Ch. 15: Monopoly

1/37

Earn XP

Description and Tags

Definitions, concepts, and practice questions for Ch. 15 of Principles of Economics by Gregory Mankiw.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

38 Terms

Monopoly

A firm that is the sole seller of a product with no close substitutes

Q: What is the fundamental cause to monopoly?

Barriers to entry (other firms cannot enter the market and compete)

Three main sources of barriers to entry

Monopoly resources

government regulation

the production process

Barrier to entry: Monopoly resources

One firm has sole access to a key resource

Barrier to entry: Government regulation (Government-created monopolies)

The government gives one person/firm the exclusive right to sell a good/service

(ex. patent and copyright laws)

Barrier to entry: The production process (Natural monopoly)

A single firm can provide a good/service to a market at a lower cost than could two or more firms

(ex: supplying water to a town)

Q: Some government grants of monopoly power are desirable if they

A: provide incentives for innovation

Q: A firm is a natural monopoly if it exhibits _________ as its output increases.

A: decreasing average total cost

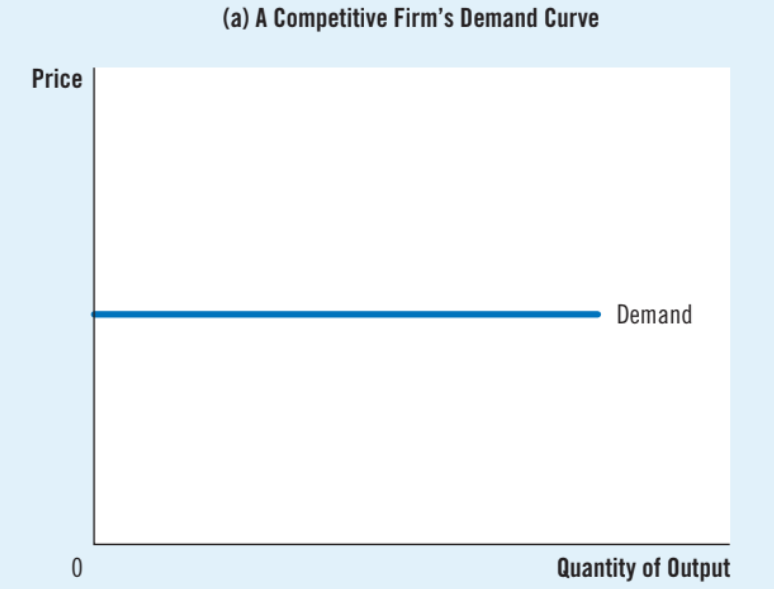

Demand curve of a competitive firm

Horizontal, perfectly elastic due to many perfect substitutes (price taker)

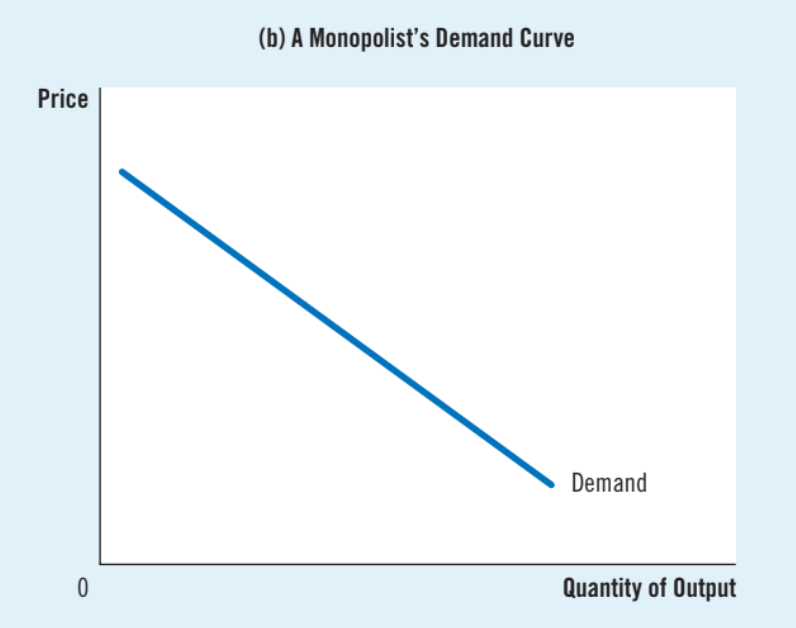

Demand curve of a monopoly

Slopes downward, it is the market demand curve because the firm is the sole producer in the market

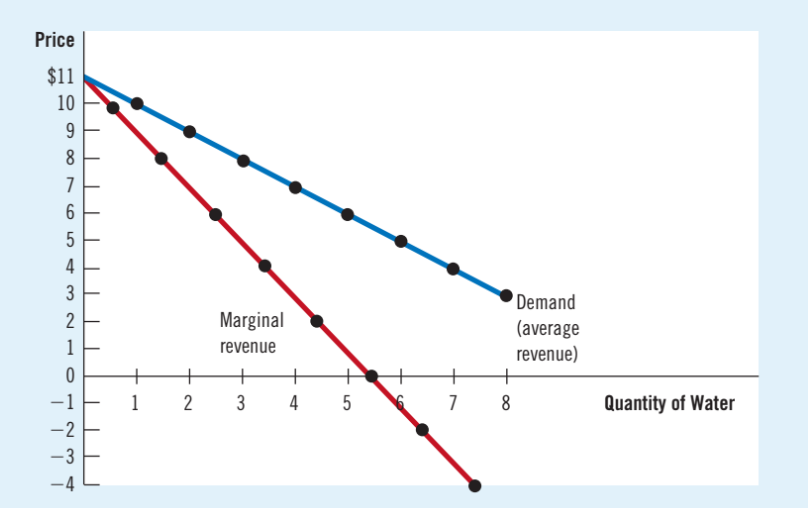

Q: A monopolist’s marginal revenue is _______ the price of its good

A: less than

The output effect

When more output is sold, Q is higher, which increases total revenue

The price effect

The price falls, so P is lower, which decreases total revenue

Q: Is a competitive firm affected by the price effect?

A: No. When production is increased by one unit, they receive market price, and do not receive less for units they were already selling. (Marginal revenue = price)

Q: Is a monopoly affected by the price effect?

A: Yes. When production is increased by one unit, they must charge less for every unit they sell, and receive less revenue for units they were already selling (Marginal revenue < price)

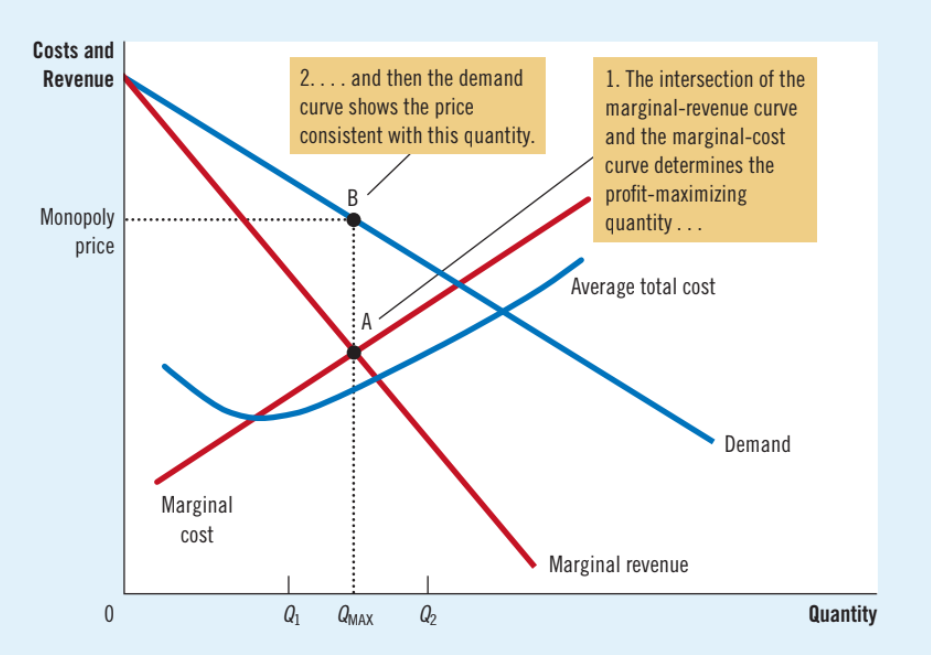

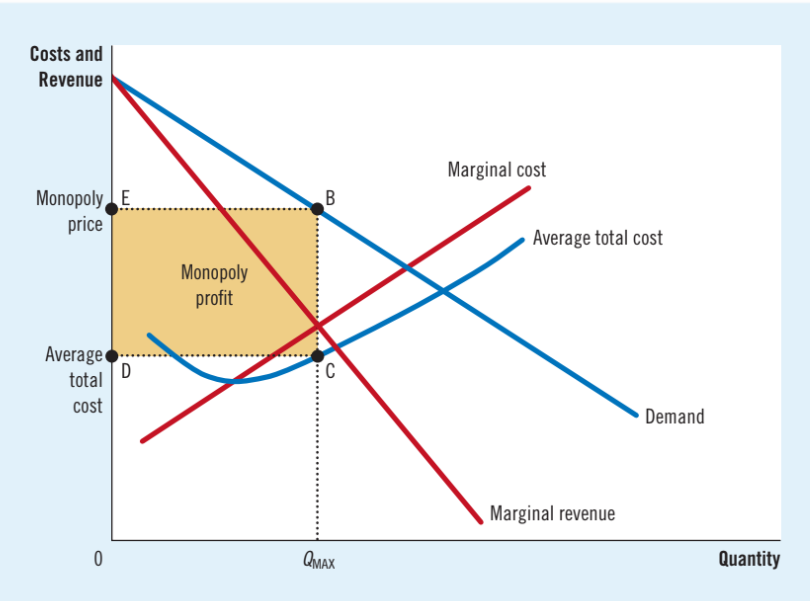

Monopoly profit maximizing

Profit is maximized at the intersection of the marginal revenue and marginal cost curve

Q: In a competitive firm, price _____ marginal cost. In a monopolized market, price _______ marginal cost.

A: equals, exceeds

Profit formula

P = (P - ATC) X Q

Profit maximizing rules for a monopolized firm

1. Derive the MR curve from the demand curve.

2. Find Q at which MR = MC.

3. On the demand curve, find P at which consumers will buy Q.

4. If P > ATC, the monopoly earns a profit.

Q: If a monopoly’s fixed costs increase, its price will ________ and its profit will _________.

A: Stay the same, decrease

Q: The monopolist produces ____ than the socially efficient quantity of output.

A: less

Q: Is monopoly profit a social cost?

A: Monopoly profit is not a social problem: producers are better off and consumers are worse off, but there is no change in total surplus.

Social cost of monopoly inefficiency

Monopolies produce and sell a quantity below the level that maximizes total surplus (inneficiently low amount of output)

Price discrimination

the practice of selling the same product at different prices to different consumers

Perfect price discrimination

The monopolist knows each customer’s exact willingness to pay and can charge each customer a different price, receiving all surplus

Q: When a monopolist switches from charging a single price to practicing perfect price discrimination, it reduces __________.

A: consumer surplus

Four ways the government responds to monopoly

Increasing competition through antitrust laws

Regulating behavior of monopolies

Public ownership

Doing nothing

Horizontal merger

a merger between two firms in the same market (more scrutinized)

Vertical merger

merger between firms at different points in the production process (less scrutinized)

Antitrust laws

group of statutes aimed at curbing monopoly power (Sherman Antitrust Act, Clayton Antitrust Act)

Synergies

benefits from a merger (lower administrative costs, lower production costs, etc)

Regulation

Government agencies regulate the price of monopolies

Problem with regulation

marginal cost and average total cost pricing both generate deadweight loss

Public ownership

Government-run monopoly

Problem with public ownership

The profit motive does a better job of ensuring firms are well run than the government system

Q: If regulators impose marginal cost pricing on a natural monopoly, a possible problem is that _________.

A: the firm will lose money and exit the industry