Looks like no one added any tags here yet for you.

accounting cost

actual expenses plus depreciation charges for capital equipment

economic cost

cost to a firm of utilizing economic resources in production, including opportunity cost

opportunity cost

cost associated with opportunities that are forgone when a firm’s resources are not put to their best alternative use

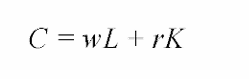

Total Cost (TC or C)

total economic cost of production, consisting of fixed and variable costs

Fixed Cost (FC)

cost that does not vary with the level of output and that can be eliminated only by shutting down

Variable Cost (VC)

cost that varies as output varies

What is the only way that a firm can eliminate its fixed costs?

shutting down

Shutting Down

does not necessarily mean going out of business

through reduction of output to zero, the company could eliminate the costs of raw materials and much of labor

How to know which costs are fixed and which are variable?

in a short time horizon (few months), most costs are fixed

in a long time horizon (ten years), nearly all costs are variable

Sunk costs

costs that have been incurred and cannot be recovered

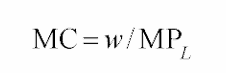

Marginal Cost (MC)

increase in cost resulting from the production of one extra unit of output, since fixed cost does not change as the as the firm’s level of output changes

Marginal Cost Equation

Average Total Cost (ATC)

firm’s total cost divided by its level of output

Average Fixed Cost (AFC)

fixed cost divided by the level of output

Average Valuable Cost (AVC)

variable cost divided by the level of output

MC from variable costs (VC) Formula

Marginal Cost in terms of labor productivity

Diminishing Marginal Returns and Marginal Cost

DMRS means that marginal product of labor declines as the quantity of labor employed increases.

As a result, when there are diminishing marginal returns, marginal cost will increase as output increases

User cost of Capital

annual cost of owning and using a capital asset, equal to economic depreciation plus forgone interest

User Cost of Capital Formula

User cost of capital as a rate per dollar of capital formula/ price of capital

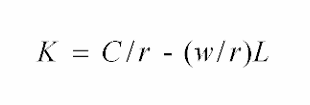

Isocost Line

graph showing all possible combinations of labor and capital that can be purchased for a given total cost

Total Cost Formula:

Isocost curves describe?

the combination of inputs to production that cost the same amount to the firm

Total Cost Equation for a straight line

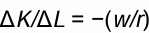

Isocost Line Slope Formula

*the ratio of the wage rate to the rental cost of capital

When the price of labor increase, the isocost curves become?

steeper

Marginal Rate of Technical Substitution of Labor Formula

*follows when a firm minimizes the cost of producing a particular output

Cost Minimization Condition/ Optimal Combination of Outputs

expansion path

curve passing through points of tangency between a form’s isocost lines and its isoquants

Steps to moving expansion path to cost curve

choose output level represented by an isoquant, then find the point of tangency of that isoquant with an isocost line

from chosen isocost line, determine minimum cost of producing output level that has been selected

graph output-cost combination

long-run average cost curve (LAC)

curve relating average cost of production to output when all inputs, including capital, are variable

short-run average cost curve (sac)

curve relating average cost of production to output when level of capital is fixed

long-run marginal cost curve (lmc)

curve showing the change in long-run total cost as output is increased incrementally by 1 unit

Reasons as to why firm’s average cost of producing output is likely to decline when output increases

if firm operates on larger scale, workers can specialize in activities where they are most productive

scale can provide flexibility. by varying combination of inputs utilized to produce the firm’s output, managers can organize production process more efficiently

firm may be able to acquire some production inputs at lower cost via buying in large quantities, thereby negotiating better prices. mix of inputs may change with the scale of firm’s operations if managers take advantage of lower-cost inputs

Reasons for shift explaining that average cost of production may begin to increase with output:

(at least in short run) factory space and machinery may make it more difficult for workers to do their jobs effectively

managing a larger firm may become more complex and inefficient as number of tasks increase

advantages of buying in bulk may have disappeared once certain quantities are reached. at some point, available supplies of key inputs may be limited, pushing their costs up

economies of scale

wherein output can be doubled for less than a doubling of cost

diseconomies of scale

wherein doubling of output requires more than a doubling of cost

increasing returns to scale

output more than doubles when the quantities of all inputs are doubled

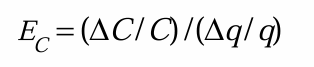

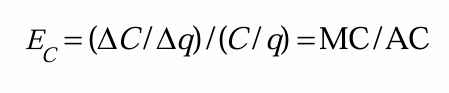

Economies of Scale Formula

Economies of Scale relating to traditional measures of cost formula: