accounting LN 1: introduction and the accounting equation

1/114

Earn XP

Description and Tags

(as of feb 3)

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

115 Terms

The Accounting Equation:

A = L + SE

ASSETS = LIABILITIES + STOCKHOLDERS' EQUITY

Investing =

Financing (Creditor Financing + Owner Financing)

Economics Resources

= Claims against resources (nonworner claimes on assest + owner claims of assets)

Assest A are the resources that represent what?

PROBABLE future economic benefits

PROBABLE future economic benefits rules

can be measured with reasonable precision

the resources we obtained/controlled by the accounting entity from PAST transactions

benefits = future cash receipt or reduction of liabilities

what can the future economic benefits of assests be

future cash receipt or a reduction of liabilities

examples of asset accounts

Cash, Accounts Receivable (A/R), Inventory, Prepaid Expenses, PP&E

assets are classified into what two types

current and noncurrent assets

current assets

resources that will be converted to cash, consumed, or sold within one year of the

balance sheet date

how are current assets presented in the balance sheet

in order of liquidity

examples of current assets

cash

marketable securities

accounts receivable

inventory

prepaid expenses

cash

and cash equivalents – currency, bank deposits, certificates of deposit

Marketable securities

short-term investments that can be quickly sold to raise cash

Accounts receivable

amounts due to the company from customers arising from the sale of products on credit. asset.

Inventory

goods purchased or produced for sale to customers

Prepaid expenses

costs paid in advance for rent, insurance, or other services

noncurrent assets

resources that will be converted to cash, consumed, or sold more than one year

from the balance sheet date.

examples of noncurrent assets

Property, plant and equipment (PP&E)

Intangible and other assets

Long-term investments

Property, plant and equipment (PP&E)

includes land, factory buildings, warehouses, office

buildings, machinery, office equipment, and other items used in the operations of the company

Intangible and other assets

patents, trademarks, franchise rights, goodwill, and other items that

provide future benefits, but do not possess physical substance

Long-term investments

investments in shares of other firms that management does not intend to sell

in the near future

liabilities are…

obligations to transfer assets or provide services that represent probable future

obligations:

rules of probable future obligations (in Liabilities)

the future sacrifice of benefits can be measured with reasonable precision

the obligations are a result of past transactions or events.

the obligations can be a future cash payment or an obligation to deliver goods or services.

examples of liability accounts

Accounts Payable, Interest/Wages/Notes Payable, Deferred/Unearned Revenue

what are liabilities classifed into

current and non-current liabilities

liabilities equation

L = CL + NCL

current liabilities

obligations that are due within one year of the balance sheet date (short-term

financing).

what are current liabilities listed in

in order of maturity

examples of current liabilities

accounts payable

accrued liabilities

short term borrowings

deferred rev

current maturities of long-term debt

accounts payable

amounts owed to suppliers for goods and services purchased on credit

Accrued liabilities

obligations for expenses that have been recorded but not yet paid

Short-term borrowings

short-term debt payable to banks or other creditors

Deferred (unearned) revenue

an obligation created when the company accepts payment in advance

for goods or services it will deliver in the future

Current maturities of long-term debt

the portion of long-term debt that is due to be paid within one

year

Noncurrent liabilities are also known as

long-term liabilities

Noncurrent liabilities

are obligations that are to be paid after one year of the

balance sheet date (long-term financing)

long-term financing

obligations that are to be paid after one year of the

balance sheet date

examples of noncurrent liabilities

Long-term debt – amounts borrowed from creditors that are scheduled to be repaid more than one year in the future

Other long-term liabilities – various obligations, such as warranty and deferred compensation liabilities, long-term tax liabilities

Equity reflects…

capital provided by the owners of the company

what remains of an entity after deducting the liabilities?

the residual interest

the residual interest

s the daily interest that accrues on a credit card balance between the end of a billing cycle (statement date) and the day your payment posts, appearing on your next statement even if you pay the current balance in full.

what is owners equity called for corporate entities

stockholder’s equity (SE) or shareholders’ equity.

SE equation

SE = Contributed Capital + Earned Capital

Contributed capital

represents stockholders’ investment s and consists of the following accounts:

Common stock

Additional paid-in capital

Treasury stock

common stock

- the capital received from the primary owners of the company

additional paid-in capital

- amounts received from the primary owners in addition to the par value or stated value of the common stock

treasury stock

- the amount paid for common stock that the company has reacquired

earned capital

the cumulative net income (or losses) after deducting dividends paid to shareholders

retained earnings

the accumulated earnings that have not been distributed to stockholders as

dividends

Accumulated other comprehensive income or loss (AOCI)

accumulated changes in equity that are not reported in the income statement.

Revenues (R) represent what?

increases in net assets (assets minus liabilities) that are caused by the company’s

transferring goods and services to customers.

expenses represent what?

decreases in net assets that are caused by the company’s revenue-generating

activities.

typical expenses

Cost of goods sold (COGS): the cost of products that are delivered to customers during the accounting period.

Operating expenses: Depreciation expense, wages expense, selling, general, and administrative expenses (SG&A)

Non-operating expenses: Interest expense

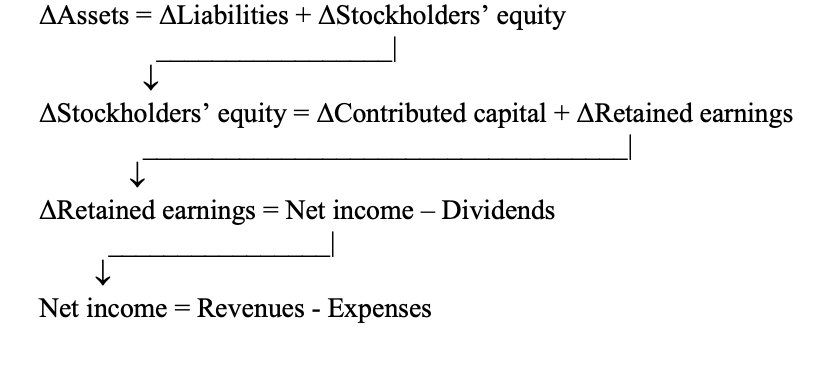

Net Income equation

NI = REV - EXPENSES

The relation between B/S and I/S via the accounting equation

when are balance sheets prepped

at a certain point in time

liquidity

the ease of converting non cash assets to cash

what are the most liquid assets

current assets

historical cost

original acquisition cost - physical assets are reported as this in the balance sheet

reliability

the use of historical cost to report asset value - has the advantage of reliability

executory contract

when conditions 1 and 2 of liabilities r met but the transaction that caused the obligation has not occured → liability is not recorded

what is special about grocery stores

few current assets but LARGE operating cash flow → good liquidity → even though it has ratios less than 1

GAAP

Generally Accepted Accounting Principals conventions, rules, guidelines etc that govern financial reporting

Constantly changing

Rule-based

SEC

Securities and Exchange Commission

Entity that sets all the rules/standards for financial reporting

FASB

Financial Accounting Standards board

who has power over FASB

the SEC

what is the single source of the US GAAP

The FASB Accounting Standard Codification

IASB

International Accounting Standards Board

is the IASB private or public, and what does it develop?

Private sector

Develops the IFRS (International Finance Reporting Standards)

difference between IASB and GAAP

Principle based (not rule based like GAAP)

Sarbanes-Oxley Act (SOX)

US federal law in response to corporate and accounting scandals bug businesses

Very government involved in businesses (biggest move since FDR)

what did the Sarbanes-Oxley Act (SOX) establish

Established Public Company Accounting Oversight Board (PCAOB) -

PCAOB purpose

overseeing everything that accounting firms do and their role as auditors

Section 404 of SOX

Requires annual assessment of internal controls and procedures for financial reporting by management

The external auditor is required to examine and report on the management's assessment of internal controls and effectiveness

FOR RELIABILITY AND TRUSTWORTHINESS

10-K

ANNUAL REPORT

Issued every year by management

Purpose: to update shareholders/interest parties of the company

elements of 10 K

MD&A, Financial Statements, Footnotes, Independent Auditor reporst

MD&A

summarizing activities of the current and past years + assessment of the future

financial statements

balance sheet, income statement, statement of shareholders equity, statement of cash flows

footnotes

summary of accounting policies/schedules of financial statements/commitments/disclosures, etc.

Independent Auditor repost prupose

Done by independent CPA

Attest fairness of all financial statements

Most opinions are unqualified

10-Q

quarterly report, same thing as 10-K but for the quarters

Things filed wit SEC

10-k, 10-Q, 8-K, Registration statement, proxy statement

8-K

filed whenever an event that is deemed material (change of auditor) occurs

Registration statement/prospectus:

documents that must accompany a new issue of securities that potential investors may find relevant

Securities

tradeable financial instruments

Proxy Statement:

information on directors compensation - provided to shareholders before voting on corporate matters

GAAS

auditing standards

PCAOB makes what

all the standards all the auditors should follow

first thing to do when starting your own business

raise cpaital

who ways to raise capital

Equity (owner financing) = raising cash from selling stocks

Creditor (non-owner financing) = like a bank loan

fancy name for raising capital

FINANCING ACTIVITIES

Equity (owner financing)

raising cash from selling stocks

No obligation for the owners/company to pay people back when someone buys the stock. You can just resell the stock

Creditor (non-owner financing)

The creditor is not the owner of the company because the company has an obligation to pay the buyer back

Liabilities are present here

Second thing to do once you get money for your business

acquire resources needed to produce and sell products and services

Investing activities

acquiring resources need to produce and sell products and services (assests)

Assets

everything that you buy in your investing activities. Resources providing future benefits to the company

Accounting Equation or B/S Equation, and what does it show?

Assets = Liabilities (the amount of capital you get from banks) + Equity (the capital you get from buyers of stocks)

Shows where the money comes from and where a company spends the money

balance sheet breaks down the WHAT of a company

breakdown of assets, liabilities and equity. All about the accounting equation.

Third thing to do (after you have assets) for your business

start operation

Operating Activities

production, promotion and selling products and services