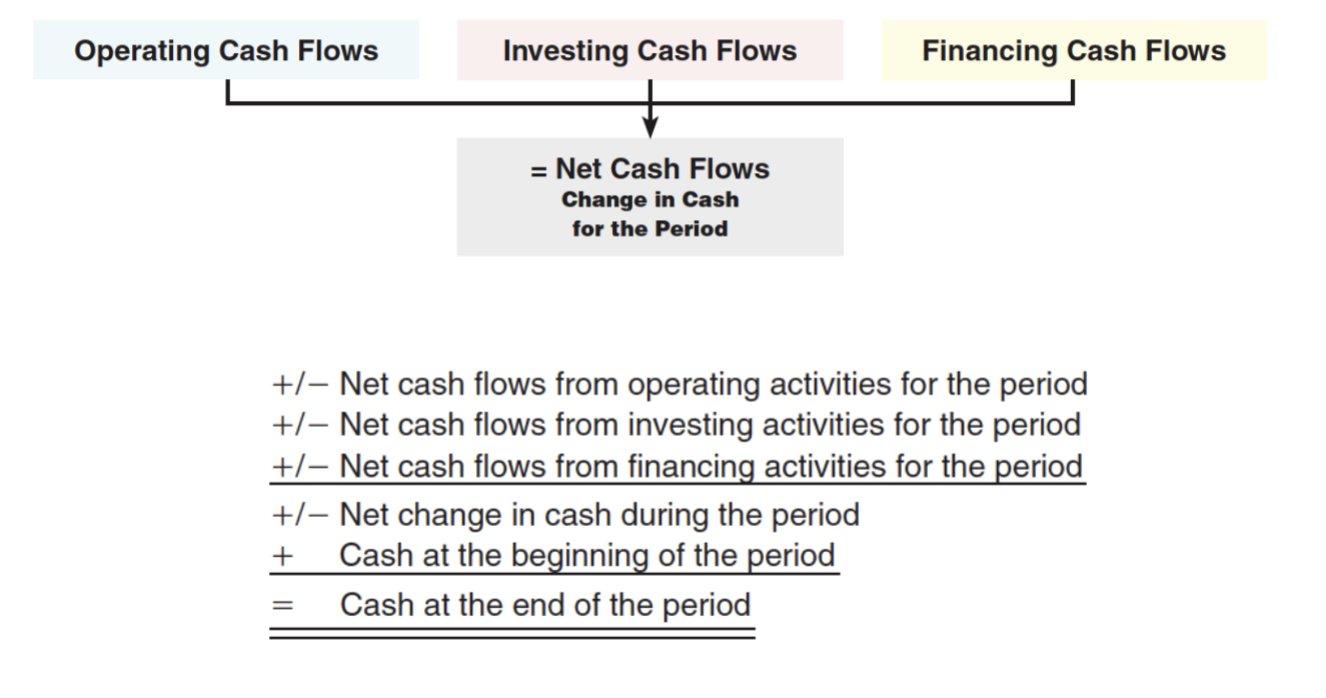

Classified as operating, investing and financing cash flows

Classification helps financial stmt users distinguish between ongoing activity and long-term strategic changes

Operating activities

generally involve producing and delivering goods and providing services

cash flows are generally the cash effects of transaction and other events that enter into determination of net income

Investing activities

include making and collecting loans and acquiring and disposing of debt or equity instruments and property, plant, and equipment and other productive assets

assets→ held for or used in the production of goods or services by the entity (other than materials that are part of the entity’s inventory)

investing activities EXCLUDE acquiring and disposing of certain loans or other debt or equity instruments that are acquired specifically for resale

Financing activities

include obtaining resources from owners and providing them with a return on, and a return of, their investment; receiving restricted resources that by door stipulation must be used for long-term purposes

borrowing money and repaying amounts borrowed, or otherwise settling the obligation; and obtaining and paying for other resources obtaining and paying for other resources obtained from creditors on long-term credit

Cash Flows from Operating Activities

a S-T or L-T TRADE note receivable (payable) is considered an operating asset (liability)

if notes are issued for reasons other than operating activities such as for a fixed asset, the cash flows are not classified as operating

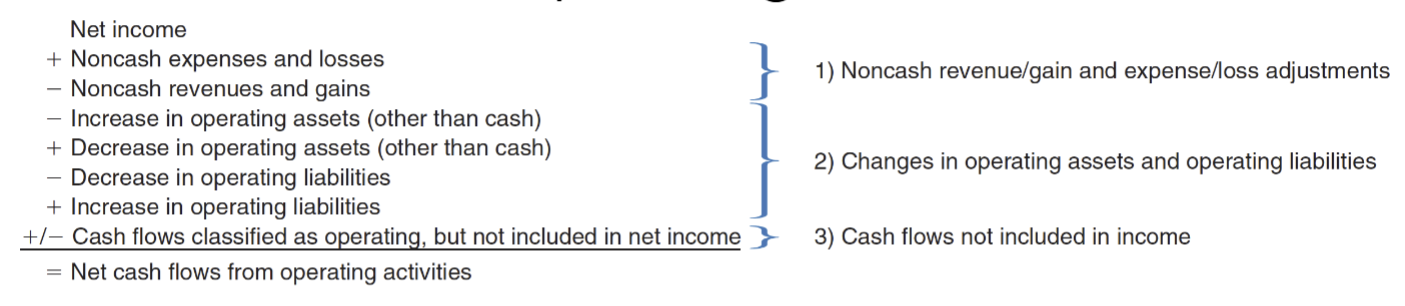

*picture is the INDIRECT METHOD

(1) Operating Activities→ Indirect method

Examples of noncash revenue/gain adjustments

gain on disposition of fixed asset or intangible asset

gain on settlement of non-operating liability

unrealized gain— income

(1) Operating Activities→ Indirect method

Examples of noncash expense/loss adjustments

loss on disposition of fixed asset or intangible asset

depreciation expense or amortization expense

stock compensation expense

unrealized loss— income

loss on settlement of nonoperating liability

(2) Operating Activities→ Indirect method

Examples of operating assets

accounts receivable

supplies

income tax receivable

miscellaneous prepaid expenses

inventory

prepaid insurance

ADD decrease in operating asset

DEDUCT increase in operating asset

(2) Operating Activities→ Indirect method

Examples of operating liabilities

account payable

income tax payable

deferred revenue

salaries payable

interest payable

accrued liabilities

ADD increase in operating liability

DEDUCT decrease in operating liability

(3) Operating Activities→ Indirect method

Cash flows not included in NI

selling and purchasing investments acquired specifically for resale by banks, brokers, and dealers

notes issued for an operating activity

Cash Inflows from Operating Activities

sale of goods or services

refunds from suppliers

dividends from investments

interest on receivables

settlements of lawsuit

proceeds from sale of investments held for resale in a trading account

collection on a L-T note receivable from a customer related to sale of goods

Cash Outflows from Operating Activities

purchase of goods for resale

salaries and other operating expenses

income taxes, duties, and fines

interest on liabilities

settlement of lawsuit

purchases of investments held for resale in a trading account

principal payment a note issued to acquire goods for resale

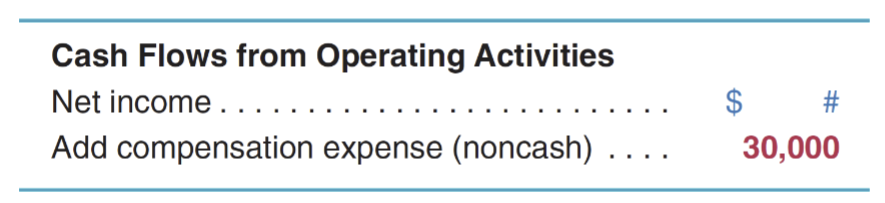

Operating Activities→ Compensation Expense

compensation for share-based plans increases compensation expense and capital accounts

no impact on cash

on the cash flow stmt: ADD amount back to NI

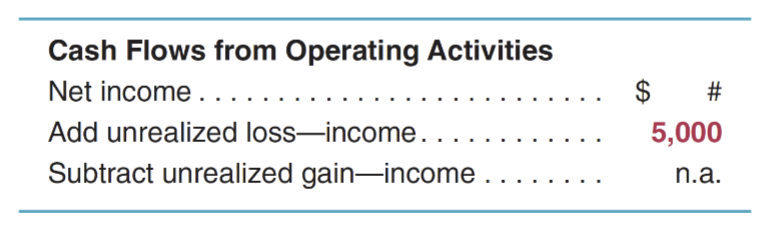

Operating Activities→ Unrealized Gain/Loss— Income

unrealized holding gains (losses) are recorded to adjust certain debt and equity securities to fair value

unrealized holding gains (losses) affect NI and the investment account

NO impact on cash

on the cash flow stmt:

ADD losses (SUBTRACT gains) to (from) NI

but NO adjustments are required for unrealized gains/losses impacting OCI

Operating Activities→ Pension Expense

pension expense recognized for defined benefit plans may differ from cash funding payments to the plan

On the cash flow statement:

- pension expense > contributions; ADD difference to NI

- pension expense < contributions; SUBTRACT difference from NI

Operating Activities→ Equity Method Noncash Adjustment

for equity investments, companies record:

investment income for a proportionate share of the investee’s income (noncash item)

cash dividends declared and received as an increase to cash and a decrease to the investment account (no NI impact)

on the cash flow stmt:

- investment income > dividends; SUBTRACT difference from NI

- investment income > dividends; ADD difference to NI

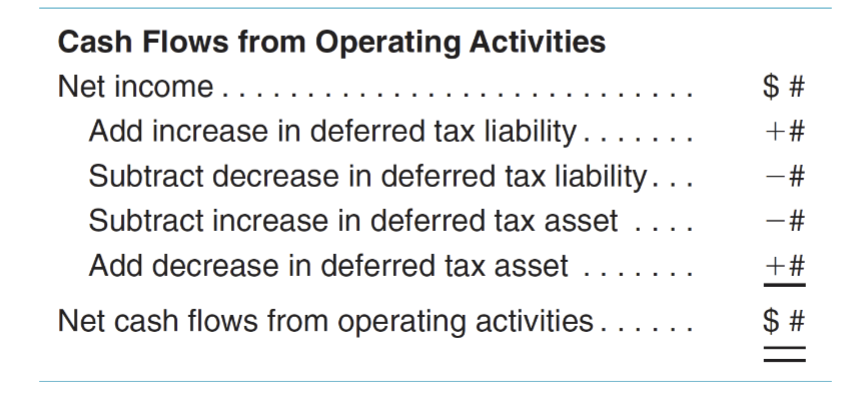

Operating Activities→ Changes in DTA and DTL

changes in DTA and DTL may affect tax expense

On the cash flow stmt:

- adjust NI for increases (decreases) in deferred tax accounts

Cash Inflows from Investing Activities

sale of property, plant, and equipment

sale of debt and equity investments in other companies (cash flows from investments held specifically for resale are classified as operating activities)

collection of a loan (excluding interest, which is an operating activity)

sale of patents or other intangible assets

Cash Outflows from Investing Activities

purchase of property, plant, and equipment

investments in debt and equity investments in other companies

loans to other entities

purchase of patents or other intangible assets

Cash Flows from Investing Activities

investing activities presented as gross cash inflows and outflows

ex: a sale is reported separately from a purchase

generally includes cash flows related to changes in fixed assets, intangible assets, investments in other companies (excluding trading accounts), and nontrade loans to other companies

cash paid for the acquisition of fixed assets includes cash paid for interest that is capitalized

Cash Flows from Financing Activities

financing activities presented as gross cash inflows and outflows

ex: a cash receipt is reported separately from a cash payment

generally includes cash flows related to equity financing, debt financing (excluding trade debt), and dividend payments

dividends are adjusted for a change in dividends payable

also includes cash flows related to:

principal payments for sale-type leases

principal payments on installment notes

Cash Inflows from Financing Activities

issuance of a company’s own stock

sale of treasury stock

issuance of bonds or other debt (S-T and L-T nontrade debt)

Cash Outflows from Financing Activities

dividends and other cash distributions to owners

reacquiring previously issued capital stock

principal payments on loans, payments to retire bonds or other debt, debt issue costs, and principal payments on finance leases

Cash Flow Statement

Demo 22-1

Answer:

Cash Flow Disclosures: Reporting Requirements

reconciliation of NI to operating cash flow

report investing and financing inflows and outflows

disclose interest and income taxes paid

disclose noncash investing and financing transactions

disclose nature and amounts of restricted cash or cash equivalents

Noncash Investing and Financing Transactions

noncash transactions involve no exchange of cash

omit noncash exchanges from the cash flow stmt but disclose if material

Examples of noncash exchanges:

conversion of debt securities to equity securities

acquisition of assets by assuming liabilities

securing a right-of-use asset in exchange for a lease liability

refinancing a long-term note payable