Ch 16 Accounting Income CPA MCQ Acct 332

1/3

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

4 Terms

Packer Corporation’s year 8 income statement reported $130,000 in income before provisions for income taxes. To compute the provision for federal income taxes, the following year 8 data are provided:

What amount should Packer report as taxable income?

127,000

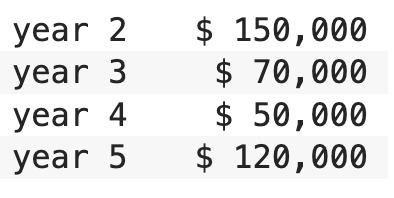

Truck Company, organized January 7th, year 1, has pretax accounting income of $720,000 and taxable income of $950,000 for the year ended December 31, year 1. The only temporary difference is accrued product warranty costs that are expected to be paid as follows:

Truck has never had any operating losses (book or tax) and does not expect any in the future. There were no temporary differences in prior years. The enacted income tax rates are 30% for year 1 and 25% for year 2 through year 5. How should the deferred income tax associated with accrued product warranty be recorded in Truck’s December 31, year 1 balance sheet?

$97,500 Asset

When accounting for income taxes, a permanent difference occurs in which of the following scenarios?

An item is included in the calculation of net income, but is neither taxable nor deductible.

Because Gene Company uses different methods to depreciate buildings for financial statement and income tax purposes, Gene has temporary differences that will reverse during the next year and reduce taxable income. Deferred income taxes that are based on these temporary differences should be classified in Gene’s balance sheet as a:

Noncurrent asset.