CH. 5: Receivables and Sales (ACC 2101)

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

36 Terms

Credit sales

Transfer of goods or services to a customer today while bearing the risk of collecting payment from that customer in the future. Also known as sales on account or services on account.

A company will debit ________ when recording a credit sale,

A. Sales Revenue

B. Cash

C, Accounts Payable

D. Accounts Receivable

D. Accounts Receivable

Invoice

A source document that identifies the date of sale, the customer, the specific items sold, the dollar amount of the sale, and the payment terms.

Accounts receivable

When the custermors owe the company money after the company already provided the good/service to the custermor

Revenue

Revenue is the inflow of assets or settlement of liabilities (or a combination of both) from delivering goods or services as part of a company’s core operations. Also, sales, sales revenue, or service revenue.

What would be the debits and credits if a company has already provided the good/service to a custermor, but the custermor plans to pay the good/service at a later date? On the com

Debit: Accounts Receivable

Credit: Service Revenue

What is the benefit of extending credit?

Lets customers buy now and pay later makes it easier for them to purchase from you, which can boost your sales and profits over time.

What is the cost of extending credit?

You have to wait longer to actually receive the cash, and some customers might never pay you back — both of which hurt your company's efficiency and bottom line.

Nontrade Receivables

Recievables originating from sources other than customers

Notes Receivable

an official written document spelling out the terms — like how much is owed, when it'll be paid back, and usually with interest included.

Revenue recognition principle

Record revenue in the period in which we provide goods and services to customers for the amount the company is entitled to receive.

What are the 4 types of accounts that reduces revenue a company actually collects?

Trade Discounts

Sales Returns

Sales Allowances

Sales Discounts

Net Revenues/Net Sales Formula

Net Sales = Gross Sales − Trade Discounts − Sales Returns − Sales Allowances − Sales Discounts

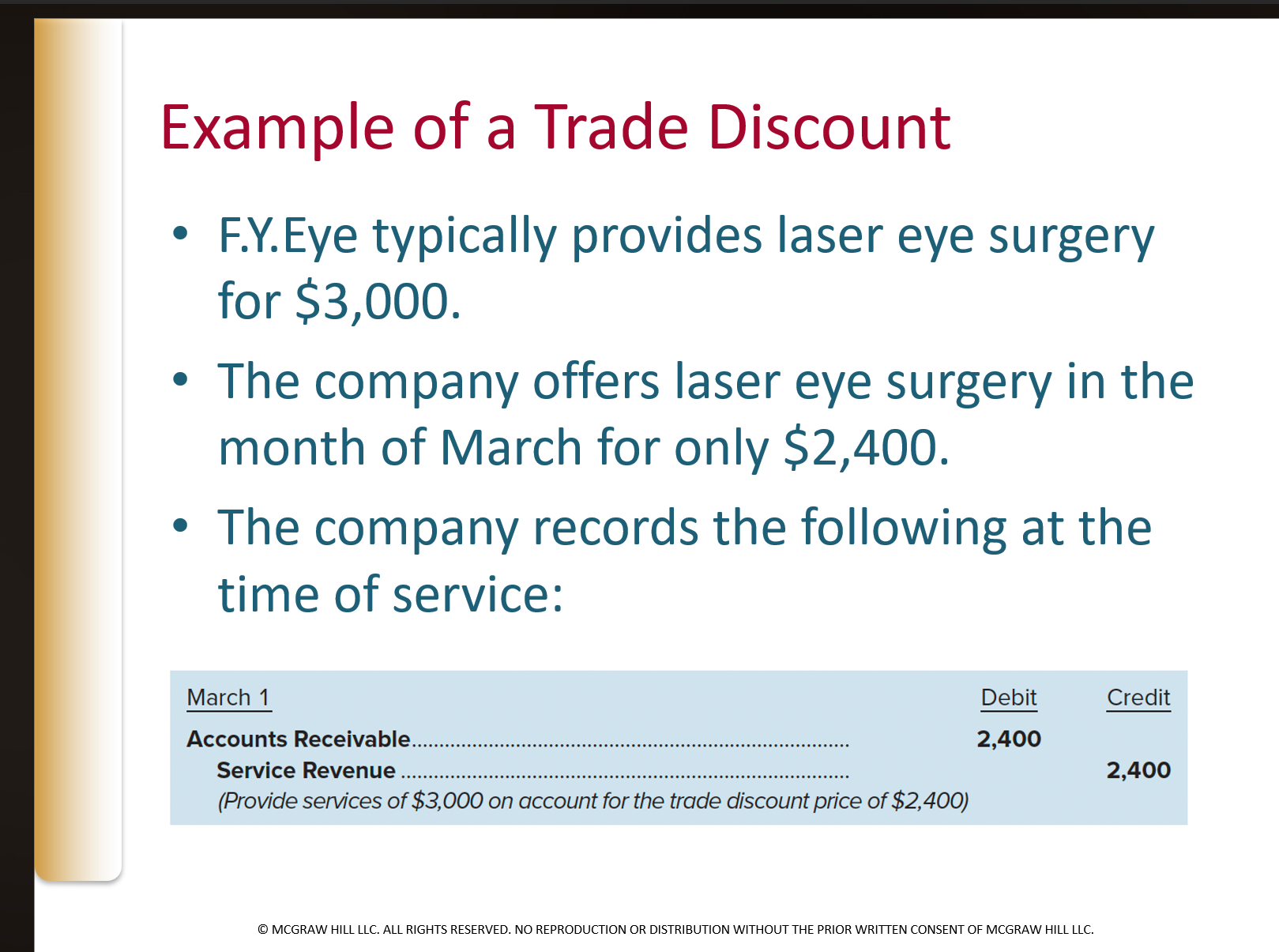

Trade discount

Reduction in the listed price of a good or service. Because sellers are entitled to receive only the discounted amount, sale is recorded at this lower amount.

Sales return

Customer returns a product. As a result, the seller reduces balance of accounts receivable if original sale was on account

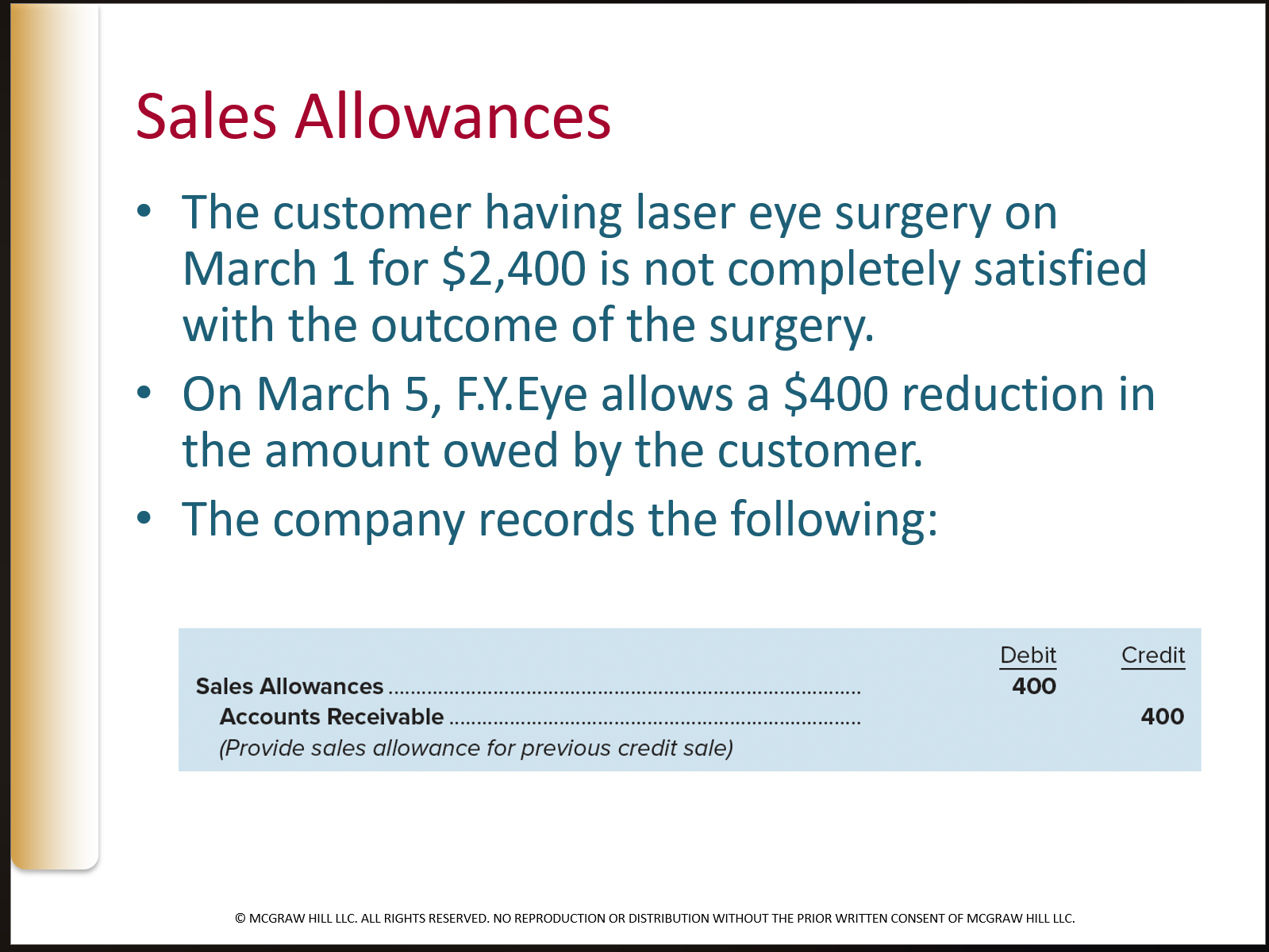

Sales allowance (Contra Revenue Account)

A reduction granted to a customer who keeps defective, damaged, or incorrect merchandise rather than returning it. The seller essentially says "keep it, but we'll knock something off the price." It's a price concession after the sale, not tied to payment timing.

Contra revenue account

An account with a balance that is opposite, or “contra,” to that of its related revenue account. Ex: Sales Return

On November 5, Phelps Outerwear sells a coat on account to a customer for $200. On November 15, the customer decides to return the coat to the retailer. The journal entry on November 15 will include a:

A) debit to Sales Revenue

B) debit to Sales Returns

C) credit to Accounts Payable

D) credit to Sales Revenue

B) debit to Sales Returns

Contra Revenue Account

Paired against a revenue account on the income statement. It carries a debit normal balance (opposite of revenue's credit balance) and reduces gross revenue down to net revenue.

Contra Asset Account

Paired against an asset account on the balance sheet. It carries a credit normal balance (opposite of an asset's debit balance) and reduces the gross asset down to its net carrying value. Ex: Sales Revenue

On May 1, Arden Wholesale sells $800 worth of goods on account to an out-of-state customer. Upon receiving the order on May 7, the customer notifies Arden that approximately 5% of the goods arrived damaged. As a result, Arden reduces the amount owed by the customer by $50. The journal entry by Arden Wholesale on May 7 will include a:

A)debit to Sales Discounts

B) credit to Accounts Receivable

C) debit to Sales Revenue

D) credit to Sales Allowances

B) credit to Accounts Receivable

Allowance Method

Making your best guess at the end of each period about how much of your outstanding receivables you probably won't collect — and recording that estimate before you actually know which specific customers won't pay. It is required by GAAP for financial reporting purposes.

Allowance for Uncontrollable Accounts

a company's best estimate of accounts receivable that will not be collected from customers

How to find the uncollectable accounts?

remains due from customers (% estimate of the total year-end accounts receivable that will not be collected)

Accounts with normal accounts include…

Allowance for uncontrollable accounts

Sales Revenue

Under the allowance method, companies are required to estimate future uncollectible accounts and record those estimates in the current year. Estimated uncollectible accounts:

A. increase total assets and increase net income.

B. decrease total assets and increase net income.

C. decrease total assets and decrease net income.

D. increase total assets and decrease net income.

C. decrease total assets and decrease net income.

Effect on total assets: The Allowance for Uncollectible Accounts is a contra asset that reduces Accounts Receivable on the balance sheet, bringing net realizable value down → total assets decrease

Effect on net income: Bad Debt Expense is an expense on the income statement, which reduces net income → net income decreases

According to the allowance method, writing off an account receivable will include a:

A. debit to Bad Debt Expense

B. credit to Cash

C. credit to Allowance for Uncollectible Accounts

D. credit to Accounts Receivable

D. credit to Accounts Receivable

Under the allowance method, the write-off of accounts receivable:

A. has no effect on total assets or net income

B. decreases total revenues.

C. decreases total assets.

D. decreases total expenses.

A. has no effect on total assets or net income

Beta Corporation wrote off $100,000 due from a specific client in March. However, this client was able to make a partial payment of $15,000 in June. Recording this cash collection will involve all of the following accounts except:

A. Allowance for Uncollectible Accounts

B. Accounts Receivable

C. Cash

D. Bad Debt Expense

D. Bad Debt Expense

How to calculate the debit to bad debt expense?

Adjusted ending balance - Balance Before Adjustment

When is the direct write off method used in financial reporting?

When an account actually becomes uncollectable due to bad debt expense. Contrast this to the allowance method, which requires estimation of uncollectible accounts before they even occur.

Writing off an account receivable using the direct write-off method includes a debit to:

A. Allowance for Uncollectible Accounts

B. Accounts Receivable

C. Cash

D. Bad Debt Expense

D. Bad Debt Expense

When does the allowance method record bad debt compared to the write off method?

Allowance Method recognizes bad debt expense in the same period as the sale through an estimate, while the write off method Only records bad debt expense when a specific customer is confirmed uncollectible

How to calculate a company’s receivables turnover ratio?

Net Credit Sales / Average Accounts Receivable

Average Accounts Receivable

(Beginning A/R + Ending A/R) / 2

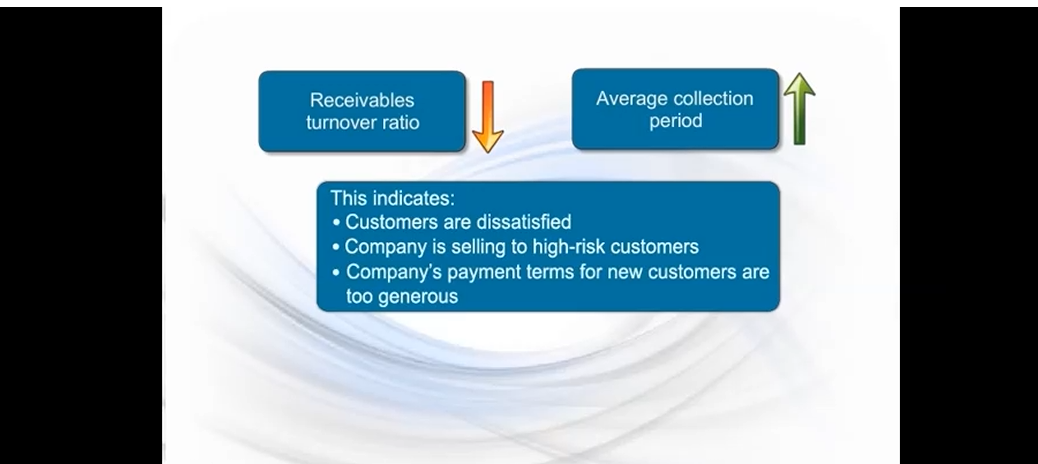

If a company’s % increase in receivables is greater than their % increase in sales, how will this effect receivables turnover ratio and the Average Accounts Receivable?

Receivables turnover ratio declines, and Average Accounts Receivable Rises. As a result, sales returns and bad debts increase.