microeconomics (all)

1/78

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

79 Terms

scarcity

the reason the economy exists (conditions: desirable and limited in supply)

economic system

a system for allocating scarce resources

economics

the social science that studies the allocation of scarce resources between society’s competing wants & needs

how to deal with the problem of scarcity

3 basic economic questions

who will get the resources

what will be produced with the resources

who will receive the finished output of resources

opportunity cost

the value of the next-best alternative that you give up in order to get an item

what could have been done with resources when a decision is made about their use

the opportunity lost

production possibilities curve

a model that shows the tradeoffs society/individuals face in how to use scarce resources

shows what is possible in our use of scarce resources between 2 competing wants/needs

linear PPC curve

when variable1 and variable2’s trade-offs are equal

constant opportunity cost

the 2 goods produced are identical and require the same resources

1 million pizzas = 1,000 cars

inefficient uses of time/resources

inside the PPC curve

impossible use of time/resources

outside the PPC curve

law of increasing opportunity cost

↑ production of a good/service = ↑ opportunity cost of producing each unit

bowed out PPC curve

this is because resources are not perfectly adaptable to all uses

the opportunity cost in terms of the other good that must be given up increases

decreasing opportunity costs in the PPC

as output for one good increases, the opportunity cost (in terms of how many units of the other good given up) decreases

resources needed to produce some goods become less scarce as outputs increases

therefore, the cost of additional units decreases

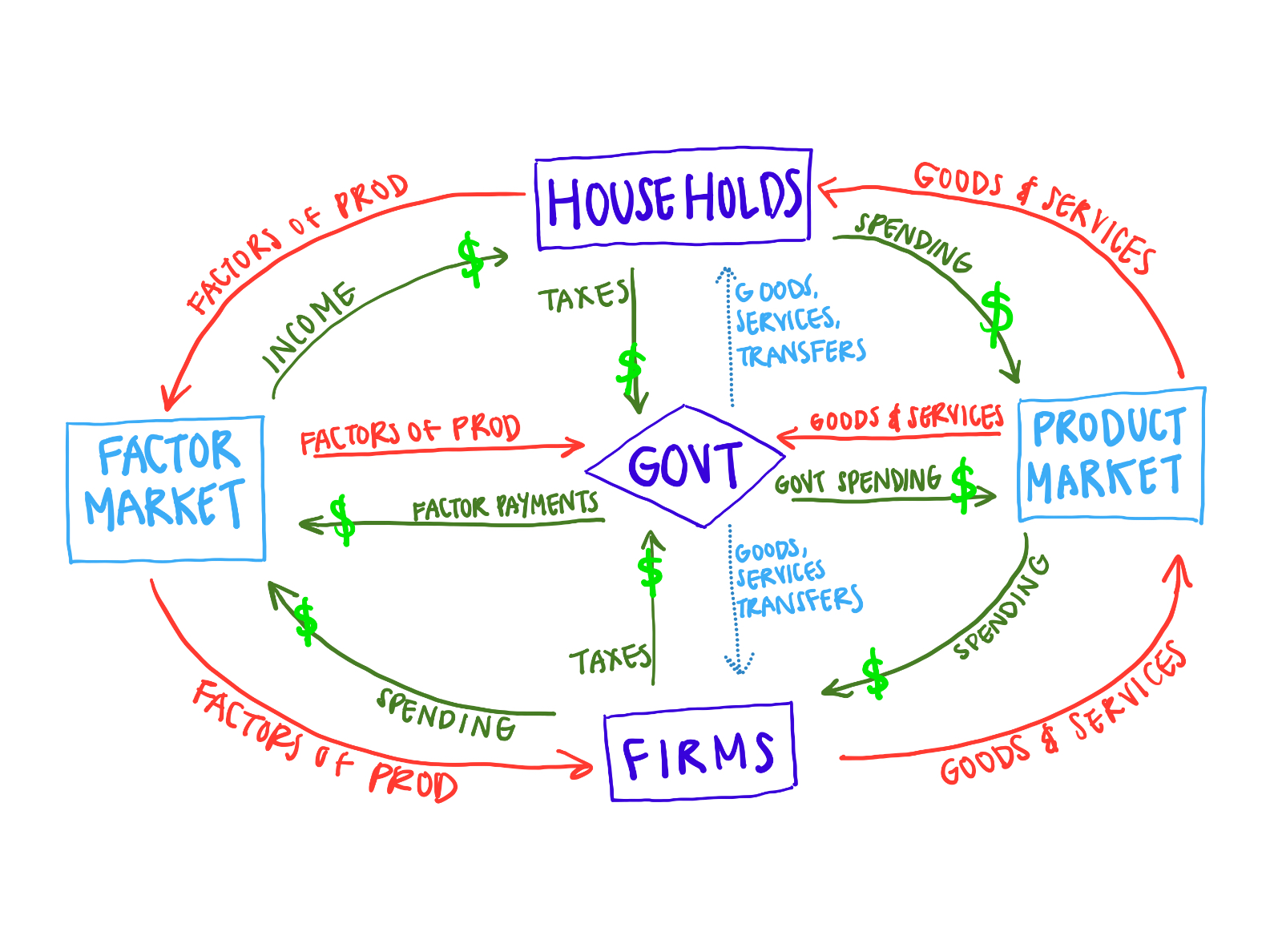

circular flow

a simplified diagram of macroeconomy

shows flow of money, goods/services, factors of production

flow of $ into each market/sector = flow of $ out of each market/sector

physical flow in the circular flow diagram (red)

goods, services, labor, raw materials

payment flow in the circular flow diagram

payment for goods, services, labor, raw materials

product markets

market where goods and services are

bought (by households)

sold (by firms)

consumer spending

household spending for goods and services

factor markets

market where resources are

bought (by firms)

sold (by households)

households own and receive income from all factors of production

government spending

everything spent on goods and services by federal, state, and local governments

taxes

required payments to the government from firms and households

tax revenue

the total amount of funds the government receives from taxes

factors of production

the economy’s resource

land, labor, capital, entrepreneurship

payments for factors of production

wages, rent, interest, profit

disposable income

(income + govt transfers) - taxes

total amount of household income available to spend on consumption

government transfers

payments the government makes to individuals without expecting a good/service in return

ex: unemployment insurance payments

private savings

disposable income - consumer spending

household income that’s not spent on consumption

financial markets

markets that channel private savings into investment spending and government borrowing

government borrowing

an amount of funds borrowed by the government in financial markets

investment spending

spending by firms on new productive physical capital

capital segways into future streams of $/output

buying machines, factories, houses

changes in inventory

inventory

stocks of goods and raw materials held to facilitate business operations

land

all natural resources (plants, water, minerals, raw materials)

labor

effort of workers

capital

manufactured goods used to make other goods and services

machinery, buildings, tools

entrepreneurship

risk-taking, innovation, organization of resources for production

marginal benefit

what you gain from doing something one more time

marginal cost

the cost of doing something one more time

marginal decisions

marginal benefit/cost

the gain/loss of doing something one more time

marginal analysis

the study of the costs/benefits of doing something a little more/less

“how much” should you do of an activity?

microeconomics

the study of how individuals, households, and firms make decisions and how those decisions interact

macroeconomics

the study of overall ups and downs of the economy

positive economics

economic analysis used to answer questions about how the economy works

has definitive right/wrong answers

descriptive

normative economics

economic analysis that involves saying how an economy should work

prescriptive

traditional economies

production and consumption are based on precedent

small villages, amish communities

market economies

factors of production are privately owned, and the decisions of individual producers and consumers largely dictate what, how, and for whom to produce

capitalist

free enterprise

a market economy with minimal government involvement

laissez-faire from the gilded age (late 1800s-1900)

command economies

factors of production are publicly owned, and a central authority makes production and consumption decisions

communism, socialism

mixed economies

combines elements of traditional, market, command economies

most modern markets (US, CHN, RUS, etc.)

incentives

rewards/punishments that motivate particular choices

property rights

establish ownership and grant individuals the right to trade goods and services with each other

applied to resources, goods, firms, intellectual property (inventions, art, etc.)

incentivize people to produce, keep, or trade for better things

ceteris paribus

“other things equal”

all other relevant factors remain unchanged in economic models

efficiency

there is no other way to make anyone better off without making at least one person worse off in an economy

no missed opportunities

productive efficiency

if an economy is producing at any point on its PPC

allocative efficiency

if an economy is producing at a point on its PPC that’s preferred by consumers

when a company produces goods/services that society desires most

economic growth

an increase in the maximum amount of goods/services an economy is able to produce

PPC shifts outwards

sources: tech, availability of resources used to produce g/s

economic shrinkage

a decrease in the maximum amount of goods/services an economy is able to produce

PPC shifts inwards

economy has shrunk

causes: loss of resources/tech, war, natural disasters

perfectly competitive market

a market with many buyers/sellers of the same good/service.

no individual’s actions have a noticeable effect on the price of a good/service sold

supply and demand model

a model that shows how a perfectly competitive market works

demand curve

factors that make the D curve shift

supply curve

factors that make the S curve shift

market equilibrium

eq price

eq quantity

the way the market changes when S or D curve shifts

demand schedule

a table that shows how much of a good/service consumers will be willing and able to buy at different prices

Law of Demand

a higher price for a good/service = less demand for that good/service

given ceteris paribus

change in demand

a shift of the demand curve

changes quantity demanded for any given price

increase in demand

a rightward shift of the D curve

consumers want a larger quantity of the good/service

decrease in demand

leftward shift of the D curve

consumers want less of a good/service

causes for a D curve shift

changes in taste, price of related goods/services, income, # of consumers, expectations that lead to a change in the economy

changes in taste

due to trends, beliefs, cultural shifts

changes price of related goods/services

when demand for a good changes due to changes in prices of substitutes or complements

complements

goods/services that are consumed together

cars + gas, phones + apps, etc.

changes in income

when demand for a good changes:

increased income = increased demand for normal goods

normal goods

demand for this good increases when consumer income increases

inferior goods

demand for this good increases when consumer income decreases

a less desirable version of more expensive dupes

changes in # of buyers

when demand for a good changes:

more consumers = more demand

less consumers = less demand

changes in expectation

when demand for a good changes because of expected changes in price/salary/other

equilibrium

an economic situation where no buyer/seller would be better off doing something different.

where S and D curves intersect

quantity of a good demanded = quantity supplied

equilibrium price

the price of an item that matches the quantity supplied and quantity demanded

price = Q demanded by consumers = Q supplied by sellers

“market-clearing prices”

equilibrium quantity

quantity bought/sold at the equilibrium price

disequilibrium

when the market price is above/below the price that equals the quantity demanded and quantity supplied

market price

all sellers receive and all buyers pay around the same price

surplus

quantity supplied (Qs) > quantity demanded (Qd)

occurs when the price is above equilibrium

“excess supply”

shortage

quantity demanded (Qd) > quantity supplied (Qs)

occurs when price is below equilibrium

“excess demand”

market response to changes in demand

increased demand = raised eq price & eq quantity

decreased demand = lowered eq price & eq quantity

market response to changes in supply

increased supply = decreased eq price & increased eq quantity

decreased supply = increased eq price. & decreased eq quantity