C37 CIA IFRS 2

1/21

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

22 Terms

Purpose of RA

Adjusts PV of future CFs to reflect compensation entity requires for bearing uncertainty ab amount & timing of CFs from non-financial risk

RA is higher for risks with:

Low freq / high sev

Longer duration contracts

Wide prob distr

Less known ab current estimate & its trend

RA is lower for risks with:

Emerging experience → more aware ab timing & amt of CFs

RA → Level of Aggregation

IFRS 17 Principles

Measurement → requires unit of account level

Presentation & Disclosure → requires aggregated level

Possible RA granularities

Aggregate → allocate back to unit of account level to satisfy Measurement

Unit of Account level → sum to get aggregate RA to satisfy Presentation & Disclosure

RA → Diversification Benefit

If units of account are diversified → lower aggregate RA

If RA calculated @ aggregate lvl

Benefit factored in

If RA calculated @ unit of acount lvl then sum

Diversification benefit might not be accurately reflected

Is reinsurance credit risk reflected in the RA?

NO

Reflected thru reduction in expected CFs

4 Methods for Calculating RA

Quantile methods

Cost-of-Capital method

Margin method

A combination of methods

Calculating RA → Quantile Method

Use distr of FCFs to determine RA for a given prob

Ex: VaR, CTE

Generate distr using Monte Carlo, bootstrap, etc

Pro: satisfies IFRS17 Disclosure req → gives CI for RA

Con: inaccurate if distr misrepresented

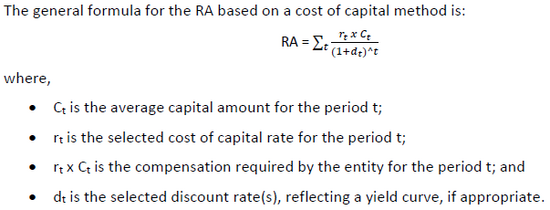

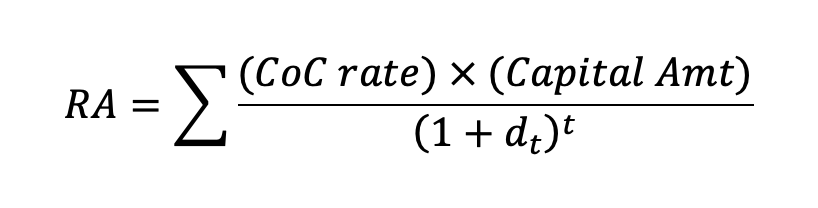

Calculating RA → Cost of Capital (CoC) Method

RA based on compensation required to meet target return on capital

3 Components

Projected capital amts

CoC rates

Discount Rates

Pro: conceptually close to def’n of RA

Con: operationally complex bc need projection of capital requirements

Calculating CoC Rate

CoC Rate = Target ROE - Investment Rate

Note: If Target ROE is after tax → remove tax first!

CoC Rate = Target ROE/(1-Tax%) - Investment Rate

Calculating RA → Margin Method

Select margins that reflect compensation entity requires for uncertainty of non-financial risk

RA for Reinsurance Held → Granularity

Pick 2 of gross, net, or ceded

Then add/subtract to get the third

4 Methods for Calculating RA for Reinsurance Held

Quantile methods

Cost of Capital methods

Catastrophe models

Proportional scaling

specific to reinsurance held

Calculating RA for Reinsurance → Catastrophe Models

Use output from cat model tailored to entity’s book of business

Select percentile directly from given distr

Calculating RA for Reinsurance → Proportional Scaling

Best for quota share

Use RA for direct business → scale to ceded portion

i.e. use same RA as % of PV(future CFs)

Can be modified to consider ceding commissions, expense allowances, etc.

RA for Catastrophe Reinsurance

May need to calculate net RA & ceded RA separately

Reason:

Low freq, high sev events

Standard Quantile method may product RA that’s too small

Method for Calculating: CoC method

w/ assumption for required capital set at higher percentile

Calculating RA → Ex of combining methods

Unit of account level combination

For groups w/ less skewed distr → VaR quantile method

For groups w/ highly skewed distr → CoC

Calculating RA → Aggregate/entity-level approach

Primarily use Quantile or CoC method

Simplified CoC Method

IDEA: Target profit margin allocated between

Reserve risk

UW risk

Other risks not relevant to RA

Given:

Profit Margin %

Capital Allocation % → Reserve / UW / Other risks

RA for LIC = EP x (Profit margin %) x (Capital % for Reserve risk)

RA for LRC = UEP x (Profit margin %) x (Capital % for UW + Reserve risks)

Quantile Method → Methods to generate Distribution

Monte Carlo

Bootstrap

Pro: recognizes heavy tails & other observations that departs from theoretical distr

Con: Bad for small samples → assumes each sampled variable is indep from another

May not adequately represent low freq/high sev events

Scenario Modelling

Ex: FCT

But may not meet materiality threshold for RA

Calculating RA using CoC Method

CoC Rate

r = Target ROE/(1-Tax Rate) - Investment Rate

Undiscounted Capital

Unpaid Loss x Liability/Surplus Ratio

Undiscounted Capital for non-financial risk

Remove other risks → market, operational

RA → IFRS17 Disclosure Requirements

Need CI for RA

Use quantile method