Econ terms and questions: micro

0.0(0)

Studied by 0 peopleCard Sorting

1/87

Earn XP

Description and Tags

Last updated 11:47 PM on 4/29/23

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

88 Terms

1

New cards

what does ceteris paribus mean

it means “assuming all other things stay the same”. You use it when analyzing an isolated shock to indicate that you are only assuming the specific shock is what caused the change

2

New cards

what are the 4 factors of production (FOPs)

land, labour, capital, and entrepreneurship

3

New cards

who can own FOPs and what are the reasons that each owner produce goods

they can be publicly (government) or privately (companies) owned, public sector produces goods that will better society eg. health care, the private sector produces to gain profits

4

New cards

what are the 3 types of capital

physical capital, human capital, financial capital

5

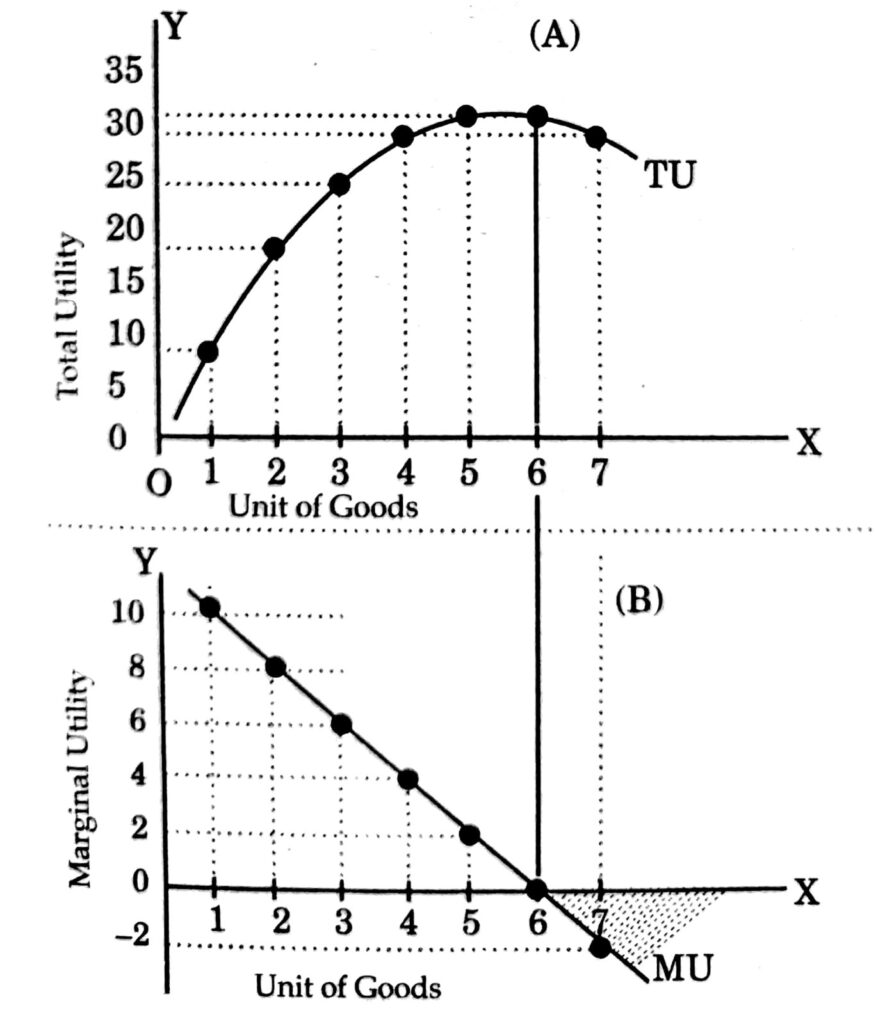

New cards

define marginal utility

the amount of additional satisfaction each extra unit of a good produces when consumed

6

New cards

explain the law of diminishing marginal utility

as more of a good is consumed each additional unit will provide less satisfaction than the last

7

New cards

define opportunity cost

it is the cost of making a decision on how to use scare resources; the cost of deciding. It is the cost of giving up the next best option

8

New cards

define free goods vs economic goods

there is an infinite access to the resources required to produce the good and they do not cause an opportunity cost eg. oxygen, sunlight, sunset

vs

they use scarce resources in their production and there is always an opportunity cost to make them

vs

they use scarce resources in their production and there is always an opportunity cost to make them

9

New cards

define capital goods

goods created to produce other goods eg. machinery

10

New cards

define consumption goods

goods used for final consumption to directly satisfy a need/want eg. food, clothing

11

New cards

what is the purpose of a ppf

to show us how much or what combination an economy can produce of 2 goods with a certain amount of FOPs

12

New cards

where is inefficient on a ppf, where is efficient, and where is unattainable

anywhere along the ppf curve FOPs are being used efficiently, below the ppf curve they are being used inefficiently, and producing an amount above the ppf curve is impossible because there is not enough FOPs available

13

New cards

define GDP - gross domestic product

a monetary measure of the market value of all the final goods and services produced and sold in a specific time period by a country or countries, usually measured each year

14

New cards

economic growth

the rate of change is the output (production of goods and services) of a given country from one year to the next measured in monetary terms. Change in GDP.

15

New cards

what is the result of investing in capital goods

investing in them will increase your FOPs and increase your capacity for production which will shift out the curve of the ppf and therefore increase GDP

16

New cards

what is industrialization

when a country starts to produce more capital goods than consumption goods to invest in the future of their economy

17

New cards

what is economic development

the process of improving the quality of human life by increasing income, reducing poverty, bettering education, improving health care, etc.

18

New cards

explain the difference between economic growth vs economic development

the rate of change is the output (production of goods and services) of a given country from one year to the next measured in monetary terms

vs

the process of improving the quality of human life by increasing income, reducing poverty, bettering education, improving health care, etc.

vs

the process of improving the quality of human life by increasing income, reducing poverty, bettering education, improving health care, etc.

19

New cards

explain the difference between increasing productivity vs increasing production

increasing productivity involves using FOPs more efficiently eg. use tech to produce faster

vs

increasing production involves utilizing unused FOPs or gaining more FOPs to increase the amount you are able to produce

vs

increasing production involves utilizing unused FOPs or gaining more FOPs to increase the amount you are able to produce

20

New cards

define public goods

goods or services not provided by private investment or the free market eg. national security, roads and bridges, etc. which means that the government must produce them

21

New cards

define merit goods, their production, and their main characteristics

goods that are beneficial to society but are underproduced by the free market considering what society needs. eg. health care, education, etc. they. are underproduced by the free market because consumers may not be able to afford or feel the need to buy them. merit goods have positive externalities in consumption that may be ignored by the consumers eg. libraries, museums, etc.

22

New cards

define sustainable development

development that is able to provide for and meet the needs of current generations without compromising the ability to meet those needs for future generations

23

New cards

define demand

the relationship between price, and the quantity of what consumers are willing and able to pay for a good/service

24

New cards

state the law of demand

the law of demand states that price and quantity demanded of a good have a negative relationship because as the price of a good increases the QD decreases, and vice versa.

25

New cards

what are exogenous variables

a factor outside of the demand function that affects quantity demanded for example weather, income, population, etc. Anything other than price

26

New cards

what are endogenous variables

a factor within the demand function that effects quantity demanded. This can only be price.

27

New cards

what is a veblen good and what is its relationship with the law of demand

is is a good where quantity demanded increases as price increases. this can because consuming the good will show status/it is a popular good, or because the value of the good is expected to rise as you own it for longer eg. gold it is an exception to the law of demand because quantity demanded increases as price increases.

28

New cards

what is a giffen good and what is its relationship with the law of demand

it is a good with no substitute that people consume even as the price rises. for example potatoes that low income people buy regardless of price because everything else is still more expensive

29

New cards

define supply

the willingness and ability for producers to produce a good at a given price. The relationship between quantity supplied and it price

30

New cards

what are the determinants of supply

price of FOPs and resources

government intervention eg. taxes + subsidies

number of suppliers in the market

state of technology

\

\

government intervention eg. taxes + subsidies

number of suppliers in the market

state of technology

\

\

31

New cards

state the law of supply

the higher the price of a good in the market, the more incentive to increase the quantity supplied, ceteris paribus. Therefore the as price of a good increases, so does the quantity produced

32

New cards

what are 3 things needed for markets to reach equilibrium

there must be many buyers and sellers so one single firm cannot influence the price, there must be free competition and no barriers to enter the market, and it must be the same good and price is the only thing determining demand

33

New cards

market disequilibrium: what happens if the price is above the equilibrium

if price is above the equilibrium supply is increased however there aren't enough people willing and able to pay the price so there is an overproduction of the good which creates an excess of production

34

New cards

market disequilibrium: what happens if price is below the equilibrium

if market price is below the equilibrium there are many people willing and able to pay that price however there is not enough of an incentive to produce the good so this creates a shortage

35

New cards

how do markets achieve equilibrium on their own

when a price is too high one supplier will lower their price to entice consumers and other producers will compete with that price, lowering it until equilibrium is reached. if the price is too high, consumers will bid up the prices, producers will produce more at new higher prices until equilibrium is reached

36

New cards

what is allocative efficiency

an allocation of resources that allows production to align with a state where production aligns with consumer wants and, and for each good produced its marginal cost of production is equal to the selling price. this can also be defined as when P=MC

37

New cards

how will an an exogenous shock on supply affect demand

an exogenous shock on supply with create an endogenous shock on demand

38

New cards

how will an exogenous shock on demand affect supply

an exogenous shock on demand with create an endogenous shock on supply

39

New cards

define consumer surplus

the value of the difference between what consumers are willing and able to pay and what they actually pay

40

New cards

define producer surplus

the value of the difference between what producers are willing and able to sell at and what they actually sell at

41

New cards

define social welfare

consumer surplus and producer surplus together, the amount the society is benefitting from the price at the time

42

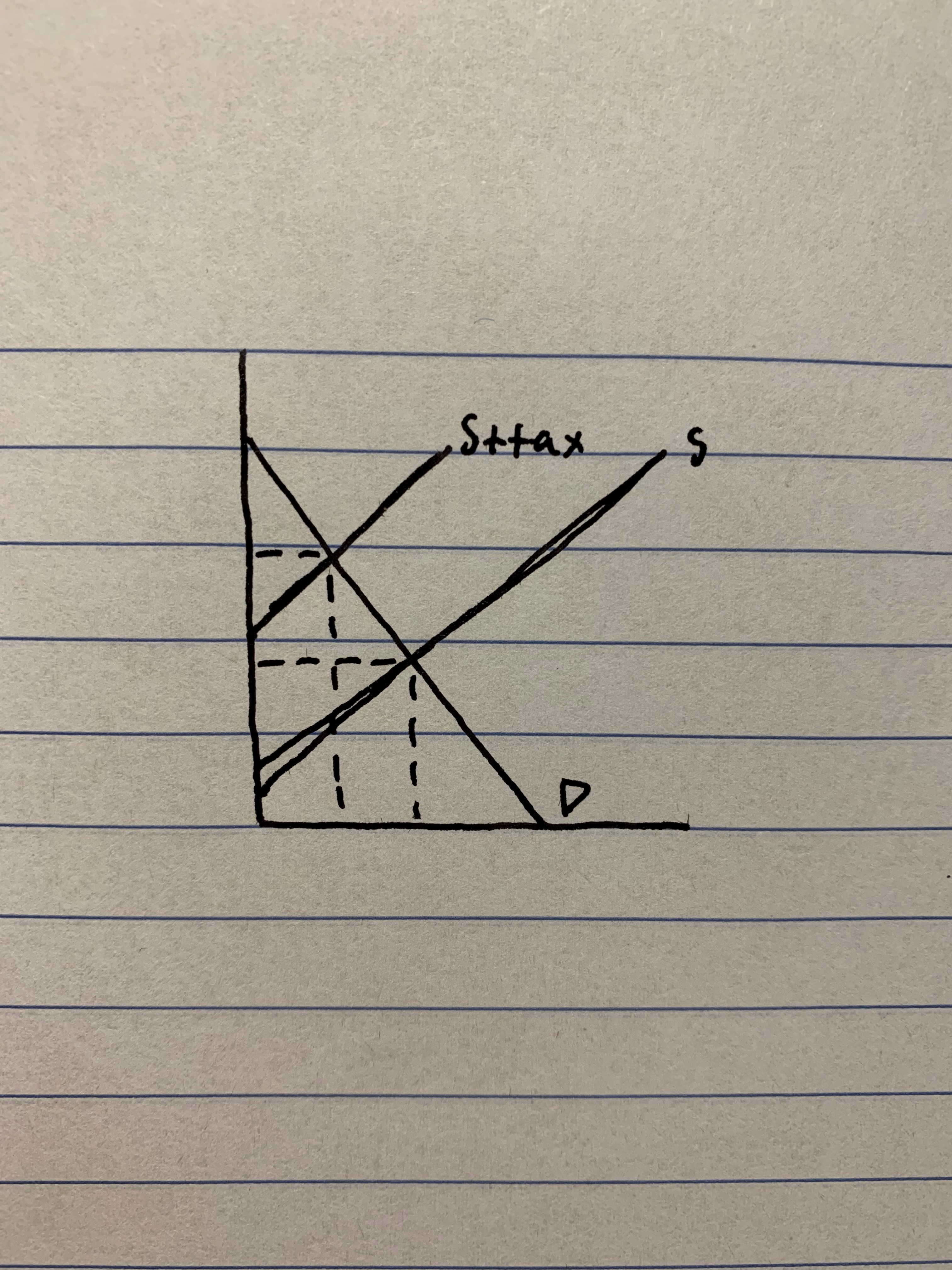

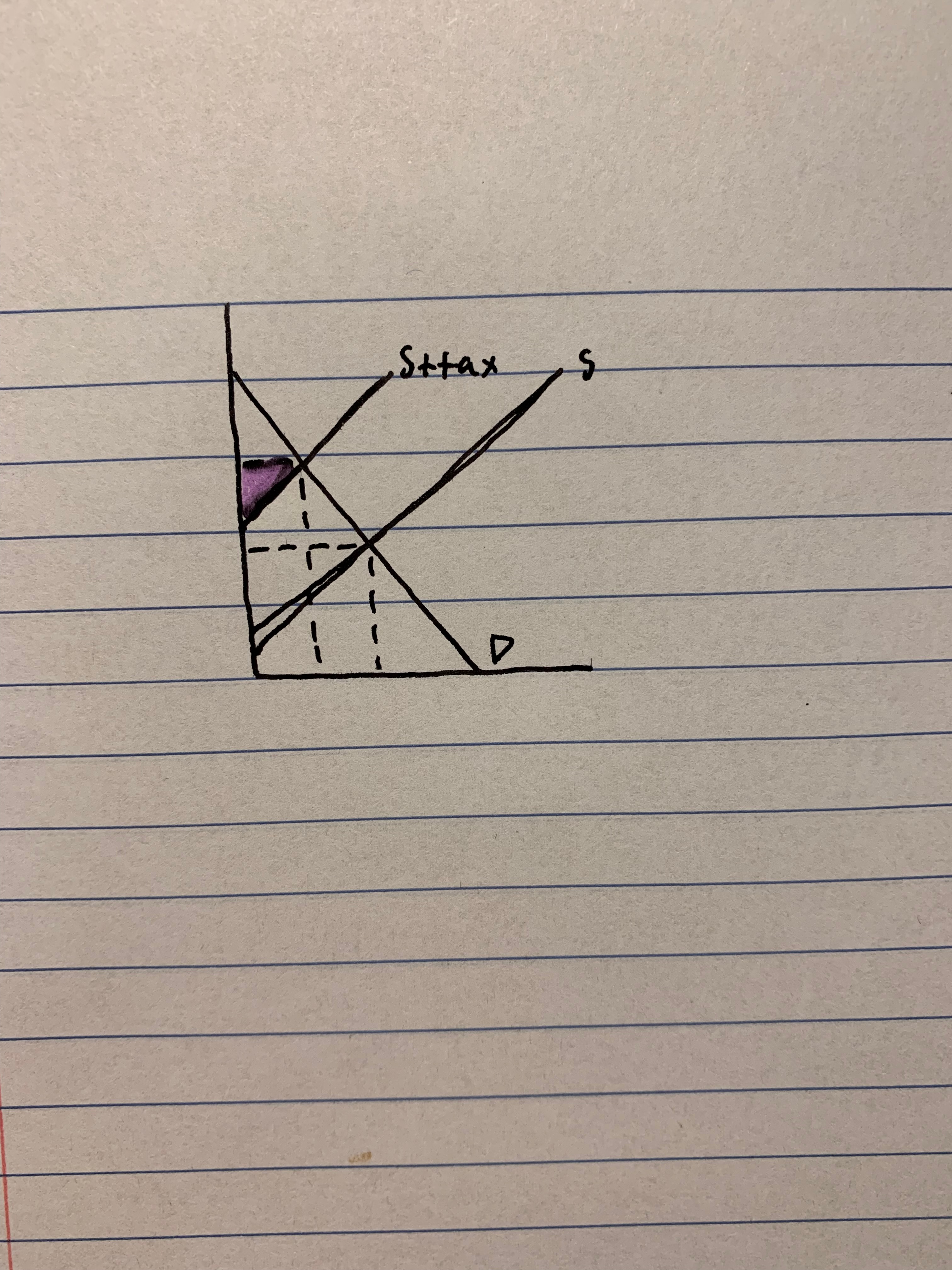

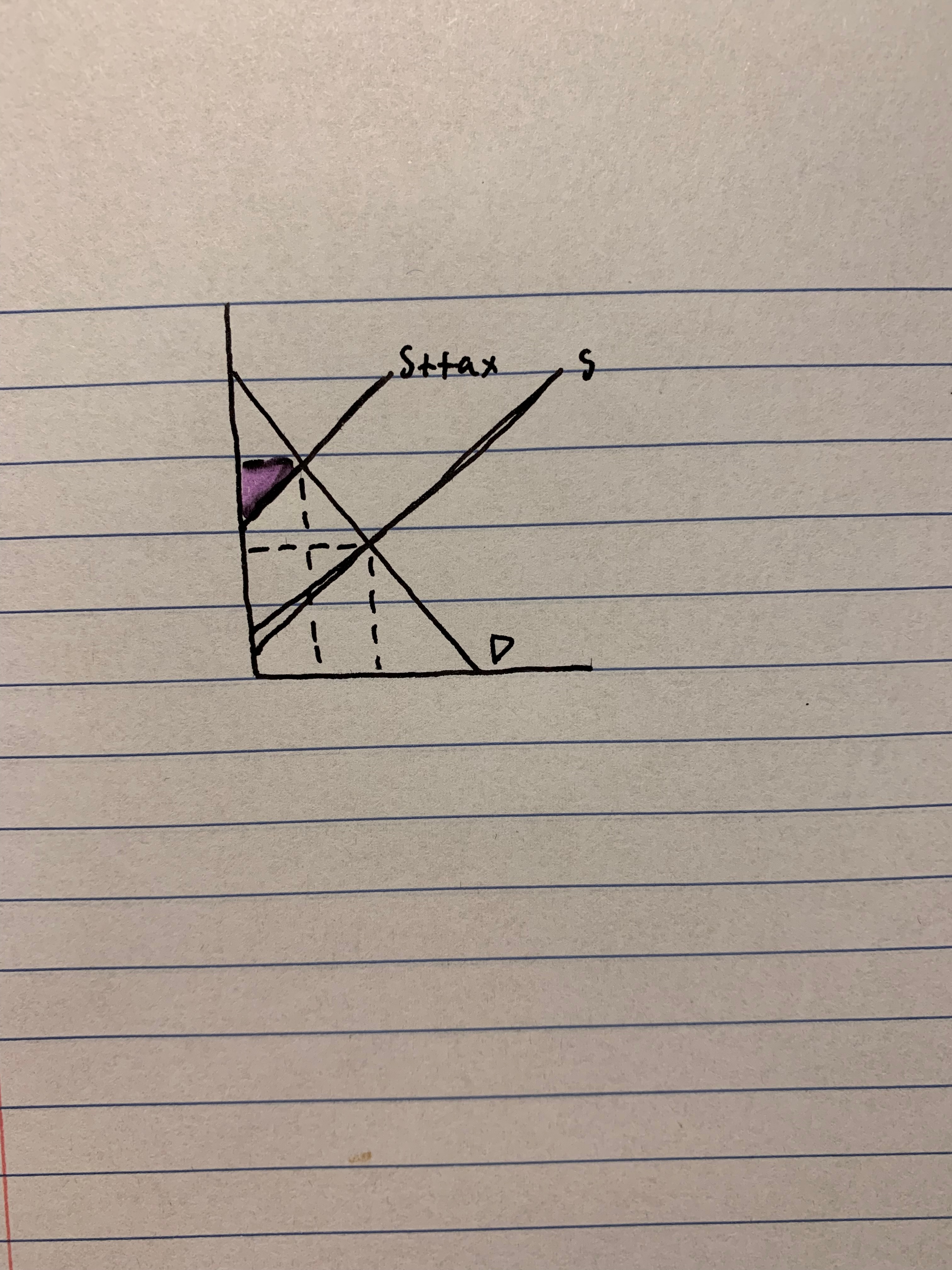

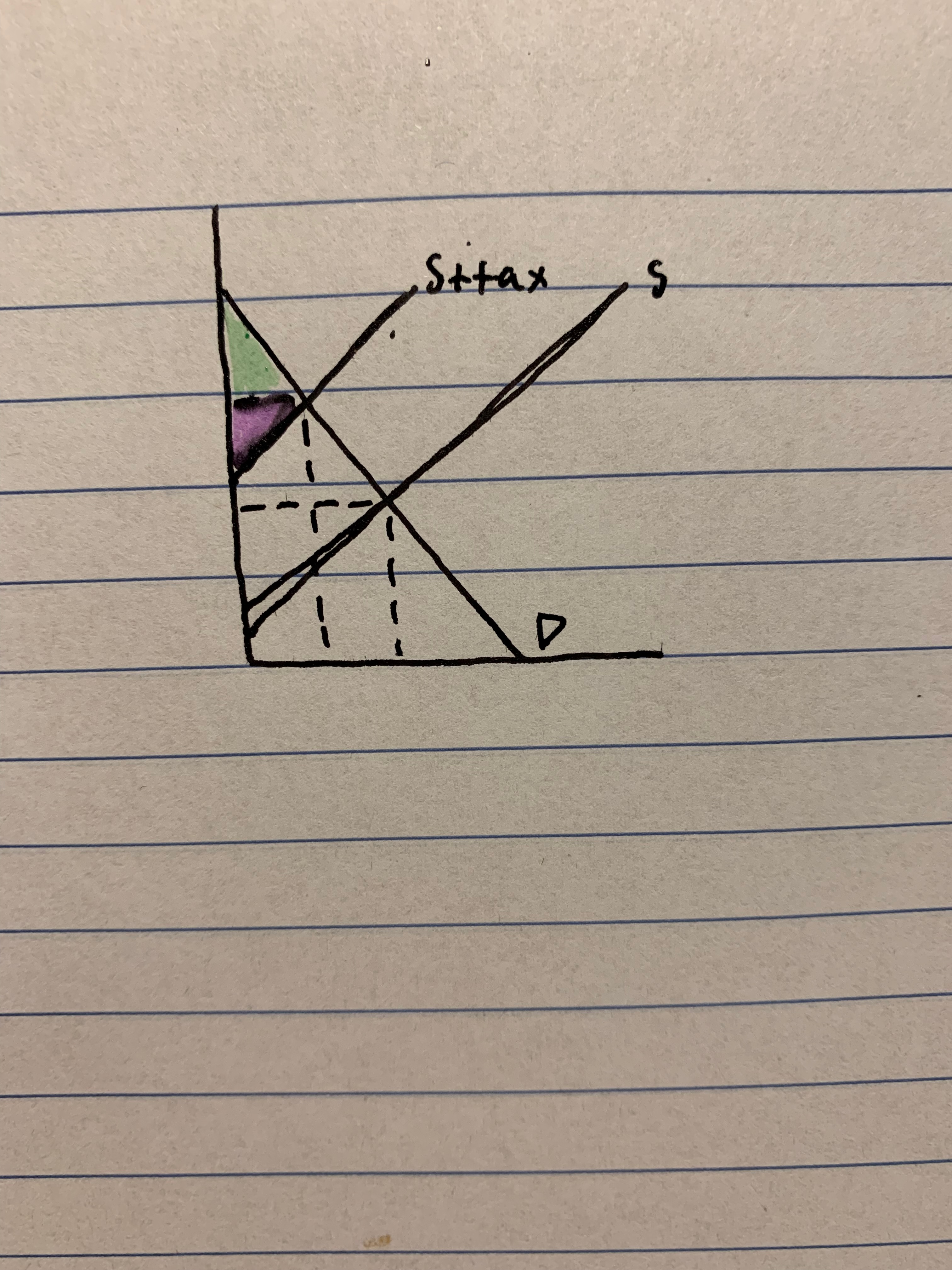

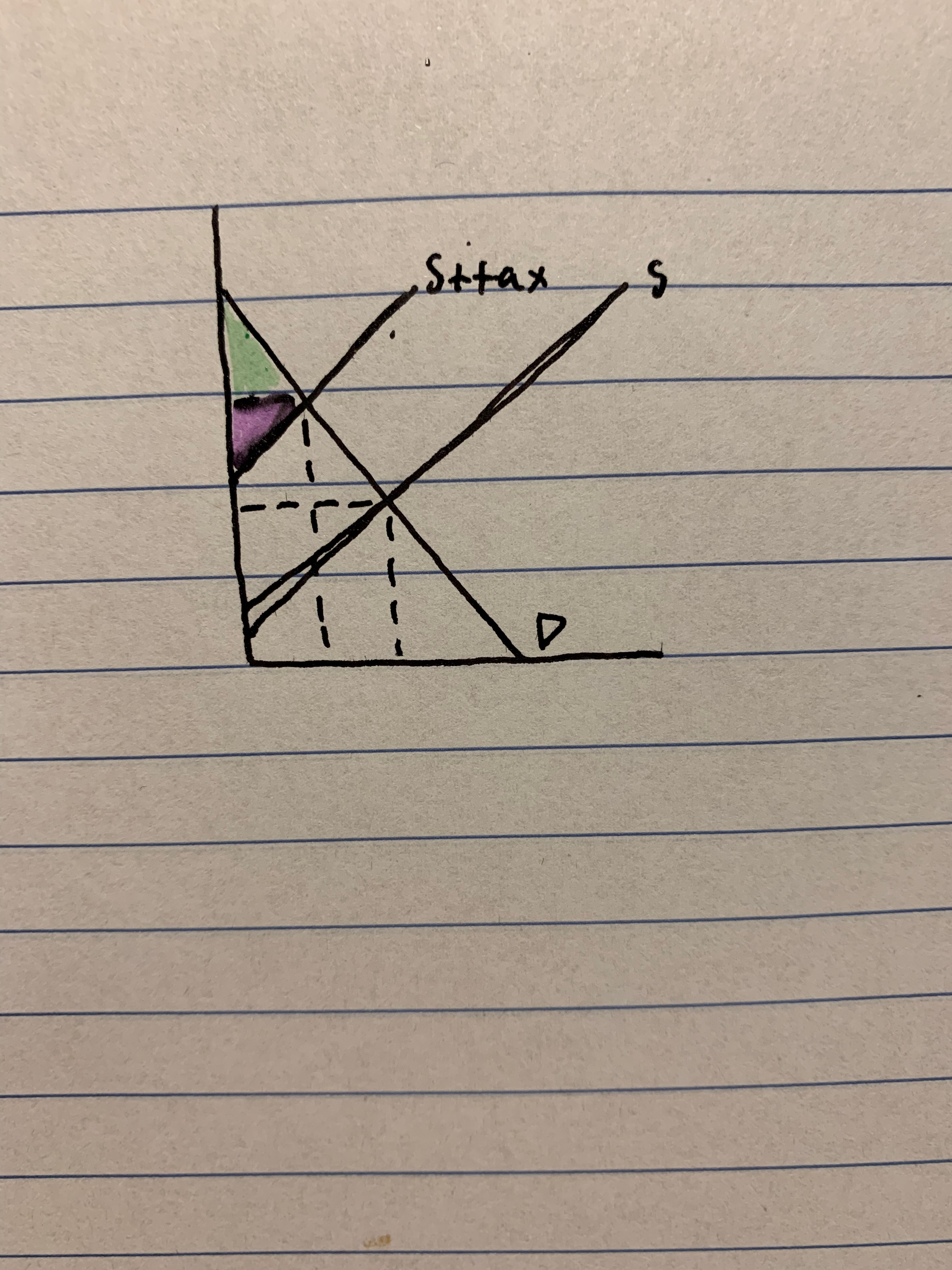

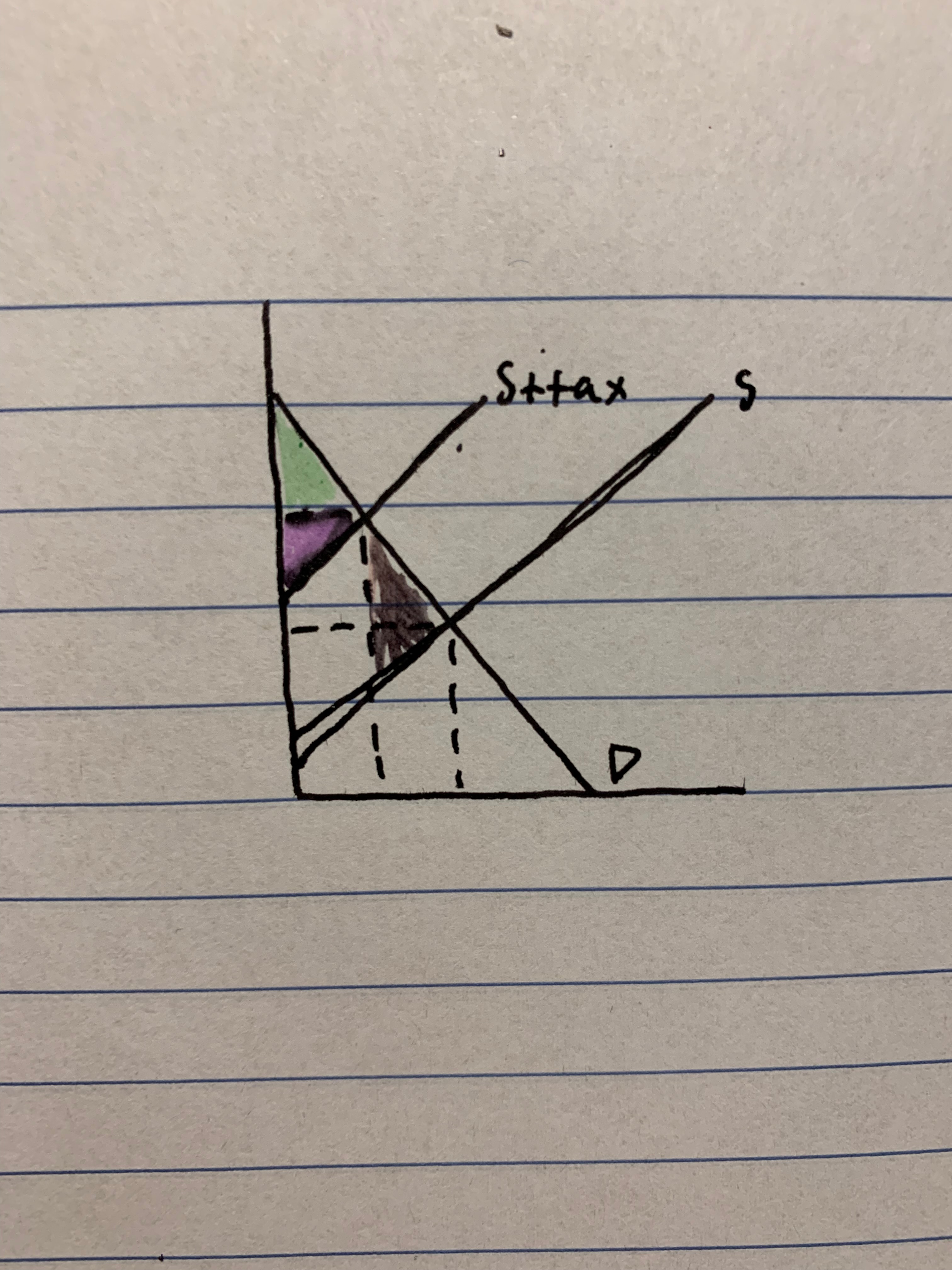

New cards

identify producer surplus after the tax

43

New cards

identify consumer surplus after the tax

44

New cards

identify welfare loss after the tax

45

New cards

what is welfare loss

a cost to society created when the market is not operating at the equilibrium. It is the loss of a portion of the social welfare due to market failure and MSC not equalling MSB

46

New cards

what is economic efficiency

when equilibrium is met all goods and FOPs are distributed, allocated, and produced to their most valuable uses and waste is eliminated. when allocative and productive efficiency is reached. when MSB is equal to MPB or when MSC is equal to MPC. When the Pareto Optimum is reached and when social welfare is maximized. WHEN ALLOCATIVE EFFICIENCY IS REACHED

47

New cards

what type of diagram do you use to illustrate allocative efficiency?

supply and demand

48

New cards

what type of diagram do you use to illustrate productive efficiency

a PPF

49

New cards

what are the 2 types of taxes

direct and indirect

50

New cards

what is a direct tax

a tax on income or profits of a person

51

New cards

what are the 2 types of indirect taxes

fixed tax and ad valorem tax

52

New cards

what is a fixed tax

when the tax is a the same amount no matter the price of the good

53

New cards

what is an ad valorem tax

when the tax is a percentage of the price of a good, so as the price increases, the tax also increases

54

New cards

what is a subsidy

it is money granted by the government to producers to assist the industry or business and decrease the cost of production so that the final price can be lower for consumers

55

New cards

using demand and supply, and quantity and price explain the effect of a tax on cigarettes

a tax will increase the cost of production which will shift the demand curve in causing the final sale price to be higher than before, therefore because of the law of demand less people will be willing and able to buy cigarettes

56

New cards

using demand and supply, and quantity and price explain the effect of a subsidy on electric cars

a subsidy will decrease the cost of production which will shift the demand curve out causing the final sale price to be lower than before, therefore because of the law of demand more people will be willing and able to buy electric cars

57

New cards

explain a price ceiling

opposite of what you think! it is set by the government BELOW the equilibrium price, it is the maximum price producers are allowed to sell at

58

New cards

explain a price floor

opposite of what you think! it is set by the government ABOVE the equilibrium and it is the lowest price producers are allowed to sell at

59

New cards

explain why a government would want to set a price ceiling

price ceilings are set when the price becomes too high compared to what the government thinks it should be. the price ceiling is set BELOW the equilibrium to try and lower the market prices

60

New cards

explain why a government would want to set a price ceiling

price ceilings are set when the price becomes too low compared to what the government thinks it should be. the price ceiling is set ABOVE the equilibrium to try and raise market prices

61

New cards

what is the definition of a monopoly and describe the characteristics

a Monopoly is when there is one dominant seller of a good.

high barriers to enter

cannot be other close substitutes

no supply curve in a diagram because the 1 firm can just determine the price as they wish and consumers must pay that price if they want the good

high barriers to enter

cannot be other close substitutes

no supply curve in a diagram because the 1 firm can just determine the price as they wish and consumers must pay that price if they want the good

62

New cards

what is the definition of a oligopoly and describe the characteristics

the same as a monopoly (when there is one dominant seller of a good.

high barriers to enter

cannot be other close substitutes

no supply curve in a diagram because the 1 firm can just determine the price as they wish and consumers must pay that price if they want the good)

but with a few large firms dominating the market, can collude and act as a monopoly

high barriers to enter

cannot be other close substitutes

no supply curve in a diagram because the 1 firm can just determine the price as they wish and consumers must pay that price if they want the good)

but with a few large firms dominating the market, can collude and act as a monopoly

63

New cards

what is monopolistic competition

large amounts of firm producing similar goods that are differentiated, they can set the price and share the market by differentiating their products, and entry barriers are particularly low. almost every market we know eg. shoes, pens, cars, etc.

64

New cards

what is the difference between perfect competition and monopolistic competition

in perfect competition, firms produce exactly the same goods, the only difference is the prices, and in monopolistic competition, firms produce the same goods but with different characteristics

65

New cards

what is elasticity of demand

a measure of the responsiveness of the quantity demanded of a good in respect to a change in the price of a good. how much will QD change proportionally compared to the change in price. if price goes up how willing are people to still buy it?

66

New cards

what determines how elastic demand is (3 things)

1. how available perceived alternatives are

more substitutes available means more elastic

2. how much time you have to find an alternative

shorter time period to find an alternative makes a good more inelastic

3. the proportion of income spent on the good

the smaller the proportion of income spent on it the more elastic it is (the less people will respond to a price change)

67

New cards

on a linear demand curve where are the different areas of elasticity?

the top half is elastic

middle is unit elastic

bottom half is inelastic

middle is unit elastic

bottom half is inelastic

68

New cards

describe the characteristics of an inelastic good in regards to revenue vs price change

total revenue will decrease when price decreases and total revenue will increase when price increases, this is because a price change will result in a small change in amount of people buying it

69

New cards

describe the characteristics of an elastic good in regards to revenue vs price change

revenue will increase when price decreases and vice versa, this is because a price decrease will result in a high proportion of people buying it

70

New cards

what is a superior good

it is a good with an elasticity greater than 1, so a small percent change in income will result in a large percent change in quantity demanded

71

New cards

what is the relationship between superior goods and income

as income increases so will the quantity demanded of superior goods

72

New cards

what is an inferior good

they are necessities or goods that no matter your income you will need the same amount of it, they are unit elastic or inelastic goods

73

New cards

what is the relationship between income and inferior goods

as income increases you will buy less inferior goods and as income decreases you will buy more inferior goods because they may be substitutes for other superior goods

74

New cards

define price elasticity of supply

the ability and capacity for producers to provide more or less of a good in response to a change in price, how responsive is quantity supplied to a change in price

75

New cards

what are the 2. determinants of supply elasticity

1. time period, if the goods can be changed and produced quickly, the producers can respond quickly to a change in price which makes a shorter time period good more elastic

2. the availability of FOPs, the less available they are the more inelastic it will be.

76

New cards

define market failure

market failure occurs when the free market fails to achieve efficiency or when resources are not allocated properly. market failure occurs when the pareto optimum is not reached or when the equilibrium is not met. it can also be defined by the fact that social welfare is not maximized and when MSB does not equal MSC

77

New cards

define productive efficiency

when goods are produced at the lowest possible cost per unit and resources are used at their best capacity to produce

78

New cards

what are the reasons and root causes for market failure

markets fail because of

public and merit goods also known as missing markets

lack of competition

externalities in production and consumption, and common access resources

information failure

poverty and inequality in an economy

public and merit goods also known as missing markets

lack of competition

externalities in production and consumption, and common access resources

information failure

poverty and inequality in an economy

79

New cards

define the Pareto optimum, or Pareto efficiency

pareto optimum is said to be achieved when no economic changes can make one individual better off without making someone worse off. It is the point in the economy where society wants to produce

80

New cards

define externality

an externality is a benefit or cost to a third party that is the result of the production or consumption of a good

81

New cards

what is a positive externality in production

a positive externality in production happens when MSC is lower then MPC, so the production of a good gives more benefits to the society as a whole than it does to the producer

82

New cards

what is a negative externality in production

a negative externality in consumption is when MSC is larger then MPC, so the cost to society is larger than the cost it takes for someone to produce the good

83

New cards

what is a positive externality in consumption

a positive externality in consumption is when a third party receives a benefit that they do not pay for because of the consumption of a good, so MSB is larger than MPB and the benefit to society is greater than the benefit to the individual consuming the good

84

New cards

what is a negative externality in consumption

a negative externality in consumption means that the MSB is lower than the MPB, so the individual consuming the good is receiving more benefit than the society

85

New cards

what is a Pigouvian tax

it is a specific tax aimed to correct market failures and and offset negative externalities

86

New cards

define a merit good

good that is desirable for consumers but is under-provided by the free market. this could be because

there is a positive externality in consumption

consumers with low income cant afford it

or the benefits of the good are ignored

there is a positive externality in consumption

consumers with low income cant afford it

or the benefits of the good are ignored

87

New cards

define a demerit good

a good that is bad for consumers but is over-provided by the free market. they may be over-provided because there is a negative externality in consumption or the negative effects of them are ignored

88

New cards

what are the determinants of demand

income

price of substitute goods

price of complimentary goods

population

\

price of substitute goods

price of complimentary goods

population

\