Chapter 17: Advanced Issue in Revenue Recognition

1/77

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

78 Terms

What is the core principle in revenue recognition?

A company should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

What is revenue in Revenue Recognition?

increases in assets or settlements of liabilities during a period from delivering or producing goods, rendering services, or other activities that are the company's ongoing major or central operations.

What is the 5-Step Revenue Recognition Model?

1. Identify the contract with a customer.

2. Identify the performance obligations in the contract.

3. Determine the transaction price.

4. Allocate the transaction price to the performance obligations in the contract.

5. Recognize revenue when or as the company satisfies the performance obligation

What is a customer?

a party that has entered into a contract with a company to obtain goods or services that are an output of that company's ordinary activities.

What is a contract?

an agreement between two or more parties that creates enforceable rights and obligations. A contract may be written, oral, or implied by customary business practices.

What is the Criteria 1 to be met for contracts to apply the revenue recognition standards:

All parties to the contract approve the contract (written, orally, implication) and commit to perform their obligation under contract.

What is the Criteria 2 to be met for contracts to apply the revenue recognition standards:

The company is able to identify each party's rights regarding goods/services to be transferred

What is the Criteria 3 to be met for contracts to apply the revenue recognition standards:

The company is able to identify the payments terms for the goods/services to be transferred. Doesn't imply transaction is fixed, explicitly stated, price may vary due to discounts or rebates

What is the Criteria 4 to be met for contracts to apply the revenue recognition standards:

The contract has commercial substance (contract must change the timing, amount, probability of company's future cash flow)

What is the Criteria 5 to be met for contracts to apply the revenue recognition standards:

It is probable that the company will collect the consideration to which it is entitled in exchange for the good/services that it will transfer to the customer.

What are the four issues in identifying a contract?

1. Termination Rights

2. Combining Contracts

3. Contract Modifications

4. Collectability

What are termination rights?

A contract that doesn't qualify for revenue recognition and no revenue can be recognized if the contract is unperformed. Either party can cancel before performance without compensating the other party

What is a wholly underperformed contract?

The seller has not transferred the goods/services to the customer, nor received or is entitled to receive, consideration in exchange for the promised good/service

What is the key objective of combining contracts?

So that the economics of the revenue to be recognized from the transaction can be only understood with reference to the arrangement as a whole

A company must combine two or more contracts and account for them as a single contract if the following criteria are met: (4)

1. If it enters the contract at or near the same time with the same customer.

2. The company negotiates the contracts as a package with a single commercial objective.

3. The amount of consideration to be paid in one contract is dependent upon the price or performance of the other contract.

4. All or some of the goods or services promised in the contracts comprise a single performance obligation.

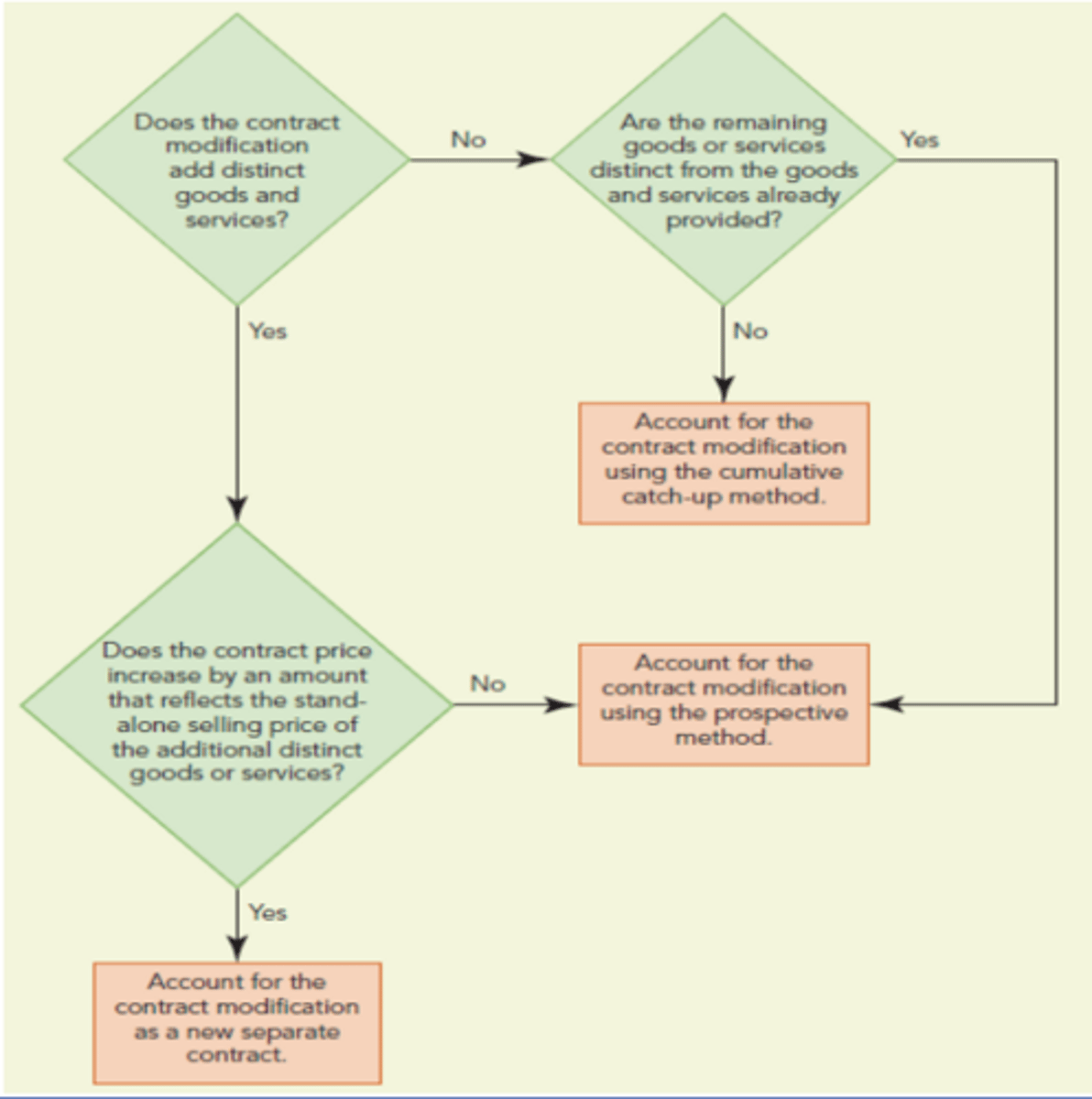

The contract modification graph look like?

What is the prospective method used if the modification does what?

1. Adds distinct goods or services but the consideration for those goods or services does not reflect the standalone selling price

2. Does not add goods or services but the remaining goods or services are considered distinct from the goods and services transferred in the original contract.

When accounting for the prospective method, it assumes?

the original contract is terminated and a new contract is created

What is the cumulative catch-up method?

It is used when the remaining good/services that are to be delivered are NOT distinct from the goods/services delivered in the original contract

In the Cumulative Catch-Up Method, how is the revenue account adjusted?

It is adjusted at the time of the contract modification for the cumulative amount of revenue that would have been recognized in prior period if the new contract terms had existed.

In Collectability, in order to recognize revenue, we must?

It must be probable that the seller will collect the expected consideration in exchange for the goods/services it is transferring to the customer

In Collectability, it must be assessed by who and includes what?

It must be assessed by the seller and include the customers ability/intent to pay (credit risk), as well as any price concessions expected to be provided to the customer

In Collectability, any amount not expected to be collected should?

Reduce the contract price, which is the starting point to apply the remaining steps in revenue recognition

What is a performance obligation?

a promise in a contract with a customer to transfer goods or services. The promise may be explicit or implicit .

What is a constructive obligation?

an implicit promise in which the seller creates a compelling expectation that it will provide the promised goods or services based on its customary business practices, published policies or specific statements.

What is the criteria for distinct goods or services?

1. Promised G/S are capable of being distinct because the customer is able to benefit from the G/S either on its own or together and are available

2. Promised G/S is distinct within the context of the contract because the sellers promised to transfer the G/S to the customer is separately identifiable from other promises in the contract

What is the first separately identifiable characteristics:

The G/S is not significantly integrated with other promised G/S offered offered by the seller

What is the second separately identifiable characteristics:

The G/S does not significantly modify or customized another G/S promised to the contract

What is the third separately identifiable characteristic:

The G/S is not highly dependent or interrelated with other promised G/S

If the promise to deliver goods or services is distinct?

The performance obligation is accounted for separately

If the promise to deliver goods or services is NOT distinct, then

The seller combines it with other promised G/S to which it relates until it has identified a bundle of promised G/S that is distinct. Once identified a separate performance obligation exists.

What are other issues in identifying performance obligations?

1. Upfront Payments

2. Licensing

3. Principal - Agent Contract Consideration

What are upfront payments/

payments from customers before a product or service is delivered.

What upfront payments are nonrefundable?

set up fees, activation fees, initiation fees, or membership fees.

What upfront payments are for goods and services that can be redeemed?

Gift Cards

What upfront payments are for goods and services to be delivered in the future?

Fares for flights, entertainment events, rent

When upfront payments are received, companies must determine?

The performance obligation to which the upfront fee relates. Revenue should not be recognized until the performance obligation is satisfied.

In Licensing Issues, we have to identify what about the performance obligation?

Identify whether the performance obligations associated with a license is distinct from other performance obligations in the arrangement

What is the nature of license?

Does it provide access to intellectual property throughout the license period (performance obligation satisfied over time) vs. Does it provide access to the use of intellectual property as it exists at a point in time (performance obligation satisfied at a point in time)

What is a Principal’s performance Obligation?

provide goods or services to customers.

What is the Agent’s performance obligation?

arrange for goods or services to be provided by the principal to the customer.

What is Principal Contract Consideration?

recognizes gross amount received from the customer as revenue when the performance obligation is satisfied.

What is Agent Contract Consideration?

recognizes commission revenue for the net amount of consideration retained after paying the principal for the goods or services provided to the customer.

What is the first indicator that a company may be an agent?

Another company is primarily responsible for fulfilling the contract.

What is the second indicator that a company may be an agent?

The company does not have inventory risk before and after the goods have been ordered by a customer, during shipping or upon return

What is the third indicator that a company may be an agent?

The company does not have discretion in establishing prices for the goods and services.

What is the fourth indicator that a company may be an agent?

The company’s consideration is in the form of a commission.

What are the factors in determining transaction price? (4 factors)

the time value of money

variable consideration

noncash consideration

consideration payable to a customer

Sellers transaction prices is determined by..

Discounting the promised amount of future consideration to reflect the time value of money

The time value money is not required when the time period between customers payment and company’s transfer of good or services is….

less than one year

If it was separate financing arrangement then…

Discount rate is used

What is the objective of the time value of money?

For the seller to recognize revenue at the amount that would have been recognized if the customer paid cash at the time of transfer

What are the results for the time value of money?

The contract is separated into revenue element accounted for with the revenue recognition model and financing element accounted for as financing

When a contract contains variable consideration, GAAP requires what to be recognized?

The total consideration in an amount the seller expects to receive when the uncertainty is resolved

In Variable consideration, the seller must complete the following step? (Step: 1)

Estimate the total amount to which it expects to be entitled (the variable consideration).

In Variable consideration, the seller must complete the following step? (Step: 2)

Determine if there is an applicable constraint on the variable consideration

In Step 1: Estimation of total amount it expects to be entitled (Variable Consideration), what are the two approaches?

Expected value approach & Most-likely amount approach

What is expected value approach?

A company identifies the range of possible outcomes and the probabilities associated with each outcome. The expected value is then calculated as the probability-weighted amounts in this range.

What is the most-likely amount approach?

the consideration is the single most likely amount within a range of possible variable consideration amounts.

In Step 2: Assessing Whether an Applicable Constraint Exists, what can a company may only include?

The variable consideration estimate from step 1 in the transaction price to the extent that is probable that a significant reversal of the revenue previously recognized will not occur

What are the 5 factors that will indicate a significant reversal of revenue could occur:

Estimate of consideration depends on factors outside of company’s control

Uncertainty regarding amount of consideration will not be resolved for a long time

Limited experience with similar contracts (limited predictive ability)

Price concessions or changes the payment of terms

Large number and board range of possible consideration amounts

If a noncash consideration is received the seller includes…

the fair value of the noncash consideration in transaction price

If the fair value of the noncash consideration cannot be estimated then it can be determenined?

Indirectly based on the stand-alone selling price of the promised G/S

How is noncash measured in US GAAP & IFRS?

GAAP: Measured as the contract inception date

IFRS: Measured date is not specified

If the payments are for discounts, refunds, coupons, rebates, free services, etc, the seller accounts for…

the consideration as a reduction in the transaction price.

If the payments are for a distinct good or service that the customer transfers to the seller, then the payment is accounted

as a purchase from a supplier.

In Allocate transaction Price to Performance Obligations: If there is only one performance obligation…

no allocation is necessary.

If there is more than one performance obligation, the seller allocates what?

he transaction price to each performance obligation in proportion to the relative stand-alone selling prices of those G/S.