Macroeconomics Exam One Study Set

1/63

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

64 Terms

economics

the study of how society manages its scarce resources

what is scarcity?

idea that we have unlimited wants and limited resources

Two Branches of Econ

Mirco & Macro

Microeconomics

individuals making decisions

Macroeconomics

economy as a whole or group decision making

How many econ principles are there?

8 (well that we go over)

1. People face trade offs

since every resource is scarce and not enough time

2. Cost of something is what you give up to get it

Opportunity cost: the value of the best alternative that you give up when you make a choice

3. Rational people think at the margin

A rational decision-maker takes action if and only if the marginal benefit of the action exceeds the marginal cost.

4. People respond to incentives

Behavior changes when costs or benefits change. (attendance policy)

5. Trade can make people better off

people specialize in different goods and services meaning that someone can make it possibly quicker and more efficiently so it makes more sense to trade something the other person may be able to do better

6. Markets are usually a good way to organize economic activity

under markets we have decisions to decide what to buy, what to sell, how much to sell for, etc.

7. Government can sometimes improve market outcomes

provide polices to provide stabilization

8. The 3 most important Marco variables are

GDP

Inflation

Unemployment

Father of Economics

Adam Smith

Model

Simplified version of the world

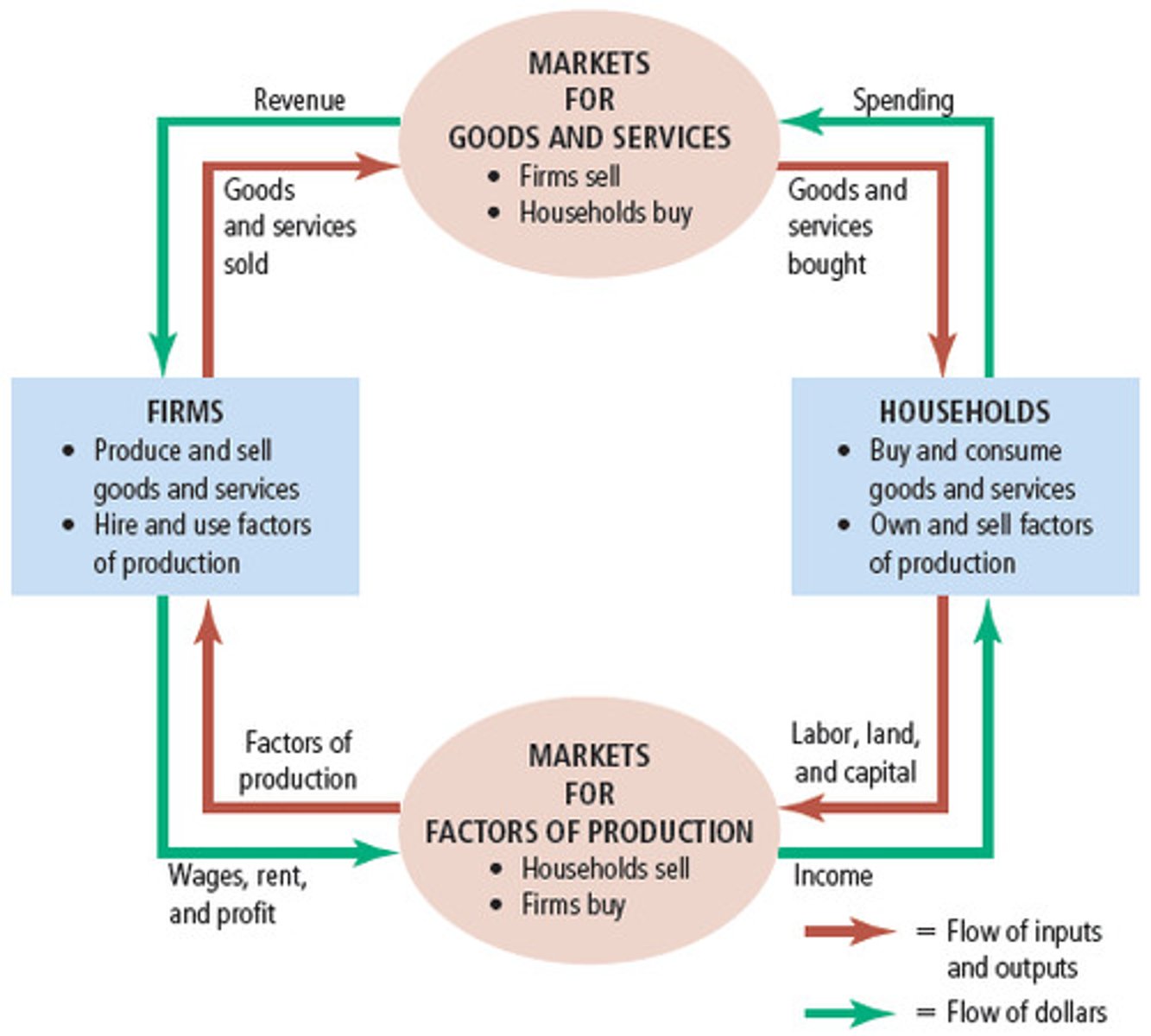

Circular Flow Diagram

shows firms & households and how they trade

Comparative Advantage

the ability to produce a good at a lower opportunity cost than another producer

Absolute Advantage

the ability to produce a good using fewer inputs than another producer

Why economists disagree?

Differences in positive statements and normative statements

Positive Statements is

testable

Normative Statements is

not testable (opinion)

GDP

the market value of all final goods & services produced within a country in a given time period

GDP equation

Y = C + I + G + NX

Y=

GDP

C=

Consumption

I=

Investment

G=

government spending

NX=

net exports (exports-imports)

Do imports effect GDP?

No they do not increase or decrease GDP

GDP deflator

Nominal GDP/Real GDP x 100

inflation deflator

( deflator current - deflator previous ) / ( deflator previous ) x 100

Inflation

general rise in overall prices

Consumer Price Index (CPI)

measure of the overall cost of goods & services bought by a typical consumer

5 Steps to Calculate CPI (inflation)

1. Fix the Basket

2. Find Prices (things in basket)

3. Compute cost of the basket

4. Chose a base year & compute CPI

5. Compute inflation rate

inflation rate equation

CPI Year 2 - CPI Year 1/ CPI Year 1 x 100

CPI equation

100 x (cost of basket in current year/cost of basket in base year)

Shadow Inflation

occurs when prices stay the same but the quality of products declines

2 types of unemployment

Cyclical & Natural Rate of Unemployment

What does it mean to be unemployed?

out of work and actively looking for a job

Categories to measure unemployment

Employed: paid, work with family, temporary absences

Unemployed: not employed, available for a job, looked for a job in the last 4 weeks

Not in labor force: not employed & not unemployed (students & elderly people)

unemployment rate formula

unemployed/labor force x 100

labor force formula

employed + unemployed

labor force participation rate formula

labor force/adult population x 100

real gdp

GDP adjusted for inflation

nominal gdp

the production of goods and services valued at current prices

marginal benefit

the additional benefit to a consumer from consuming one more unit of a good or service

marginal cost

the cost of producing one more unit of a good

final goods

goods and services that have been purchased for final use and not for resale or further processing or manufacturing

intermediate goods

goods used in the production of final goods

can one person have comparative advantage for both goods?

No

A person can have absolute advantage in producing both goods

true

Specialization and trade based on comparative advantage increase total output and make everyone better off.

True

CPI tends to overstate inflation by about 1%.

True

Due to biases (quality change, new goods, substitution), CPI overstates inflation by about 1%.

Household production is included in GDP

False

Household production (like cooking at home) is not bought or sold in markets, so it is excluded.

Black market activity is included in GDP.

False

Black market activity is illegal and unreported, so it is not counted in GDP.

New housing is counted as consumption

False

New housing is counted as investment, not consumption.

Stocks and bonds are considered investment in GDP

False

Stocks and bonds are financial assets and do not represent current production

Marginal Principle

states that decisions should be made by comparing marginal benefits (MB) and marginal costs (MC). The rational rule is to continue an activity until MC exceeds MB

Explain how the Circular Flow Diagram illustrates the relationship between households, firms, factor markets, and product markets. Include how income equals expenditure.

● Households supply labor and other factors of production

● Firms hire factors and produce goods and services

● Income flows to households through wages, rent, and profit

Spending flows to firms through product markets

Explain the three biases that cause the CPI to overstate the cost of living and why they matter for measuring inflation.

● Quality improvements: Better products raise prices but also raise value

● New goods bias: CPI is slow to reflect new products

● Substitution bias: Consumers substitute cheaper goods, but CPI assumes a fixed basket

● These biases cause CPI to overstate inflation

Explain the difference between final goods and intermediate goods, and why only final goods are counted in GDP

Final goods are fully processed and ready for consumption, while intermediate goods are inputs used to produce other goods. Only final goods are counted in GDP to avoid double counting the value of inputs already included in final products

Describe the difference between nominal GDP and real GDP and explain why economists prefer real GDP

Nominal GDP measures output using current prices, while real GDP measures output using base-year prices. Economists prefer real GDP because it removes the effects of inflation and better reflects true changes in production.

What is opportunity cost, and why is it central to economic decision-making?

Opportunity cost is the value of the next best alternative that must be given up when a choice is made. It is central to economics because all decisions involve trade-offs due to scarcity.