Savings by Government

Savings by Government = Tax Revenues - Government Purchases of Goods and Services - The Value of Government Transfers

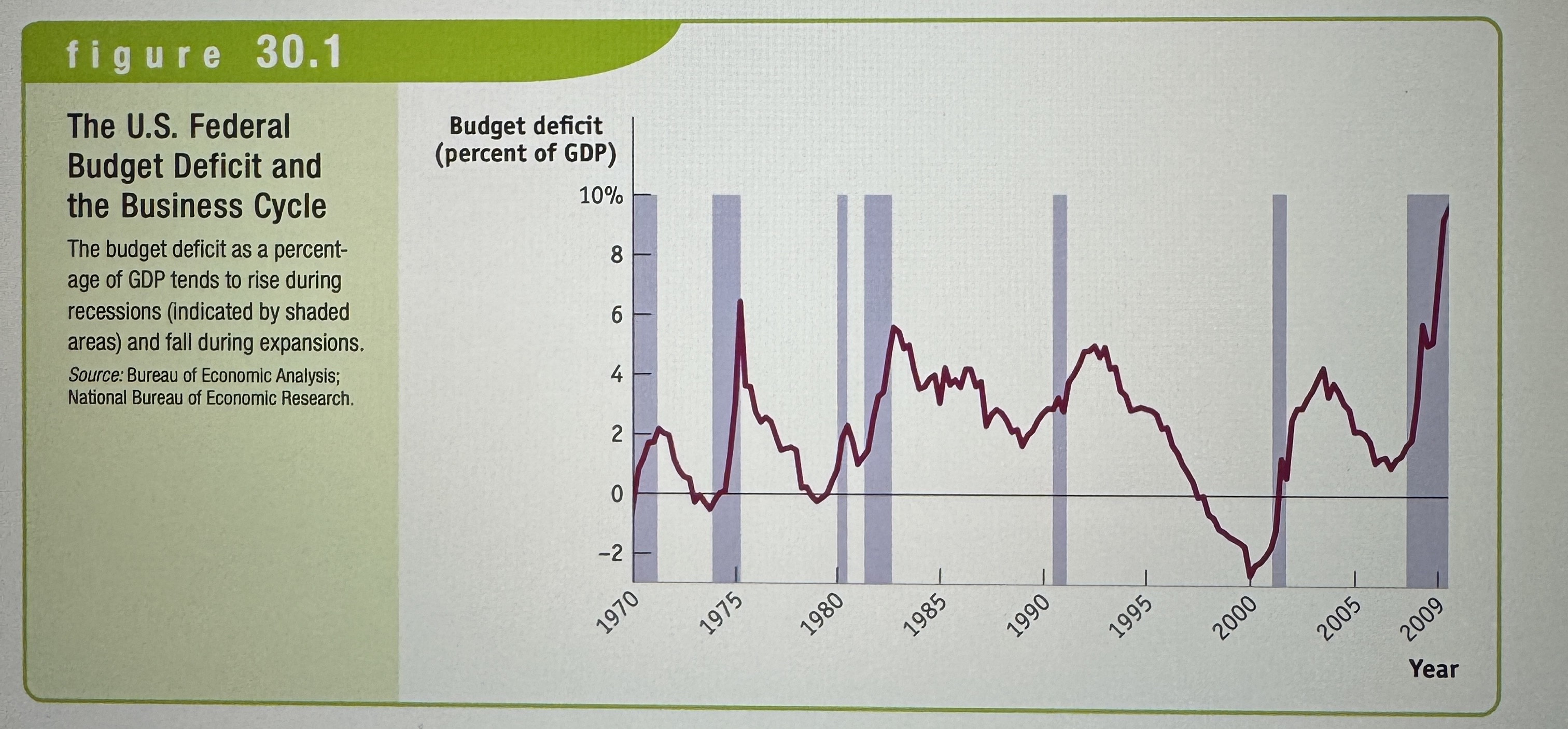

The U.S. Federal Budget Deficit and the Business Cycle

Ex.

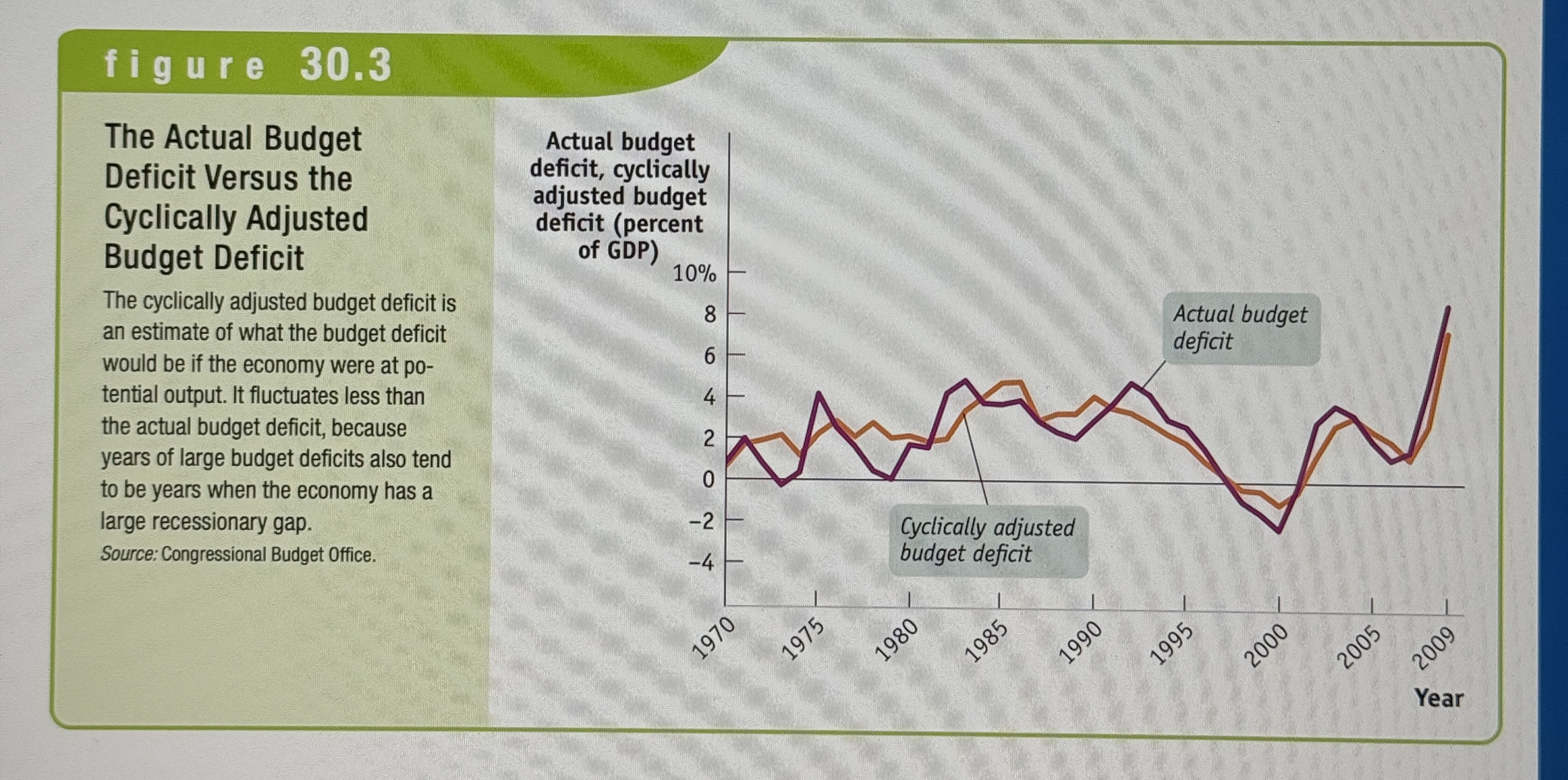

Cyclically adjusted budget balance

An estimate of what the budget balance would be if real GDP was exactly equal to potential output.

The U.S. Federal Budget Deficit and the Unemployment Rate

Ex.

The Actual Budget Deficit Versus the Cyclically Adjusted Budget Deficit

Ex.

Fiscal Year

Runs from October 1 to September 30 and is labeled according to the calendar year in which it ends.

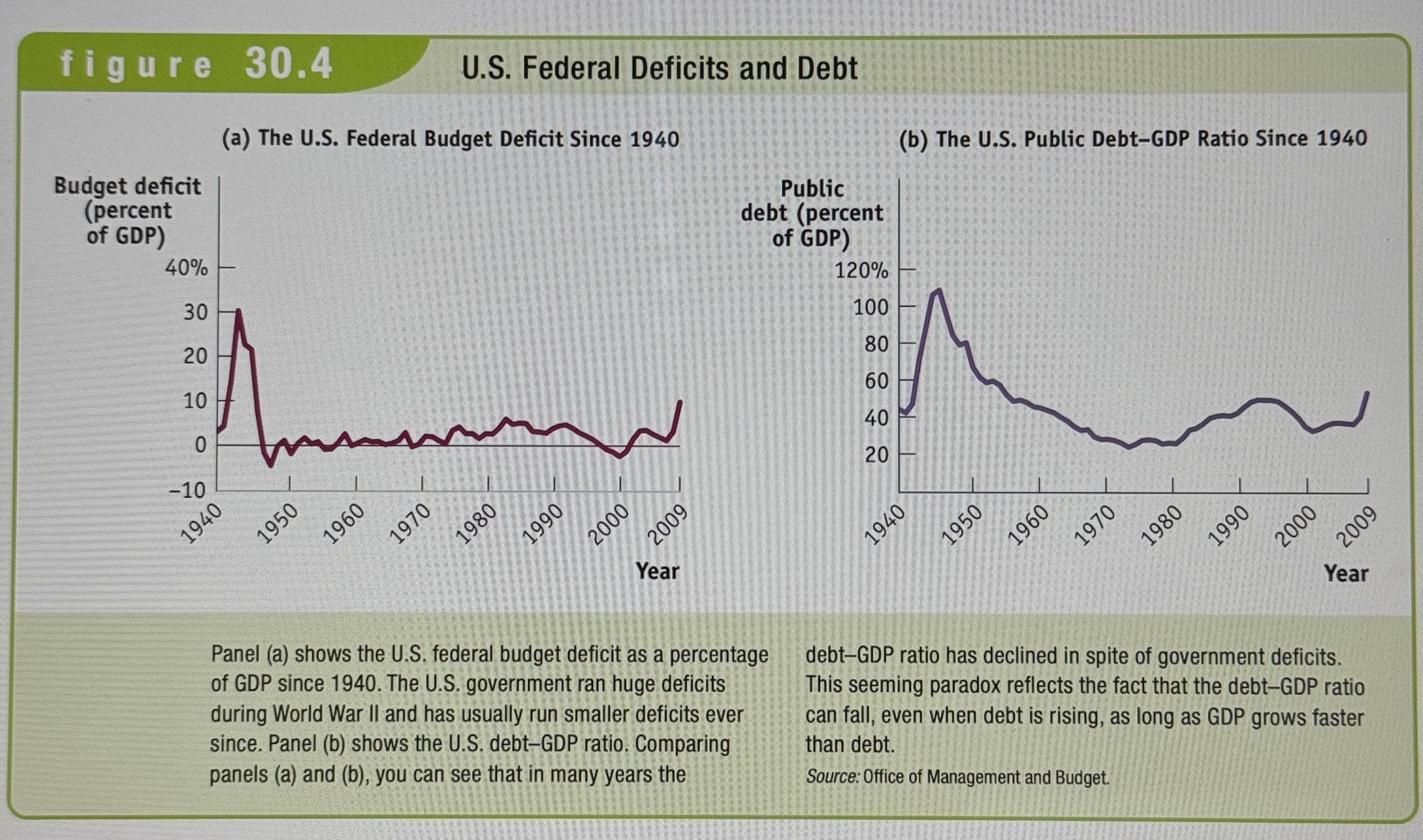

Public Debt

Government debt held by individuals and institutions outside the government.

debt-GDP Ratio

The government’s debt as a percentage of GDP.

U.S. Federal Deficits and Debt

Ex.

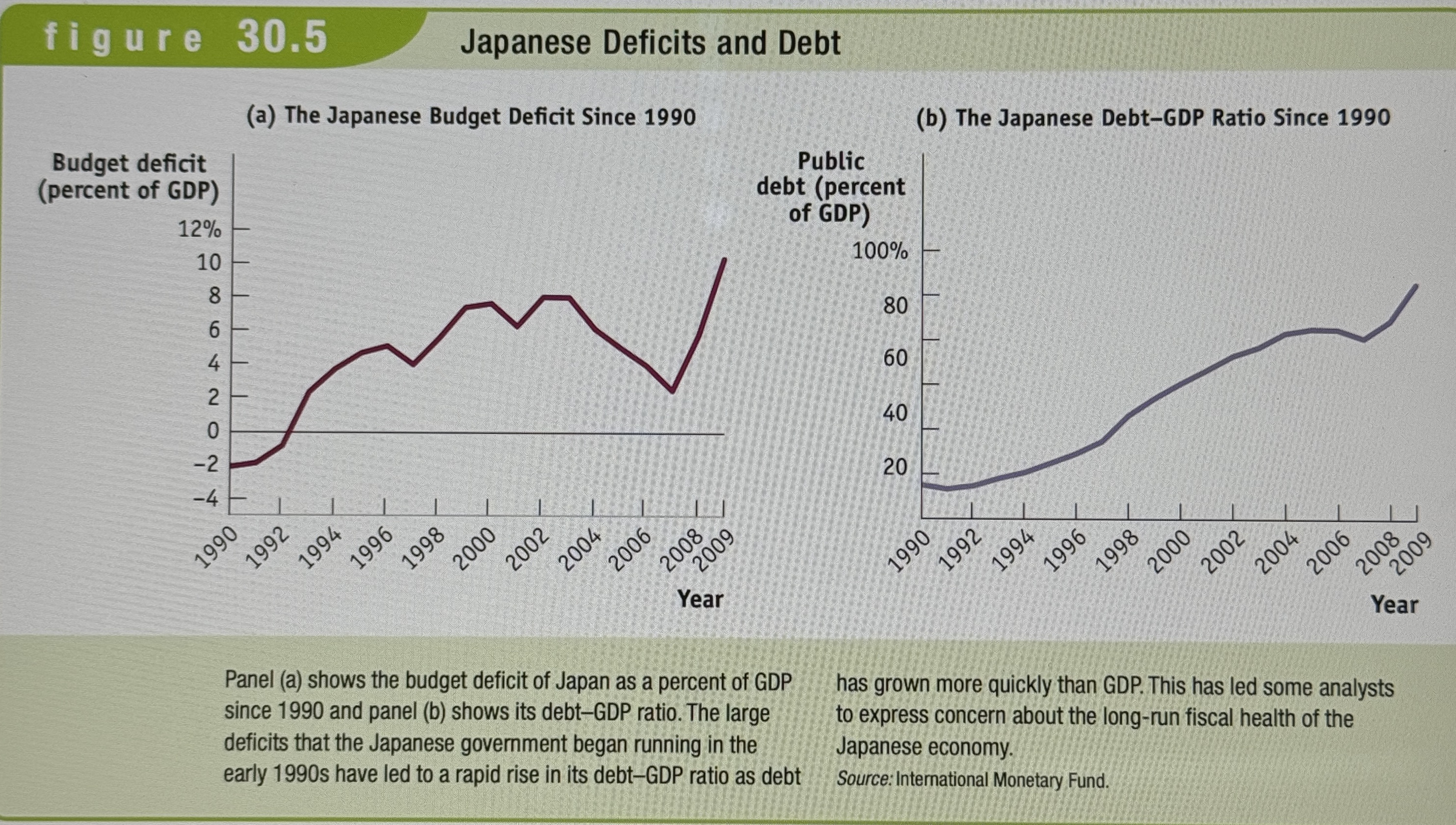

Japan Federal Deficits and Debt

Ex.

Implicit liabilities

Spending promises made by governments that are effectively a debt despite the fact that they are not included in the usual debt statistics. Ex. Social Security and Medicare

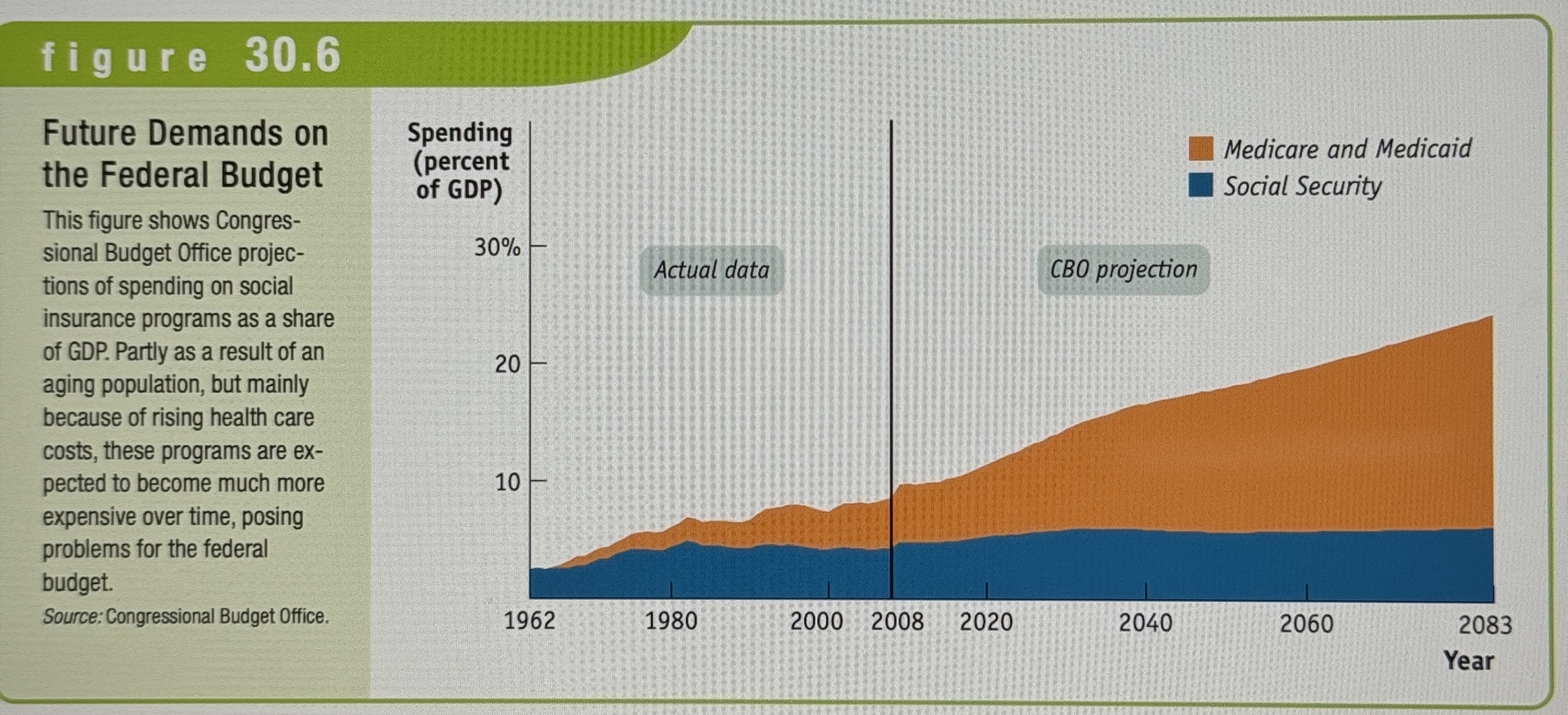

Future Demands on the Federal Budget

Ex.

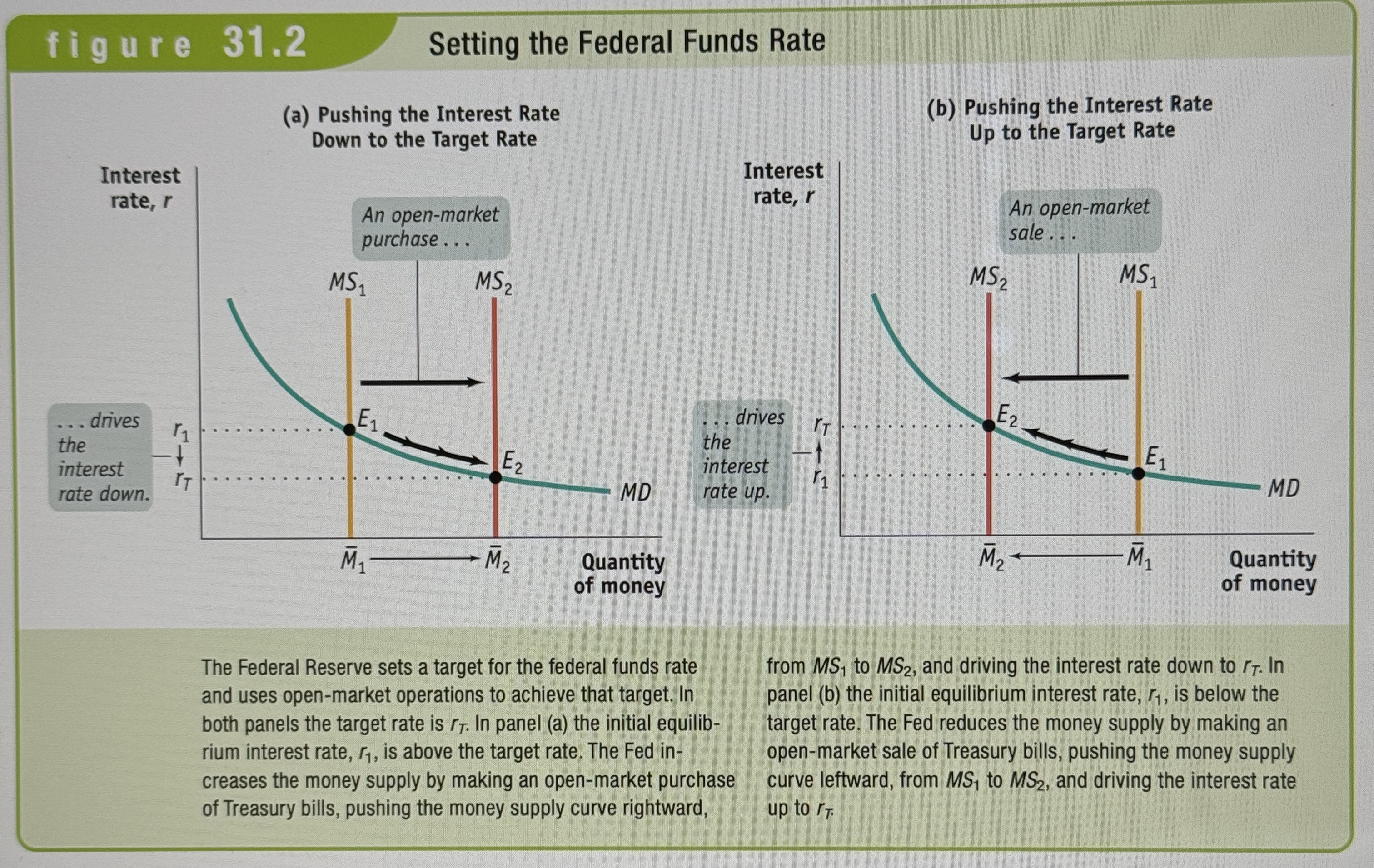

The Target Federal Funds Rate

The federal reserve can move the interest rate through open market operations that shift the money supply curve. In practice, the FED sets a target federal funds rate and uses open market operations to achieve that target.

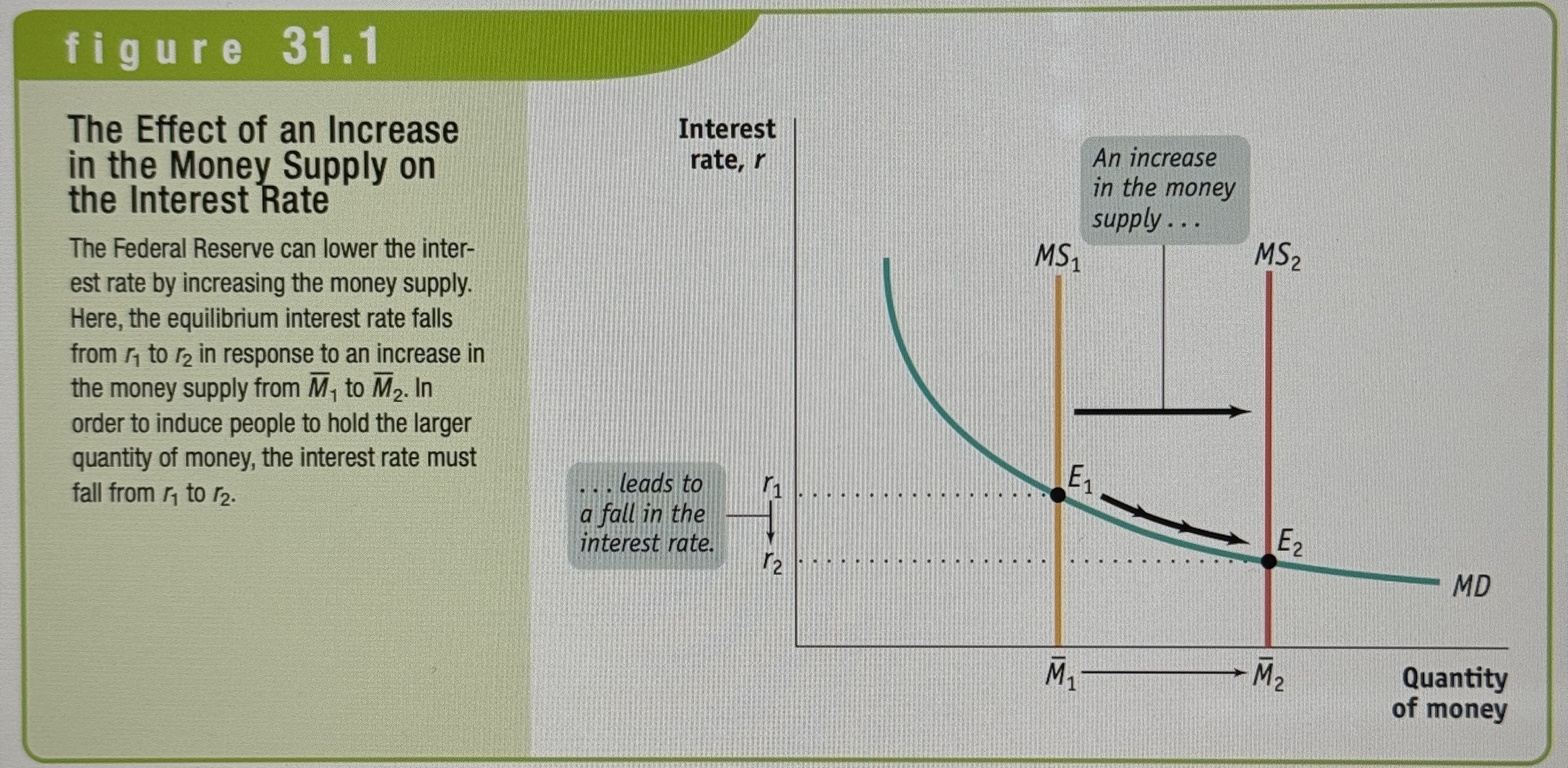

The Effect of an Increase in the Money Supply on the Interest Rate

Ex.

Setting the Federal Funds Rate

Ex.

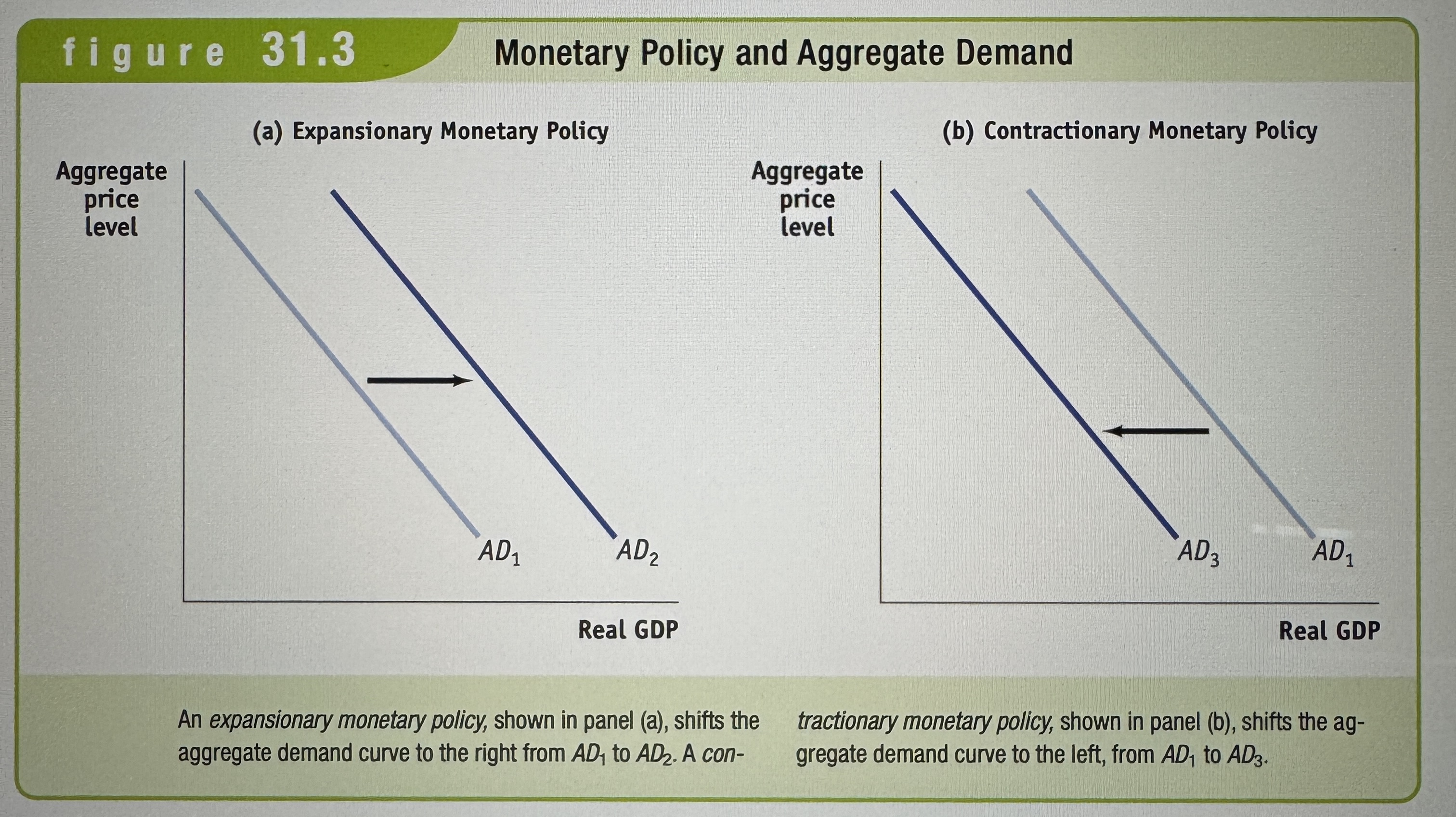

Expansionary monetary policy

Monetary policy that increases aggregate demand.

Contractionary monetary policy

Monetary policy that reduces aggregate demand.

Monetary policy and aggregate demand

Ex.

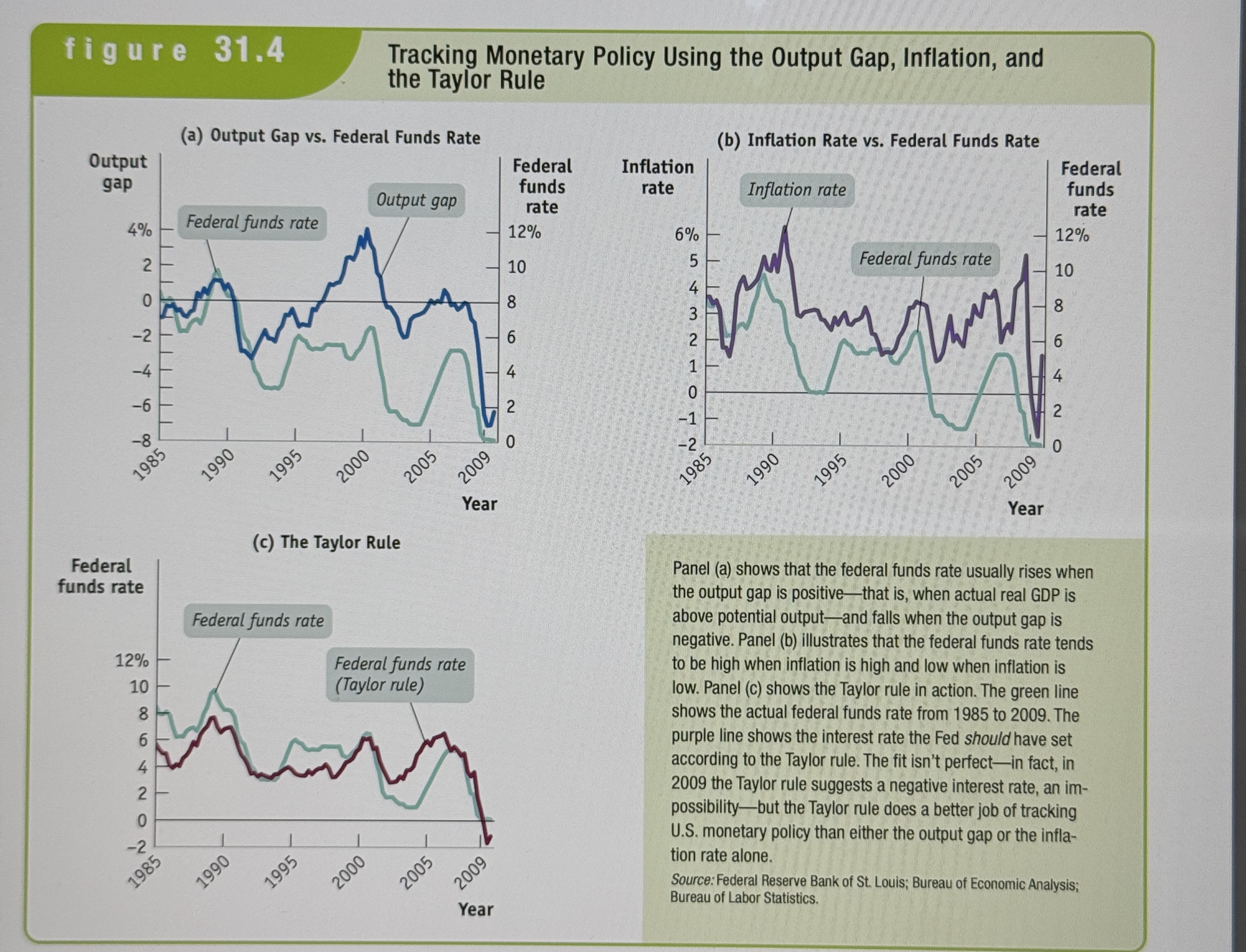

Tracking Monetary Policy Using the Output Gap, Inflation, and the Taylor Rule

Ex.

The Taylor rule for Monetary Policy

A rule for setting the federal funds rate that takes into account both the inflation rate and the output gap.

Inflation Targeting

Occurs when the central bank sets an explicit target for the inflation rate and sets monetary policy in order to hit that target.

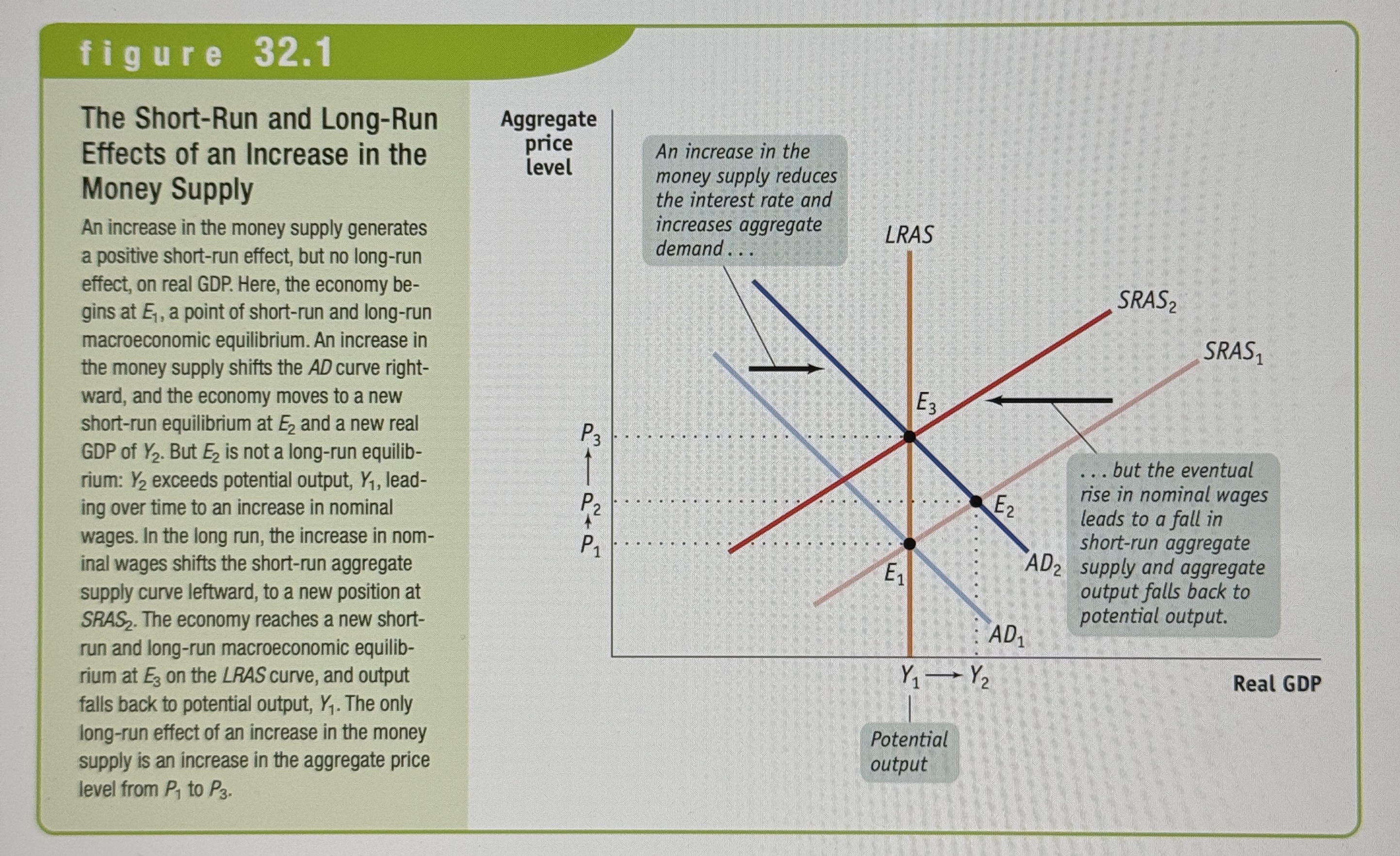

The Short-Run and Long-Run Effects of an Increase in the Money Supply

Ex.

Monetary neutrality

According to this concept changes in the money supply have no real effect on the economy.

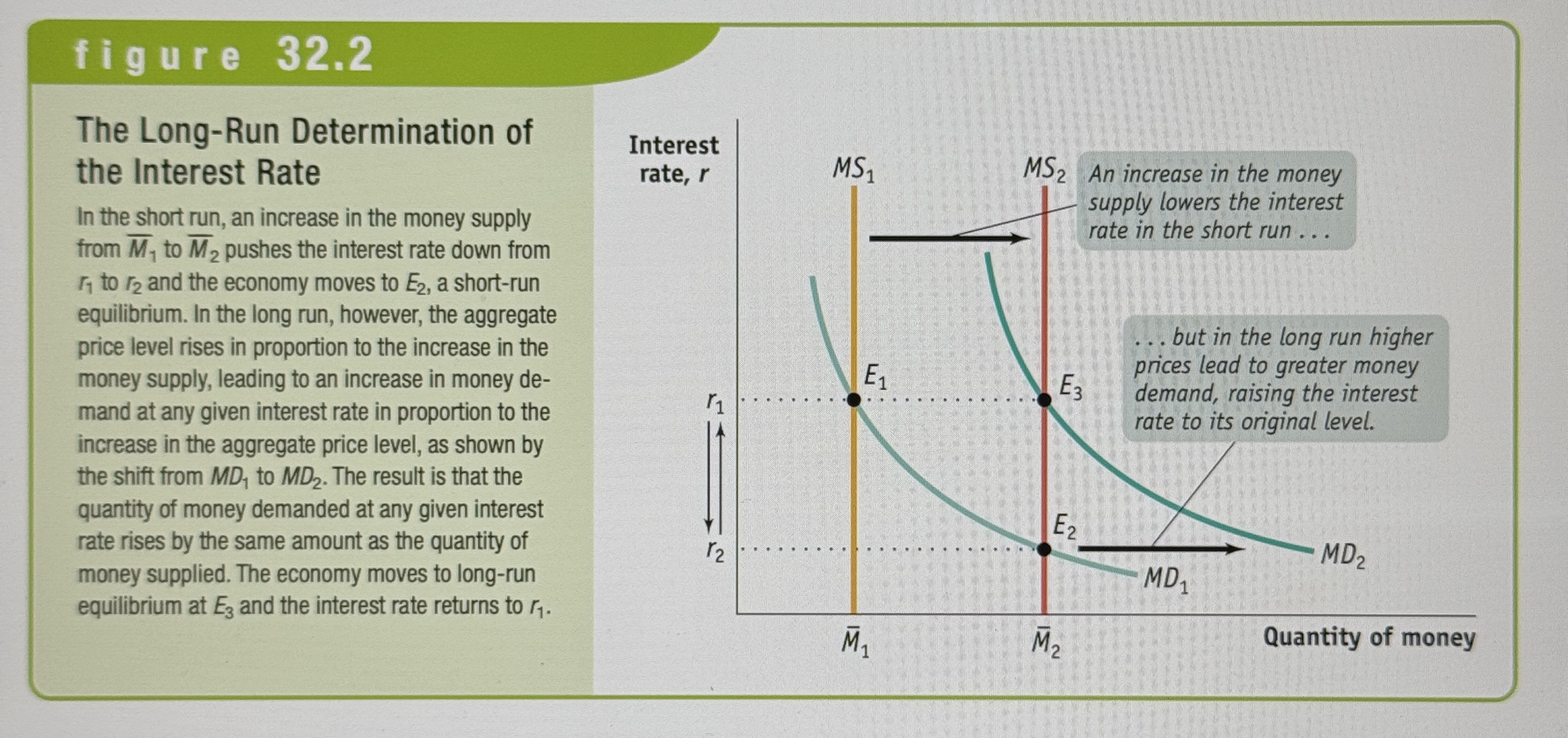

The Long-Run Determination of the Interest Rate

Ex.

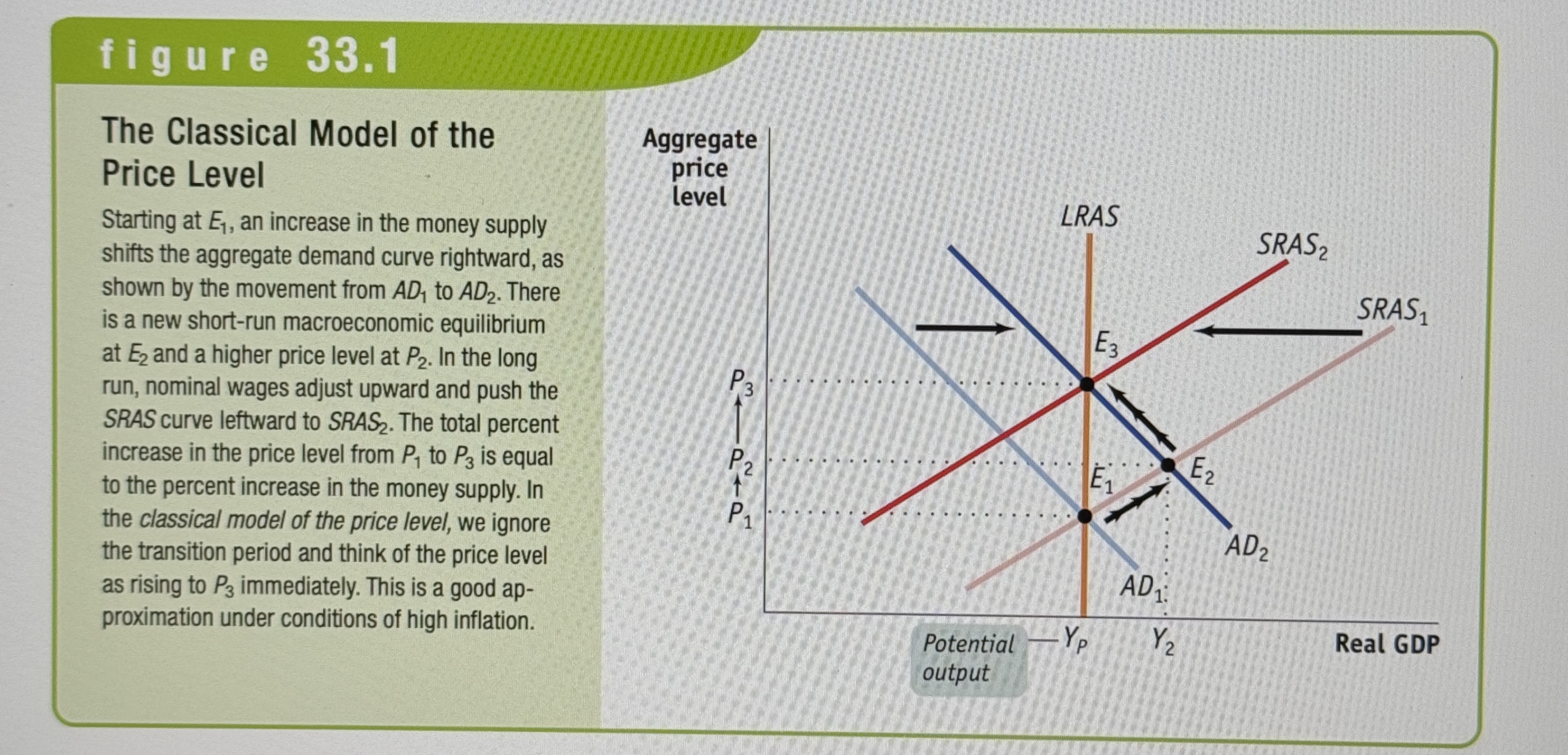

The classical model of the price level

The real quantity of money is always at its long run equilibrium level.

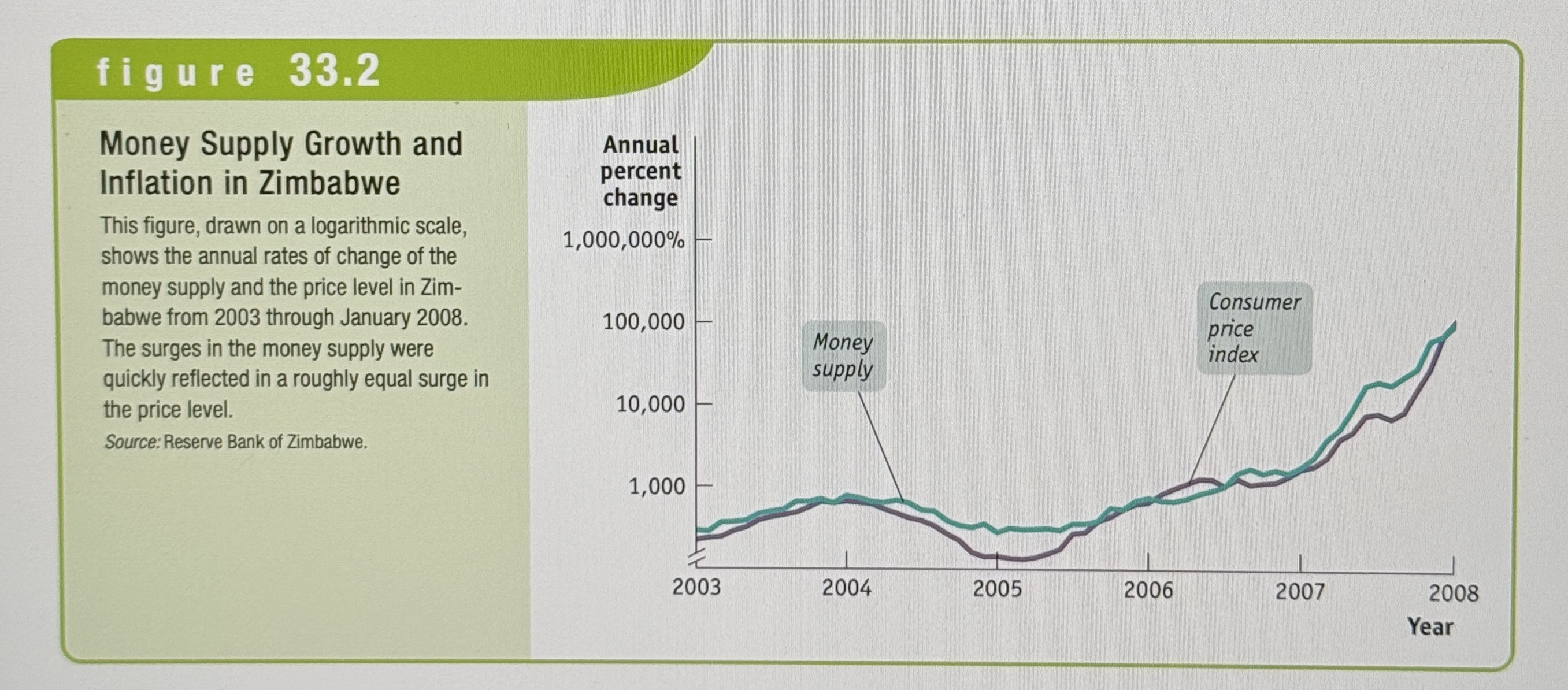

Money Supply Growth and Inflation in Zimbabwe

Ex.

Inflation Tax

A reduction in the value of money held by the public caused by inflation.

Real Seignorage

Real Seignorage = Rate of Growth of the Money Supply * Real Money Supply

Cost-push inflation

Inflation that is caused by a significant increase in the price of an input with economy wide importance.

Demand pull inflation

Inflation that is caused by an increase in aggregate demand.

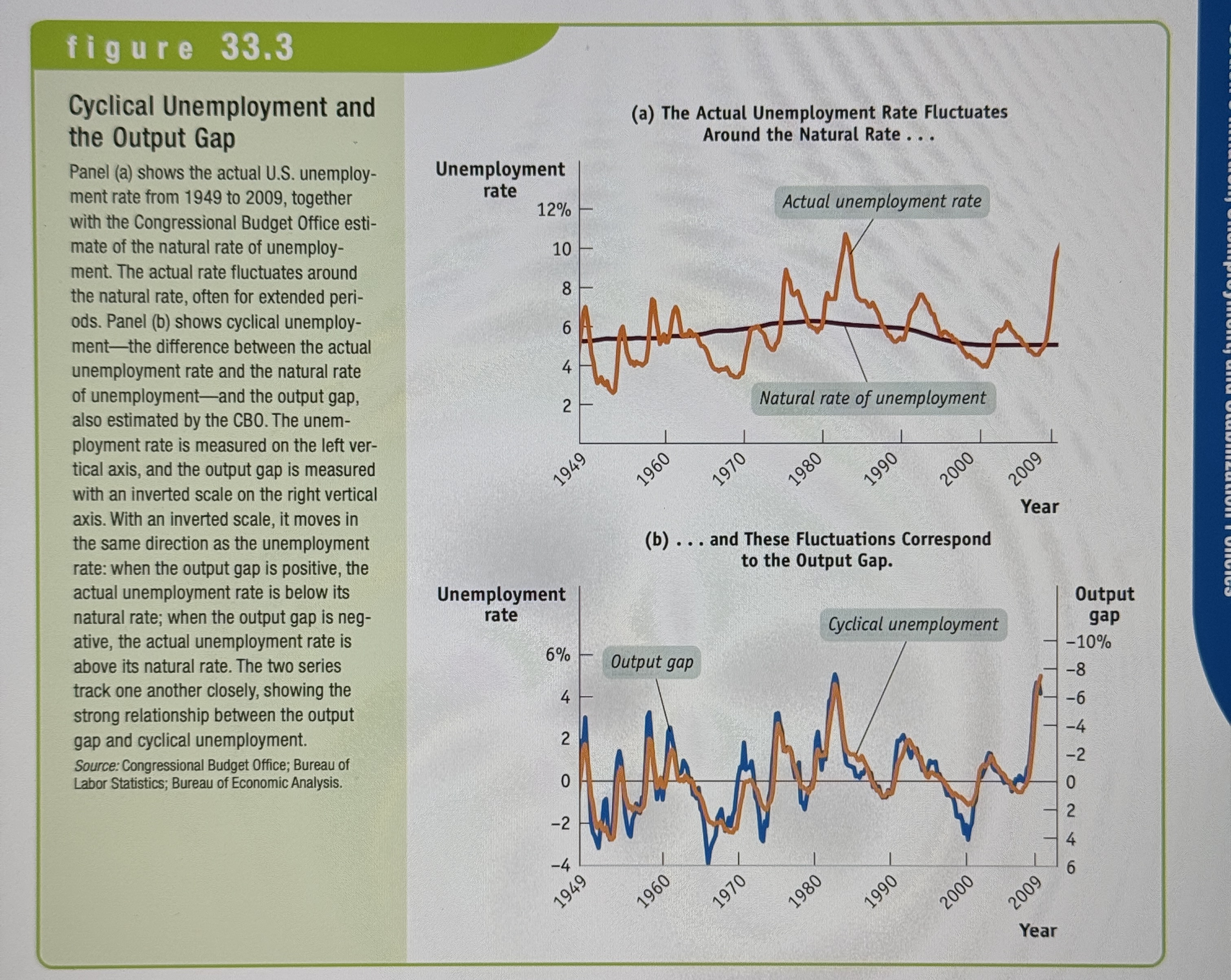

Cyclical Unemployment and the Output Gap

Ex.

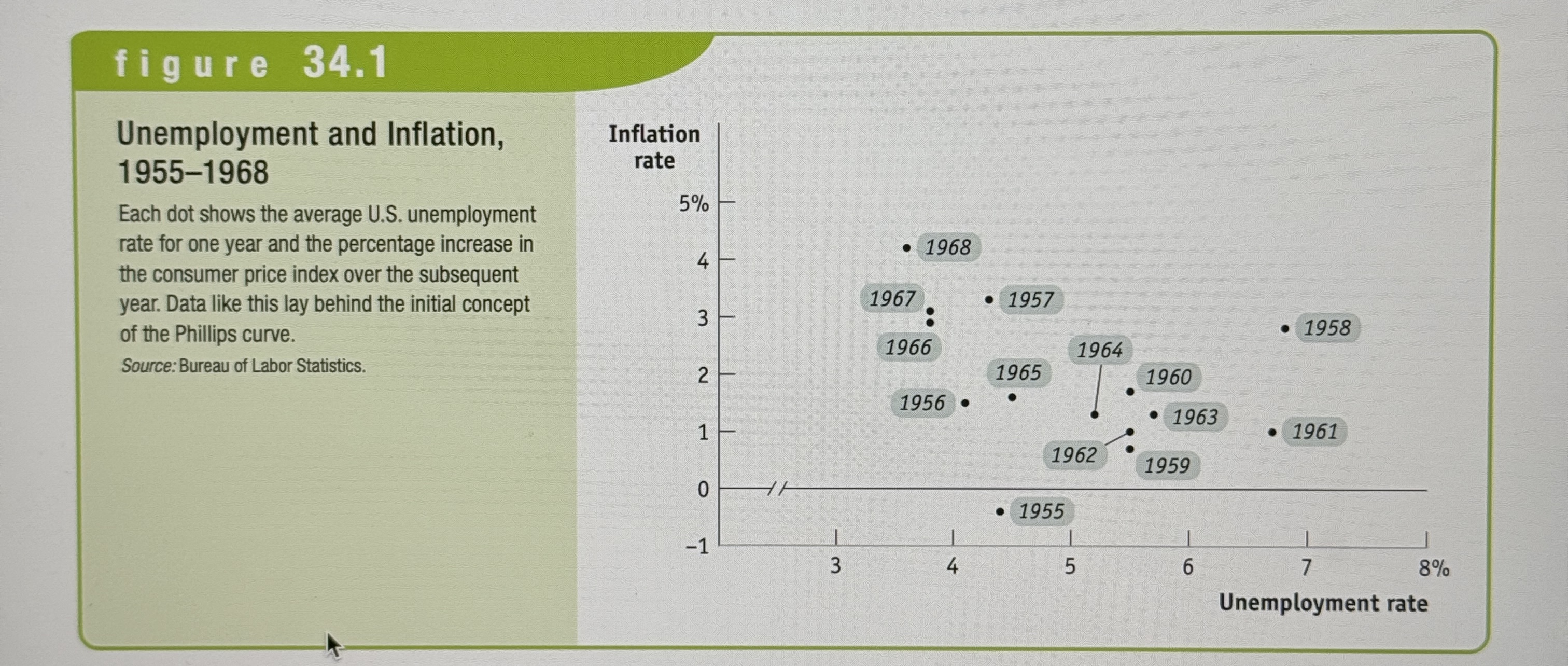

Unemployment and Inflation, 1955-1968

Ex.

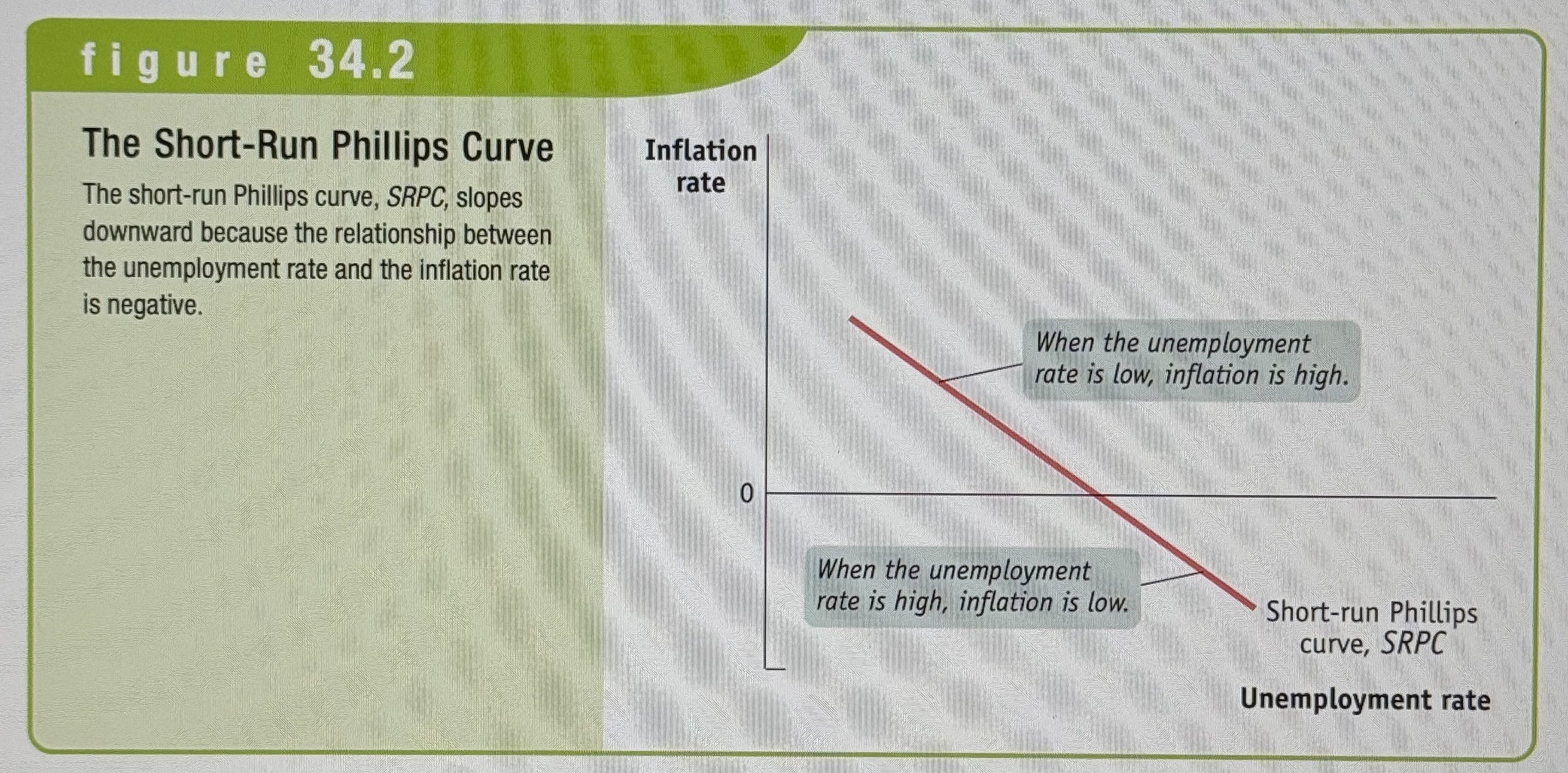

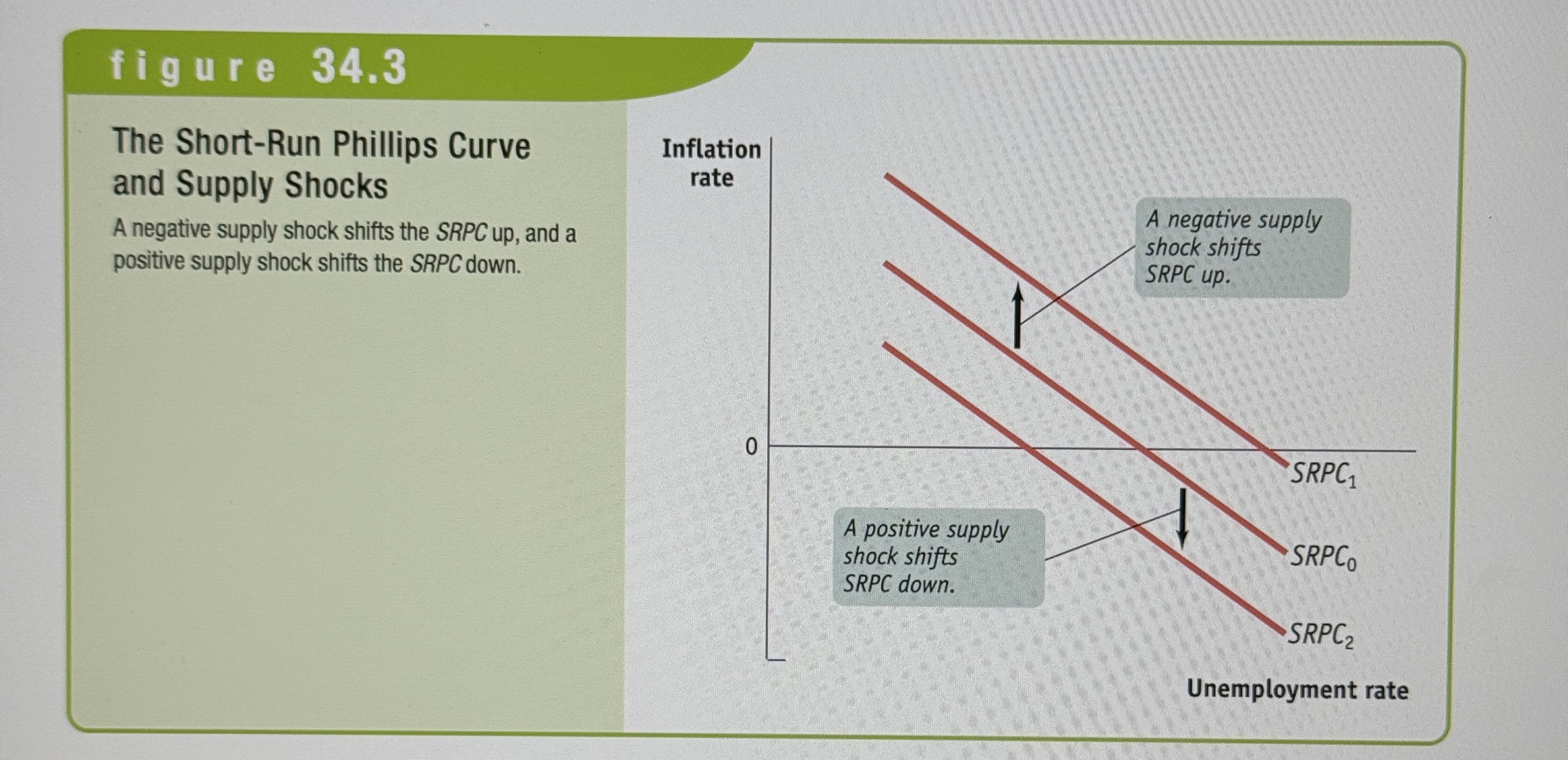

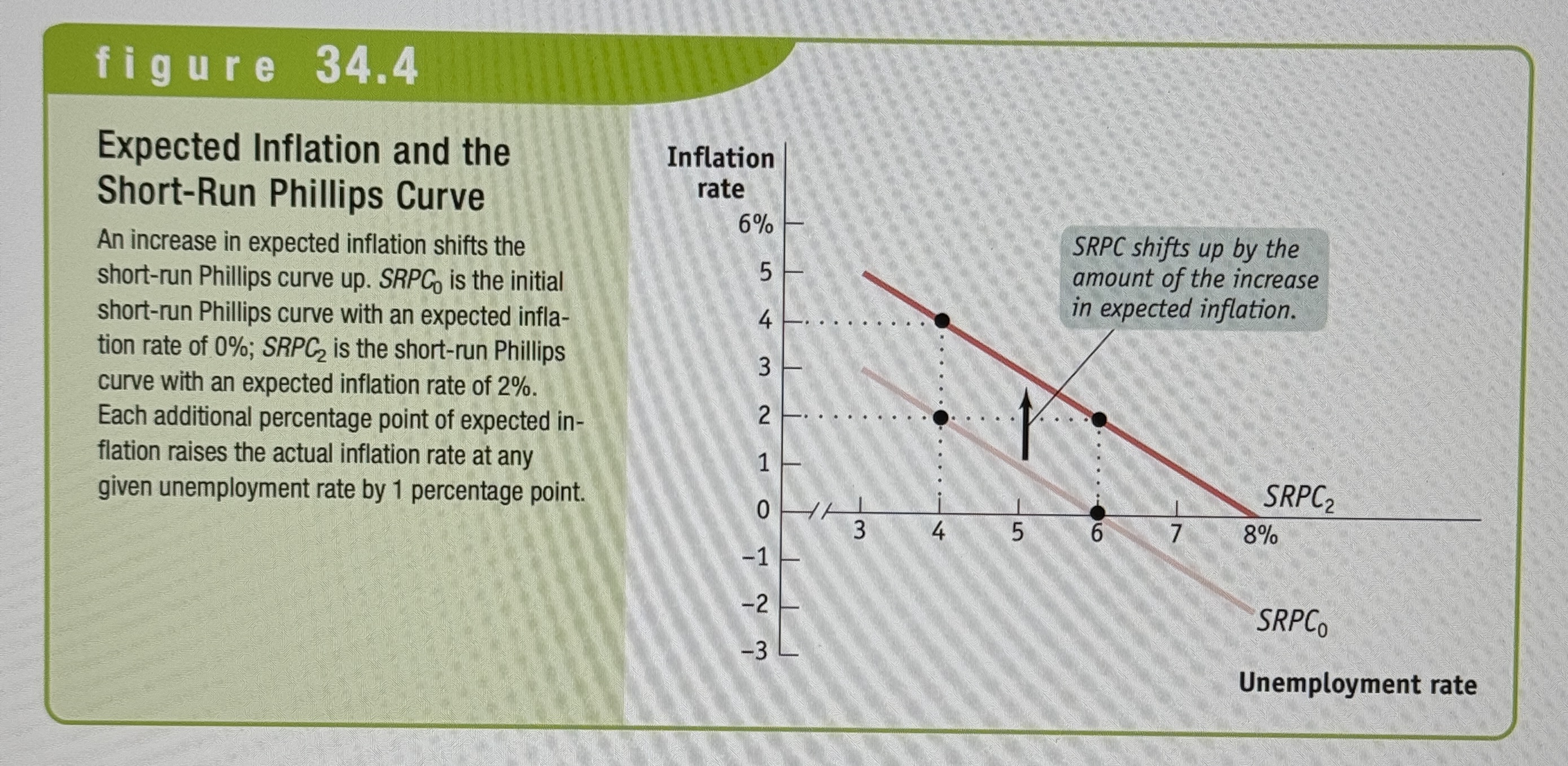

Short-Run Phillips Curve

The negative short run relationship between the unemployment rate and the inflation rate.

The Short-Run Phillips Curve and Supply Shocks

Ex.

Expected Inflation and the Short-Run Phillips Curve

Ex.

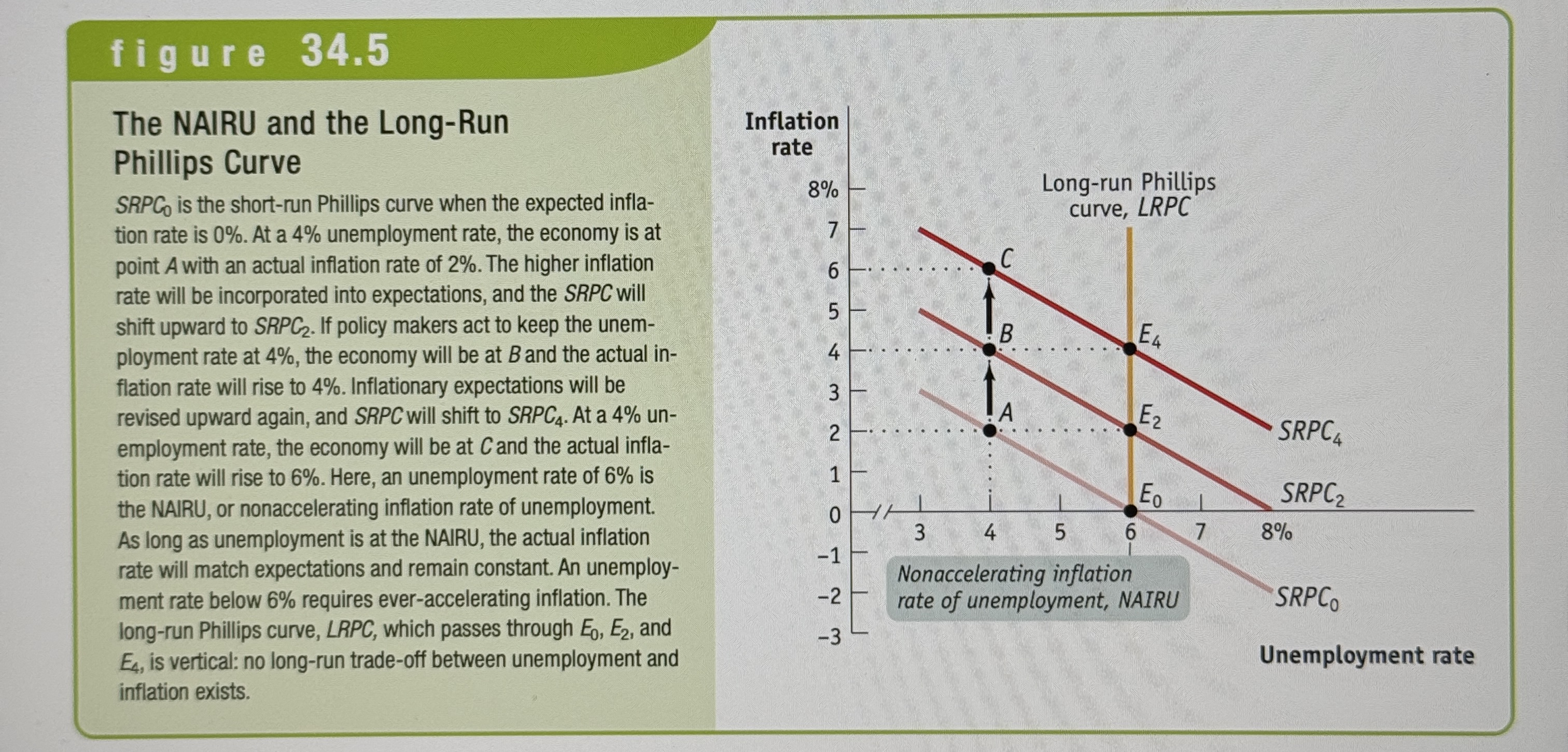

The non-accelerating inflation rate of unemployment or NAIRU

The unemployment rate at which inflation does not change overtime.

The long-run Phillips Curve

Shows the relationship between unemployment and inflation after expectations of inflation have had time to adjust to experience.

The NAIRU and the Long-Run Phillips Curve

Ex.

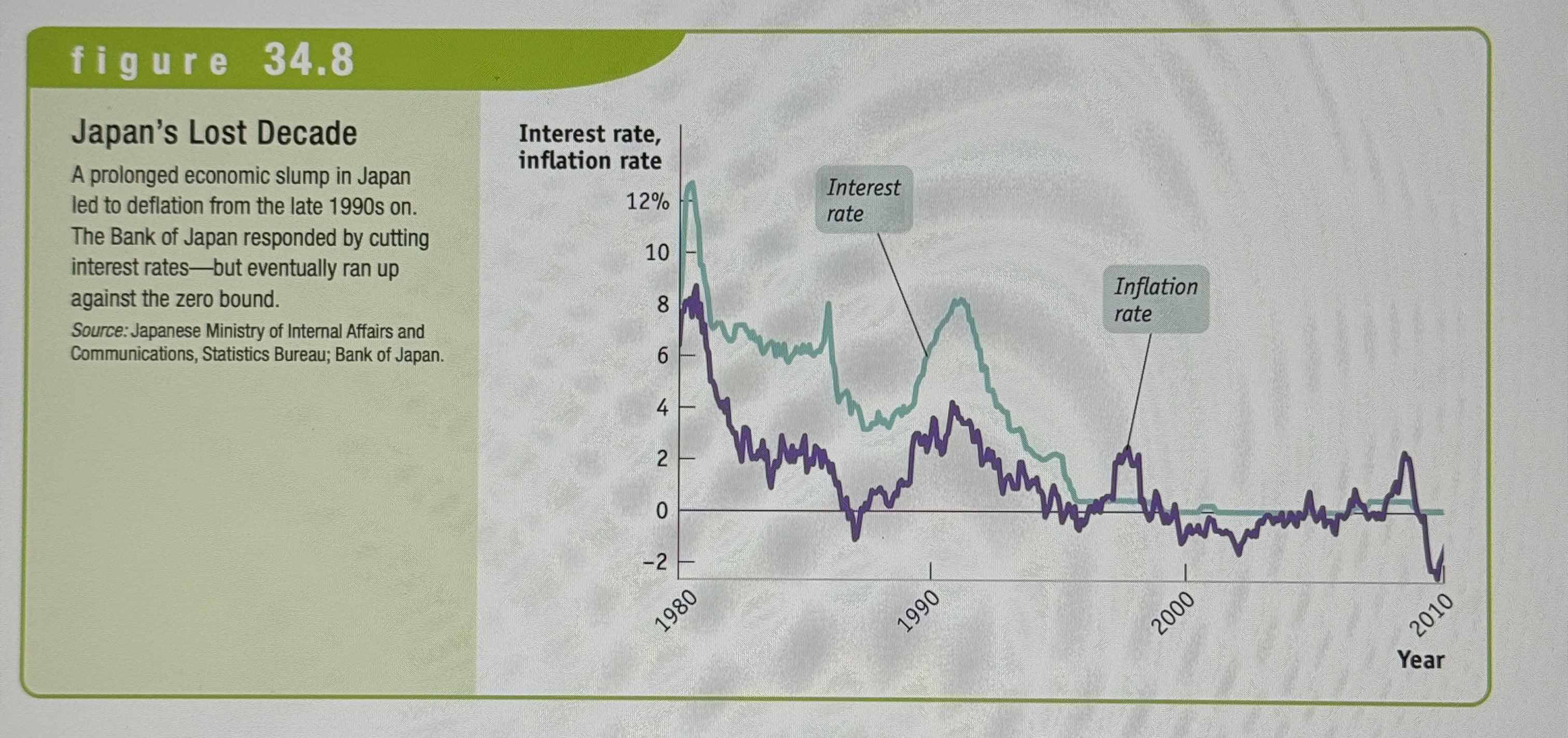

Debt Deflation

The reduction in aggregate demand arising from the increase in the real burden of outstanding debt caused by deflation.

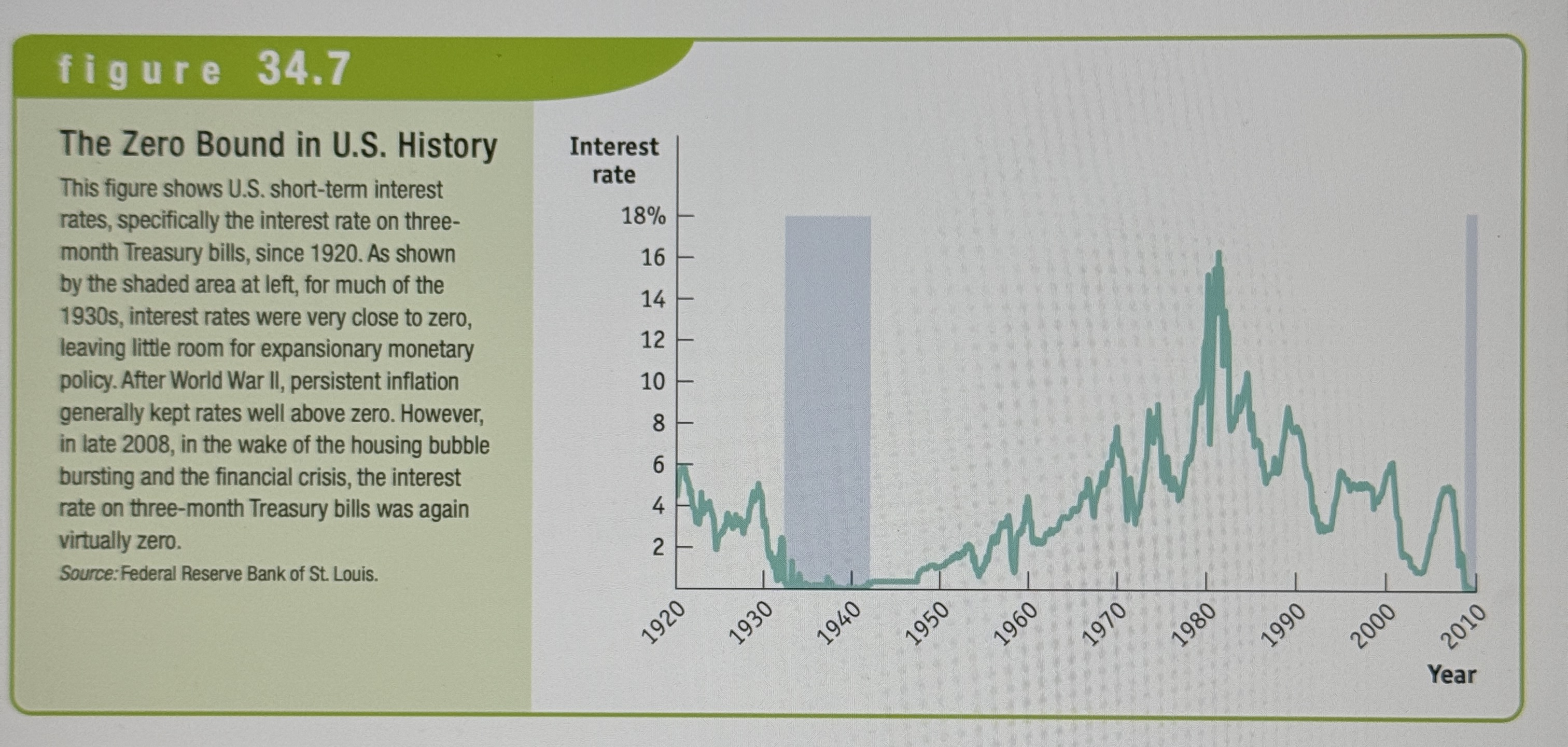

Zero Bounds

There is a zero bound on the nominal interest rate – it cannot go below zero.

Liquidity Traps

A situation in which conventional monetary policies is ineffective because nominal interest rates are up against the zero bound.

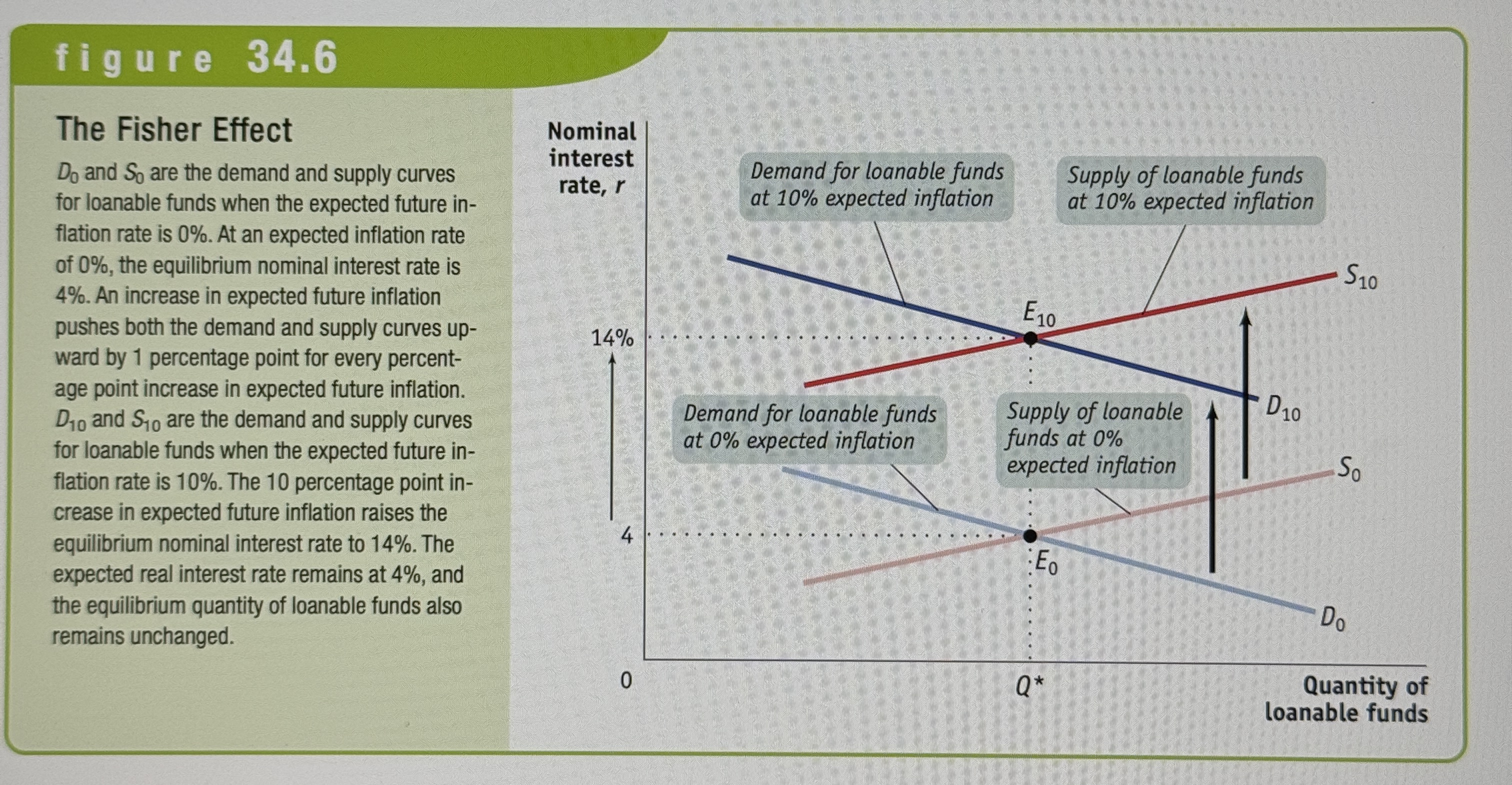

The Fisher Effect

Ex.

The Zero Bound in U.S. History

Ex.

Japans Lost Decade

Ex.

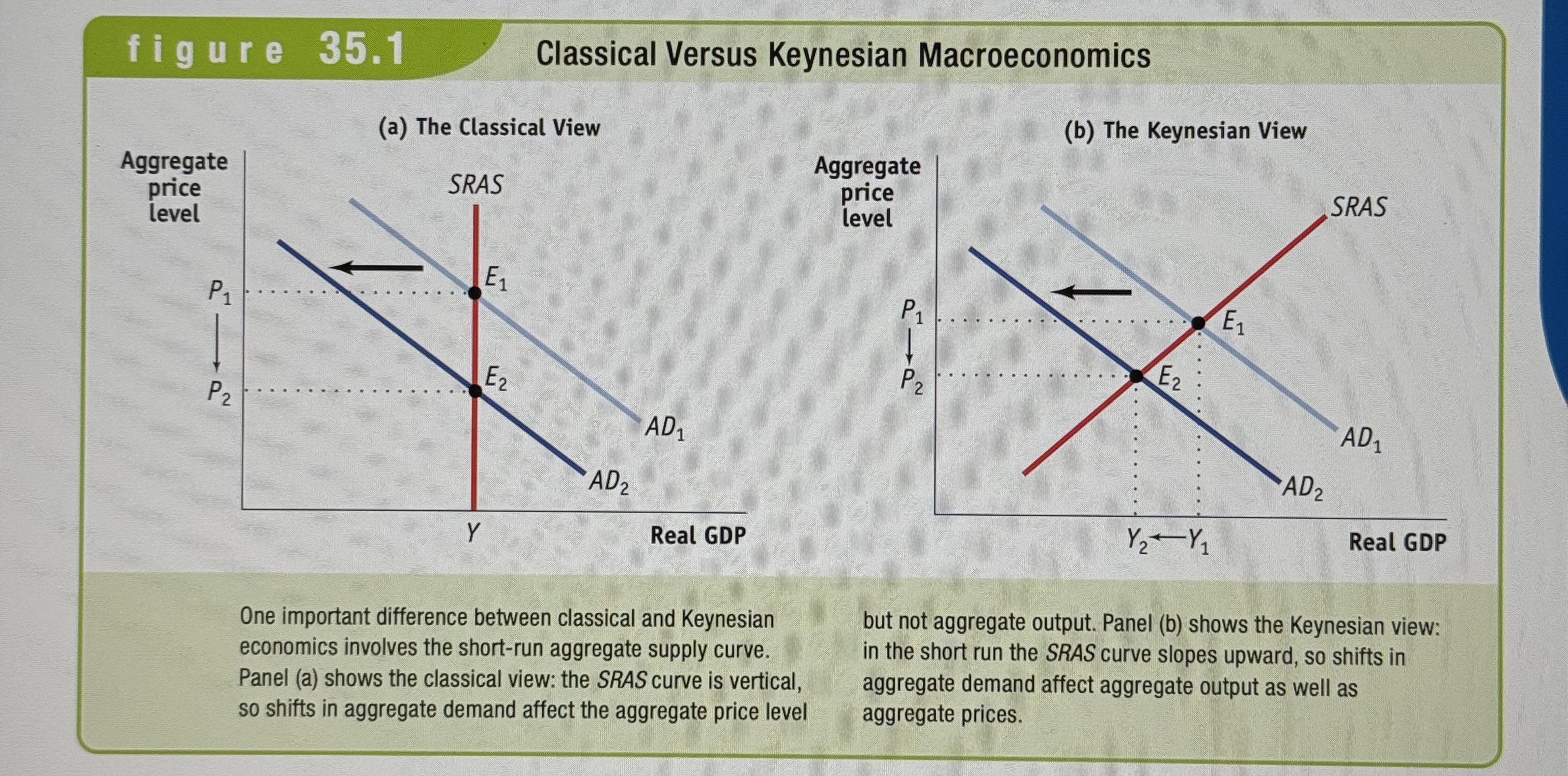

Classical Versus Keynesian Macroeconomics

Ex.

Macroeconomic policy activism

The use of monetary and fiscal policy to smooth out the business cycle.

Monetarism

Assert that GDP will grow steadily if the money supply grows steadily.

Discretionary monetary policy

The use of changes in the interest rate or the money supply to stabilize the economy.

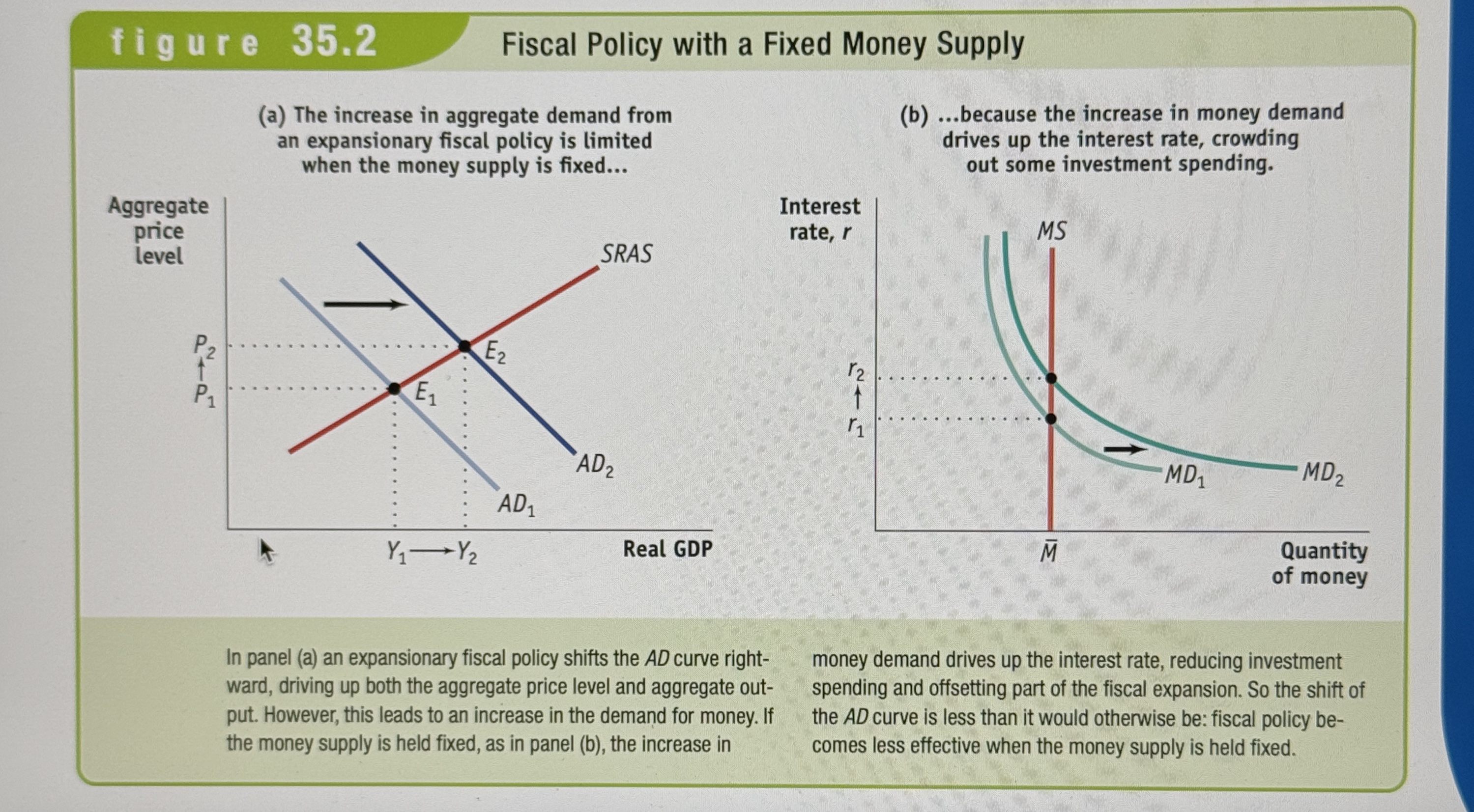

Fiscal Policy with a Fixed Money Supply

Ex.

Monetary policy rule

A formula that determines the central banks actions.

The quantity theory of money

Emphasizes the positive relationship between the price level and the money supply. It relies on the velocity equation (Money Supply*Velocity = Aggregate Price Level*Real GDP

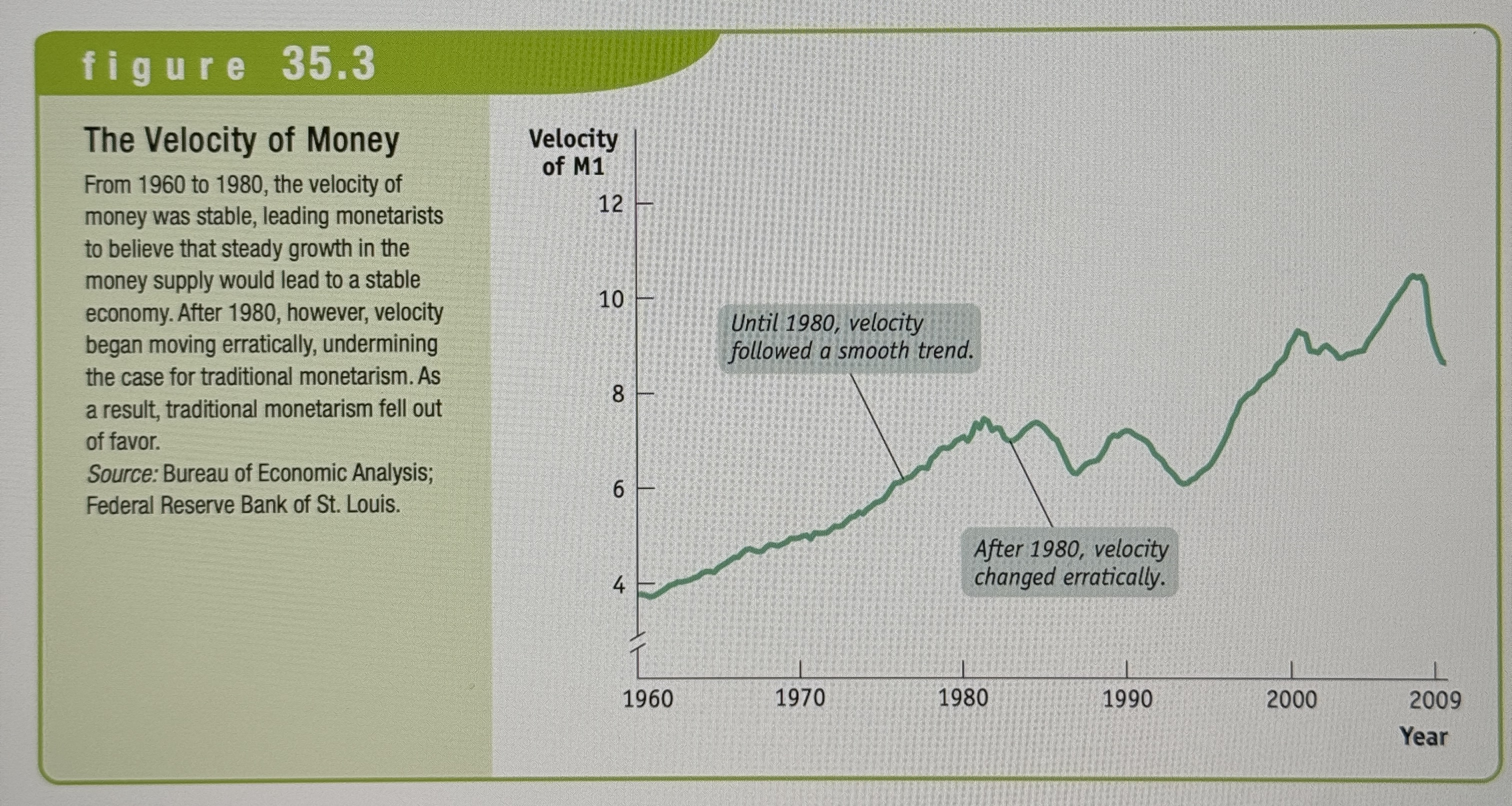

The velocity of money

The ratio of nominal GDP to the money supply. It is the measure of the number of times the average dollar bill is spent per year.

Natural Rate Hypothesis

To avoid accelerating inflation overtime, the unemployment rate must be high enough that the actual inflation rate equals the expected inflation rate.

Political business cycle

Results when politicians use macroeconomic policy to serve political ends.

New classical macroeconomics

An approach to the business cycle that returns to the classical view that shifts in the aggregate demand curve effect only the aggregate price level, not aggregate output.

Rational expectations

The view that individuals and firms make decisions optimally, using all available information

New Keynesian economics

Believes that market imperfections can lead to price stickiness for the economy as a whole.

Real business cycle theory

Claims that fluctuations in the rate of growth of total factor productivity cause the business cycle.

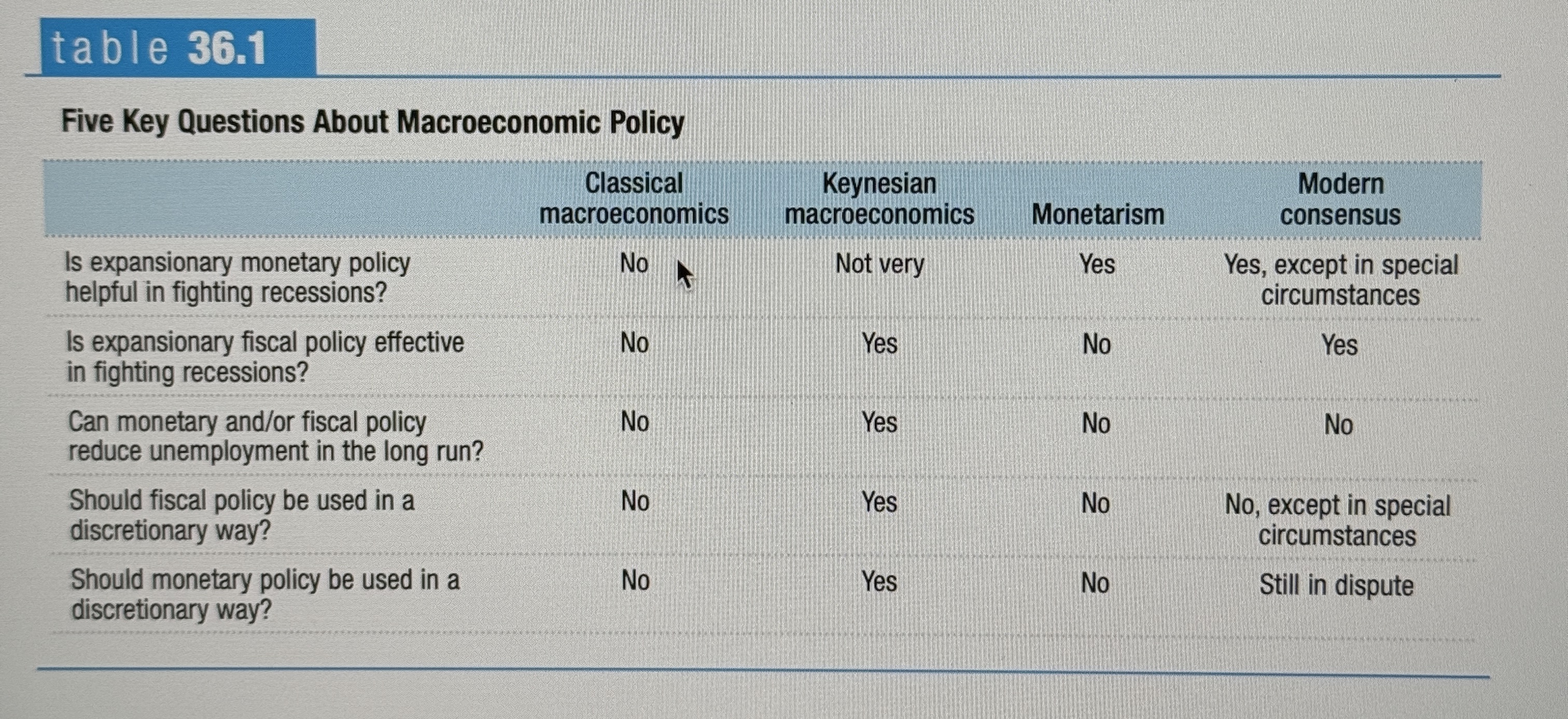

Five Key Questions About Macroeconomic Policy

Ex.

Summary #1

Some of the fluctuations in the budget balance are due to the effects of the business cycle. In order to separate the effects of the business cycle from the effects of discretionary fiscal policy, governments estimate the cyclically adjusted budget balance, an estimate of the budget balance if the economy were at potential output.

Summary #2

U.S. government budget accounting is calculated on the basis of fiscal years. Persistent budget deficits have long-run consequences because they lead to an increase in public debt. This can be a problem for two reasons. Public debt may crowd out investment spending, which reduces long-run economic growth. And in extreme cases, rising debt may lead to government default, resulting in economic and financial turmoil.

Summary #3

A widely used measure of fiscal health is the debt-GDP ratio. This number can remain stable or fall even in the face of moderate budget deficits if GDP rises over time.

However, a stable debt-GDP ratio may give a misleading impression that all is well because modern governments often have large implicit liabilities. The largest implicit liabilities of the U.S. government come from Social Security, Medicare, and Medicaid, the costs of which are increasing due to the aging of the population and rising medical costs.

Summary #4

Expansionary monetary policy reduces the interest rate by increasing the money supply. This increases investment spending and consumer spending, which in rum increases aggregate demand and real GDP in the short run. Contractionary monetary policy raises the interest rate by reducing the money supply. This reduces investment spending and consumer spending, which in turn reduces aggregate derand and real GDP

Summary #5

The Federal Reserve and other central banks try to stabilize their economies, limiting fluctuations of actual output to around potential output, while also keeping inflation low but positive. Under the Taylor rule for monetary policy, the target interest rate rises when there is inflation, or a positive output gap, or both; the target interest rate falls when inflation is low or negative, or when the output gap is negative, or both. Some central banks engage in inflation targeting, which is a forward-looking policy rule, whereas the Taylor rule is a backward-looking policy rule. In practice, the Fed appears to operate on a loosely defined version of the Taylor rule. Because monetary policy is subject to fewer implementation lags than fiscal policy, it is the preferred policy tool for stabilizing the economy.

Summary #6

In the long run, changes in the money supply affect the aggregate price level but not real GDP or the interest rate. Data show that the concept of monetary neutrality holds: changes in the money supply have no real effect on the economy in the long run.

Summary #7

In analyzing high inflation, economists use the classical model of the price level, which says that changes in the money supply lead to proportional changes in the aggregate price level even in the short run.

Summary #8

Governments sometimes print money in order to finance budget deficits. When they do, they impose an inflation tax, generating tax revenue equal to the inflation rate times the money supply, on those who hold money. Revenue from the real inflation tax, the inflation rate times the real money supply, is the real value of resources captured by the government. In order to avoid paying the inflation tax, people reduce their real money holdings and force the government to increase inflation to capture the same amount of real inflation tax revenue. In some cases, this leads to a vicious circle of a shrinking real money supply and a rising rate of inflation, leading to hyperinflation and a fiscal crisis.

Summary #9

A positive output gap is associated with lower-than-normal unemployment; a negative output gap is associated with higher-than-normal unemployment.

Summary #10

Countries that don't need to print money to cover government deficits can still stumble into moderate inflation, either because of political opportunism or because of wishful thinking.

Summary #11

At a given point in time, there is a downward-sloping relationship between unemployment and inflation known as the short-run Phillips curve. This curve is shifted by changes in the expected rate of inflation.

The long-run Phillips curve, which shows the relationship between unemployment and inflation once expectations have had time to adjust, is vertical. It defines the nonaccelerating inflation rate of unemployment, or NAIRU, which is equal to the natural rate of unemployment.

Summary #12

Once inflation has become embedded in expectations, getting inflation back down can be difficult because disinflation can be very costly, requiring the sacrifice of large amounts of aggregate output and imposing high levels of unemployment. However, policy makers in the United States and other wealthy countries were willing to pay that price of bringing down the high inflation of the 1970s.

Summary #13

Deflation poses several problems. It can lead to debt deflation, in which a rising real burden of outstanding debt intensities an economic downturn. Also, interest rates are more likely to run up against the zero bound in an economy experiencing deflation. When this happens, the economy enters a liquidity trap, rendering conventional monetary policy ineffective.

Summary #14

Classical macroeconomics asserted that monetary policy affected only the aggregate price level, not aggregate output, and that the short run was unimportant. By the 1930s, measurement of business cycles was a well-established subject, but there was no widely accepted theory of business cycles.

Summary #15

Keynesian economics attributed the business cycle to shifts of the aggregate demand curve, often the result of changes in business confidence. Keynesian economics also offered a rationale for macroeconomic policy activism.

Summary #16

In the decades that followed Keynes's work, economists came to agree that monetary policy as well as fiscal policy is effective under certain conditions. Monetarism is a doctrine that called for a monetary policy rule as opposed to discretionary monetary policy. The argument of monetarists-based on a belief that the velocity of money was stable-that GDP would grow steadily if the money supply grew steadily, was influential for a time but was eventually rejected by many macroeconomists.

Summary #17

The natural rate hypothesis became almost universally accepted, limiting the role of macroeconomic policy to stabilizing the economy rather than seeking a permanently low unemployment rate. Fears of a political business cycle led to a consensus that monetary policy should be insulated from politics.

Summary #18

Rational expectations suggests that even in the short run there might not be a tradeoff between inflation and unemployment because expected inflation would change immediately in the face of expected changes in policy. Real business cycle theory said that changes in the rate of growth of total factor productivity are the main cause of business cycles. Both of these versions of new classical macroeconomics received wide attention and respect, but policy makers and many economists haven't accepted the conclusion that monetary and fiscal policy are ineffective in changing aggregate output.

Summary #19

New Keynesian economics argues that market imperfections can lead to price stickiness, so that changes in aggregate demand have effects on aggregate output after all.

Summary #20

The modern consensus is that monetary and fiscal policy are both effective in the short run but that neither can reduce the unemployment rate in the long run. Discretionary fiscal policy is considered generally unadvisable, except in special circumstances.

Summary #21

There are continuing debates about the appropriate role of monetary policy. Some economists advocate the explicit use of an inflation target, but others oppose it.

There's also a debate about whether monetary policy should take steps to manage asset prices and what kind of unconventional monetary policy, if any, should be adopted to address a liquidity trap.