Microeconomics

1/231

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

232 Terms

Free goods

Goods that are not scarce and therefore available without limits. Zero opportunity cost e.g. Air

Economic goods

A consumable item that is useful to people but scarce in relation to its demand

Opportunity cost

The value of the next best alternative foregone

Positive statement

An objective statement that can be tested, amended or rejected by referring to available evidence

Normative statement

A value judgement that is a subjective statement of opinion rather than a fact that can be tested

Needs vs Wants

Needs are defined as goods or services that are required and cannot be done without. Wants are goods or services that are not a necessity but we desire/wish for

Cost-benefit principle

Every purchase is a trade-off

Rational decision makers

An assumption that economic agents weigh the marginal benefit that one receives from a good or service against its marginal cost

Economic agents

Decision makers that have effects on the economy of a country by buying selling, producing, investing, taxing, etc. Government, firms and households

Government

Elected representative of the consumers that should act on behalf of the people. The government must decide whether or not to intervene in the economy or leave it as is.

Firms

An organisation that uses factors of production alongside each other in order to produce output. They produce goods and services demanded by consumers

Households

A group of consumers that buy goods and services. They also supply their labour to firms to produce goods and services in order to earn the income needed to purchase g+s

Factors of production

The available resource inputs used in the production process of g+s (Capital, Enterprise, Land and Labour)

Capital

Man made aids for production; goods used to make other goods

Entrepreneurship

The willingness of an entrepreneur/individual to take risks and organise production. An entrepreneur is someone who bears the risk of a business and organises production

Labour

The human resource that is available in the economy; the quantity and quality of human resources

Land

The natural resources available in the economy; the quantity and quality of natural resources

Factor payments/rewards

Capital=Interest

Enterprise=Profits

Labour=wages

Land=rent

A model

A simplified representation of reality used to create hypotheses about economic decisions and events

Production

Any economic activity that leads to a flow of goods and services for which people are willing and able to pay

Production possibility frontier

A curve showing the maximum quantities of different combinations of goods and services that can be produced in a set time period given the available resources and current state of technology

Law of diminishing returns

As a firm adds variable factors of production(usually labour) to fixed capital, the marginal returns that the firm gains will gradually begin to decrease

Consumer good

A finished good that is sold for consumption

Capital good

Ant tangible asset that an organisation uses to produce goods or services such as office buildings, machinery etc.

Specialisation

Where individuals, businesses and whole economies are not self-sufficient but concentrate on producing certain goods and services, then trading their surplus.

Division of labour

The assignment of different parts of a manufacturing process or task to different specialised people in order to improve efficiency

Productivity

Output of a good or service, per factor of production, per period of time

Functions of money

A medium of exchange-it should be accepted universally for the payment of goods, services and debt

Unit of account-It allows the value of goods, services and other assets to be compared so that the prices of products reflect the value that society places on them

Standard of deferred payment-Money can be used to pay back debt

Store of value-It must be possible to use for future transactions and so it must be non-diminishable

Resource allocation

The way in which a society's factors of production are divided amongst their alternative uses

Objectives of households

Households make decisions about how to allocate expenditure based on the utility they derive from consuming a good or service

Objectives of firms

Firms make decisions about what to produce and how much to produce (how to use their factors of production) in order to receive a return/profit for their endeavours.

Objectives of the government

Government's objectives are to maximise social welfare and will do this through decision making regarding taxation to fund public expenditure, enforcement of laws and regulation that provide a system for the market to work in. May aim to achieve 'macroeconomic performance indicators'

Utility maximisation

The aim of trying to achieve the highest level of satisfaction possible from the consumption/production of a good

Profit maximisation

The aim of trying to achieve the highest levels of profit possible

Incentives for households

Their decisions will depend on the benefits gained form consumption relative to the costs involved. Both including the price and the opportunity cost of consumption A04: Time delays may mean consumers may take time to respond to changes in price and firms may take time to respond to consumer's changes in tastes. Workers may also not seek the highest wage possible as they may do a job to fulfil a sense of vocation or for the non-pecuniary benefits.

Incentives for firms

Firms decisions will depend on the potential profits that supplying a product can create. EG. if the price of a product rises, a firm has an incentive to provide more of it assuming that this increases the return they can make from producing it. A04: Not all firms are profit maximisers

Incentives for governments

Governments base their decisions on how they can further meet the political ideals of those in power, which are typically based on improving people's quality of life. A04: Government officials may be driven by self interest and not what is best for society

Market economy

An economy in which the market forces of demand and supply determine the allocation of resources

Centrally planned economy

An economy in which the state determines the allocation of resources

Mixed economy

An economy in which both the market forces of supply and demand, and also the intervention of the state, determine the allocation of resources

Capitalism

An economic system characterised by the private ownership pf productive resources, and the ability of individuals to freely pursue their self-interest with minimal interference from the government

Market economy characteristics

Self-interest

Private ownership of property

Free choice and enterprise

Competition

Decentralised decision making-'The invisible hand'

Limited government intervention

The invisible hand

A term coined by Adam Smith to describe the way in which buyers and sellers are brought together due to self-interest as the buyer wants the product, the seller wants to sell the product to fulfil their objectives.

Market economy advantages/Centrally planned disadvantages

Choice

Innovation

Efficiency

Market economy disadvantages/Centrally planned advantages

Public, merit, demerit good provision

Unequal distribution of income

Environment

A market

An arrangement by which buyers and sellers negotiate the exchange of goods and services

Sub-market

A recognised or distinguishable geographic, economic or specialised subdivision of a market, also known as a market segment

The price mechanism

Provides the information needed to co-ordinate the workings of a market economy and ensure that decisions can be taken at a decentralised level by millions of individual consumers and producers operating in thousands of different markets.

Functions of the price mechanism

Rationing-Scarce resources are divided among their competing uses according to what is demanded

Signalling-The price of a product reflects the market conditions and signals if producers should increase or decrease production

Incentive-Prices act as an incentive for both consumers and producers, low prices encourage consumers to purchase more and suppliers will leave the market due to low profit margins forcing the price back up, whilst high prices encourage producers to enter the market or produce more, increasing supply and pushing the price back down.

Demand

The quantity of a good or service that consumers are willing and able to purchase at a given price

Law of demand

A law that states that, ceteris paribus, there is an inverse relationship between the quantity demanded and price of a product

Notional demand

The desire or want for a product

Effective demand

The willingness to buy a good or service, backed up by the purchasing power to buy it

Demand curve

A graph that shows how much of a product will be demanded at any given price

Demand schedule

The collection of data that is used to draw a demand curve for a product

Individual demand

The amount of a good or service that an individual consumer is willing and able to buy at any given price over a period of time

Market demand

The sum of all the individual demand curves

Composite demand

When a good has various uses, Rising demand for one rations the availability of the good for another use. E.g. milk for yoghurt or cheese

Derived demand

Where the demand for a good or service is determined by the demand for another good or service E.g. demand for labour is only there as there is a demand for the goods they produce

Joint demand

When two goods are complementary and needed together e.g. printers and printing ink.

Competitive demand

A market where there are two goods offering very similar products from which consumers can derive very similar levels of satisfaction e.g. two brands of mineral water are substitutes and are therefore in competitive demand

Why is the demand curve downward sloping?

The law of diminishing marginal utility-as more of a product is consumed, the marginal benefit to the consumer falls, hence the consumer is prepared to pay less

The income effect-As prices rise, the amount of disposable income falls

The substitution effect-As prices rise, consumers will start to evaluate alternatives

Demand shifters

Population

Price of related goods

Changes in interest rates

Expectations of future prices

Seasons

Changes is tastes and advertising

Legislation

Average disposable incomes

Consumer surplus

The difference between the amount the consumer would be willing to pay and the amount the consumer actually paid

Marginal social benefit

The additional benefit that society gains form consuming one more unit of a product

Supply

The quantity of a good or service that producers are willing and able to offer at different price levels over a period of time

Law of supply

A law that states that, ceteris paribus, there is a direct relationship between the quantity supplied and the price of a good or service

Supply curve

A graph that shows how much of a product will be supplied at any given price

Market supply

The sum of all the individual supply curves/the total supplied to the market

Competitive supply

When a firm can use its factors of production to produce more than one type of product

Composite supply

(Rival supply)-when supply of a product comes from more than one source; a product whose demand can be satisfied through various sources e.g. electricity as it can be satisfied through various sources like hydroelectric, geothermal, wind energy, gas etc

Joint supply

When a firm can produce more than one type of product with roughly the same factors of production e.g. the supply of beef and leather both using cows

The market period

The ultra short-run. Day of the market, and supply is perfectly inelastic with all factors of production fixed

The short-run period

At least one factor of production is fixed whilst others can be varied-supply can be increased but only by a small amount

The long-run period

All factors of production are fully flexible although the state of technology is fixed. Output can be significantly increased

Producer surplus

The difference between the amount that a seller receives for a product, and the price at which they would have been prepared to sell it

Why is the supply curve upward sloping?

The profit motive-When the price of a product rises, it becomes more profitable for businesses to increase their output as they can increase potential return

Production and costs/Law of diminishing returns- When a firm increases output, this tends to lead to an increase in their costs, so a higher price is needed to cover these extra costs. As variable f.o.p are added to fixed state of capital, marginal costs of production will rise so a higher price is needed to cover this

New suppliers/entrants into the market- Higher prices can incentivise other suppliers to enter, leading to an increased quantity supplied as more firms are willing and able to provide output

Determinants of supply

Productivity and costs of production

Raw material costs

Technology

Subsidies and taxation

Seasons/weather

Prices of related goods

Capacity expansion

Elasticity

Measures the responsiveness of the quantity demanded or supplied of a product to a small change in its price or other variables such as incomes.

Price elasticity of demand

Measures the responsiveness of quantity demanded relative to a change in the price of a good or service

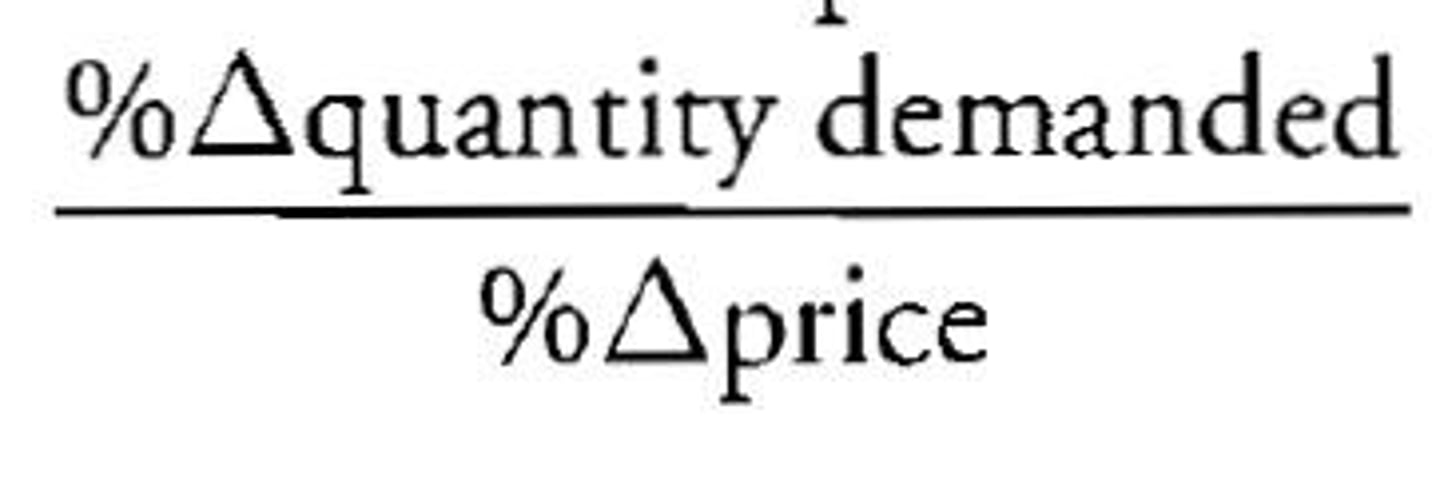

PED formula

PED Conditions

If...

PED=0 Perfectly price inelastic demand

0

PED=infinity Perfectly price elastic

[negate the negative sign]

Price elastic demand

Quantity demanded of a product is sensitive to a change in price e.g. luxuries, goods with many substitutes, goods that are bought frequently

Price inelastic demand

Quantity demanded of a product is insensitive to a change in price e.g. addictive goods, few substitutes, necessities, small % of income expenditure

Price unitary elastic demand

Where the percentage change in the quantity demanded of a product is equal to a change in price of the product

PED determinants

Habit forming goods

Proportion of income expenditure

Time period (SR=inelastic)

Availability and closeness of substitutes

Brand loyalty

Necessities

Durability

A04: Elasticity may change over time

Income elasticity of demand

A measure of the responsiveness of quantity demanded to a change in incomes

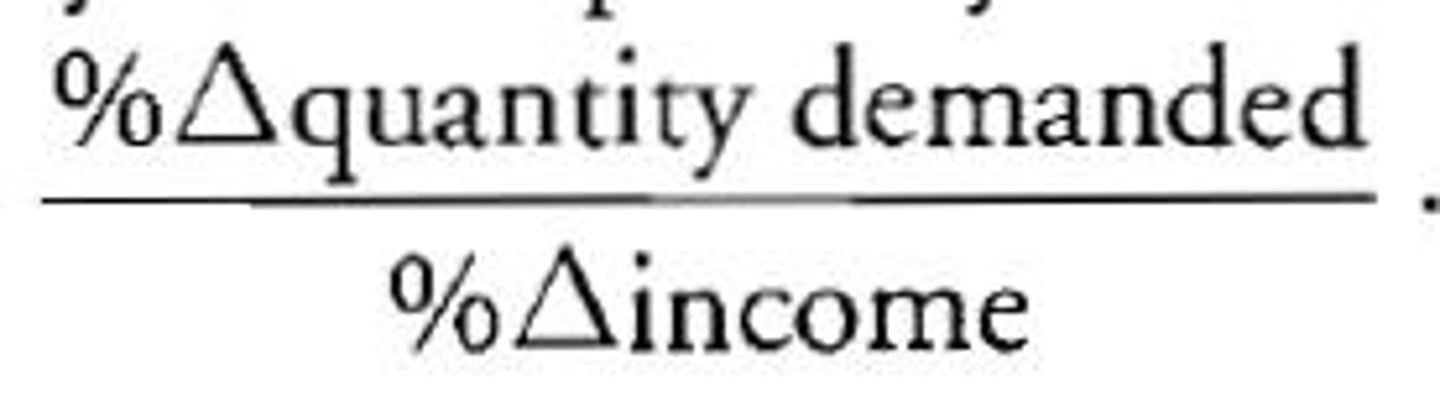

YED Formula

YED Conditions

If...

YED<1 Income inelastic demand

YED>1 Income elastic demand

YED=1 Income unitary elastic demand

Income inelastic demand

Goods for which a change in income produces a less than proportionate change in quantity demanded (YED<1) eg. necessities

Income elastic demand

Goods for which a change in income produces a greater than proportionate change in quantity demanded (YED>1) eg. Luxury goods

Normal goods

A good where the quantity demanded increases when income rises (YED>0)

Luxury good

A good where the quantity demanded increases by a proportionately greater amount than a rise in income (YED>1)

Necessity good

A good where the quantity demanded increases by a proportionately smaller amount than a rise in income (0

Inferior good

A good where the quantity demanded decreases as incomes rise (YED<0)

Cross price elasticity of demand

A measure of the responsiveness of quantity demanded for one product relative to a change in price of another product

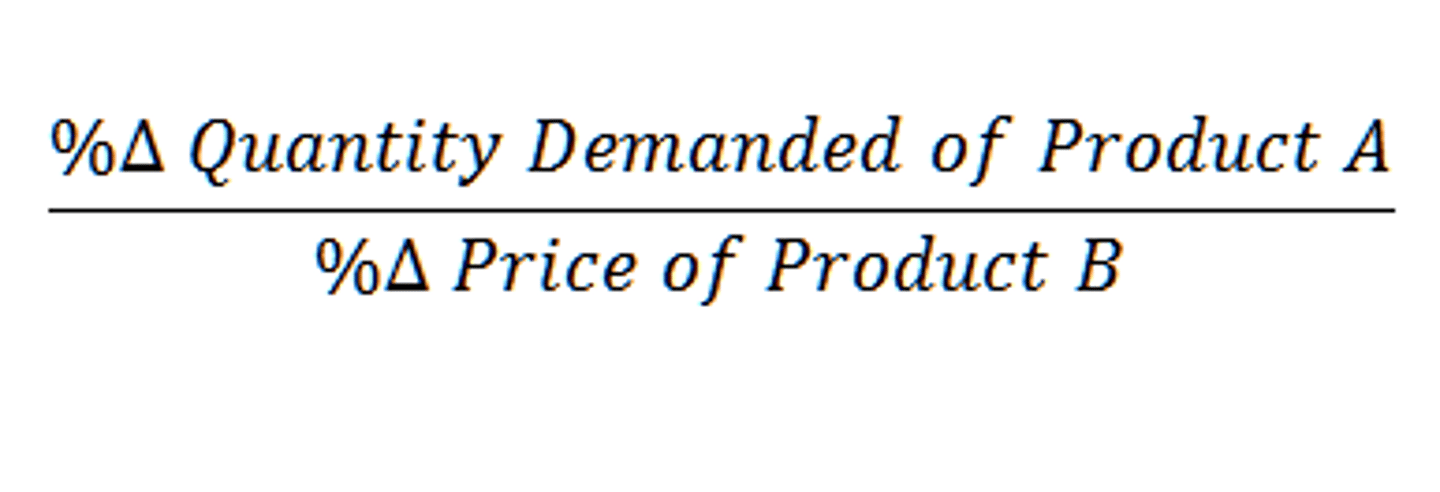

XED Formula

XED Conditions

If...

XPED=0 Goods are unrelated

XPED > 0 Substitutes

XPED < 0 Complements

XPED=infinity Perfect substitutes

XPED=neg. inf Perfect complements/must be bought together

Substitutes

Products that can be used for similar purposes, such that if the price of one product rises, demand for the other product is likely to rise

Complements

Products that tend to be consumed jointly, such that the price of one product rises, demand for the other product is likely to fall.