Global Macro Investing - theory

1/269

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

270 Terms

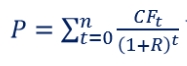

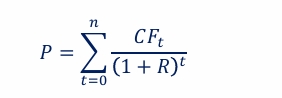

How do you determine the value of an asset?

determined by summing the present value of its expected future cash flows

determined by the discount model

the longer you wait, the higher the return on the asset

How do you determine the expected return of an asset?

using the fama-french 3/5 factor model

risk-free return (ie free lunch) + additional risk + size factor + value factor + profitability factor + investment factor

highlights the importance of diversification

only systematic risk will be rewarded

why is it difficult to consistently beat the market?

because it is efficient

how is asset pricing different from investment?

asset pricing theory explains returns using large datasets

ie it focuses on historical data

investment focuses on decision-making based on current conditions to determine the best action

eg after US invaded Venezuela, is it better to long or short oil?

asset pricing theory can’t help us as this event has never happened before

is the size factor always a good investment strategy to follow?

it can be a good investment strategy as you can short large firms and go long on small firms and earn a risk-free return

ie we are using the proceeds from one commodity to buy another

however, the SMB value factor fluctuates a lot overtime so it is not always a good investment decision

What can help to explain the large difference between S&P500 firms and Russell 2000 firms?

S&P 500 firms are mainly dominated by tech and AI firms which has seen a massive growth in recent years

Russell 2000 index is only up 24% over the past 5 years whereas S&P 500 has increased over 80%

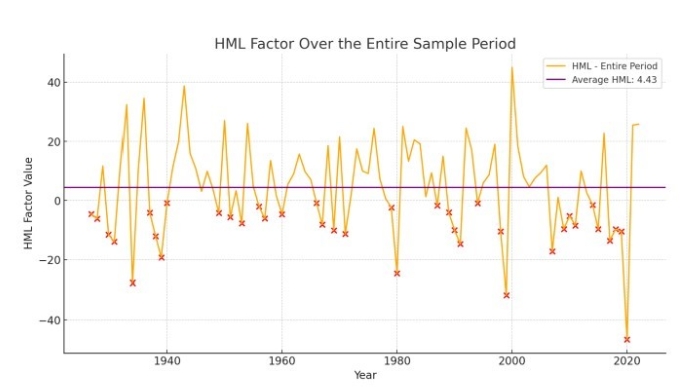

is the value factor a good investment strategy?

it can be viewed as a good strategy as it can provide an average annual return of 4.43%

however, Fama-French discovered that the factor is redundant once you include profitability and investment factors

small picture investing example (fund managers)

job is to beat a benchmark by trying to identify the shares (or bonds or other assets) that will outperform their peers

decision begins with the specifics

UK firm has expensive share prices, cost pressures, and profits are stagnating

Germany firm has cheap share price, managing costs well, and profits are growing

it would be in the fund manager’s interest to sell the share of the UK firm but buy the share of the Germany firm

big picture investing example (macro investors)

still in invest in shares, bonds, and other assets

instead of starting with company specific, they start with the bigger picture

identify large external forces that can drive the performance of companies, asset classes, and markets over time and distil these into a focused portfolio of investments

external forces include: economic developments, social change, and demographic shifts

invest in companies and other assets, across sectors and regions, that have the potential to benefit from these forces

try to profit from short exposure to companies/assets we expect to do badly as a result of these forces

no benchmark to constrain investors

aren’t reliant on rising markets to generate returns on investment

how is social change an external force for investing?

if we have an ageing population, how could this affect inflation?

furthermore, how does this impact dividends?

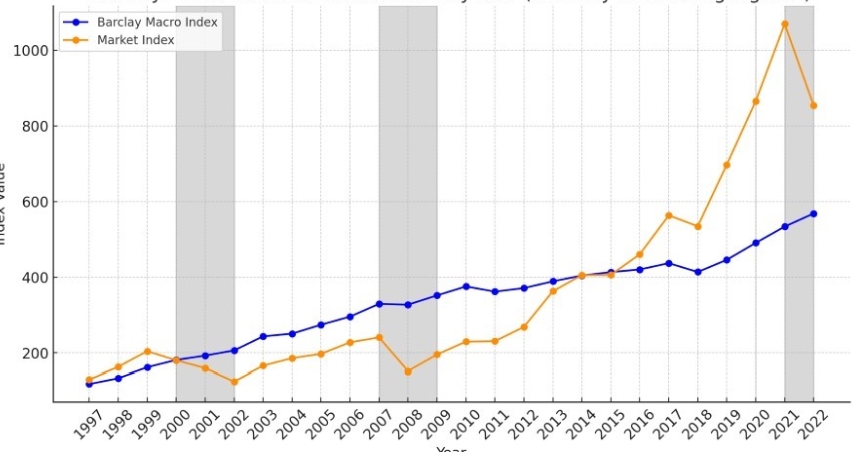

why do macro-style funds tend to yield slightly lower returns?

macro-style funds will buy AND sell whereas a typical macro investor will only buy

therefore, macro-style funds will have reduced risks

especially evident during market crashes when the macro strategy can both mitigate losses and profit from downward movements

how do large institutional investors possess significant information advantages over retail investors?

can afford large trading costs

eg a Bloomberg terminal (a financial software platform) costs $20,000+ per year

institutional investors exert substantial influence over manager compensation, encouraging ongoing communication

ie their reputation allows them to continue to succeed

they can act as market-moving information creators

eg if Blackrock is unhappy with a firm, they will be vocal about it and this will cause the share price of that firm to crash

lower financing and transaction costs provide a competitive edge

value investing/bottom-up strategies are particularly exposed to information asymmetry

Managers may have discrepancies in their approach to information disclosure, creating barriers for external investors. However, this is not a severe issue for macro investing, why?

free and fair access to most of the data

trading the entire economy, which diminishes the influence of individual participants, and even large institutions

communication is designed for the public, making it straightforward

presence of consensus topics leads to extensive coverage and liquidity

what financial assets are most commonly traded?

currencies

equities

fixed income

commodities

characteristics of currencies

the FX market is the most liquid financial market with a massive trading volume

has the highest trading volume

operates as a truly 24-hour market, due to time zone differences

major currencies have super tight bid-ask spreads

ie they have very low transaction costs

UK is most commonly traded within the FX market

trading the US dollar for the british pound

important to consider the currency regime when investing as different regimes have varying effects

characteristics of fixed income securities

for macro investing, sovereign/government bonds have a pivotal role

they represent the ‘risk-free’ rate as the government is very unlikely to default

this means the payoff is almost always realized

government bonds act as the primary tool for implementing monetary policy

they are also a major source of funding for governments to execute fiscal policies

how are fixed income assets distinct from other asset types?

their expected payoffs remain fixed when no default occurs

favourable for risk-averse investors

what is the crucial thing to know for fixed income securities?

when cash flows are known, the only uncertainty is the discount rate

predicting the discount is crucial

makes long-dated fixed income funds unfavourable as any changes in R are amplified

they are not intended to be kept until the end date due to the high duration risk

need to consider investment horizon

characteristics of equities

equity returns are not fixed, reflecting uncertainty in payoffs

makes them favourable for risk-loving individuals

equity returns are closely linked to earnings and the broader economy

index exposure is often obtained via derivatives, without individual stock analysis

individual stocks can still provide valuable information

in the long-run, equities will derive higher levels of return

why is it important to keep an eye on the Magnificent seven?

if one of these firms fails, it will cause the market to collapse as they hold a large percentage

characteristics of commodities

commodity producers naturally take long positions, benefitting from price increases

to reduce uncertainty, they often hedge by offsetting positions

commodities are among the most volatile asset classes but they lack the secular trends observed in equities

don’t experience a drift as the price fluctuations will be small

are derivatives high risk?

yes because they are traded on margin

examples of broad markets ETFs

SPY: tracks the S&P 500

QQQ: tracks the Nasdaq-100

examples of thematic/regional ETFs

ESGV: US ESG equities

PDJ: Chinese internet firms

IDA: Indian equities

examples of leveraged ETFs

SQQQ: - 3* daily return of the Nasdaq-100

TQQQ: +3*daily return of the Nasdaq-100

these are high risk

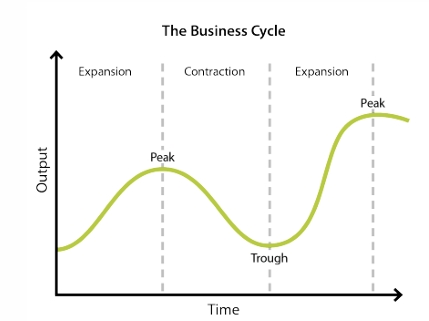

stages of a business cycle

expansion

peak

contraction

trough

characteristics of economic expansion

decreasing unemployment

increasing wages

increased spending

characteristics of economic contraction

increasing unemployment

results in the supply of labour to be greater than the demand

decreasing wages

decreased spending

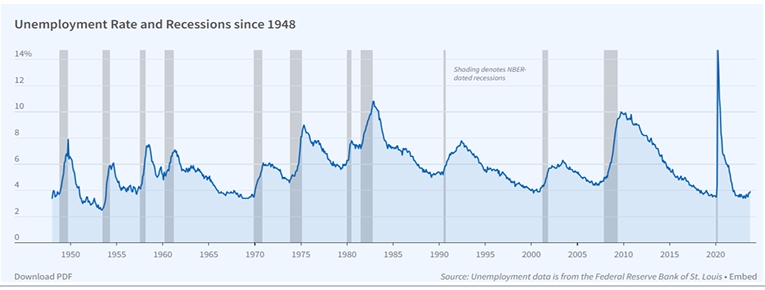

who identifies economic recessions and expansions? (in the US)

the NBER’s Business Cycle Dating Committee identifies the dates of peaks and troughs that frame economic recessions and expansions

what is noticeable about unemployment in recessions?

unemployment increases quickly but goes down quite slowly

it doesn’t move in a symmetric way

what factors determine the natural output level?

labour force and human capital

determined by social structures rather than economy

capital stock and technology

natural resources

institutional and structural characteristics

education and training

economic policies

demographics and population health

if a country has an ageing population, this means there are not enough young people to pay for taxes to support the older generation

sociopolitical stability

overall, very long-run exogenous factors determine natural output level

why must we determine the natural output level?

if the economy is growing too quickly, this will result in very high levels of inflation

if we are growing too slowly, this will result in high levels of unemployment

although the NBER Business Cycle Dating Committee determine when recessions occur, what problem do we still have?

they can’t predict when a recession will happen (ie no ex-ante predictions are made)

although they determine the dates of cycles for us, their announcements are made ex-post

they are informing us of the research findings after we are already in that particular phase of the cycle

this is not very useful when making investment decisions

need to adopt a forward-looking perspective on the business cycle

why do we care about business cycles?

it affects the value of an asset

business cycles shape monetary and fiscal policy

policy actions affect the discount rate (R)

the discount rate includes the risk-free rate plus the discount premium

if the economy is ‘over-heating’ the interest rate will increase

if the economy is slow, the interest rate will decrease

business cycle also affects firm earnings, and hence cash flows

how does long historical data help us assess where we are in the cycle?

when output is below trend, it often signals economic stress or downturns

eg: 70s oil crisis and inflation, early 90s recession, 2008 global financial crisis and subsequent European debt crisis, the COVID-19 shock and post-Brexit uncertainties

what is the UK natural output rate?

around 1% per year

lower than previous years due to Brexit and other political reasons

how do policy responses help the natural output level?

shocks can deviate output, creating an output gap

this may lead to higher unemployment or inflationary pressures

policy responses can act as counter-shocks, helping to narrow the gap and return output toward its natural level

these measures are predictable which creates trading opportunities

ie if the economy is overheating, we expect higher interest rates so would be a good time to buy a government bond

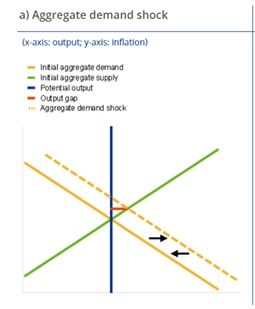

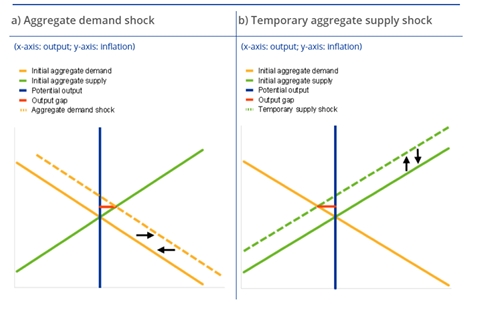

example of an aggregate demand shock

introduction to open AI

resulted in aggregate demand shock to the right

causes the economy to be richer

example of an aggregate supply shock

70s oil crash

results in aggregate supply shock to the left

quantity theory of money formula

M = money supply

V = velocity of money

P = price level

T = transactions or output

if we hold the left constant, this implies a negative relationship between P and Y

ie if price goes up, transactions will go down and vice versa

what can help to close the output gap?

shifts in aggregate demand

governments can artificially create a shock to demand or supply

eg Trump’s helicopter money during COVID-19

eg Sunal’s eat out to help out scheme during COVID-19

is giving money to everyone a good way to stimulate the economy?

the money has been raised through taxpayers; not coming from nowhere

it raises the supply of money, resulting in inflation

there are different welfare impacts

would have no effect on super rich individuals but have a huge impact on poorer individuals

results in high levels of demand

could stimulate supply instead

used in China during COVID-19 pandemic by subsidizing suppliers

results in jobs being maintained which is more beneficial in the long-run

however, this results in more being produced than needed, creating a downward pressure on prices

how can we gain insight into the current state of the economy?

by examining output (real GDP) and unemployment

however, GDP growth is not reflective of how individuals are doing

eg, salaries could be low but net exports could be high

output level is more reflective on how individuals are doing

trends in these indicators help us assess whether the economy is expanding or contracting

ways to identify a business cycle

two consecutive quarters of negative real GDP growth

the Conference Board Leading Economic Index (LEI)

it provides an early indication of significant turning points in the business cycle and the near-term economic outlook

is nowcasting accurate and precise?

no, the margins are very large

common sources of shocks

financial market disruptions

eg Blackrock don’t publish their deals but even if they did, we wouldn’t understand the impact of them

international disturbances

technological changes

energy price fluctuations

monetary policy actions aimed at controlling inflation

hard to make ex-ante predictions on the impact of the shocks

COVID-19 recession was short-lived

few anticipated the AI-driven boom in 2022

are business cycles the same?

no

the great recession differed to the energy crisis recessions

facts about the great recession

longest economic downturn since WWII

deepest recession prior to COVID-19

real GDP fell 8.5% in Q4 2008

unemployment peaked at 10% in October 2009

triggered by the subprime mortgage crisis and the collapse of the US housing bubble

facts about the energy crisis recessions

energy crisis 1: january - july 1980

energy crisis 2: july 1981 - november 1982

after the oil shock , the economy expanded briefly, but inflation remained high, peaking around 15% in 1980

period ended in a ‘double-dip’ recession

the 1980 recession was partly triggered by Fed rate hikes to combat inflation

the 1981-82 recession was the worst since the Great Depression

unemployment reached nearly 11% and GDP fell by 1.8%

Ray Dalio’s credit cycle explanation

Ray Dalio argues that the business cycle is driven by the credit cycle

in periods of optimism, borrowing expands

eventually, debt must be repaid, leading to contractions

if only one individual accumulated a lot of debt, it would have no impact but if the whole population does this, it can be very problematic

the process generates excessive booms and busts in economic activity

it is intuitive as credit expansion and contraction fluctuates over the business cycle

characteristics of a recovery

unemployment declines as firms begin to increase hiring

inflation remains relatively low, but may start to rise as demand picks up

consumer spending increases, potentially leading to moderate inflation

discount rate (R) may stay low to encourage borrowing and investment (ie low interest rates)

cash flow (CF) typically improves as economic activity picks up

characteristics of overheating/expansion

strong labour demand tightens the job market and pushes wages higher

low unemployment and rising inflation emerge

this means there are more job posts for one individual (ie labour demand > labour supply)

central banks respond by raising interest rates to cool the economy

discount rate (R) tends to increase in order to cool down the economy and curb inflation (due to increased interest rates)

cash flow (CF) peak or near peak levels (due to high levels of spending) but inflation may erode real gains

ie high cash flow but decelerating

characteristics of stagflation/slowdown

employment may stagnate

economic performance deteriorates

most challenging environment for central banks

interest rates must remain high despite slowing growth

discount rate (R) is challenging to adjust

may increase to control inflation or decrease to stimulate growth

high interest rate, peaked

cash flow (CF) may stagnate or grow minimally due to economic sluggishness (lower CF)

characteristics of contraction/recession

rising unemployment

reduced consumer spending

central banks cut interest rates to stimulate growth

discount rate (R) generally decrease to stimulate borrowing and economic activity

cash flow (CF) often declines as companies face reduced demand and potentially lower profitability

what matters when we want to invest in fixed income assets?

cash flow are given so interest rates (R) are the dominant factor

fixed income tends to be attractive when interest rates peak/start to fall

indication of the economy entering a downturn/contraction

means interest rates will be low, resulting in high price

what matters when we want to invest in equities?

cash flows and interest rates

recovery and early recession phases often signal improving prospects

typically favourable for equity investment

when do fixed income asset perform the best?

when the economy begins to contract

the return is much higher

shows how returns are heavily influenced by business cycles

when do equities perform the best?

perform the best in the contraction (recession) and recovering stage

however, they don’t do their best in the start of the slowdown (it can be very negative)

therefore, a common portfolio strategy is 60/40 fixed income/equities

this is because it creates a hedge as when equities are not doing well, fixed incomes are doing well

are all industries experience pro-cyclical movements with their assets?

no

during the slowdown phase, defensive or counter-cyclical sectors such as Health Care and Utilities tend to perform well

why is utility counter-cyclical?

energy is always needed, no matter how the economy is doing

additionally, since the uprise of open AI, a vast amount of energy is needed to power the plants

results in the industry to be even more counter-cyclical

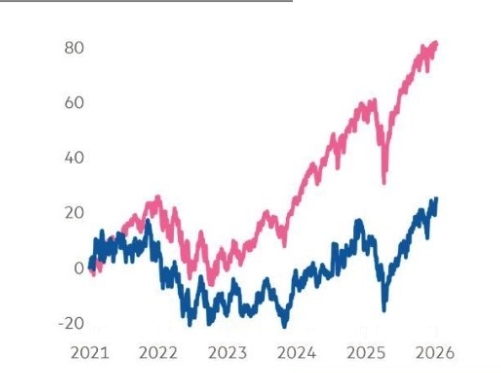

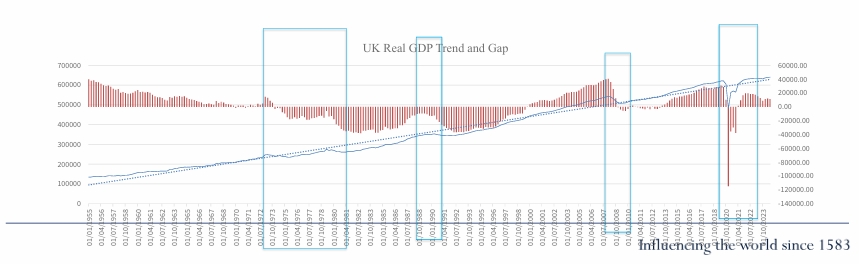

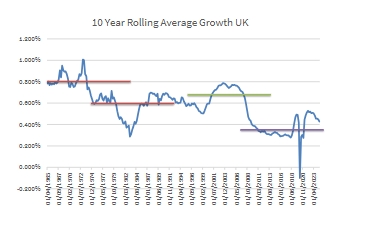

what does this graph show us?

shows that although there are some short-term fluctuations in output growth, real output will gradually drift up

emerging economies are growing faster than developed economies

factors such as innovation in AI and change in population structure are more important for long-term investment

short term noise such as Trump’s discussion about greenland won’t have major impact on long-term investment

it is only important if we are looking at short-term speculation

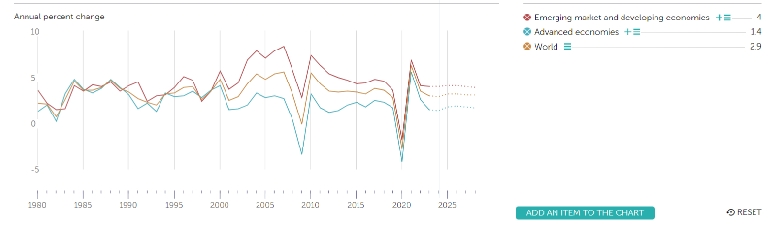

What does this graph show us?

it shows that over the long run, output tends to grow but long-term average growth rates has varied widely

eg in the 70s we had the oil price crash, resulting in lower growth

have to understand what ‘normal’ is to identify what is ‘abnormal’ and set realistic expectations

key assumptions of the solow growth model

the economy only produces a single output (goods)

there are diminishing returns to capital and labour

the economy has a constant savings rate and population growth rate

technology improves at a constant rate

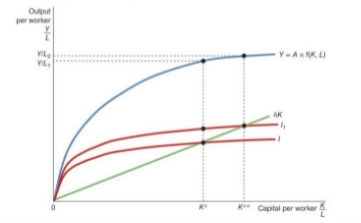

production function in the solow growth model

Y = output

function of capital and labour

K = capital

L = labour

A = productivity

it is a scaling factor that allows us to compare economies whose growth are determined by different factors (eg AI vs cultural)

f(k) = a function that represents how capital per worker is transformed into output per worker

assumes constant returns to scale

exhibits diminishing marginal returns to both capital and labour

production function describes how total output is generated from inputs of capital and labour

how can output be allocated, according to the solow model?

current output can be allocated for both saving and consumption in the following year

we can make into per-capita by dividing by total population

consumption brings us happiness but by saving, we will be able to consume more in the future

savings don’t just sit in the bank, they will be converted into investment

investment equation in solow mdoel

investment will always represent a proportion of the total output

investment will be converted into capital and can be used to produce more output in the future

net capital accumulation formula in solow model

the difference between investment and depreciation

as investment increases and the capital stock grows, depreciation rises proportionally, reducing the net rate of capital accumulation

is the value of capital constant?

no

once capital is built, their value gradually declines over time through depreciation

depreciation affects the entire existing capital stock, not just newly added capital

even when new investment occurs, older capital continues to lose value

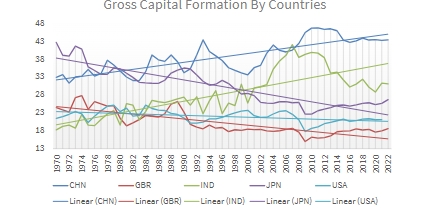

why do India and China experience growth through capital formation but not the UK, Japan, or the US?

China and India benefit as the initial capital stock was low, meaning depreciation was low

although at some point, they will face diminishing returns

comparing to the UK, US, and Japan, they had higher levels of initial capital stock meaning that their levels of depreciation were higher and they reached their steady state quicker

this is why they invest less heavily in infrastructure

what is the effect of higher levels of saving in an economy?

higher saving rate means that, for a given level of output, more resources are allocated to investment, leading to a higher equilibrium level of output

what is the effect of a declining working age population?

results in change in demand for goods

eg we may need fewer houses but more house carer services

what is the prediction of the solow model with higher levels of population?

an increase in the rate of population growth reduces the capital per worker, leading to a lower level of output per worker

on average, everyone will become poorer as the average output per worker drops

this is not entirely accurate though as we see in India and China that have very high levels of population but have not become poorer due to this

what can help to explain why the solow model prediction that higher population = poorer population is wrong?

differences in demographic structure can lead to different economic outcomes

ie the life-cycle hypothesis

a larger working-age population increases aggregate saving, and therefore investment, leading to higher levels of output

we would expect workers to save for retirement, large purchases such as a house etc

this results in investment to be positively associated with population

the structure of the population is a large determinant for investment

why do developed economies continue to experience growth, sometimes even at a faster rate than emerging markets?

economic development/productivity growth

change in productivity (A in the solow model) affects output per worker and therefore, living standards

higher level of A will scale all inputs up, resulting in higher levels of output

even if labour and capital is low, higher levels of productivity can result in higher levels of output

resources are allocated in a more efficient way

developed economies continue to grow mainly through technological progress

this is because if there is slow population growth, this constrains the labour input

additionally this constrains capital due to lower levels of investment

why is productivity not growing that fast in Europe?

could be due to EU regulations

what is an interesting insight on east Asian economies with productivity?

they are doing very well in terms of innovation which allows them to grow

they are unable to grow through labour due to low fertility rates

what increases labour productivity growth?

greater or higher-quality capital

more efficient use of labour and capital together

can look into changes in capital intensity and capital quality

how does AI affect the productivity of economies?

will result in different levels of productivity

a country’s access to new technologies will ultimately decides this

AI is now overtaking entry-level jobs, affecting graduates’ job prospects

possible reasons behind Britain’s productivity puzzle

chronic and road based under-investment

inadequate diffusion of productivity-enhancing practices between firms and places

institutional fragmentation and lack of joined-up policies

what is the effect of productivity on incomes?

low productivity growth = poorer economy

eg in the UK, productivity should be about 24% higher than it is today if it continued to follow its pre-crisis trend

this means that our salaries should be 24% higher

relationship between growth and corporate savings

some companies (earnings per share/EPS) have a higher correlation with domestic output than with global output

suggests that these countries are more self-sufficient and don’t need to rely on other countries

if EPS growth has higher correlation with global GDP, the country is driven more by exports

this means exposure to foreign markets will become important

corporate earnings and growth rates are highly correlated

corporate announcements can given an indication of future growth as companies tend to have forward-looking strategies

does high output = high stock return?

not really

Ritter (2025) found that there was no positive relationship between return and GDP growth

reasons behind this:

if increase in capital and labour inputs go into new corporations, these do not boost the present value of dividends on existing corporations

equity index does not directly capture new innovation, meaning that the relationship found may be subject to some measurement error

technological change does not increase profits unless firms have lasting monopolies, a condition that rarely occurs

countries with high growth potential do not offer good equity investment opportunities unless valuations are low

ex-ante vs ex-post (measuring relationship between output and stock returns)

output are lagged compared to the equity market

using ex-ante measure to forecast lagged variable doesn’t make sense

also we would be using the stock market to predict the output when we are wanting to use output to predict the stock market

expected return and realized return are different

expected returns are not observable; we can only estimate

eg using historical return or asset pricing model such as CAPM

realized return can be very different from the expected return

why is it important to understand the relationship between output and asset returns?

important from risk perspective: market tends to crash when the output crashes

helps us to understand the motivations of other market participants

unlike investors, who are mainly driven by returns, corporations tend to be more earnings-driven

policy markets care about output, and their policies will influence investment decisions

eg if output has been low for a long time, policy makers will make some effort to increase investment incentives to increase output

builds a foundation for global asset allocation

helps us to understand the consensus view and, therefore, market sentiment

are new technologies/innovation captured in equity index?

no

this is because new innovative firms are relatively small whereas the equity index captures mature firms

can explain why we don’t see the positive relationship between equity return and GDP empirically

why did the price of gold/silver drop at the end of january?

due to Trump’s announcement of the new Fed head

shows how much of an influence news about central banks have on financial market

the announcement removed some uncertainty, which had previously led to an increase in prices of gold and silver

additionally, Warsh (new nominee) is seen as hawkish

interest rates and price of gold typically move in opposite directions

this means that price of gold is likely to be low for a while as he increases interest rates

key functions of the central bank

issuing currency

sole authority

responsible for issuing banknotes and coins

banker to the government

manages government accounts and public debt

regulating banks

supervises and regulates commercial banks to ensure financial stability

implementing monetary policy

controls the money supply and interest rates to influence economic activity

dual mandate of Federal Reserve

two main objectives: to promote maximum employment and ensure price stability

output is NOT an objective

maximum employment

refers to the highest level of employment an economy can achieve without triggering an acceleration in inflation

need to strike a balance

although higher wage increases welfare, it will result in wage-price spiral inflation

price stability

defined as maintaining a low and stable rate of inflation over an extended period

eg the Fed aims for an inflation rate of around 2%

however, they don’t adjust the policy so frequently as they look over the long-run horizon

eg if for one quarter there is low inflation but in the next quarter there is high inflation, as long as on average it is around 2%, the policy won’t change

summary of Fed’s mandate

promote price stability and maximum employment (dual mandate)

moderate long-term interest rates

summary of BoE’s mandate

maintain price stability (inflation target set by government)

support economic policy (including growth and employment)

oversee financial stability

summary of Bank of Japan (BoJ)’s mandate

achieve price stability (around 2% inflation over medium/long term)

contribute to financial system stability

summary of European Central Bank (ECB)’s mandate

primary objective: maintain price stability (~2% inflation target)

secondary objective: support general economic policies of the EU (eg growth, employment)

summary of People’s Bank of China (PBoC)’s mandate

maintain stability of the RMB’s (Renminbi - chinese currency) value

carry out monetary policy under state council direction

promote economic growth and financial stability

difference in mandates for BoE and Fed

inflation is the priority for BoE

inflation AND employment are equally as important for the Fed

how is the People’s Bank of China different to most central banks?

it is not independent

decisions are made at state council level

this makes it more complicated but the policies taken by the bank will be more aligned to the government’s policies

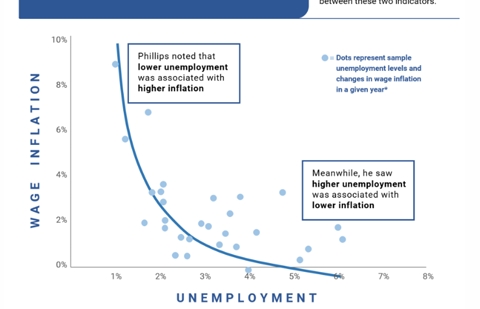

what does the phillips curve illustrate?

it illustrates the negative relationship between unemployment and inflation

intuition: a lower unemployment rate means people are working, increasing demand for labour

puts upward pressure on wage so firms raise prices for their products

never a linear relationship

a one percentage difference in unemployment makes a more than proportionate change in inflation

this makes it more difficult for central banks (especially the Fed with their dual mandate) to create optimal policies

as unemployment increases, it has less of an impact on price levels

it’s not until it decreases to around 4% where we see a large impact on price levels

this is when central bankers will become more hawkish as they know having this price level is unsustainable

in what way does the Fed have a triple mandate?

although it isn’t an explicit mandate, the Fed plays a key role in stabilizing financial markets during crises

eg in March 2023, stress in the US banking system following problems at Silicon Valley Bank promoted the Fed to intervene

the Fed stopped what they were doing to help support the financial market in the short run

despite ongoing rate hikes and quantitative tightening, the ed introduced the Bank Term Funding Program (BTFP) to inject liquidity, leading to a temporary expansion of its balance sheet

key features of Bank Term Funding Program (BTFP)

offered loans of up to one year to banks

institutions could use US treasury bonds and other high-quality collateral as securities for loans, valued at par

avoided banks selling these securities in times of financial stress

program aimed to provide liquidity to financial institutions, helping them meet the needs of depositors and stabilize the banking sector during periods of uncertainty

introduce in March, 2023 in response to the banking crisis

objectives of the Federal Open Market Committee

promote maximum employment, price stability, and moderate long-term interest rates

makes key decisions on interest rates and the US money supply

importance of an independent central bank

the Fed sets the risk-free rate, which serves as the anchor for asset prices

unlike the executive branks, the Fed is not subject to elections

can lead to tensions between the Fed and the President

while the President nominates both Fed Governors (14-year terms) and the Chair (4-year term), any loss of credibility would be disastrous

there isn’t an actual limit to the Chair

ie, you could re-elect the same Chair after the 4 years was up