Economics: Supply & Demand Curves, Equilibrium, and Market Interventions

1/157

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

158 Terms

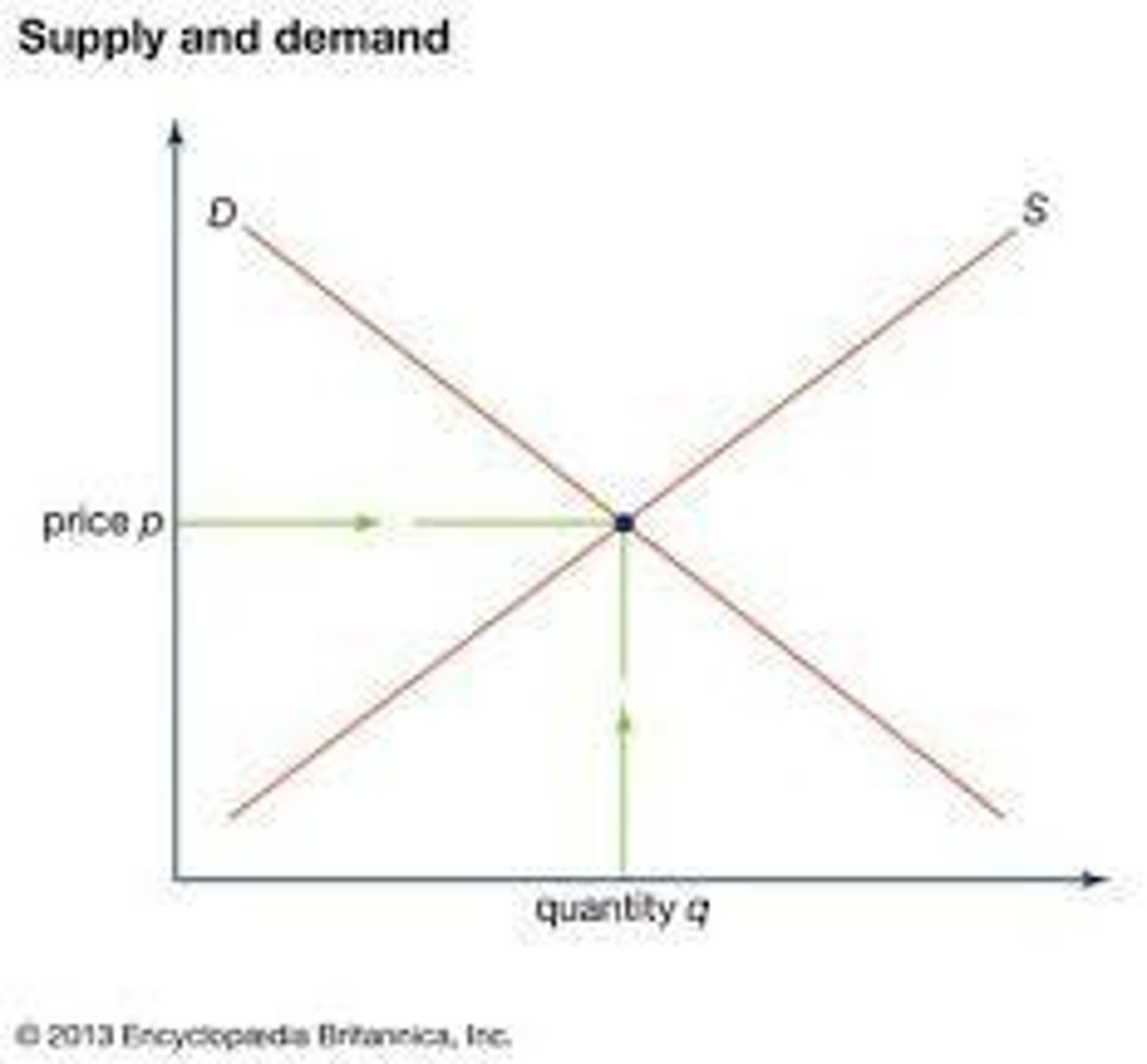

Supply curve

positive relationship between quantity supplied and price

Demand curve

negative relationship between quantity demanded and price

Equilibrium point

intersection point of the supply curve and the demand curve (Only at EP does Qs = Qd)

Price too low

shortage (Qd > Qs)

Price too high

surplus (Qd < Qs)

Price

primary allocator of resources in a free market system. (invisible hand = Adam Smith)

Shortage exists

prices will rise towards equilibrium

Surplus exists

prices will fall towards equilibrium

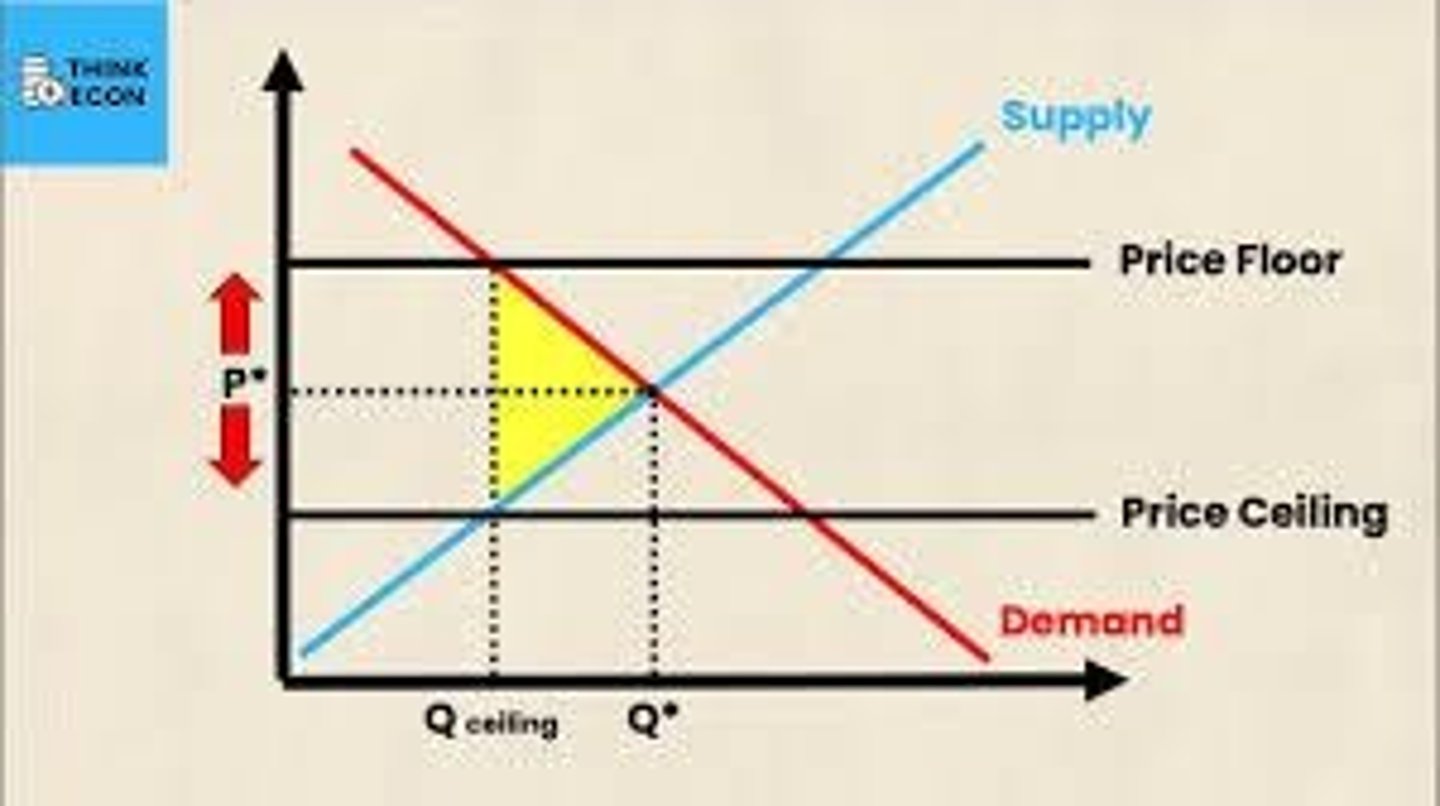

Price ceiling

law that says the price is not allowed to go above a certain price. (rent controls, price gouging laws)

Price floors

Law that says the price is not allowed to go below a certain price. (daily price supports, minimum wage)

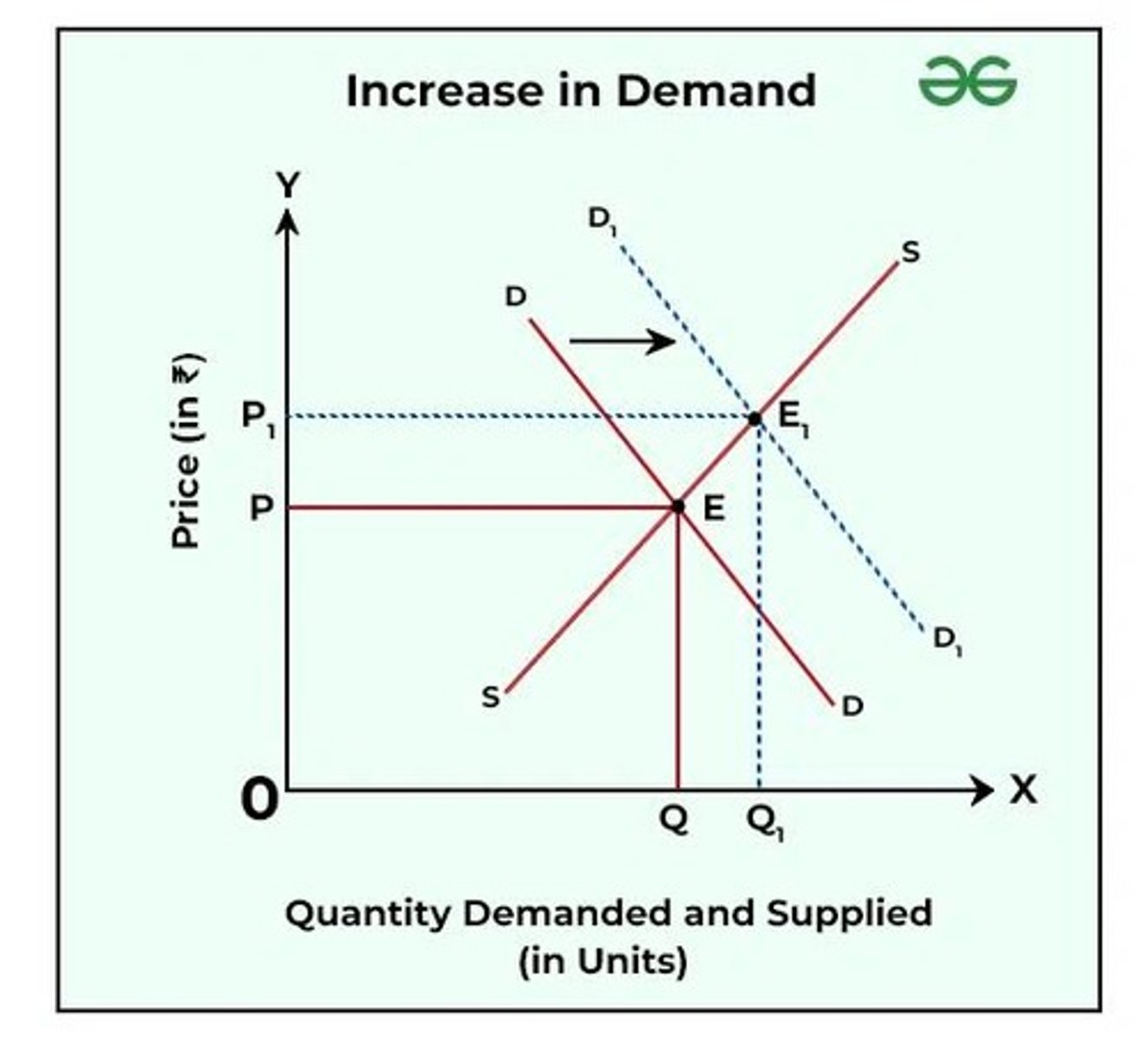

Demand increase

Demand curve shifts right, Price increases, Quantity increases

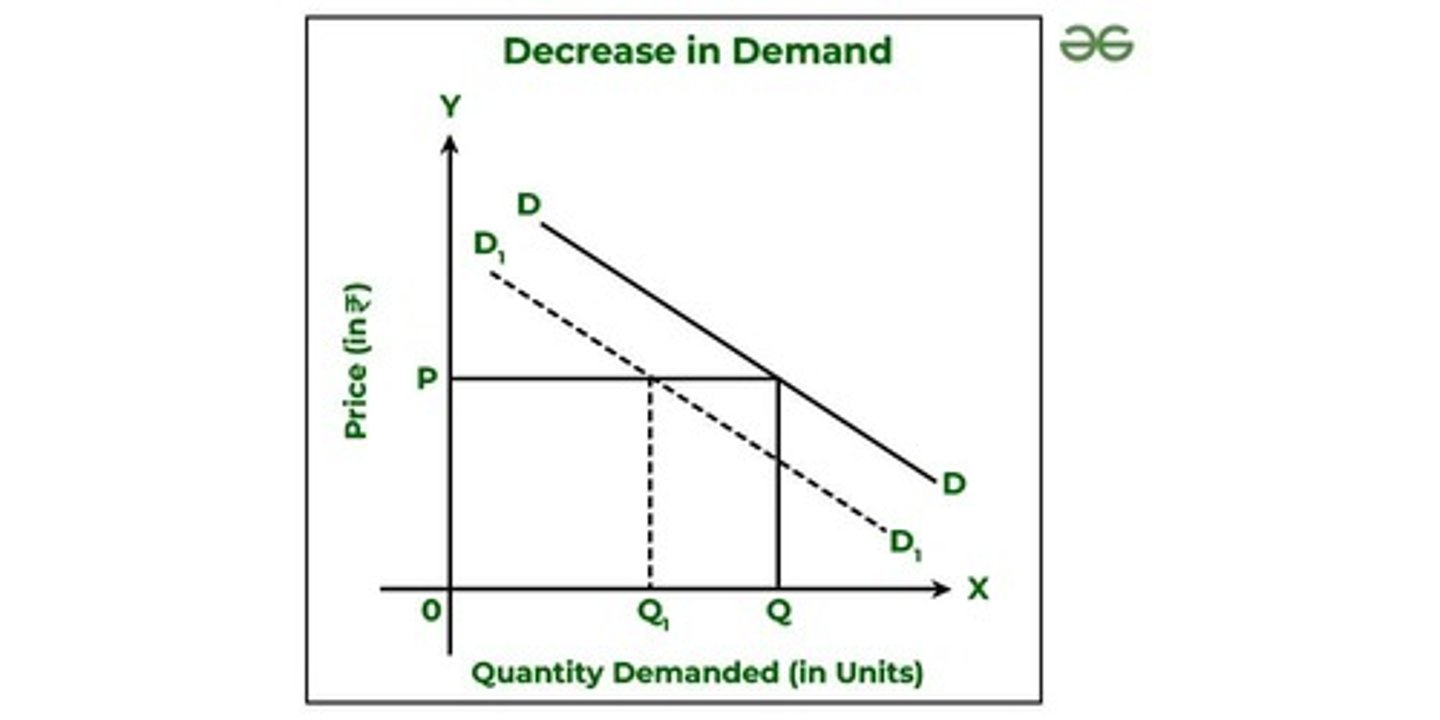

Demand Decrease

Demand curve shifts left, Price decreases, Quantity decreases

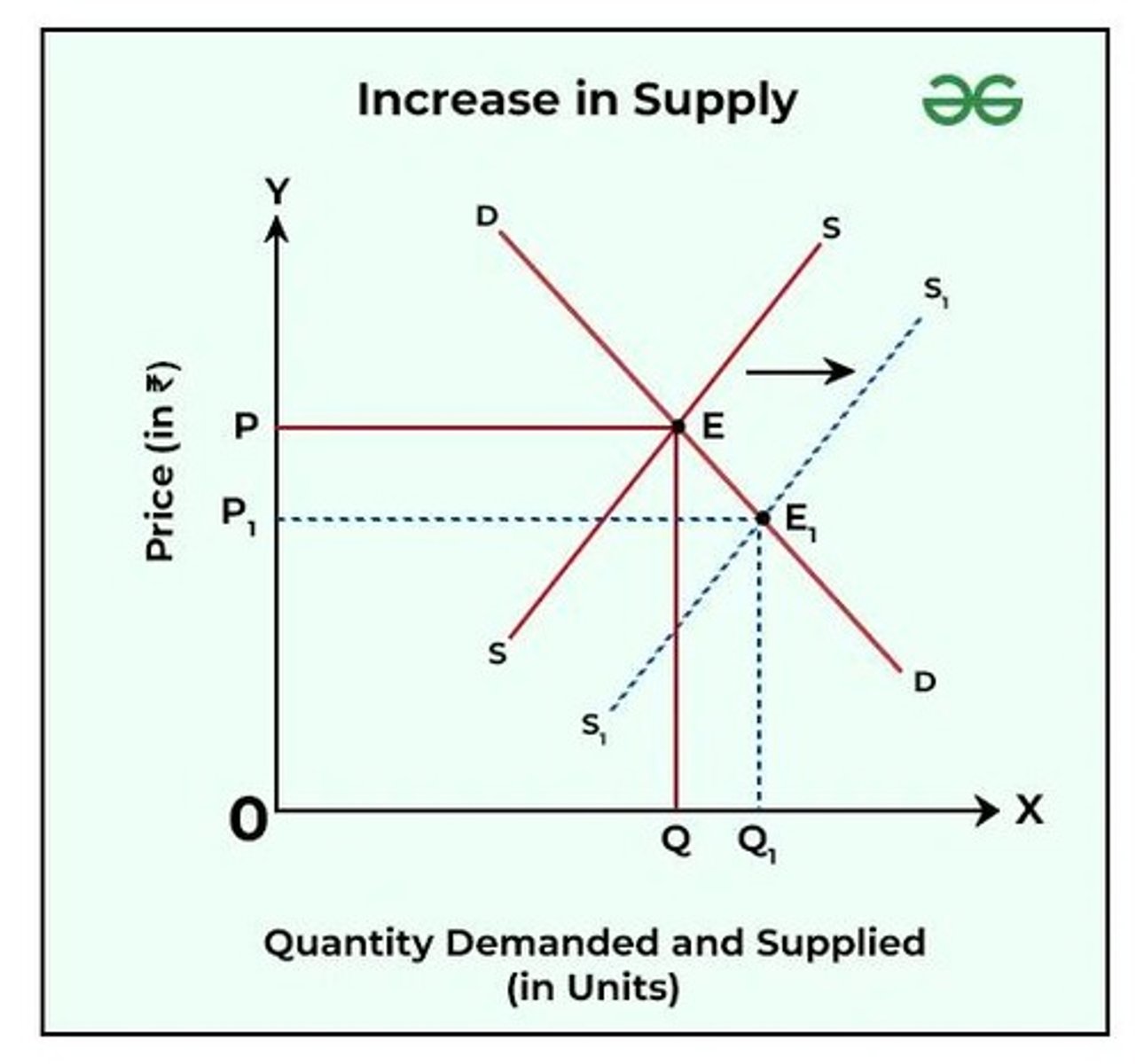

Supply Increase

Supply curve shifts right, Price decreases, Quantity increases

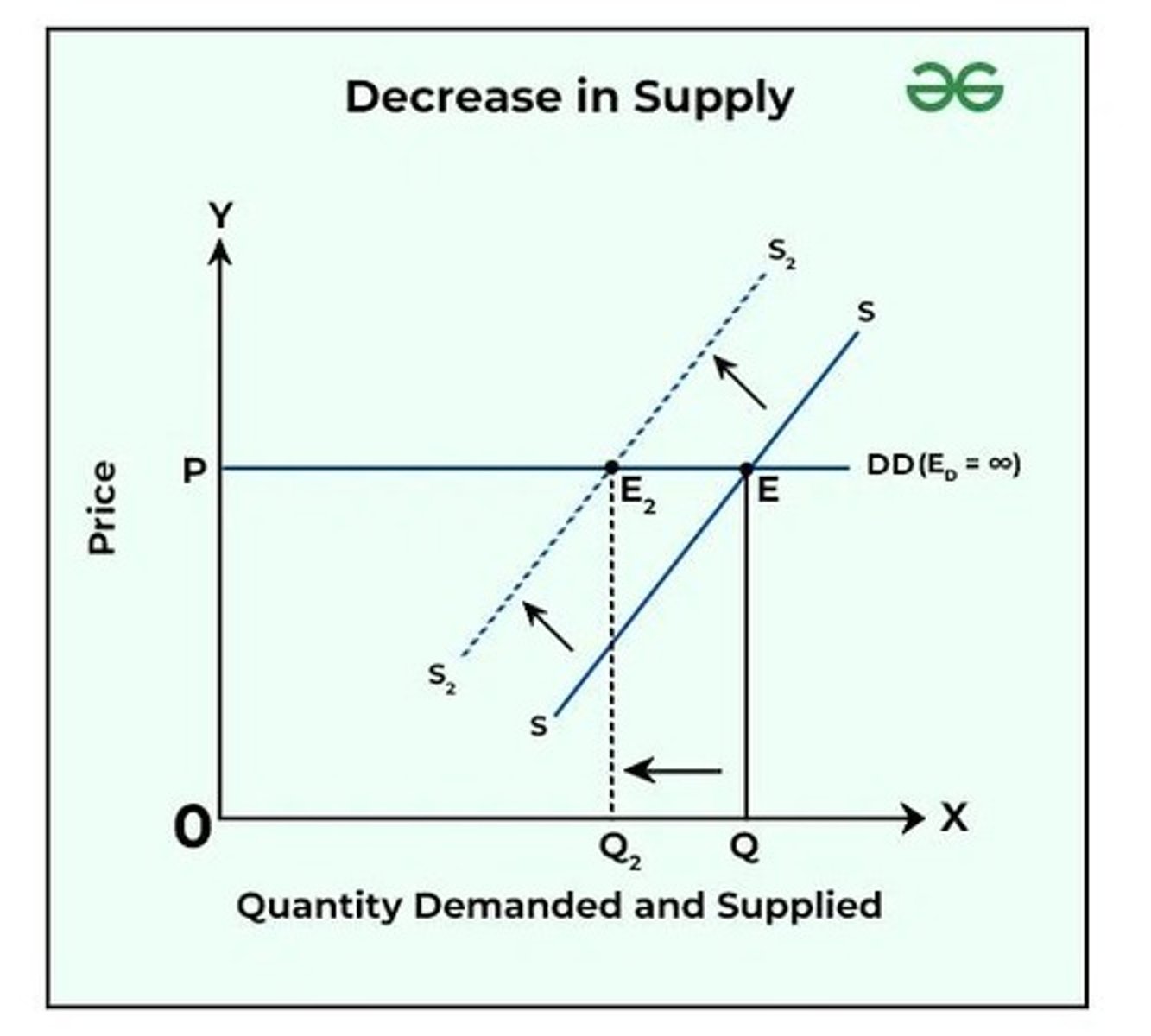

Supply Decrease

Supply curve shifts left, Price increases, Quantity decreases

Normative Economics

how things should be (opinions, values).

Positive Economics

how things are (facts, testable).

Cost-Benefit Analysis

Used by individuals, firms, and governments. Decision rule = Benefits - Costs.

Substitutes

Price of X ↑ → demand for Y ↑ (e.g., Coke & Pepsi).

Complements

Price of X ↑ → demand for Y ↓ (e.g., Coffee & Cream).

Normal Goods

Income ↑ → demand ↑ (e.g., vacations, restaurants).

Inferior Goods

Income ↑ → demand ↓ (e.g., ramen, cheap beer).

Network Effect

Demand rises as more people use it (e.g., social media, iPhones, colleges).

Exogenous Supply Shocks

Sudden events that decrease supply (e.g., storms destroying crops, war reducing oil supply).

Economics

the study of how society allocates scarce resources

Microeconomics

studies individual markets, firms, consumer

Macroeconomics

studies all markets together (the economy)

Scarcity

a limited amount of resources in society.

Opportunity cost

The cost of something is what you give up to get it. Opportunity cost is the value of the best foregone alternative.

You came to class today. What is your opportunity cost of coming to class

whatever you would be doing if you did not come to class

Specialization

when resources such as labor are devoted exclusively or overwhelmingly to a specific production task

Specialization Example

A tax accountant only does taxes. He doesn’t make his own milk from scratch. A dairy farmer makes milk. He doesn’t do his own taxes.

Trade

The foundation of all business activity. Part of everyday life.

Comparative Advantage

The ability of an individual, firm, or country to produce a good or service at a lower opportunity cost than another.

Absolute advantage

the ability to produce more of a good or service with the same amount of resources, or produce the same amount with fewer resources

Production Possibilities Curve

Illustration of the trade-off society faces from scarcity. (Production Possibilities Frontier)

Resources

Land, Labor, and Capital.

PPC shifting outwards

Good. (More output can be produced given the resources)

PPC shifting inwards

Bad. (pandemic, natural disaster)

Opportunity cost

Slope of PPC between 2 points

Ceteris Paribus

All Else Equal

Supply curve

= positive relationship between quantity supplied and price

Demand curve

= negative relationship between quantity demanded and price

Equilibrium point

= intersection point of the supply curve and the demand curve (Only at EP does Qs = Qd)

Price too low

= shortage (Qd > Qs)

Price too high

= surplus (Qd < Qs)

Price

= primary allocator of resources in a free market system. (invisible hand = Adam Smith)

Shortage exists

= prices will rise towards equilibrium

Surplus exists

= prices will fall towards equilibrium

Price ceiling

= law that says the price is not allowed to go above a certain price. (rent controls, price gouging laws) +(Government sets price ceiling = Qd > Qs = shortage)

Price floors

= Law that says the price is not allowed to go below a certain price. (daily price supports, minimum wage) (Government sets price floor = Qd < Qs = surplus)

Circumstances in which society may not want price to allocate resources

= (ex. Organ donations, ethical objections to “markets for everything”)

Demand curve shifts right

Price increases

Quantity increases

Demand Decrease

Demand curve shifts left

Price decreases

Quantity decreases

Supply Increase =

Supply curve shifts right

Price decreases

Quantity increases

Supply Decrease =

Supply curve shifts left

Price increases

Quantity decreases

%change in Quantity/% Change in Price ((NEW – OLD) / OLD)

Example = Suppose that a decline in the price of Good X from

$147 to $145 causes an increase in the quantity

demanded from 8,730 to 8,870.

8870 - 8730 / 8730 = 0.01604

145-147 / 147 = -0.0136

0.01604 DIVIDED BY -0.0136 = -1.179

Example #2 = Suppose that an increase in the price of Good Y from $1,050 to $1,080 causes a decrease in the quantity demanded from 204 to 200.

200 - 204 / 204 = -0.0196

1080 - 1050 / 1050 = 0.2857

-0.0196 DIVIDED BY 0.2857 = 0.0686

-0.686

Susie’s Consumer Surplus = 13600 – 12000 = 1,600

Bob’s Producer Surplus = 12000 – 11200 = 800

Economic efficiency (lesser DWL the better)

Distributional Effects (Vertical Equity)

Horizontal Equity

Simplicity in compliance and ease of administration

Politically acceptable way of raising revenue

Inputs from workers (labor) and other businesses (raw materials and capital / financing)

Costs

Accounting Profit formula

Revenue – Explicit Costs

Economic Profit formula

Revenue – Implicit Costs – Explicit Costs (Accounting Profit – Implicit Costs)

Opportunity costs that show up on a financial statement. Typically money exchanges hands. (Ex: Pizza place paying the bakery for dough.)

Must decide on how much output (Q) to produce. Must decide the method to produce the output. Must decide on product attributes. Must decide on any alternative pricing schemes

Marginal Cost

the additional cost incurred from producing one additional unit of output (the change in total cost from producing one more unit of output.)