elasticity chp 5

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

40 Terms

elasticity

is a measure of the responsiveness of one variable to changes in another

price elasticity of demand formula

% change in quantity/ % change in price

price elasticity of demand

it is always a negative number, whihc is why we use the absolute value

a larger number (in absolute value) indicates greater elasticity

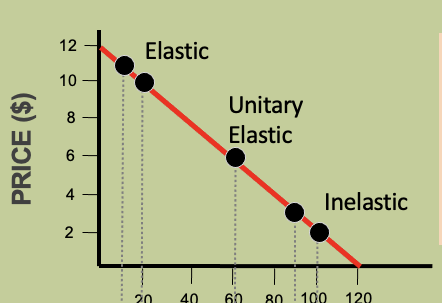

what is the categorizing price elasticity of demand

when it is less than 1= inelastic

when it is greater than 1= elastic

when it equals 1= unit elastic

consumers of goods with elastic demand are _____ to price changes

sensitive

consumers of goods with inelastic demand are ______ to price changes

less sensitive

how will a perfectly elastic graph look?

completely horizontal

how would a relatively elastic graph look like?

horizontal line but slightly slanted

how would a unit elastic graph look like?

looks similar to a U

how does a relatively elastic graph look like?

it is vertical and slightly slanted

how does a perfectly inelastic graph look like?

completely vertical

what are the 4 determinants of elasticity

availability of close substitutes

proportion of income spent on a product

luxuries versus necessities

time period

good with elastic demand have many substitutes, represent a large portion of one’s budget, tend to be luxuries, and have a long time horizon for decisions

whats the midpoint method?

when calculating percentage changes, the midpoint method results in the same number regardless of the direction of the change

whats the midpoint method formula

Q1-Q0/ (Q0+Q1)/2

how do you find the elasticity and total revenue

total revenue= price x quantity

elasticity and total revenue

when demand is inelastic, price changes are larger than quantity changes (in percentage terms)

an increase in price results in higher total revenue

a decrease in price results in lower total revenue

when demand is elastic, quantity changes are larger than price changes (in percentage terms)

an increase in price results in lower total revenue

a decrease in price results in higher total revenue

when demand is unit elastic, quantity changes are equal to price changes (in percentage terms)

an increase in price does not change total revenue

a decease in price does not change total revenue

when you move down a linear demand curve, what happens to elasticity?

it falls from elastic to inelastic

total revenue is _____ when demand is unit elastic

maximized

what are other elasticities of demand?

price, cross and income

cross elasticity of demand

measures how changes in the price of one good affect the demand for another good

cross elasticity of demand formula

% change Qb/ % change Pa

unlike for price elasticity, the sign (+ or -) matters

the sign determines whether goods are substitutes or complements

when the cross elasticity of demand is greater than 0, that means goods A and B are substitutes!!

when the cross elasticity of demand is less than 0, that means goods A and B are complements!!

ex: if the price of salads increases, demand for salad dressing decreases

income elasticity

measures how responsive quantity demanded is to changes in consumer income

income elasticity of demand

% change in quantity/ % change in income

the sign of the answer (+ or -) also matters

the sign determines whether goods are normal, luxury, or inferior with respect to income

normal goods

between 0 and 1

an income increases, consumers buy more normal goods.

as income decreases, consumers buy fewer normal goods

luxury goods

usually greater than 1

an increase increases, purchases of luxury goods increase by more than the change in income

inferior goods

usually goods less than 0

an income increases, consumers buy fewer inferior goods

as income decreases, consumers buy more inferior goods

price elasticity of supply

measure the responsiveness of quantity supplied to changes in price

elasticity of supply formula

% delta quantity supplied / % delta price

the answer is always a positive number because of the law of supply

elasticity of supply definition

increases over time as businesses adjust their production decisions

market period

output and the number of firms are fixed

short run

the number of firms does not change but each firm can adjust output

long run

firms can enter or exit the industry

elasticity of supply over time

supply becomes more elastic (flatter) over time, from the short run to the long run

incidence of a tax

describes who bears the economic burden of a tax

this is influenced by elasticity

3 types of taxes

progressive, flat and regressive

progressive tax

a tax in which those with higher income pay a higher average tax rate (ex: federal income tax)

flat tax

a tax that is a constant proportion of one’s income (ex: medicare tax)

regressive tax

a tax in which those with higher incomes pay a lower average tax rate