Final Exam MTHEL 131

1/163

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

164 Terms

Risk

Variability in future outcomes over a specific time

Risk: Importance

Can cause us to use resources inefficiently, often because individuals are believed to be risk averse

ERM: Purpose

Minimize the negative effects of risk

Enterprise Risk Management (ERM)

Decision-making process by which negative3 effects of risk are minimized

Risk Averse

Willing to give up value to reduce variability risk

Risk: Negative Effects

Giving up possible opportunities/benefits because of risk

Spending resources with the intent of reducing risk

Spending resources with the intent of paying for losses if they happen

ERM: Process

Set Objectives

Identify RM problems

Measure RM problem dimensions

Identify and evaluate alternatives to manage risk

Select among alternatives and implement selection

Monitor the system

Risk: Types of Situations

Speculative vs. Pure

Diversifiable vs. Non-diversifiable

Pure Risk

Equal-to or worse-off after situation

Diversifiable Risk

Offset-able. Ex. a company sells both umbrellas and sunscreen

GARP Wheel

There are many types of risk and ERM is represented in the centre of the wheel to incorporate all risks

Objectives: Types

Strategic: An organization's mission/goal

Operational: Day-to-day activities to achieve strategy

Risk management: Actions designed to ensure ability to meet operational objectives

Objectives: Communication

Internal documents: Mission statement, employee handbook, etc.

External communication: Advertisements, new releases, spokesperson, etc.

Objectives: Examples

Survive

Continuity of operations

Maintain expenses below some level

Hold variability below some level (stable earnings)

Meet outside responsibility (complying legally)

Be socially responsible

Some risks are non-diversifiable

True

Risk reduction is not costly

False

Risk is associated with only foreseen cost fluctuations

False

Exposures

Underlying assets that may experience loss. Ultimately the intention is to identify the existence and value of each exposure.

Exposure: Types

Property

Liability

Human capital / employee benefits

Consequential

Peril

Direct causes of loss. We try to know the probability and velocity of relevant perils

Hazard

Conditions that increase the probability and/or severity of loss. We try to know hazards

Hazard: Types

Physical

Economic

Cultural: social, political, regulatory, legal

Cognitive and behavioural

Moral Hazard

Behaviour that makes negative outcomes more likely and/or larger, induced by the fact that costs are not borne entirely by the actor

not necessarily intentional

Physical Assets: Property

Ownership:

Real property

Personal property

Use/possession

How to value a physical asset for risk/insurance purposes

Replacement cost. For ex., If a machine is destroyed, the firm must:

Replace it or shut down production.

Replacement cost determines how much insurance is needed

Value in Use

The economic cash flows an equipment generates in the future

Replacement Cost

Typically the insurance amount. i.e. the cost to replace property

Physical Assets: How to Identify

Document analysis (financial statements)

Inspections/interviews

Expertise outside the organization

Compliance review

Liability

The legal responsibility to remedy some harm experienced by another party. The effect is an allocation of costs

Liability: Exposure

Financial assets used to fulfill the responsibility to pay for another party's harm

Liability: Peril

The filing of a legal claim (not the occurrence of harm)

Liability: Hazard

Wrongful conduct, poor record keeping, operating in locations where laws are more favourable toward plaintiffs than defendants, etc.

Tortious Conduct

Type of wrongful conduct, intentional and unintentional.

Negligence

The failure to is the failure to exercise reasonable care, resulting in unintended harm or loss to another party. It is the foundation of liability in Canada

Negligence: Requirements

Owe a duty

Breach the duty

Harm

The breach of duty is the proximate cause of harm

Unreasonable Behaviour: How It's Shown

Court, precedent rulings

Learned Hand's Ruling

Learned Hand's Ruling

If Cost to prevent harm > Pr(loss) x size of loss, then it is reasonable to not prevent

Negligence: Defenses

Contributory negligence, comparative negligence

Contributory Negligence

The plaintiff is partly responsible for their own injury.

If the plaintiff failed to take reasonable care for their own safety, their damages are reduced.

Comparative Negligence

Fault is divided between plaintiff and defendant by percentage.

Each party is assigned a percentage of responsibility.

The plaintiff's damages are reduced in proportion to their fault.

This is the dominant modern approach in Canada

Assumption of Risk

The plaintiff knowingly and voluntarily accepted the risk of harm.

Defendant argues the plaintiff understood the danger and chose to proceed anyway

Example: Signing a waiver before a dangerous activity.

Cap on General or Punitive Damages

The law limits how much money a plaintiff can receive.

Even if the defendant is negligent, damages may be legally capped for:

Pain and suffering (general damages)

Punitive damages

Contributory vs. Comparative Negligence

Contributory negligence asks whether the plaintiff was negligent. Comparative negligence asks how much each party was negligent

Fault

Refers to blameworthy conduct

Expansions of Liability

Joint and several liability

Vicarious liability

Strict liability

Joint and Several Liability

Each defendant can be held responsible for the entire loss.

Applies when multiple defendants cause the same harm.

Plaintiff may recover 100% of damages from any one defendant, even if that defendant is only partly at fault.

That defendant can later seek contribution from others.

Vicarious Liability

One party is held liable for the negligence of another.

Most common relationship: employer-employee

Employer is liable for negligent acts committed within the scope of employment, even if the employer did nothing wrong.

Vicarious Liability: Key Question

Was the employee acting in the course and scope of employment when the harm occurred?

Strict Liability

Liability without fault.

Plaintiff does NOT need to prove unreasonableness or negligence.

Instead, must show:

A dangerous condition or activity

The condition caused the loss

Worker's Compensation

Workers' compensation is a system to pay workers for their work-relatedinjuries/illnesses. The employer provides payment and it is required by statute.

Worker's Compensation: Conditions

Accident/no fault

Arising out of employment

In the course of employment

Worker's Compensation: Coverage

Reasonable medical expenses

Rehabilitation expenses

Portion of lost wages

Portion of Lost Wages: Formula

0.85 x Min(weekly wage, Ontario average wage)

Worker's Compensation: Purpose

To ensure compensation for workplace injuries and specify payment

To improve safety and spread costs of injuries

Reduced administrative costs

Worker's Compensation: Execeptions

Volunteers, owners do not count

Generally < 3 employees

Some employment sectors

Human Capital: Exposure

To employee:

Financial & emotional costs of medical care, lost wages, satisfaction/feeling good

To employer (our focus):

Intellectual capital, Cost of searching for, hiring, training, developing, keeping talent, Financial assets used to pay for liabilities, Financial assets used to pay for non-wage compensation (employee benefits)

Employee Benefits: Peril

Employee's inability to earn income

Disability, Retirement, Unemployment

Employee's use of health care

Employee Benefits: Hazards

Workforce characteristics

Labour supply

Pension Plan: Types

Defined benefit (DB)

Defined contribution (DC)

Pension Plan: Defined Benefit

Employer promises a certain pension amount to the employee upon retirement(benefit amount calculated by a formula)

Pension Plan: Defined Contribution

Employer promises to create a fund on behalf of the employee, and decides anamount to be paid into the fund (contribution) each pay period

Pension Plan: Contributory vs Non-Contributory

Either type of pension plan may be "contributory," where employees pay into the system (and often the employer does as well) or "non-contributory," where only employers pay into the system

Common Law

A body of law derived from judicial decisions and precedents rather than statutes. It evolves through court rulings and is foundational to many legal systems.

Consequential Loss

Conditions that may result in a reduction in revenues and/or increase in expenses due to the disruption of normal operations caused by some other event (loss).

Consequential Loss: Exposure

Net income

Consequential Loss: Peril

loss of use of property

Develop Probability Distributions: Methods

Identify all possible outcomes

Calculate probabilities for all possible outcomes

Identify All Possible Outcomes: Types

Collectively exhaustive: account for all possibilities

Mutually exclusive: the occurrence of one outcome preludes the occurrence of another

Probability Distribution: Mean

Probability Distribution: Range

Largest value - smallest value. Range represents the total spread between the minimum and maximum possible losses or claims, providing a measure of potential risk exposure

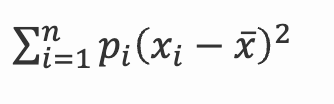

Probability Distribution: Variance

x^— is the mean. Variance quantifies overall uncertainty and risk in claim sizes or frequencies for premiums

Probability Distribution: Standard Deviation

sqrt(variance). Standard deviation represents the typical deviation of actual losses from their mean, offering a scale for risk assessment.

Probability Distribution: Coefficient of Variation

Standard Deviation/ Mean. Coefficient of Variation represents a relative measure of dispersion or risk

Probability Distribution: Value-at-Risk (VaR)

Maximum probable loss. If an organization is risk averse, then they will increase their VaR as the organization sets a higher safety buffer for potential losses.

Value-at-Risk (VaR): How Organizations Increase

Buy insurance: VaR becomes more predictable

Diversify Operations

Hold more capital

Uncorrelated/Independent Events

The occurrence of one event does not indicate anything about the probability of the other

Correlated/Dependent Events

The occurrence of one event tells us something about the probability of the other

Expected Loss Formula

Pr(loss)(value of loss)

Pooling

Combining risks or losses from many individuals to make the outcomes more predictable. With pooling, the expected loss per person does not change, but the risk per person decreases

Law of Large Numbers

As the number of observations increase, the relative dispersion decreases

Law of Large Numbers: Key Facts

Larger losses are not necessarily more predictable than smaller losses

The law of large numbers explains how pooling can increase predictability

Resource allocation decisions can be made with greater relative certainty as the number of observations increases

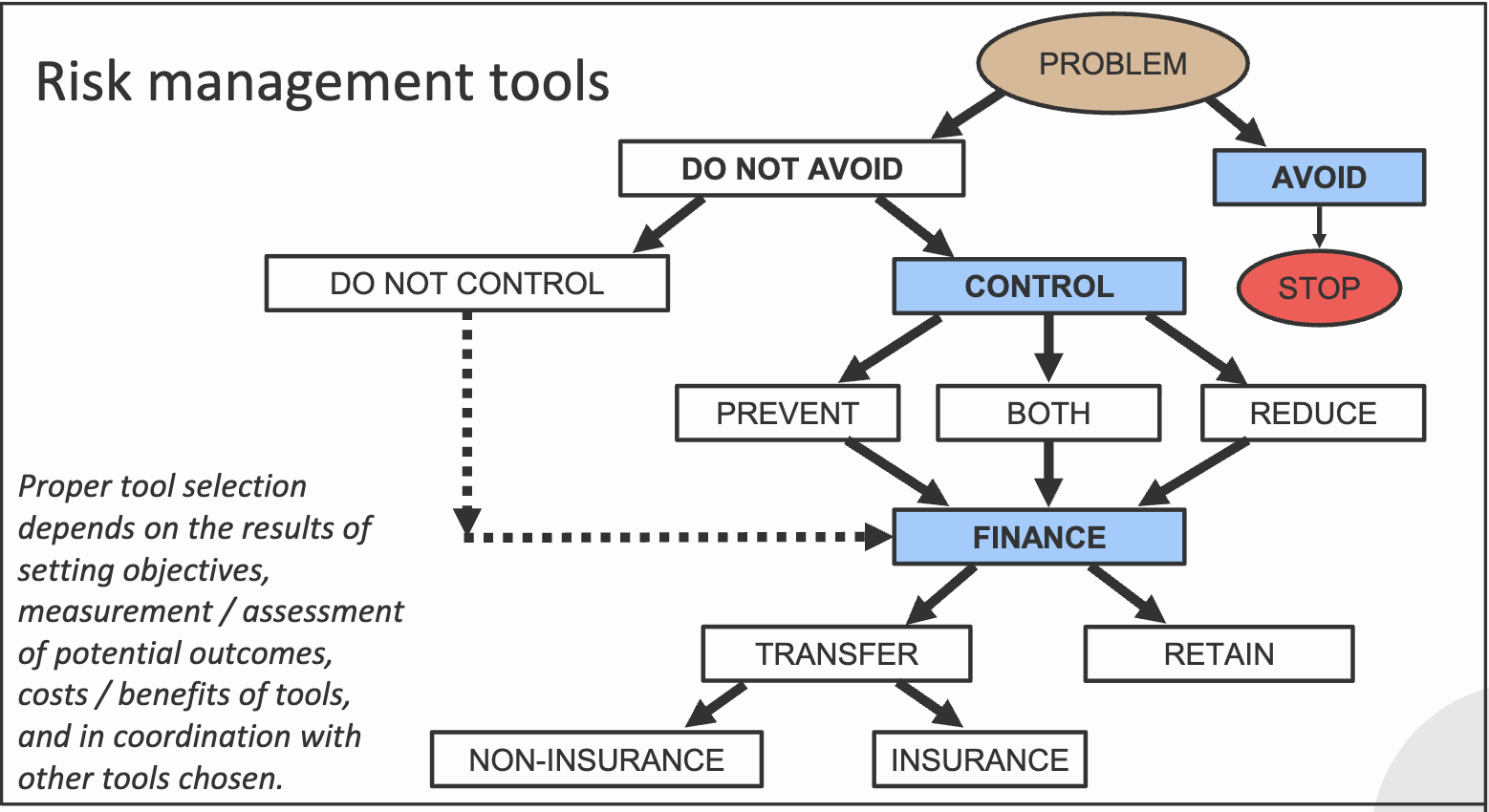

Risk Management Tools: Purpose

To reduce variability

Avoidance

Making decisions with the intention of eliminating either: Some potential for loss or a future potential for loss from a new venture.

Lost opportunities

Elimination is the extreme form of avoidance

Risk/Loss Control

Actions that reduce frequency and/or severity of loss

Risk/Loss Control: Mechanisms

Prevention: any measure that reduces the probability of loss

Reduction any effort that lessens the severity of losses that occur/occured

Reduction: Segregation

Lower the dependence on any single asset, activity, or person, and as

a result, each loss is smaller in size

Segregation: Examples

Separation: diversification

Duplication: reproduce assets with the duplicate’s purpose as a back-up

Reduction: Crisis Management

Plans of action to prepare for an emergency

Risk/Loss Control: Heinrich’s Domino Theory

Focuses on people’s behaviour

Social environment leads to fault of person leads to unsafe act leads to accident leads to injury (SFUAI)

Emphasizes the intervention of the “unsafe act” phase

Risk/Loss Control: Haddon’s Release of Energy Theory

Focuses on physical environment

Suggests that accidents result from the release of excess energy

Suggests that loss control is possible by suppressing build-up of energy and enhancing accident-retarding conditions

Risk/Loss Financing

Paying for losses not avoided

Risk/Loss Financing: Types

Retain: Do not shift risk but rather pay for losses directly as they occur

Transfer: Shift risk to another party

Risk Management Tools: Diagram

Pooling: Benefits

Organizations and entities opt to pool their losses because the standard deviation decreases. This causes variability and individual risk to decrease.

Pooling: Why it Fails with Positive Correlation

Pooling works because risks are independent. So, If risks are positively correlated, then losses happen together. So:

Variability does not decrease

Insurer can’t diversify risk

Evaluate RM Alternatives: General Criteria

Choose tools to support organizational objectives

Choose tools to promote efficiency

Retention

Pay for losses directly out of the organization’s own funds, so “retain risk.”

Retention: Types

Passive: not even being aware of the potential for loss

Current expensing: paying losses as they occur as normal operating expenses

Reserving: Setting up liability account that reflects the losses over time. Expense losses in each period (accrual accounting) even though they will be paid in the foreseeable future