Economics Mock Exam March 2026

1/124

Earn XP

Description and Tags

Paper 2; ALL CONTENT (EXCLUDING HL)

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

125 Terms

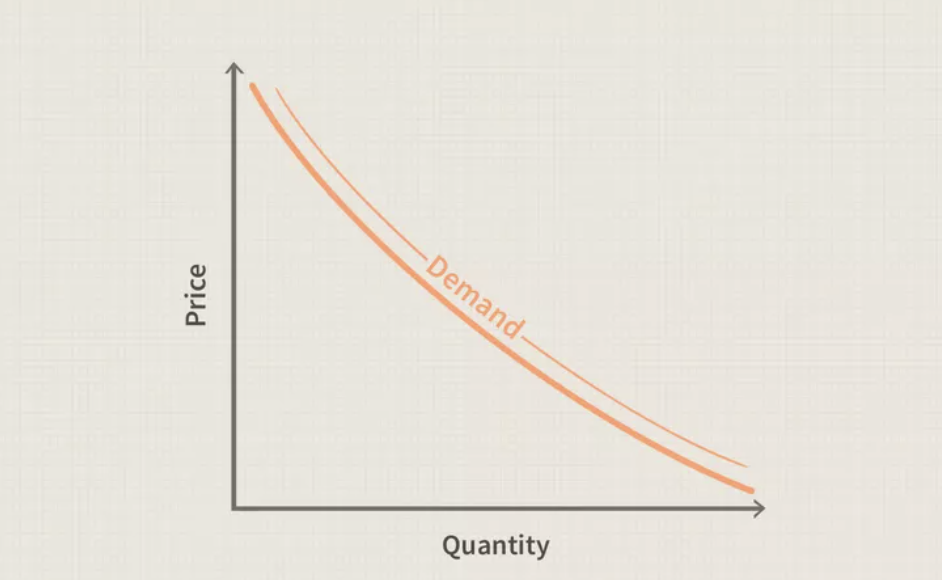

Law of demand

As price of product goes down, quantity demanded increases, ceteris paribus

Non-price determinants of demand (shift in demand)

Income (normal/inferior goods)

Price of related goods (substitutes/complements/unrelated goods)

Taste and preferences

Future price expectations

Number of consumers

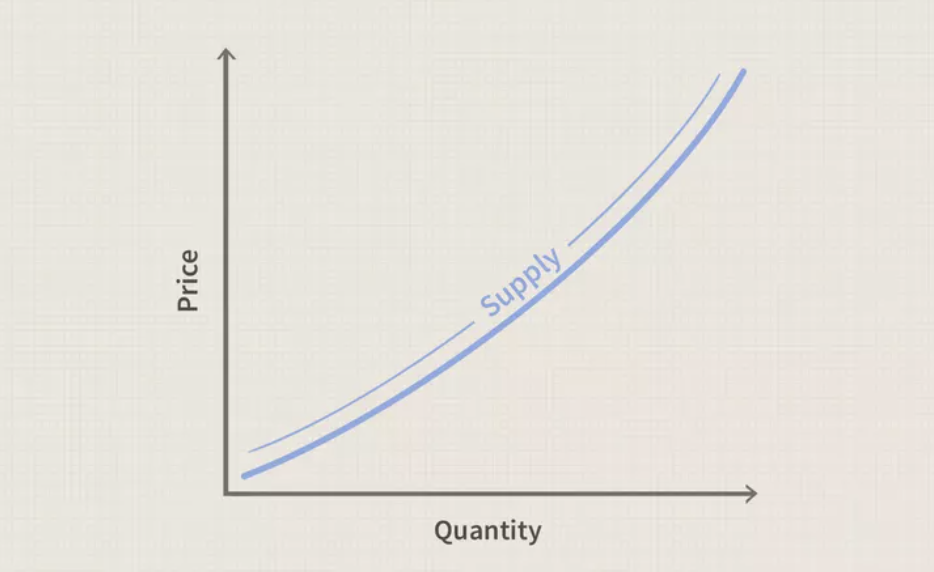

Law of supply

As price of product rises, the quantity supplied increases, ceteris paribus

Non-price determinants of supply

Costs of factors of production

Price of related goods (joint/competitive supply)

Government intervention (indirect taxes/subsidies)

Expectations on future prices

Changes in technology

Weather/natural disasters

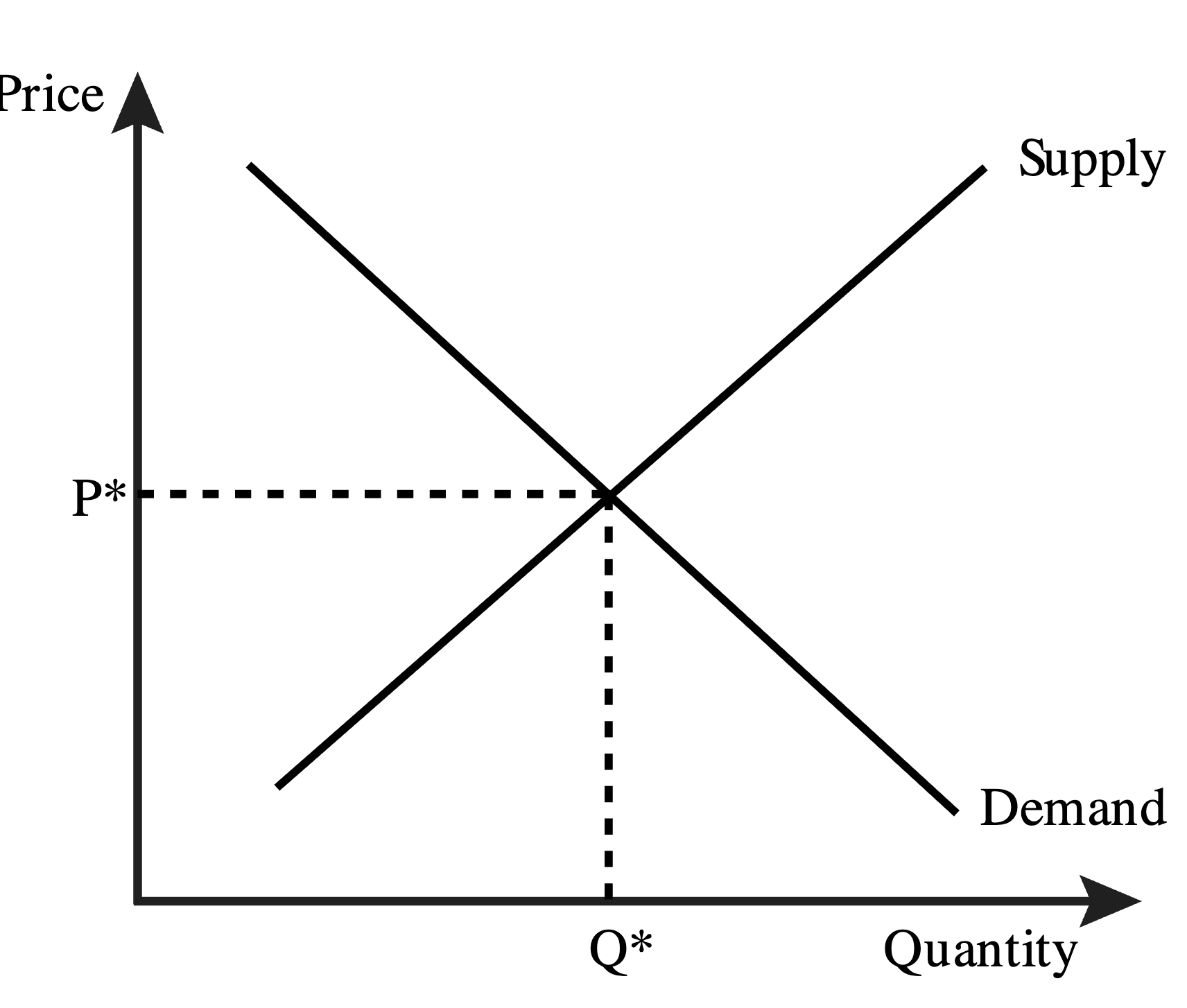

Market equilibirum

Point where supply meets demand, so both buyers/sellers are satisfied with the price and quantity in the market (profits and utility are maximized at market clearing price)

Allocative efficiency

Resources were used to productively meet societies’ wishes

Signalling function

Type of price mechanism to signal information to consumers and producers (set by actions in the market, reflecting of change)

Rationing function

Type of price mechanism to ration scarce resources by price

Incentive function

Type of price mechanism to incentivize producers and consumers to either increase prices, buy more, or by less (which lowers price)

Price elasticity of demand

Extent to which demand for a good or service will be affected as a result of change of one its price

PED formula

Change in demand / change in price

(New - old / old) / (New - old / old)

If price is elastic, total revenue…

Increases as price decreases, or decreases as price increases, demand is changed

If price is inelastic, total revenue…

Increases as price increases, or decreases as price decreases, demand is unchanged

Determinants of PED

Availability of substitutes

Necessity of a product

How widely the product is defined (iPhones vs smartphones as a whole)

Proportion of income spent

Time period considered

Importance of PED for government decision-making

Provides a view to determine taxing and subsidies

Example: Government placing tax on fuel, allowing firms to raise price without major changes in demand as it is inelastic

Income elasticity of demand

Measure of how much the demand for a product changes when there’s a change in consumer income

YED formula

Change in demand / change in income

(New - old / old) / (New - old / old)

If YED is positive, the good is...

A normal good (inelastic)

If YED is negative, the good is…

An inferior good (elastic)

If YED is between 0-1, the good is…

A necessary good (elastic)

If YED > 1, the good is…

A luxury good (elastic)

Price elasticity of supply

The extent to which quantity supplied is impacted by variations in price

PES formula

Change in supply / change in price

(New - old / old) / (New - old / old)

Determinants of PES

How much costs rise as output rises (unused capacity/mobility of factors)

Time period considered (immediate/short/long-term)

Ability to store stock

Why governments intervene markets in the first place

Have the ability to support households, firms, influence consumption, production, protect consumers from monopolistic issues, promote well-being, earn revenue, etc.

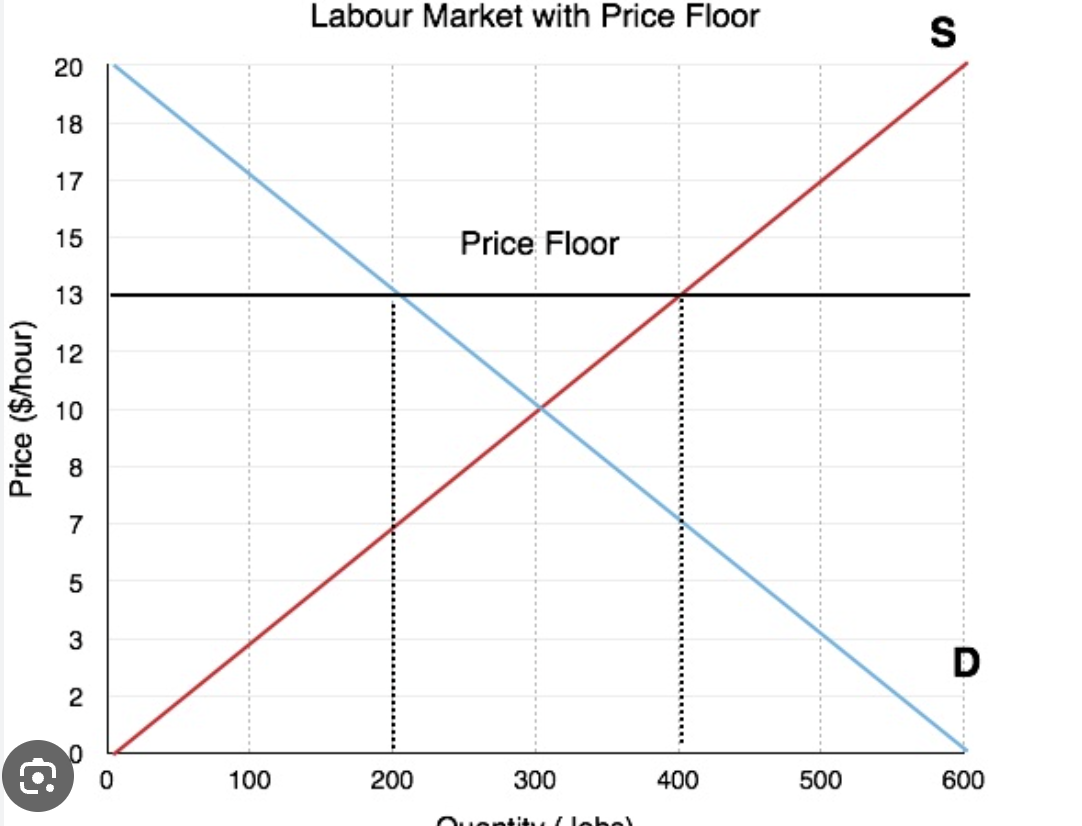

Price floors

Government intervenes by setting a minimum price that prevents producers from reduce price (price is set above equilibrium), to raise income for producers, protect workers, which leads to excess supply

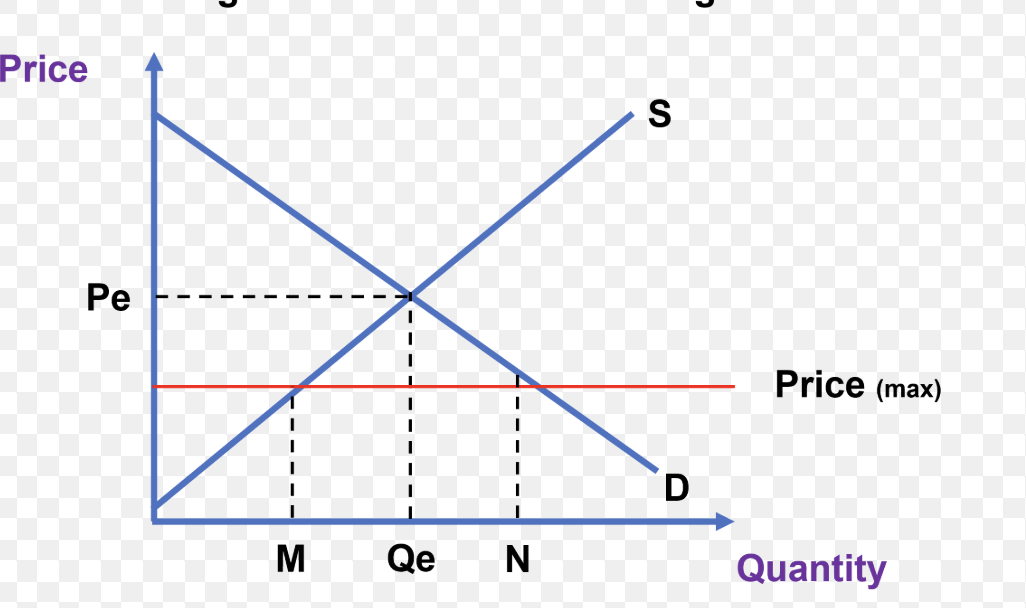

Price ceilings

Government intervenes by setting a maximum price that prevents producers from raising price above equilibrium (price is set below equilibirum), to help consumers in markets of necessity goods, ensuring affordability, which leads to excess demand

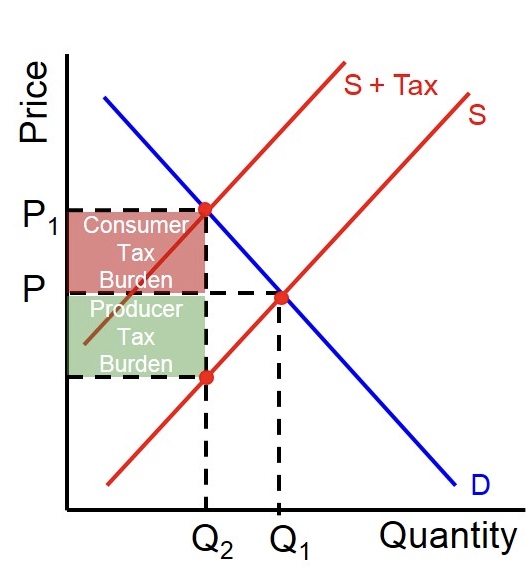

Indirect taxes

Tax imposed by the government on producers for goods and services (e.g., VAT, excise duties), increasing costs and shifting supply left, reduces consumption and raises revenue

Subsidies

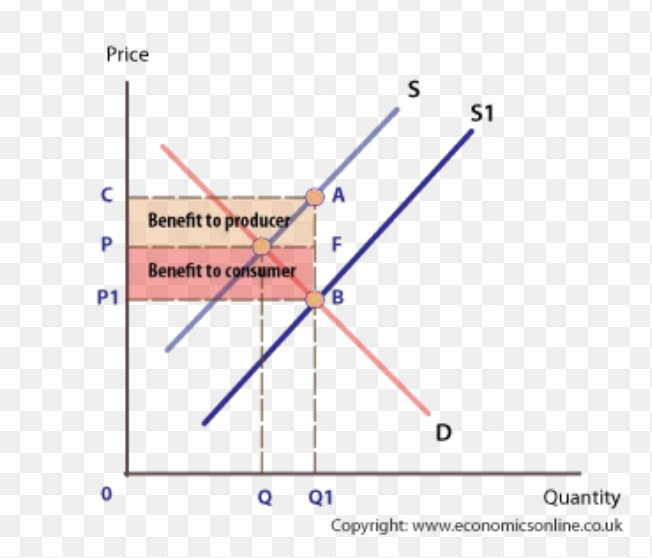

Government payment to producers to lower production costs, shifting supply right to increase output and lower prices

Tax burden diagram

Where consumer + producer burden = government revenue

Subsidy burden diagram

Where benefit to consumer + benefit to producer = government loss

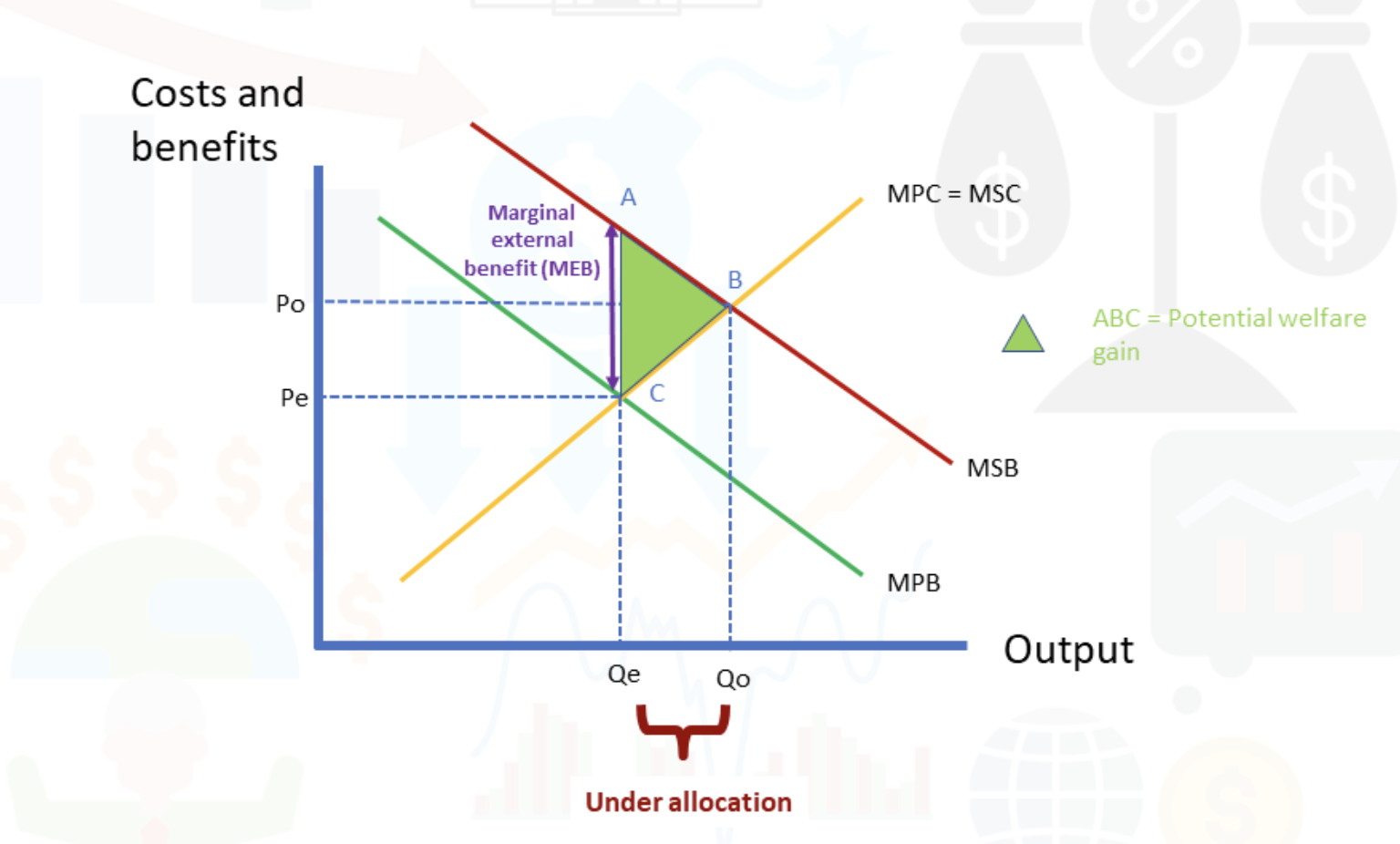

Positive externalities of consumption

When an individual's consumption of a good or service provides an unintended benefit to a third party (society)

Positive externalities of production

When the production of a good or service creates benefits for third parties not involved in the market transaction

Negative externalities of consumption

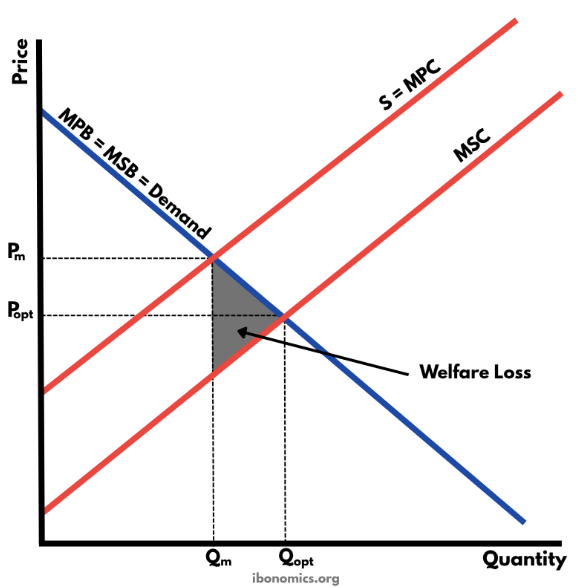

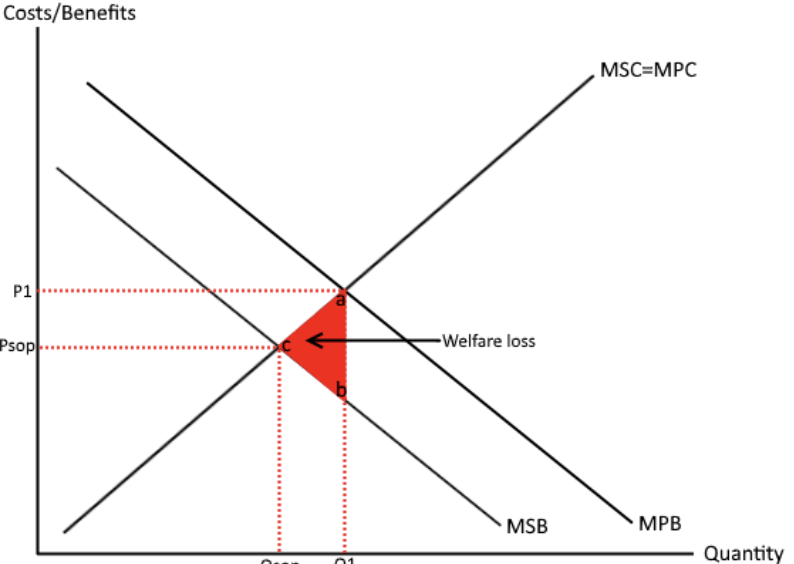

When an individual's consumption of a good or service imposes external costs on third parties, resulting in market failure where the MPB > MSB

Negative externalities of production

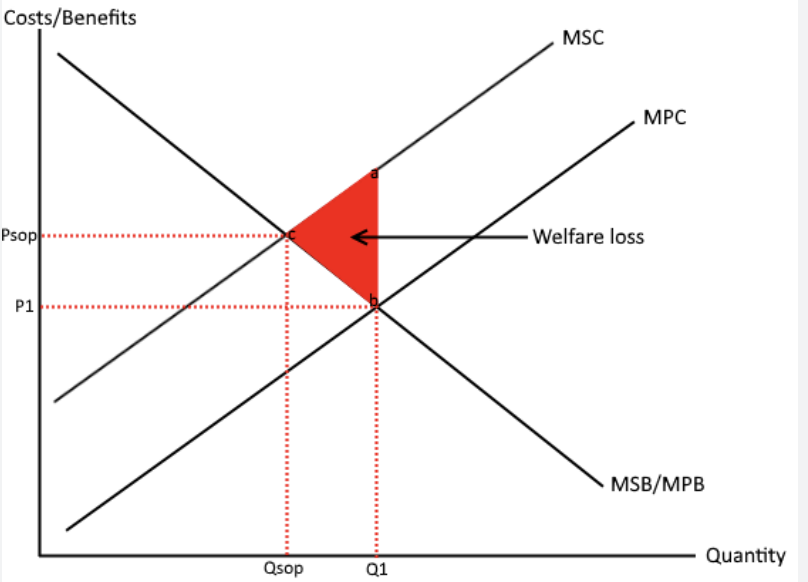

Costs imposed on third parties (society, environment) arising from the production of a good, which are not reflected in the market price, when MSC > MPC

Merit goods

Goods that are beneficial to consumer but people may not consume enough because they ignore the potential benefits (imperfect information), where demand of it is lower than it should be (like vaccines, university, sports, etc.)

Demerit goods

Products or services such as tobacco, alcohol, and junk food, that are harmful to consumers and society, resulting in overconsumption and market failure, and a negative externality of consumption

Common pool resources

Natural resources that are difficult to exclude people from (fishing grounds, forests, etc.,), which are rivalrous and result in the tragedy of the commons and negative externalities

International agreements on negative externalities and common pool threats

Intended agreements that are legally binding with the primary purpose of preventing the abuse of human impact on natural resources

Ex. UN Framework Convention Paris Agreement

Tradable permits

Market-based approach which limits access to a resource, where the permission can be traded around, which allows incentive to adopt cleaner technology and sustainable action-making

Carbon tax

Tax imposed when fossil fuels are burned, eliminating the negative externality (Pigouvian tax), to incentivize reduction of electric consumption, and carbon emissions, generating government revenue

Subsidies reducing negative externalities and threats to common pool resources

Governments allocating funds to reduce costs to producers to make energies that are sustainable more affordable, with cooperation needed

Improving positive externally knowledge on explaining benefits

Using advertising public campaigns to mitigate the imperfect information that consumers may have, shifting MPB curve to MSB curve

Legislation on achieving potential welfare gain

Passing laws to insist certain actions of positive externalities (like requiring vaccinations), but could be seen as infringing

Public goods

Goods not to be provided in a free market (national defense, flood barriers, streetlights, etc.,), which are non-excludable, non rivalrous, but causes the “free-rider problem”, direct provision may be needed (using tax payers money), or private partnership

National income

Total value of all final goods and services produced by a country's factors of production, or the total income earned by residents, within a specific period (usually a year)

GDP (Gross Domestic Product)

Total value of final goods/services produced in a national (domestic) economy

GNI (Gross National Income)

Total income earned by a country’s factors of production regardless of where assets are located

(Nominal) GDP formula

C + I + G + (X - M)

Where…

C = Consumption

I = Investment

G = Government Spending

X = Exports

M = Imports

Real GDP/GNI

When the GDP/GNI have been adjusted for inflation

Real GDP formula

(Nominal GDP / GDP deflator) x 100

GDP Deflator formula

(Real GDP / Nominal GDP) x 100

OECD Better Life Index

Measure of economic well-being that promotes policies to improve socio-economic well-being including 35+ countries and key members, allowing for comparison of well-being across countries based on 11 essential topics (material living, quality of life)

Happiness Index

Measure of economic well-being put by the UN sustainable development solutions to rank happiness levels and immigration, drawn from polls

Happy Planet Index (HPI)

Measure of economic well-being that measures sustainable well-being taking account of sustainability

GDP/GNI per capita formula

total GDP/GNI / size of population

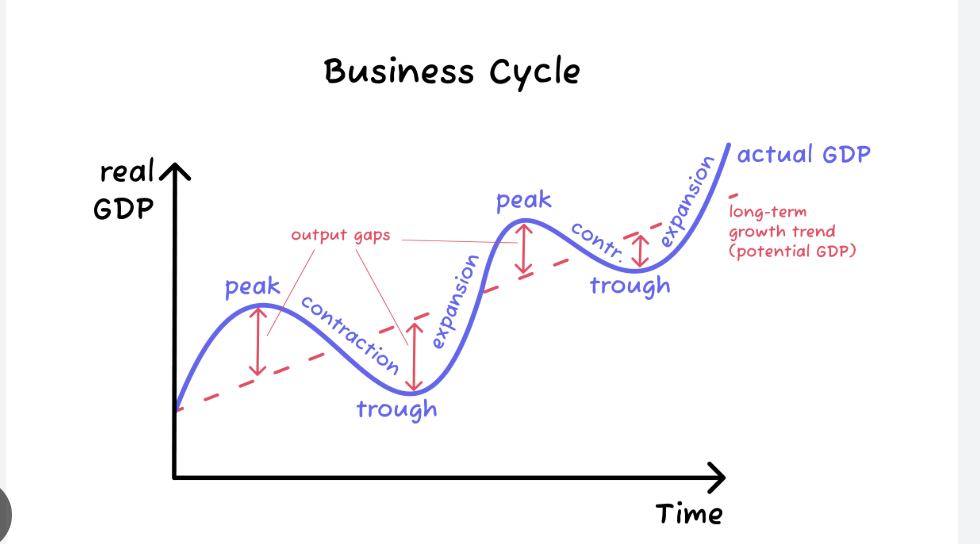

Business cycle + phases

Graph that shows periods of growth and slow/falling growth of GDP/output over time

Phases: boom, recession, trough, recovery

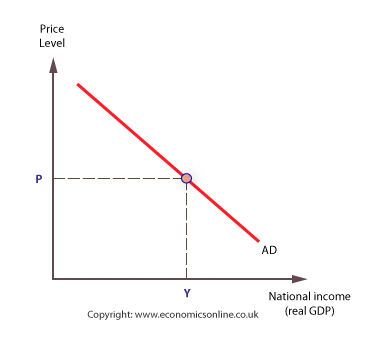

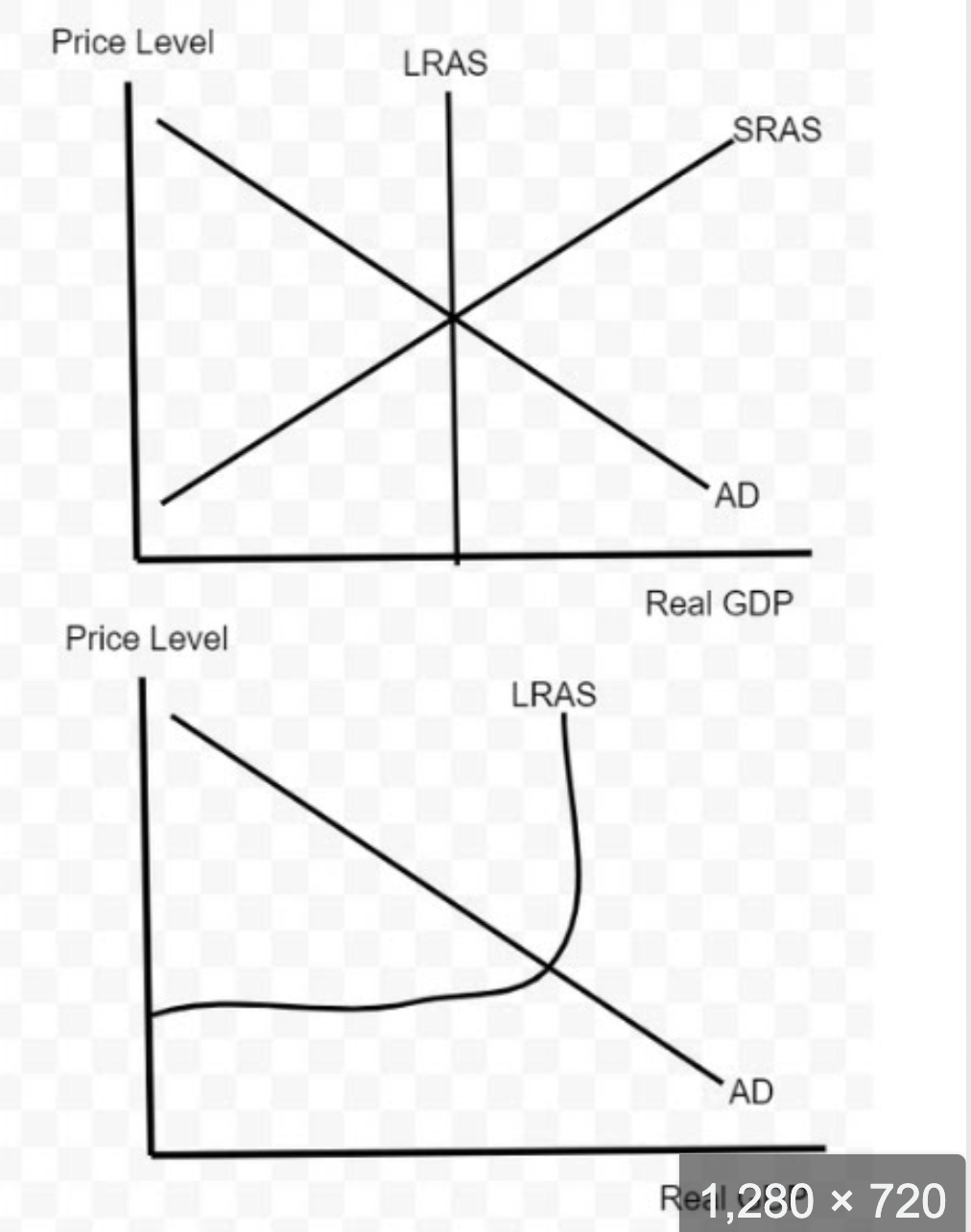

Aggregate demand

Total spendings on goods and services in a period of time at a given price level

Graph shows relationship between average price level and real output

Determinants of aggregate demand

Consumption (spendings on goods/services domestically)

Can change due to income taxes, interest rates, wealth, expectations/confidence, debtness

Investment (additional capital to economy)

Can change due to interest rates, business taxes, tech changes, expectations/confidence, debtness

Government spending (on health, edu, law, etc.)

Can change due to political/economic priorities

Net exports

+ net = trade surplus —> shift right

- net = trade deficit —> shift left

Can change due to export levels or import levels

Aggregate supply

Total amount of goods/services that all industries produce at every given price level

—> sum of supply curves in ALL industries in the economy

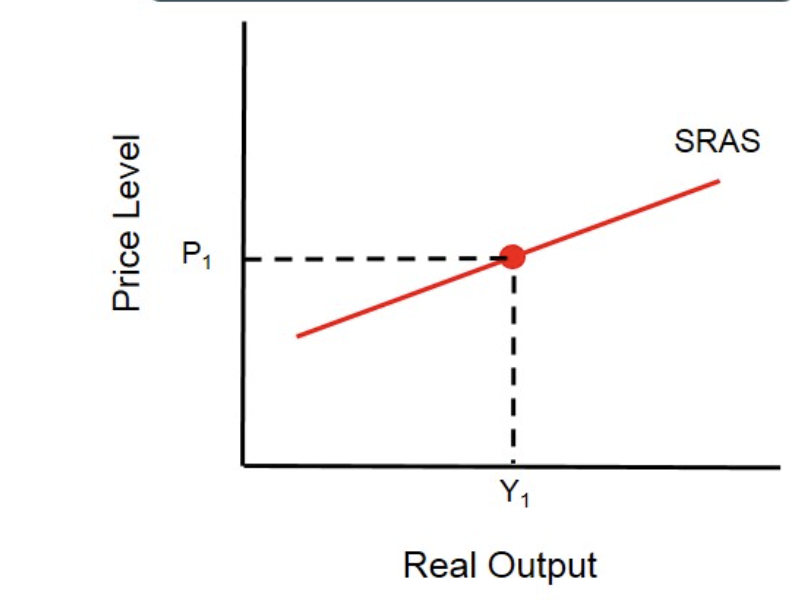

Short-run AS

Positive relationship between price level and amount of output that a country’s industry may supply

Factors of production don’t change

Price of labour is fixed

Larger level of output = higher average costs of production

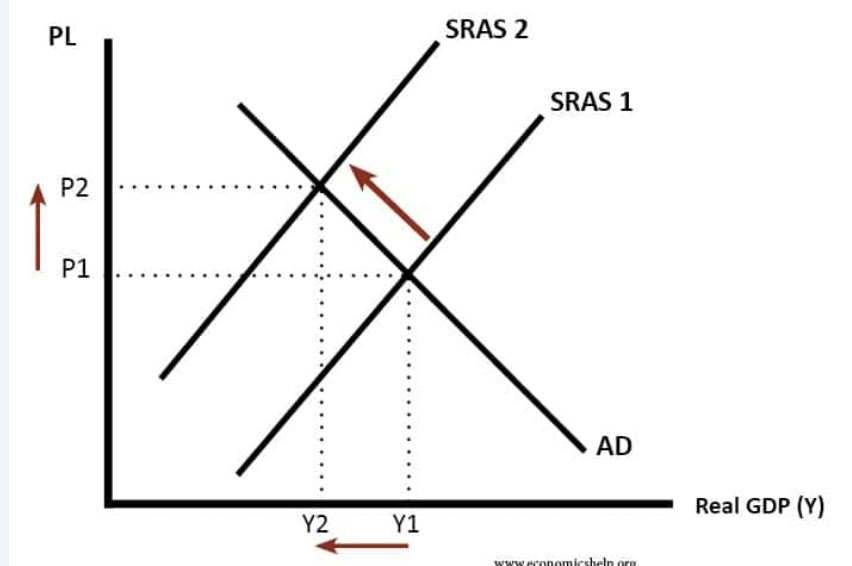

Determinants of SRAS (supply-side shocks)

Change in costs of production

Wage rates, raw materials, imports, taxes/subsidies

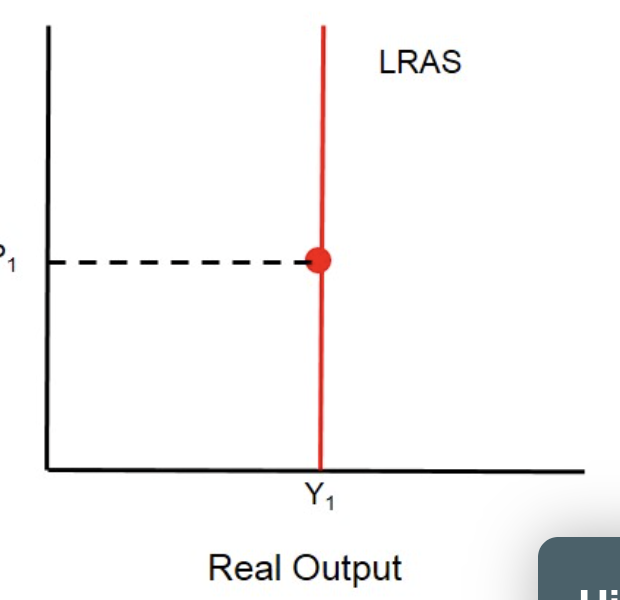

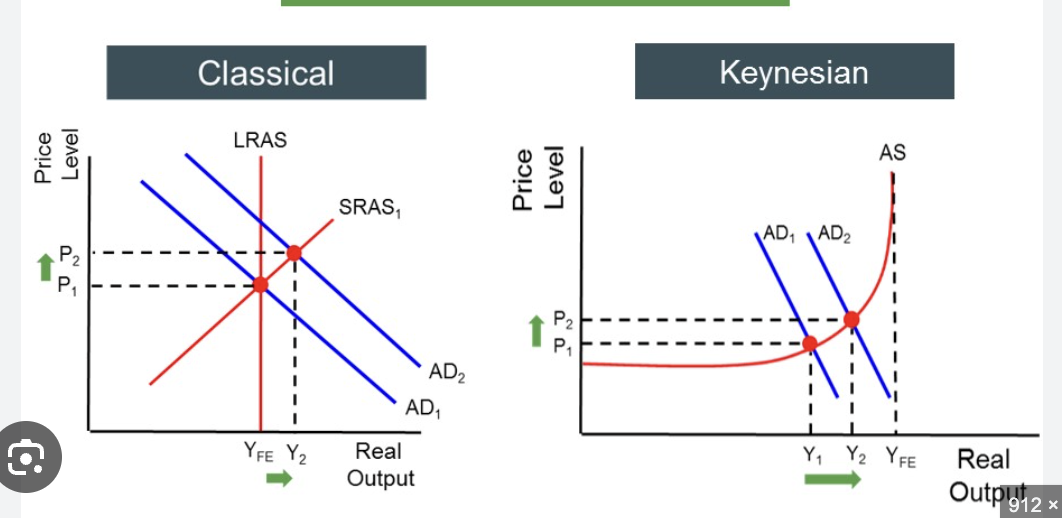

Neo classical Long-run AS

Curve viewed as perfectly inelastic/vertical, known as “full employment level of output” —> where output is at FULL CAPACITY, also assumes that potential output is based entirely on quantity/quality of factors of production

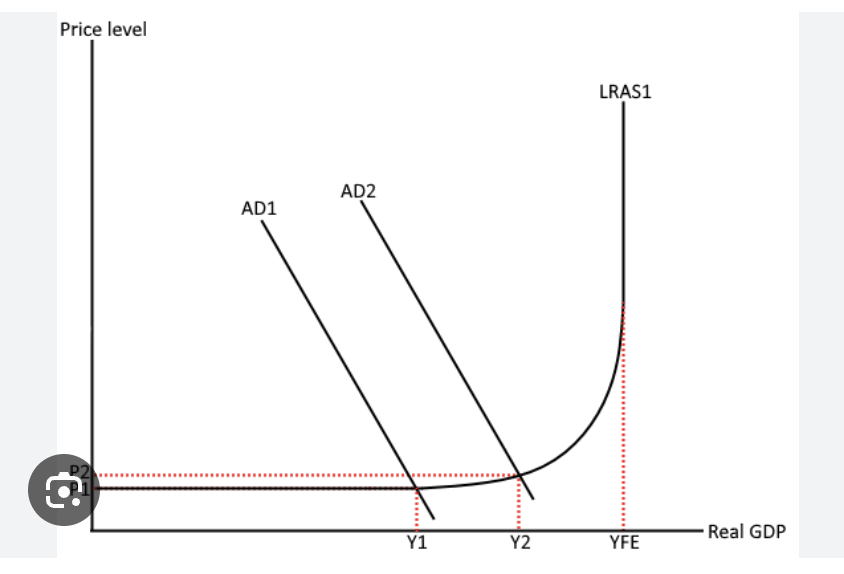

Keynesian AS

Shows 3 possible phases and doesn’t distinguish between short/long-run

Phase 1: Perfectly elastic at low levels of economic activity, producers raise levels without having larger costs due to SPARE CAPACITY

Phase 2: Spare capacity used up, factors are scarce, price will rise for higher costs

Phase 3: Impossible to increase output further, perfectly inelastic

Determinants of Keynesian/Neoclassical AS curves

Will shift as country’s factors of production change

Tech changes (land), birth rate (labour), investment (capital)

Supply-side policies (interventionist or market-based)

Macroeconomic equilibrium

Point where AD=AS, national income = level of output a country produces, short and long-run are existent

Short-run: Output produced = total demand, no reason for prods to change output, no up/down pressure

Neo Long-run: Economy always move at full employement level of output, impact of AD —> price levels

Keynesian Long-run: Occurs at different levels/phases

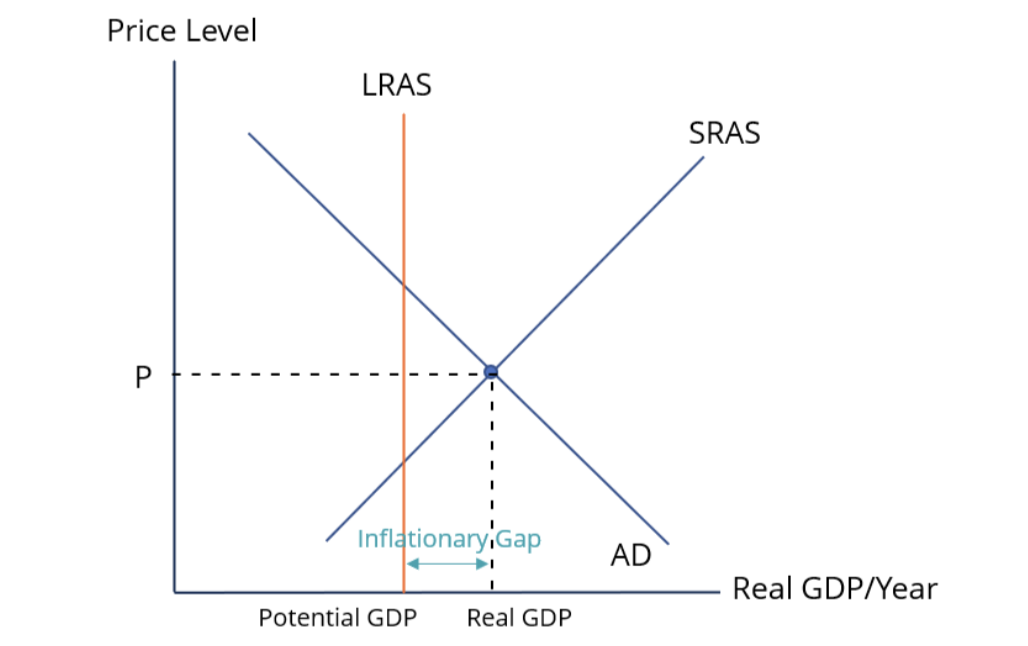

Inflationary gap

Economy is at equilibrium at a level of output > than full employment level of output, increases scarce + labour capital

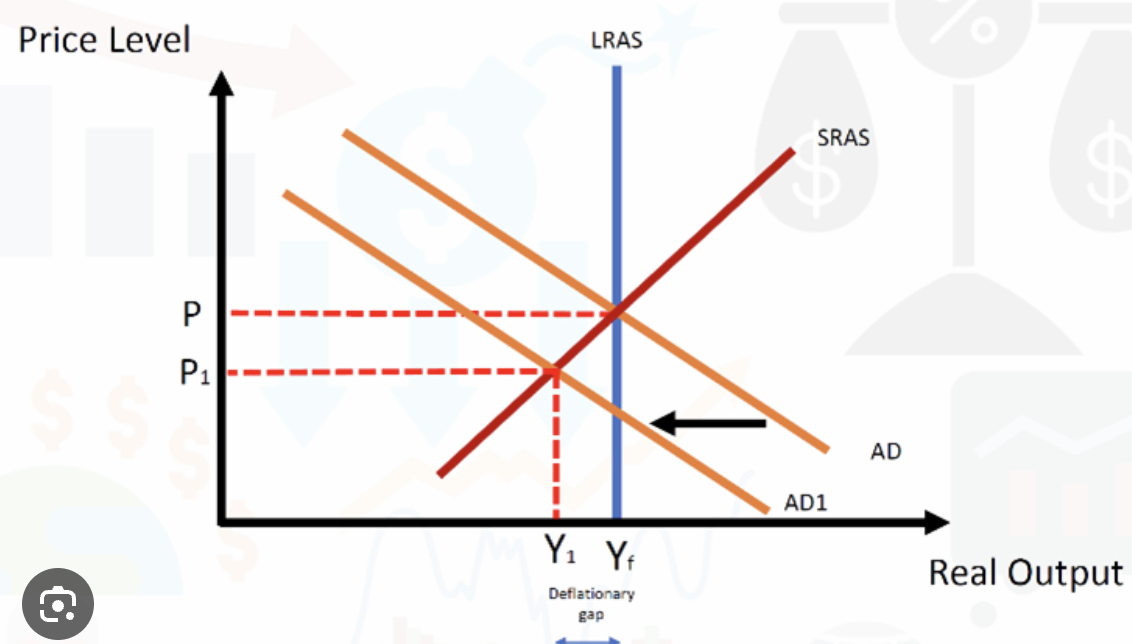

Deflationary gap

AD decrease where economy is at equilibrium but output level is < full employment level of output, so factors of production may have fallen and SRAS shifts right, government intervention is not present

Macroeconomic objectives

Low unemployment, low/stable rate of inflation (price stability), economic growth, income distribution, national debt

Unemployement

People of working age without work available and actively seeking employment

Unemployment rate

Number of unemployed / Total labour force x 100

Why is it difficult to measure unemployement?

Geographical disparities create variety among regions (urban v rural)

Age disparities

Ethnic differences create suffering due to prejudice/opportunity

Gender disparities where lack of education and discrimination causes inequality

Costs of unemployement

Less income

Lower standards in living

Higher levels of abnormal mental health

More poverty, homelessness, higher rates of crime, gang activity

Actual output less than potential

Government spends more on solving social issues stemmed from unemployment

Types of unemployement

Cyclical: related to business cycle —> firms need less labour at certain phases

Structural: worst type, related to fall in demand for labour, or difficulty to change jobs (skills needed), or change in framework of economy

Frictional: short-term, in-between jobs or left education to find one, not negative, reduced through market-based solutions

Seasonal: unemployed on a seasonal basis (tourism, agriculture, etc)

Inflation

Persistent increase in the average price level in the economy, measured through Consumer Price Index (CPI), on everything

Costs of high inflation

Loss of purchasing power for consumers

Real interest rates will be negative, so savings aren’t worth as much

Economic growth decreases due to less investment from consumers

Nominal interest rates increase to mitigate

More competitive internationally in trading (imports attractive)

Uncertainty in investments

Wages low so labour unrest + dispute

Consumer price index (CPI)

Measures the average percentage change over time in the prices paid by consumers for a representative "basket" of goods and services, primary indicator of inflation (rising cost of living) or deflation (falling prices)

Limitations of CPI

Not applicable to ALL people

Errors in data collection

Not taking account of changes

Countries differing in measurements

Prices vary for non-sustained reasons (seasons)

Changes in consumer prices

Cost-push inflation

Occurs when there’s an increase in costs of production, so short-run AS falls short, can change costs of domestic raw materials, increase imported capital costs, lowers exchange rate, increases costs of labour

Demand-pull inflation

Occurs when there’s an increase in AD, pulling up price levels, due to change of components

Deflation

Persistent fall in the average price levels of the economy (good and bad),caused by either a significant drop in Aggregate Demand (AD) or a substantial increase in Aggregate Supply (AS)

Costs of deflation

Unemployment (low AD makes businesses lay off workers)

Decreased consumption of durable goods to wait for further drops, can lead to a deflationary spiral

Fall in consumer confidence lowering AD

Investment decrease and makes less profit for businesses

Increase in debt for those taking loans or mortgage

Monetary policies ineffective to increase AD

Growth rate formula

(Real GDP in year 2 - Real GDP in year 1) / (Real GDP in year 1) x 100

Economic inequality

Unequal outcomes where treatment isn’t same for everyone —> inequality in income and wealth

Lorenz curve

Way in which income inequality is measured, divided into quintiles, useful to compare countries/distribution, modeled from GINI index, cumulative

Gini coefficient = A + (A+B)

How to calculate cumulative share of income for graphing Lorenz curve

Add through each quintile

1st, 1st + 2nd, 1st + 2nd + 3rd, etc.

5th = richest income

Gini coefficient

Numerical measure of income or wealth inequality within a population, ranging from 0 (perfect equality) to 1 (perfect inequality

Higher = more unequal distribution of income

Absolute poverty

Occurs when income of a person/household isn’t enough to meet basic needs (food, shelter, education, health, etc.), making under International Poverty Line (set by World Bank)

Purchasing power parity (PPP exchange rates)

Relative poverty

Based on living standards in a particular country

How is poverty measured?

Using World Banks International Poverty Line

Nations set own poverty line

Using OECD to provide poverty rate, or percentages below poverty line

Market-based measure —> basket of goods and services needed (setting the poverty line)

Multidimensional Poverty Index (MPI)

Developed by UN to recognize those in poverty and it’s a composite indicator to measure dimensions of poverty (health, education, standard of living)

Considered poor if experienced less in 1/3 of weighted indicator

Difficulty in measuring poverty

Many types, so varies and difficult to measure and define

Elements are impossible to measure (fear, vulnerability)

Surveys may be limited in poorer countries

Government lack of interest/efforts

Causes of inequality and poverty

Inequality of opportunities (different conditions, opportunity potentials vary, ex. poor household = less opportunities)

Discrimination (due to race, ethnicity, age, religion)

Discrimination in human capital (supply/demand for type of labour, wanting skilled people)

Different levels of ownership of resources, like capital

Globalization of tech process (leading to labour differences, hollowing out middle class)

Market-based supply-side policies (deregulation in financial market increases opportunity for wealthy)

Consequences of inequality and poverty

Pro: more incentive for entrepreneurship and innovation for investment

Con: drives productivity levels down, bringing less economic growth

Leads to low living standards and social tensions with less privilege —> also leads to promotion of criminal acts

Progressive taxes

Taxes that are based on income earned —> higher income = higher share of income, or corporate taxes

Pros: narrows gap, gov can use revenue for other finances

Cons: less incentive to work harder

Regressive taxes

Taxes that take a larger share of income from lower-income people than higher-income people

Ex. gas prices having different impact based on income (someone rich v someone poor)

Discourages consumption of negative externalities

Other domestic policies to reduce inequality/poverty

Transfer payments

Public health insurance

Programs to educate on childcare

Improved access to childcare

Diversity programs/regulation

Laws to encourage diversity

Equal wages

Minimum wages

Transfer payments

Tax revenues to redistribute income and provide different types of assistance to groups in the economy to improve living standards and opportunity

Childcare support

Paternity/maternity pensions/benefits

Depends on level to ensure what needs to be prioritized

Universal Basic Income (UBI)

Solution to benefits of unemployment being taken advantage of —> “free money for everyone”, giving everyone a guaranteed amount with no conditions, even to the rich

Fiscal policies (demand-management)

Set of government policies relating to expenditure/taxation rates, using expansionary to increase AD, or contractionary to decrease AD, aims to..

Maintain low/stable rate of inflation

Low unemployment rate

Stable long-term economic growth

Reduce business cycle fluctuations

Equitable income

Balance between imports and export