10.5 Profit Maximization in the Long Run

1/20

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

21 Terms

What is the key difference between the short run and the long run in perfect competition?

In the short run, the number of firms and plant size are fixed.

In the long run, firms can enter, exit, expand, or contract.

Can firms exit the industry in the short run?

No. They can shut down temporarily (produce zero output), but they cannot leave the industry.

What drives long‑run adjustments in a competitive industry?

Profits and losses — not the calendar.

Entry happens when profits exist; exit happens when losses exist.

What are the three assumptions used for long‑run analysis?

Entry and exit only

Identical costs for all firms

Constant‑cost industry (entry/exit doesn’t change ATC)

What is the main long‑run result in perfect competition?

Price = minimum ATC, and firms earn zero economic profit.

Why does price equal minimum ATC in the long run?

Because entry eliminates profits and exit eliminates losses until only normal profit remains.

What does zero economic profit mean?

Firms cover all costs, including opportunity cost. They earn a normal profit.

In long‑run equilibrium, what is true about incentives to enter or exit?

There are none — firms are earning exactly normal profit.

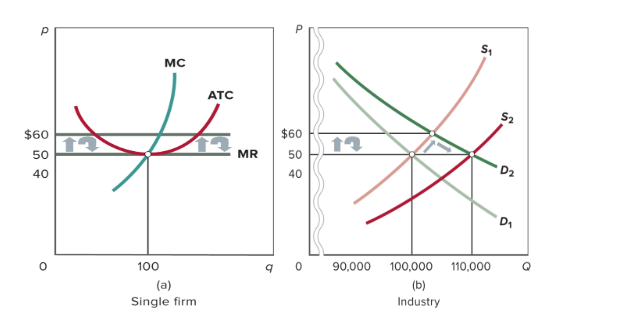

What happens when demand increases in a competitive industry?

Price rises → firms earn economic profit → new firms enter → supply increases → price falls back to minimum ATC.

What happens to the number of firms when demand increases?

It increases. Example: from 1,000 firms to 1,100 firms.

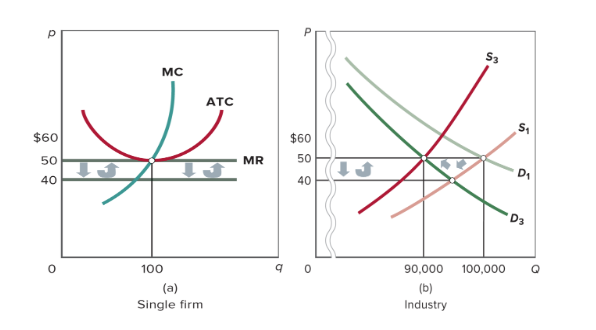

What happens when demand decreases in a competitive industry?

Price falls → firms incur losses → firms exit → supply decreases → price rises back to minimum ATC.

What happens to the number of firms when demand decreases?

It decreases. Example: from 1,000 firms to 900 firms.

Why does entry eliminate economic profits?

More firms increase supply, which pushes price down until it equals minimum ATC.

Why does exit eliminate losses?

Fewer firms decrease supply, which pushes price up until it equals minimum ATC.

In long‑run equilibrium, what output does each firm produce?

The output where ATC is minimized (e.g., 100 units in the example).

How do we find the number of firms in the industry?

Divide total industry output by output per firm. Example: 100,000 ÷ 100 = 1,000 firms.

What is the fallacy of composition in this context?

One firm cannot affect price, but all firms together do affect price.

What does a constant‑cost industry imply about cost curves?

ATC and MC do not shift when firms enter or exit.

What forces firms to produce at minimum ATC in the long run?

Competition — only firms operating at minimum cost survive.

What is the long‑run industry supply curve like in a constant‑cost industry?

Perfectly elastic (horizontal) at minimum ATC.

What is the firm’s supply curve in long-run?

The firm’s supply curve = its MC curve above the minimum AVC.