AP Macroeconomics Unit 1: Basic Economic Principles

1/39

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

40 Terms

Scarcity

When the world has unlimited wants but we have limited resources. (one of the most important parts of economics)

Economics

The study of how individuals and societies allocate scarce resources to best satisfy unlimited wants and needs.

Macroeconomics

The study of a whole economy, aka country-level. (e.g, Economic growth, inflation, trade)

Positive statements vs. Normative statements

Positive statements are objective and fact-based, while normative statements are subjective and based on opinions or beliefs.

The 5 Key Economic Assumptions

People have unlimited wants and limited resources.

People make choices by weighing marginal costs and benefits.

People will do things in their self-interest (rational behavior).

All choices involve trade-offs.

Any real-life situation can be explained with simplified models and graphs.

Opportunity cost

The value of the next best alternative that is forgone when making a choice. This is a trade off. Such choices are made after marginal analysis.

The 4 Factors of Production

The 4 factors are:

Land - the natural resources used to produce goods and services (water, sunlight, animals)

Labor - the efforts people devote to a task and get paid for it (cashiers, doctors, servers)

Capital - there are two types of capital: physical (any human-made resources that creates other products, such as a tractor) and human (any skills or knowledge gained from education/experience)

Entrepreneurship - the risks people take that combine the other factors of production to create new products (Steve Jobs, Jeff Bezos)

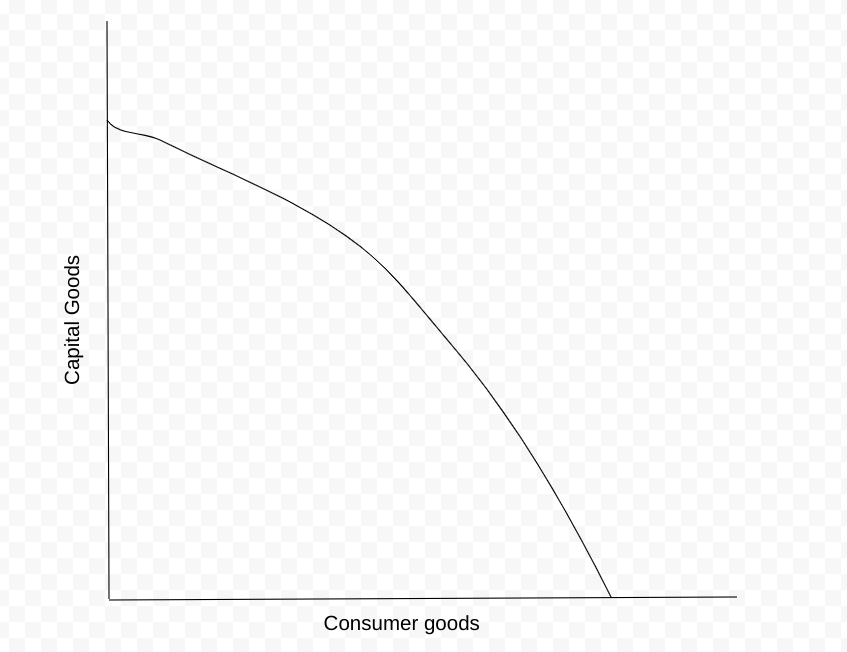

The Production Possibilities Curve/Frontier

A model that shows how an economy will use its resources. It demonstrates scarcity, trade offs, opportunity costs, and efficiency.

The 4 Assumptions of the PPC

Only two goods can be produced (capital and consumer).

All resources are fully used.

Resources are fixed (ceteris paribus)

Technology is fixed

Ceteris Paribus

A Latin phrase meaning “all things held constant”. It is commonly used by economists when describing situations.

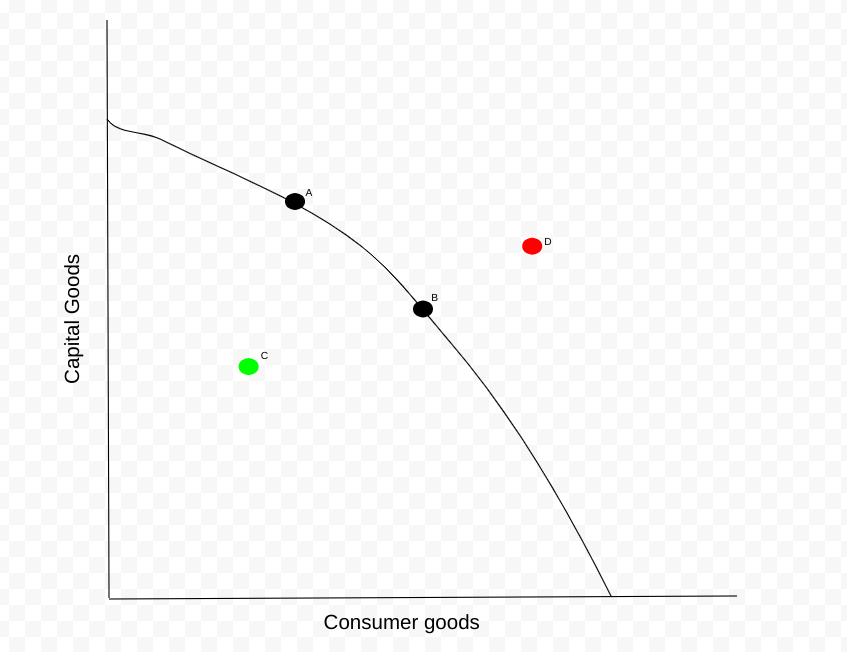

On the PPC, when is the economy at…

Full employment/utilization: On the curve itself (A and B)

Little employment/inefficient: Inside the curve (C)

More-than-full employment/impossible: Outside the curve (D)

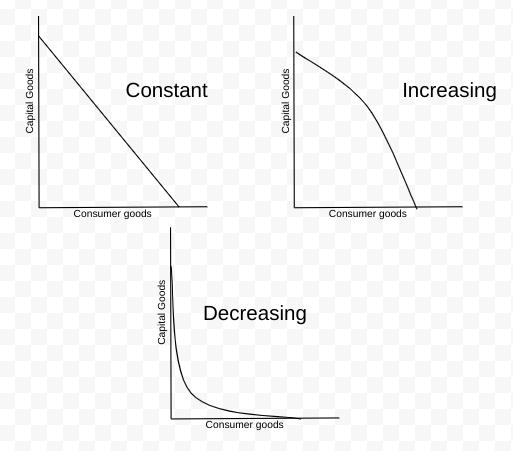

Different types of PPC curves

Constant: A straight line, the relationship is proportional

Increasing: A concave (bulging) curve, the opportunity cost increases with more of a product

Decreasing: A convex (caved-in) curve, the opportunity cost decreases with more of a product

PPC shifters

Change in resource quantity/quality

Change in technology

Change in trade

When the PPC shifts out…

It’s a sign of economic growth!

More resources/quality increases

Better technology

More trade

One “axis” of the PPC may shift, it’s almost always the consumer product. (e.g, pizza when there are more pizza-making machines)

If a country focuses on capital goods, their economic growth will be more than those that focus on consumer goods.

When the PPC caves in…

It’s a sign of economic contraction

Less resources/quality decreases

Technology is destroyed

Less trade

Absolute vs Comparative advantage

Absolute advantage happens when a country can produce more of a product numerically.

Comparative advantage happens when a country can produce a good with the least opportunity cost.

Calculating per unit opportunity cost

Opportunity cost / Units gained

Output vs input questions

Output questions focus on the amount of things produced in a set period of time. (Other product goes over)

Input questions focus on the amount of time used to produce a product. (Other product goes under)

Terms of trade

The agreed-upon conditions of trade that benefit both countries.

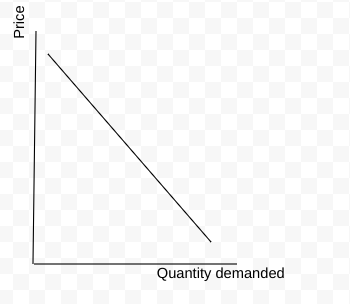

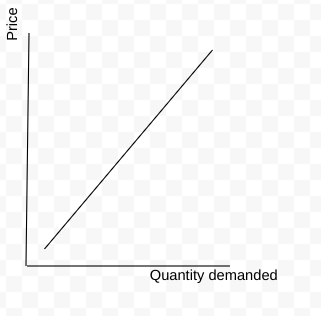

Demand

The different quantities of goods that consumers will buy at different prices.

Price on y-axis, quantity demanded on x-axis

The Law of Demand

An inverse relationship between price and quantity demanded.

The Three Reasons Law of Demand Occurs are:

The substitution effect

The income effect

Law of Diminishing Marginial Utility

The Substitution Effect

If the price goes up for one product, consumers will generally shift their spending to a substitute product.

(e.g, Coke and Pepsi)

The Income Effect

When the price of a product goes down, or someone’s income goes up, then consumers will purchase more of that product (and vice versa).

Law of Diminishing Marginal Utility

As you consume anything, the satisfaction you receive will start to decrease after some time.

Determinants of Demand

Taste and Preferences

Number of consumers

Price of related goods (substitutes)

Income

Future expectations

Complement

Two goods that are usually used together. If the price of one product increases, usually both products will be bought more.

(e.g, dry-erase marker and whiteboard.

Normal vs. inferior goods

Normal goods: As income increases, so does demand. (e.g, luxury cars, houses)

Inferior goods: As income increases, demand decreases. (e.g, used books, instant noodles)

Change in Quantity Demanded vs Change in Demand

Quantity demanded refers to a position on the curve. The change is usually caused by price. Demand refers to the whole curve. The change is caused by the determinants of demand.

Supply

The different quantities of a good that sellers are wanting to sell at different prices.

Once again, price is the y-axis and quantity supplied is the x-axis.

Law of Supply

There is a direct (positive) relationship between price and quantity supplied.

Determinants of Supply

Price/availability of inputs (includes workers)

Number of sellers

Technology

Government action (giving taxes and subsidies)

Expectations of future profit

Quantity supplied vs Supply

Quantity supplied refers to a position on the curve, and is often caused by change in price. Supply refers to the whole curve and is caused by the determinants of supply.

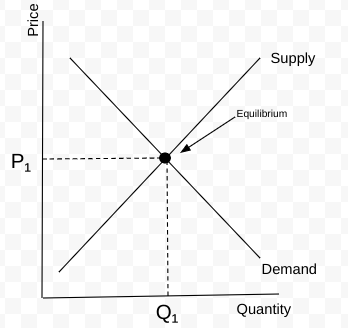

The supply and demand graph

Any point above the equilibrium is considered surplus.

Any point below the equilibrium is considered shortage.

Shortage

When quantity demanded is greater than quantity supplied.

Surplus

When quantity demanded is less than quantity supplied.

Free Market System

The “invisible force” that pushes prices towards equilibrium.

Double shift rule

If two curves shirt at the same time, price or quantity will be indeterminate.

Price ceiling

The maximum legal price a seller can charge for a product to make it affordable for everyone. (black market ceiling is low)

Price floor

The minimum legal price a seller can sell a product.