Microeconomics Exam #1

1/126

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

127 Terms

economics

social science concerned with making iotimal choices under conditions of scarcity. perspective made when making rational decisions by comparing marginal benefits and costs associated with actions.

Scarcity

limits on amount and variety of goods/services for consumption because there are limited economic resources.

trade-off

Due to limited resources and unlimited wants, trade-offs have to be made in order to acquire some things over others.

opportunity cost

To gain more of one thing you sacrifice the opportunity of gaining the next best thing that could have been acquired or created with the same resources. Next best thing not chosen is the _______ ____.

Cost

accumulating and directing set of resources to that thing acquired.

marginal

extra, additional, or change in

marginal analysis

comparisons on marginal benefits and marginal costs. Looking at how a little more can influence outcome.

Incentives

motivates one to do something. in economics, often financial in nature.

economic principle

statement about economic behavior or the economy that enables predictions of probable effects of certain actions. These are well tested and widely accepted.

models

purposeful simplifications. the scope of the economy is too complex to be fully understood, and models are geared to simplify.

models & theories

explain and often predict how individuals and institutions behave in producing, exchanging, and consuming goods and services

generalizations

economic principles are general, usually expressed as tendencies of typical people, businesses, or institutions

other-things-equal assumption

ceteris paribus, all factors besides those being considered do not change.

economic system

set of institutionalized arrangements and a coordinating mechanism to respond to the economic problem

command economy

government owns resources, and decisions are made by a central planning board. i.e socialism, communism

Laissez Faire Capitalism

against any government interference in the economy. Protects provide property and provides a legal environment for contract enforcement. People interact in markets to buy and sell.

The Market System

regarded often as “capitalism” or “mixed economy". majority of the world’s economics, it being a mix of decentralized decision making with some government control. Businesses and individuals achieve economic goals through their own decisions. Private ownership of resources.

Market System: Private Property

rights encourage people to cooperate by helping to ensure that only mutually agreeable economic transactions take place.

Market System: Freedom of enterprise

ensures that entrepreneurs and private businesses are free to obtain and use economic resources to produce their choice of goods and services, and sell them in their chosen markets.

Market System: Freedom of Choice

enables owners to employ or dispose of their property and money as they see fit.

Market System: Self Interest

gives direction and consistency to what might otherwise be chaotic.

Market System: Competition

competing among buyers and sellers diffuses economic power within the businesses and households that compose economy.

Market System: Market and Price

decisions on either side of the market determine a set of product and factor prices that guide resource owners, entrepreneurs, and consumers.

Market System: Technology and Capital Goods

advances technology and capital goods are encouraged as it helps economies achieve greater production efficiency

Market System: Specialization

ability differences, and division of labor based on this allows for people to become well acquainted with very specific aspects of a job.

Market System: Use of Money

medium of exchange, makes trade easier, without money people would have to barter.

Market System: Active but Limited Government

may be needed to alleviate market failures, increasing the overall effectiveness of the system. If there is recession or inflation the government can act to correct.

5 Fundamental Questions

What will be produced

How will it be produced

Who will get what is produced

How will the system accommodate change

How will the system promote progress

What will be produced

-Goods and services the create a profit (TR>TC)

-Consumer sovereignty determines types and quantities via dollar votes→ reflecting consumer wants and needs

How will it be produced

-at a minimal cost per unit, utilizing efficient technologies

-right mix of labor and capital

-optimal location of the production facilities

-technology

Who will get what is produced

-consumers with the willingness and ability to buy.

-dependent on income

-willingness to pay depends on preference

How will the system accommodate change

-changes in consumer taste may lead to the market systems key feature of adjusting

-Changes in technology

How will the system promote progress

-technological advancement→ incentive is provided for this and is enable better processes to supplant inferior ones.

-capital accumulation→ technological goods often require this. capital goods can be utilized by business owners to receive more profit for production processes.

The Invisible Hand

tendency of competition to cause individuals to promote the interests of society. Firms maximize profits, resource suppliers maximize incomes, and in doing so societies input and output is maximized.

Command System Issues

Coordinate problem→ central planners have to coordinate millions of small decisions, by consumers, resource suppliers, and businesses. They set target output for all goods, and any industry fail causes a chain reaction of repercussions.

Incentive problem: Government misjudgments can cause persistent surplus and shortage. There is no incentive for managers to adjust as they’re rewarded for meeting an assigned target.

individual economic problem

need to make choices because wants exceed economic means. Driven by limited income and unlimited wants

The Budget Line/Constraint

-schedule or curve that shows the combinations of two products/services that a consumer can purchase with a specific income or budget.

Budget Line Graphed

combination of services and rate at which one good would have to be sacrificed to obtain another. Displayed by the slope. Income changes or changes in price affect the budget line.

Society’s Economic problem

decisions on how the scarce resources available should be allocated. trade-offs must be made as well when choosing how to allocate on a larger scale.

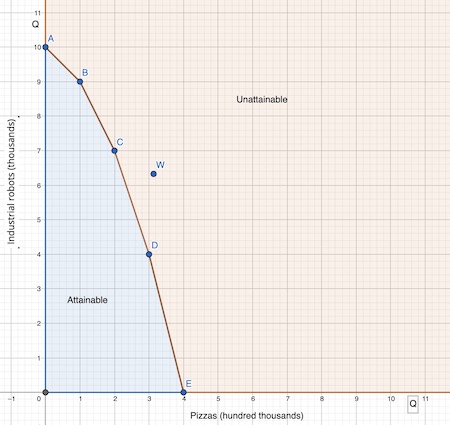

Production Possibilities Model

Alternatives available to society on how it may utilize its resources can be understood through the production possibilities model.

Production Possibilities simplified assumptions

-Full employimnet

-fixed resources

-fixed technology

-two goods

Production Possibility Table

list different combinations o two products that can potentially be produced, assuming specific set of resources and full employment

Production Possibilities Curve (PPC)

curve that shows combination of output the fully employed economy could potentially produce. each point displays a different combination that could be produce.

Law of Increasing Opportunity Cost

makes the PPC concave. as more of one good is produced, its opportunity cost for producing an additional unit rises. more pizza production is given up as more robots are created. why→ economic resources are not overtly adaptable, certain resources are much better at creating different things

PPC Outward Shift

Occurs with quality of resources and technology fixed are no longer assumed. represents the maximum potential of output increasing.

What causes economic growth?

-Increase in factor supplies and quantity

-advances in technology

Market

interaction between buyers and sellers. may be local or international. price is discovered through intentions of buyers and sellers, involved in mutually beneficial voluntary trade.

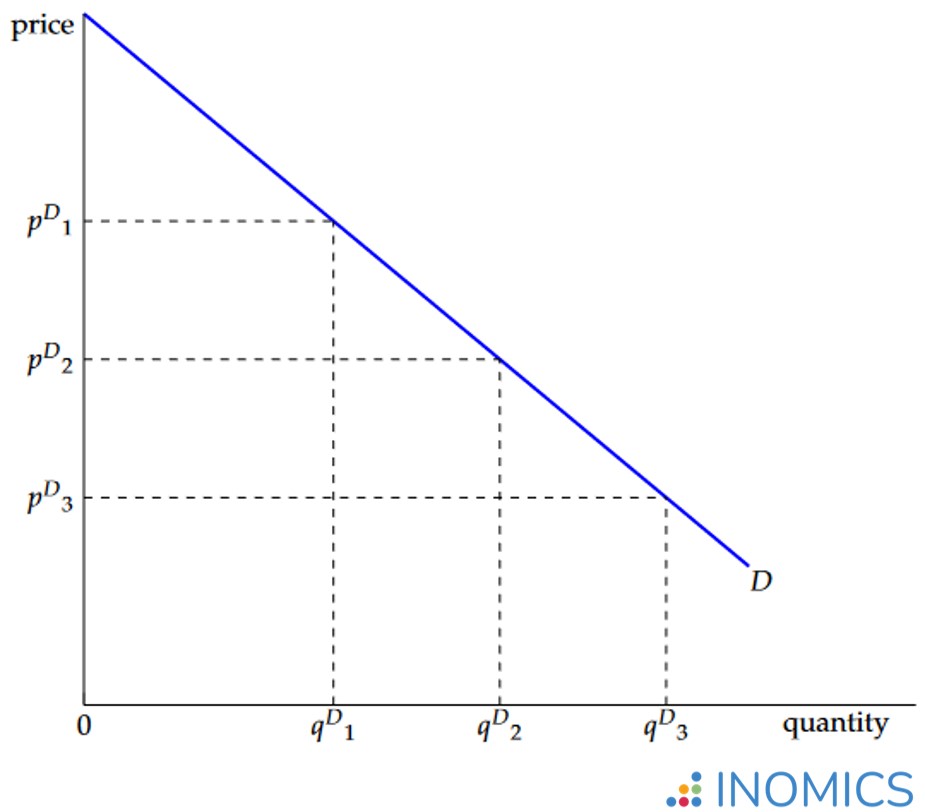

Demand

buyers portion of the market.

Demand curve

depicts how much consumers are able and willing to buy of a product at a series of specified prices during a specified time.

Law of Demand Reasonings

-Diminishing marginal utility→if a consumer increases consumption of a good, the marginal satisfaction/benefit obtained from each additional unit decreases

-Income effect→ lower price=more buying power.

-Substitution effect→ lower priced goods substitute for higher priced ones.

Demand Determinant: Consumer Preferences

-desirability causes more demand at each price

Demand Determinants: Number of Buyers

-more people buying, more demand

Demand Determinants: Income

-more money made, more demand for specific products (inferior goods exempt)

Demand Determinants: Price of Related Goods

-substitutes or complements for each other can determine price

Demand Determinants: Consumer Expectations

ideas about whether or not a price is bound to rise or fall can effect consumer purchases.

Change in Demand

-determinant of demand has changed, and the curve has shifted, with there being a different amount at each price point.

Change in Quantity Demanded

movement from one price to another. movement along a fixed curve, holding all other determinants the same. Caused by price increase or decrease.

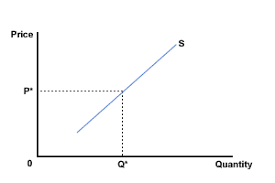

Supply

statement about a firms intention to produce a product.

Supply Schedule/Curve

shows various amounts of a product that producers are willing and able to make at a series of possible prices for a specified period.

deriving supply

only factor assumed to cause producers to produce more or less is the price of the good. all other factors that influence amount that firms will produce are constant.

Law of Supply

all else equal, as price rises quantity supplied rises, and as price falls, quantity supplied falls. to a supplier, price represents revenue→ incentive to produce more.

Supply Determinants: Change in Factor Prices

if input prices increase, cost is higher to produce a good, and larger price is needed to incentivize production

Supply Determinant: Technology Change

technological advancements can make production more efficient, meaning more can be produced with the same set of resources= more production at each price point.

Supply Determinant: Taxes and Subsidies

production can be made more costly or less costly via government influence, changing mkt price to production relationship

Supply Determinant: Price Change of Goods

If something different can be produced with the same resources, higher prices will cause producers to shift towards having that good.

Supply Determinant: Producer Expectations

if higher or lower prices are anticipated, the amount produced could be adjusted accordingly by the producer.

Supple Determinant: Number of Sellers

when there is more people in the market, more can be sold at each price point

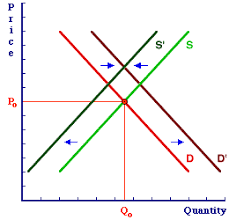

Change in Supply

a supply determinant has changed. Curve has shifted, and producers are now supplying a different amount at each price point.

Change in Quantity Supplied

Movement from one point to another along a fixed curve. all determinants are the same, caused by an increase or decrease in price, so firms produce more or less.

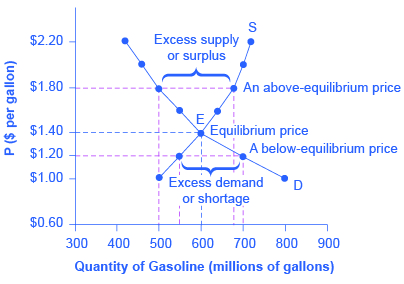

Equilibrium Price

intentions of buyers and sellers match. quantity demanded=quantity supplied

Rationing function of prices

ability for supply and demand to establish a price at which selling and buying decisions are constant.

Efficient allocation

i. Productive efficiency→ producing goods in the way that costs the least, using the best technology, and using the right mix of resources

ii. Allocative efficiency→ Producing the right mix of goods, the combination of goods most highly valued by society.

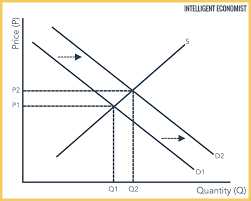

Increase in Demand

-shortage

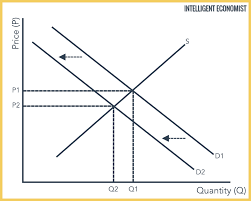

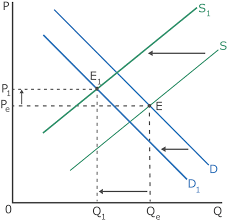

Decrease in Demand

-Surplus

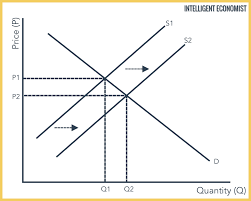

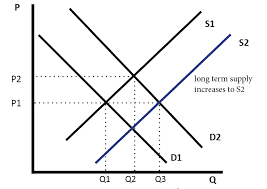

Increase in Supply

-surplus

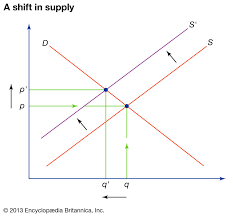

Decrease in supply

shortage

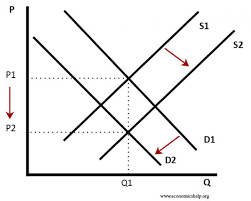

Supply Increase and Demand Decrease

-price will decrease

-quantity is dependent on size of the shift

Supply Decrease and Demand Increase

price will increase, quantity is dependent on size of the shift.

Supply Increase and demand Increase

quantity increases, price depends on size of shift

Supply decrease and demand decrease

quantity decrease, price change depends on size.

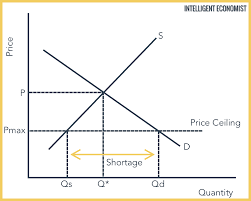

Price Ceiling

-Maximum legal price a seller can charge.

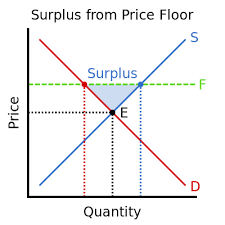

Price Floor

-Minimum legal price a buyer can pay.

Price Elasticity of Demand

consumers responsiveness or sensitivity to a change in price is measured by a products price elasticity of demand. Tells us how consumers will likely respond to price rise

Coefficient Ed>1

elastic good

Coefficient Ed<1

inelastic good

Coefficient Ed=1

unit elastic good

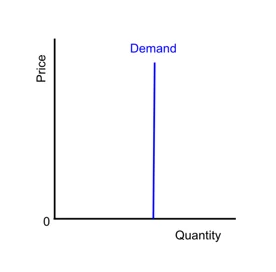

Perfectly Inelastic

consumers are unresponsive to price changes.

Perfectly Elastic

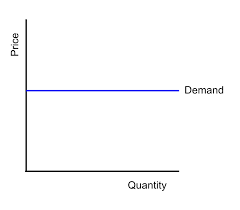

consumers are completely responsive to price change. Price reduction causes consumers to go from purchasing 0 to all they can obtain.

Total Revenue

total amount that sellers receive from the sale of their products. Easy method to deduce whether or not something is elastic or inelastic

Price decrease= TR increase

elastic demand, even though price per unit is lower, enough additional units are sold

Price decrease= TR decrease

inelastic demand. increase in sales does not offset decrease in price per unit.

increase or decrease in price= unchanged revenue

gain in sales from lower price exactly offsets to result in the same revenue.

Elasticity Determinant: Substitutability

Larger number of goods available, greater price elasticity of demand. Dependent on how narrowly the product is defined.

Elasticity Determinant: Proportion of Income

greater portion of income spent on a good, the greater the price elasticity of demand for it (i.e. house vs. toothpaste)

Elasticity Determinant: Luxuries vs. Necessities

The more a good is considered unnecessary or extra, the greater the price elasticity of the demand.

Elasticity Determinant: Time

product demand is more elastic the more it is under consideration. consumers often take ____ to adjust to price changes.

Government Taxation

goal is to reduce product consumption by making a product more expensive.

Elastic Supply

Responsive to price changes

Inelastic Supply

insensitive to price changes

Primary Supply Elasticity Determinant

Time, how quickly can producers shift resources between alternative uses.