C36 CIA IFRS 17 - LRC

1/37

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

38 Terms

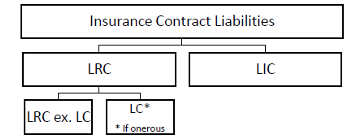

Insurance Contract Liabilities =

LIC + LRC

LRC =

If onerous: LRC = (LRC excl LC) + LC

= FCF

CSM = 0

If non-onerous: LRC = FCF + CSM

= LRC excl LC

LC = 0

LC vs CSM

LC

Onerous contracts

Recognized immediately

CSM

Non-onerous contracts

Deferred

LRC is an entity’s obligation to:

*5 NOTs

a) Investigate & pay valid claims under existing insurance contracts for insured events that have NOT yet occurred

b) Pay amts under existing insurance contracts NOT in (a) & relate to:

Insurance contract services NOT yet provided

Any investment components or other amts NOT related to provision of insurance contract services & have NOT been transferred to LIC

Contract Boundary

Defines CFs that should be included when measuring insurance liability

Ex of CFs: prem paid by policyholders, payments from insurer

Boundaries are usually policy effective & expiry date

Position of a portfolio of contracts

Asset Position: expected cash inflows > outflows

Liability Position: expected cash outflows > inflows

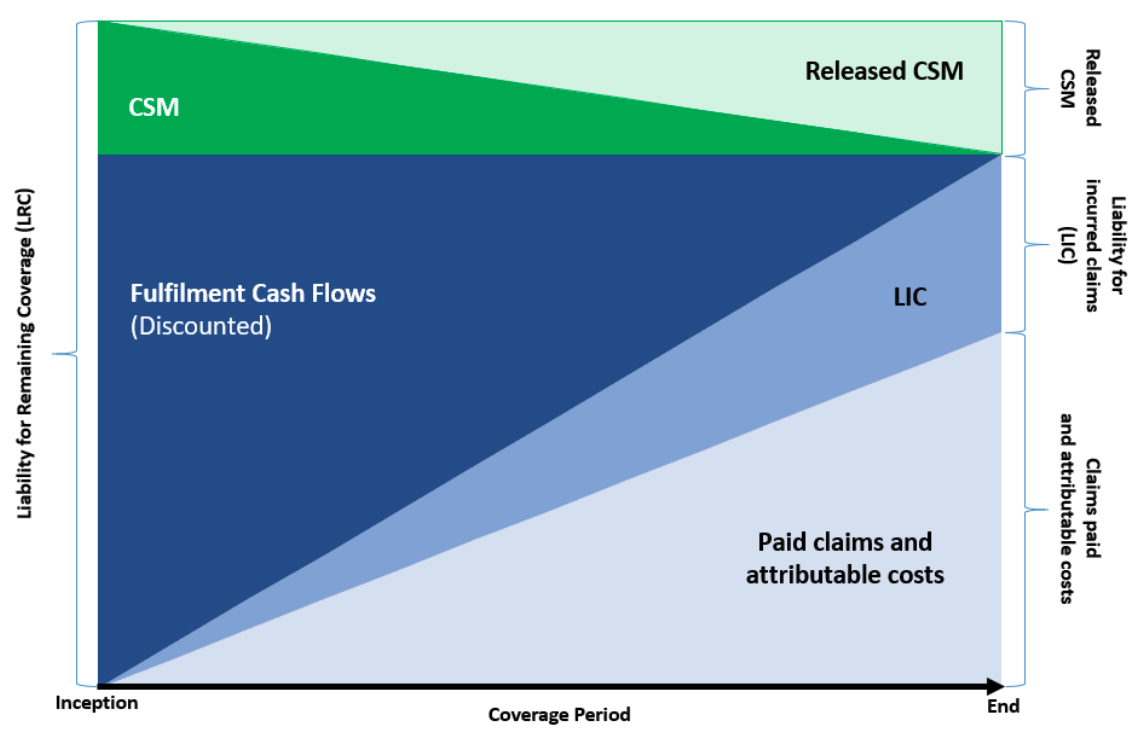

Contractual Service Margin (CSM)

Unearned profit from group of insurance contracts

Only if non-onerous

LRC (non-onerous) over coverage period

At contract inception: LRC = FCF + CSM

LIC, Paid = 0

At end of covg period: LRC = 0

FCF released into paid & LIC

CSM released into profit

Aggregation level → Expenses / LRC & CSM / FCFs

Expenses & FCFs

Must be allocated to group lvl

LRC & CSM

Must be determined @ group lvl

Future Cash Flows

Contract boundary usually policy term

Inflows = prem

Outflows = claims & directly attributable expenses

Discounting Procedure

Determine payment pattern

Apply discount factors

How to estimate timing of LRC CFs on group basis?

Estimate payment pattern on group basis

or

Adjust AY payment pattern used for LIC to a pattern consistent w/ avg acc date of group

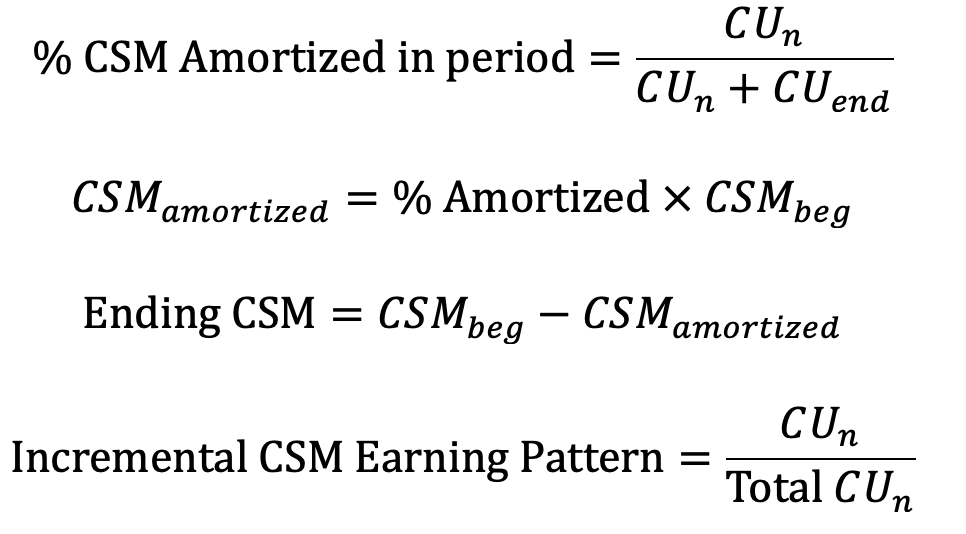

Carrying Amt of CSM @ end of reporting period

= Carrying Amt @ start + Adjustments

Adjustments include:

Effect of new contracts

Effect of FX differences

Interest during repting period

Amortization of CSM

CSM is amortized over reporting period

CSMbeg = CSM @ beginning of period

= Ending CSM of prev period!

CUn = covg units provided in period

CUend = covg units @ end of period

Steps

% CSM Amortized in period

CSMamortized

Ending CSM

Incremental CSM earning pattern

Coverage Unit

Quantity of insurance contract services provided by contracts in group

Determines how CSM is released into profits

Coverage Units → Key Principles

Quantity of benefits generally not based on expected claims

Discounting optional

Covg period extends to end of period in which insurance contract services are provided

CSM Amortization Patterns

Uniform: contracts w/ same policy limit throughout covg period

Declining: contracts w/ dec policy limit over covg period

Ex: mortgage insurance

Increasing: contracts w/ inc policy limit over covg period

Ex: product warranty w/ replacement covg

Wy do entities have to track (LRC excl LC) and LC separately?

Want to keep onerous & non-onerous contracts separate

What happens when non-onerous contract become onerous subsequently?

CSM reduce to 0

Establish an LC!

Why does accounting track non-onerous & onerous contracts separately?

Non-onerous → net intflow

Have CSM

LC = 0

Onerous → net outflow

Have LC

CSM = 0

Loss Component (LC)

Component of LRC depicting net outflow for onerous group of contracts

CSM = 0 → LRC = FCFs

PAA

For calculating LRC excl LC

If non-onerous → LRC = LRC excl LC

If onerous → LRC = (LRC excl LC) + LC

Need GMA to find LC…

PAA NOT used for LIC

How is PAA more simple than GMA?

Doesn’t require est of FCFs

Doesn’t require CSM

PAA → LRC (excl LC) @ initial recognition

= Prem received @ initial recognition

- Acquisition CFs

± Derecognition of certain assets/liabilities

PAA → LRC (excl LC) @ subsequent measurement

= Carrying Amt @ start of period

+ Prem received in period

- Acquisition CFs

+ Amortization of Acq CFs recognized as expense in period

- Insurance Revenue

- Investment component paid/transferred to LIC

Summary: UEP - Acq CFs not expensed + Adj for financing - Investment component

Only use directly attributable expenses!!!

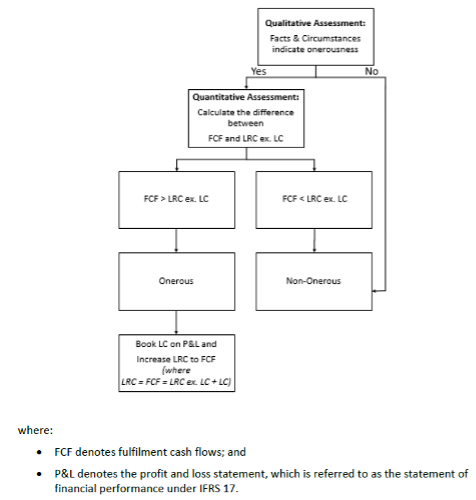

How to determine if contract is onerous

Qualitative Assessment

Facts & circumstances indicating onerousness

Quantitative Assessment

Calculate FCFs & LC

Onerousness → Decision Tree

First, use Qualitative Assessment

If not onerous → done

If onerous → apply Quantitative Assessment

Quantitative Assessment

If FCF < LRC excl LC → non-onerous

If FCF > LRC excl LC → onerous!

Book LC on P&L

Set LRC = FCF

Onerousness → Qualitative Assessment

If facts & circumstances indicate need for onerousness

Group of contracts known to be onerous

Past losses in portfolio

Aggressive UW or pricing

Unfavourable experience trends

Unfavourable external conditions

Accounting steps required if contracts are onerous

Recognize loss in insurance service expenses IMMEDIATELY for net outflow

Establish LC as part of LRC

LC throughout covg period

LC released into insurance service expenses

Amortized from LRC over covg period

LC = 0 @ end of covg period

Recognition of Acquisition Costs → GMA vs PAA

GMA → cannot recognize Acquisition Costs immediately

PAA → can recognize immediately if covg period of all contracts <= 1yr

Financing Component in PAA

Don’t have to reflect TVM on LRC if Financing Component not significant

Ex: if period between prem due & service provided <= 1 yr

Benefits entity as policyholder finances entity’s activities by pre-paying prem

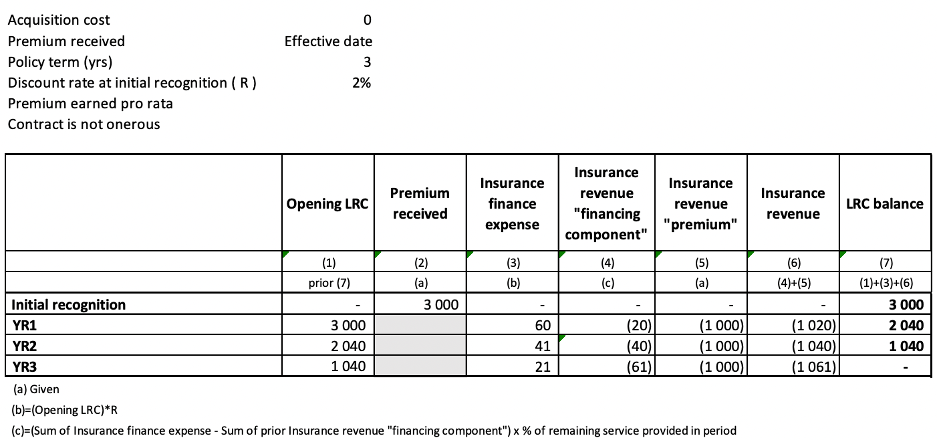

Ex of PAA est of LRC w/ significant financing component

Prem received → written @ initial recognition

Insurance Finance Expenses = Opening LRC x Discount Rate

Insurance Rev Financing Component = -1 x SUM(fin expenses + PRIOR fin components) x %remaining covg provided this period

Insurance Rev EP = -EP

Insurance Revenue = Ins Rev Fin Component + Ins Rev EP

LRC Balance = Opening LRC + Finance Expenses + Insurance Revenue

= 0 @ end of covg period!

Investment Component

Amt that insurer has to repay policyholder regardless of whether insured event occurs

LRC → GMA vs PAA

Application

GMA → all P&C contracts

PAA → only if eligible

CF Projections

GMA → yes

PAA → not unless onerous

RA

GMA → yes

PAA → not unless onerous

CSM

GMA → yes if contract is issued & NON-onerous

PAA → no

LC

Both → yes if onerous

Option to immediately recognize Acquisition Costs

GMA → no

PAA → yes if covg period of all contracts <1 1 yr

Quantitative Onerous Contract Test

GMA → always required

PAA → only if indicated by qualitative test

PAA → Calculate LC

Calculate GMA est of LRC

LC = FCF - (LRC excl LC)

= (GMA est of LRC) - (PAA est of LRC excl LC)

Use FCF & (LRC excl LC) to calculate Profit/Loss

Profit/Loss = (LRC excl LC) - FCF

Discounting LRC

Use Avg acc date = 0.33 instead of 0.5!!

ONLY FOR LRC