L6 - Hidden Dynamics

1/35

Earn XP

Description and Tags

behalve state space models

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

36 Terms

So what is the focus of this week’s lecture?

Hidden Dynamics

What are the two flavours of Hidden Dynamics?

What are the four challenges in applying models with hidden dynamics?

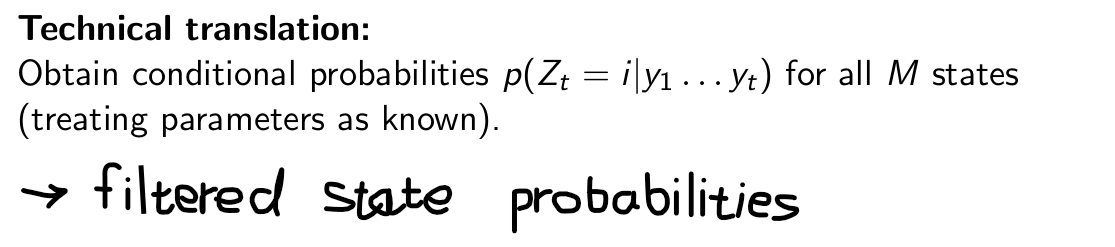

What is the technical translation of this? Which term is it related to?

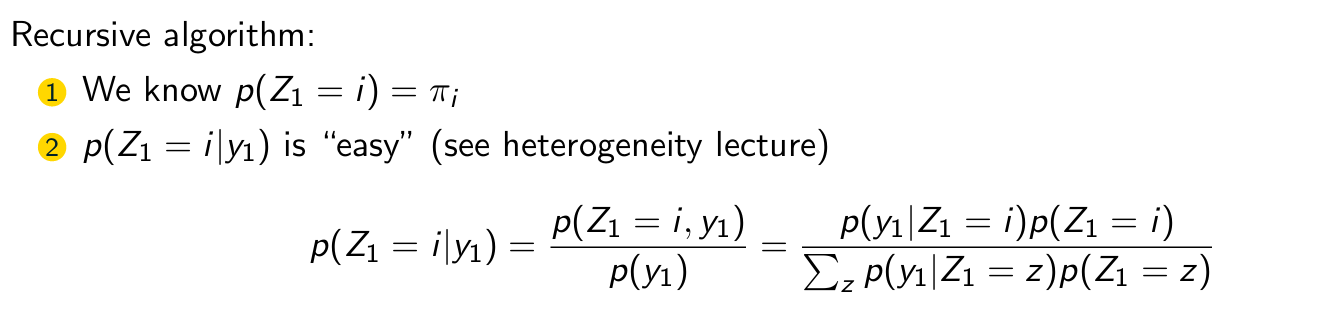

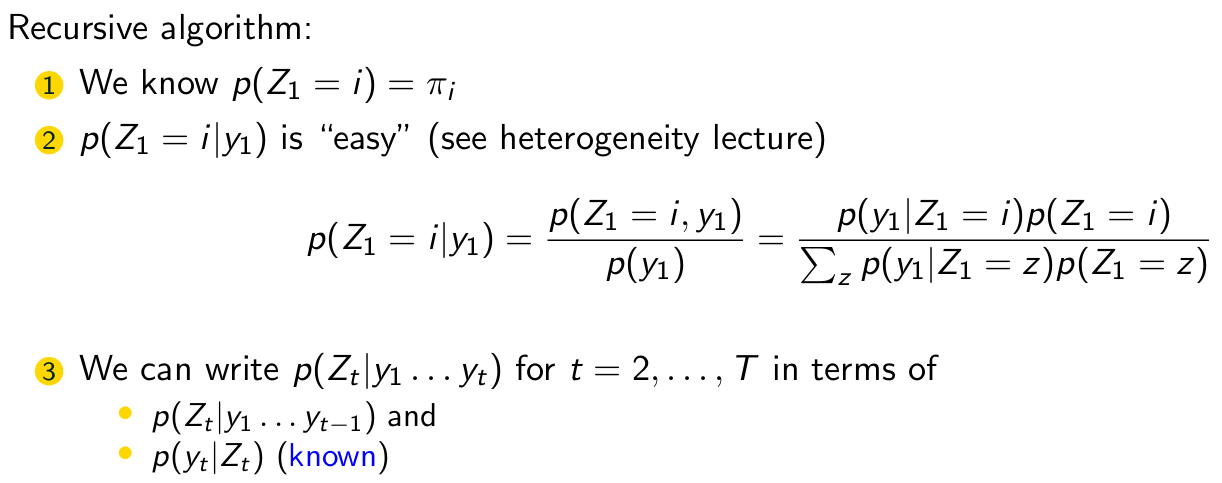

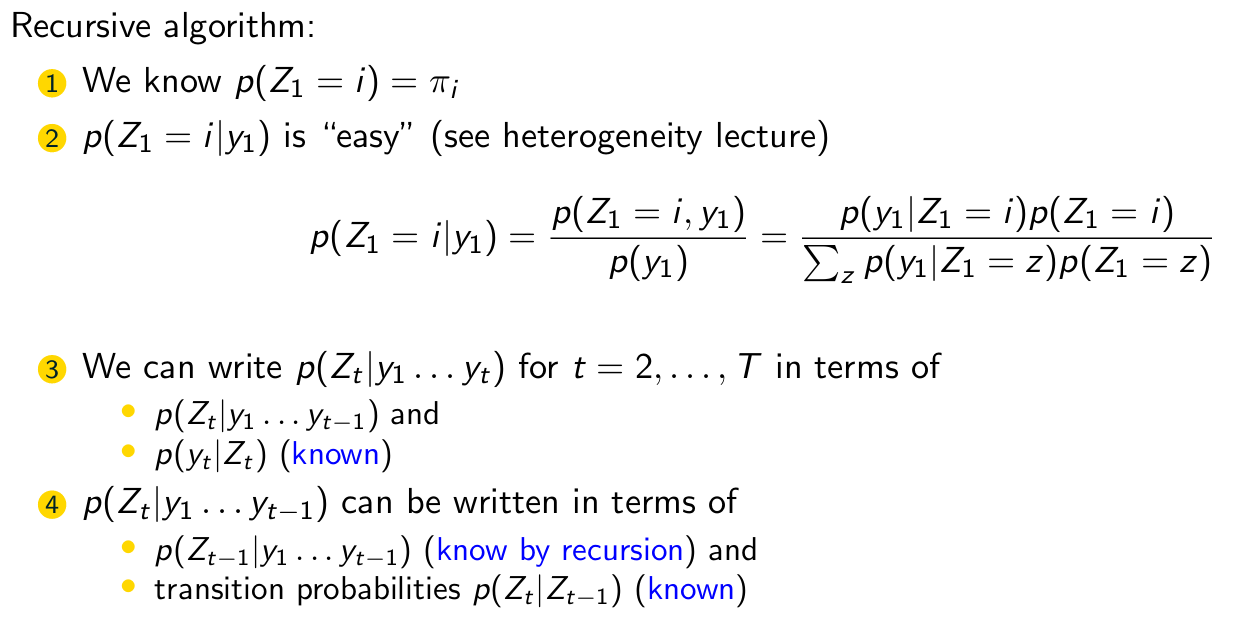

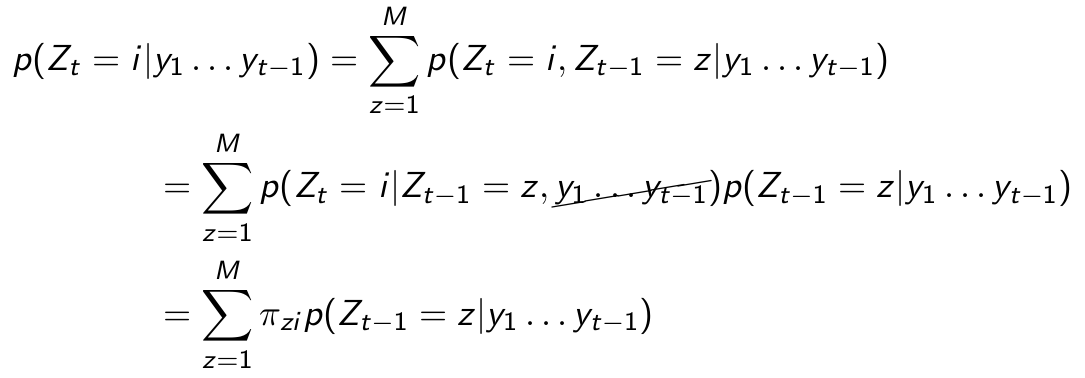

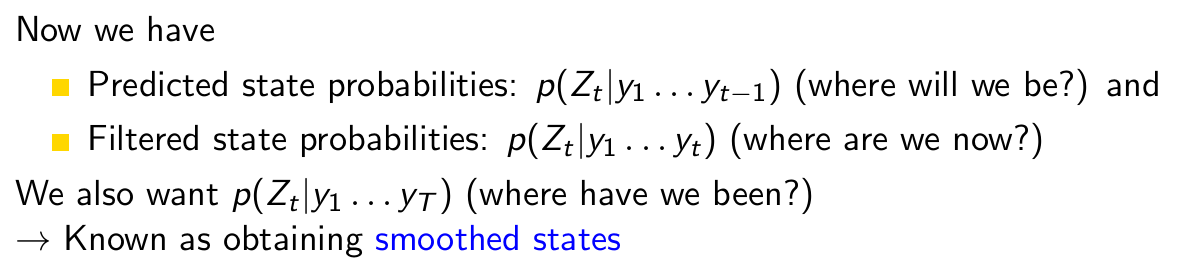

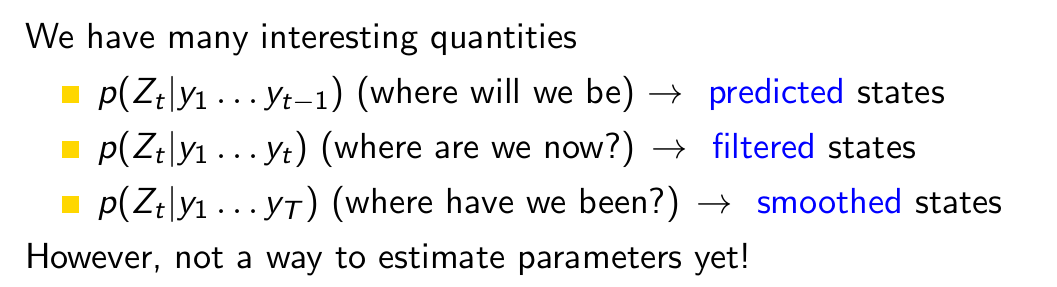

Let’s take a look at the big picture for the filtered state probabilities. What are step one and two of the algorithm?

Let’s take a look at the big picture for the filtered state probabilities. What is step three of the algorithm?

Let’s take a look at the big picture for the filtered state probabilities. What is step four of the algorithm?

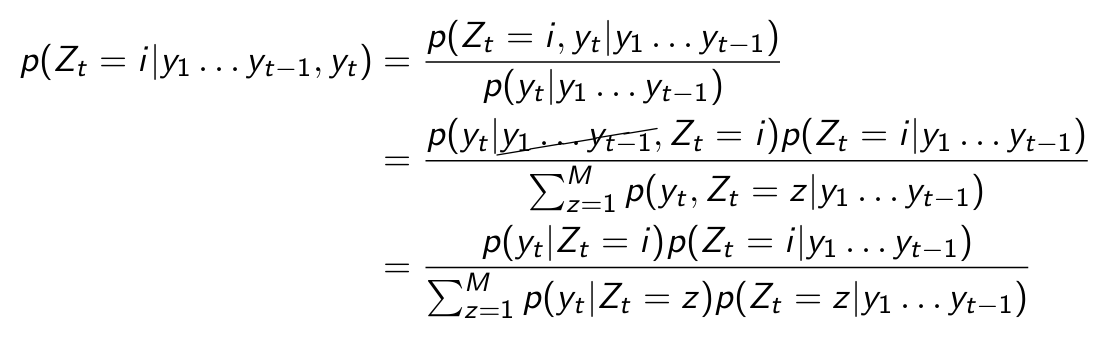

Perform step three.

Perform step four.

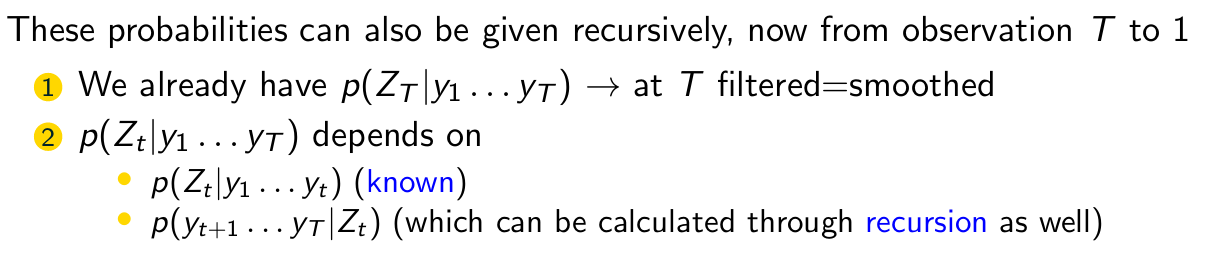

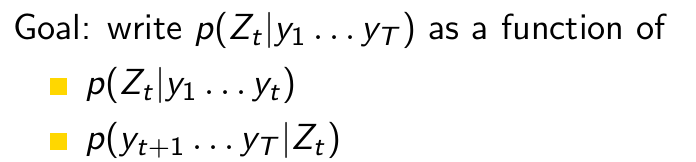

What are step one and two for the recursive algorithm for smoothing?

Do this.

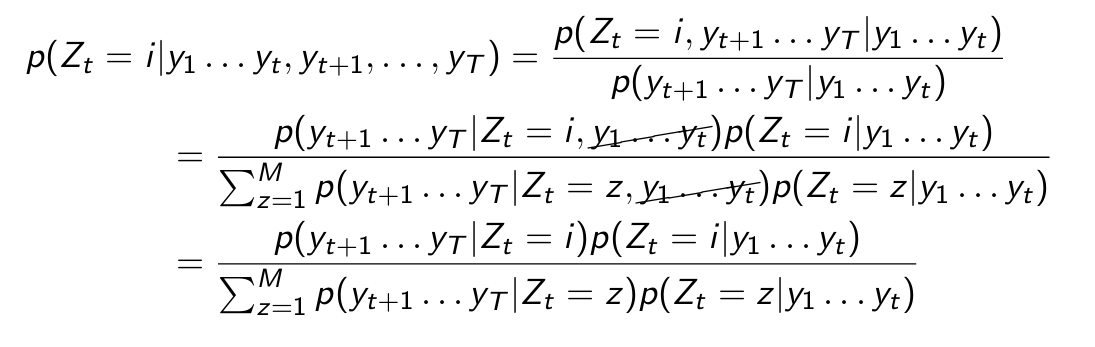

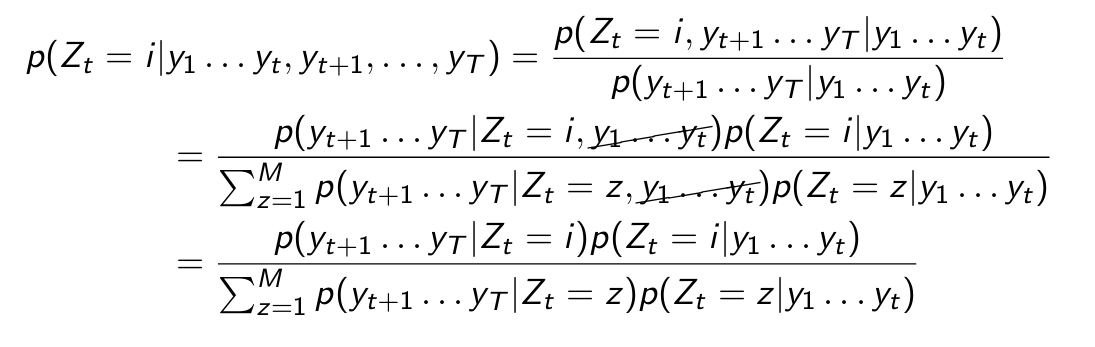

What is the “problem” here?

p(yt+1 ...yT|Zt = i) is not yet known!

But it can also be recursively calculated.

So how do we do this?

Maximizing the log likelihood directly is (very) complex.

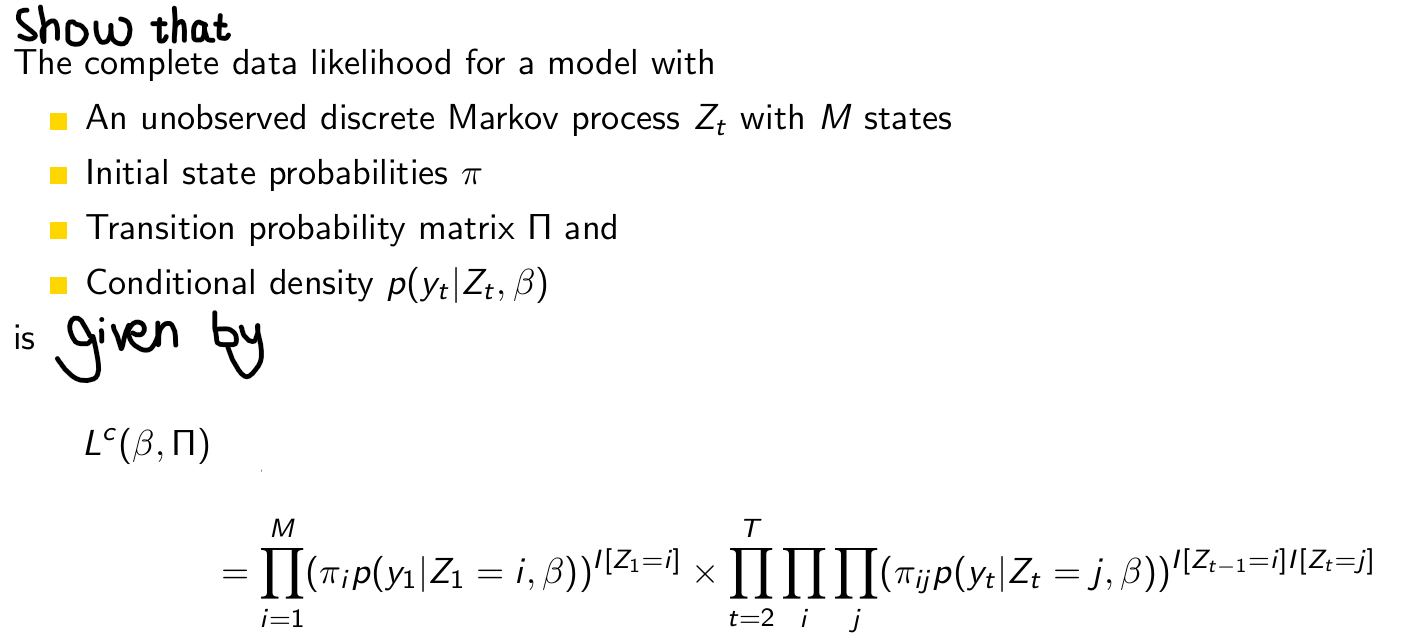

Familiar solution: Complete data likelihood & EM algorithm.

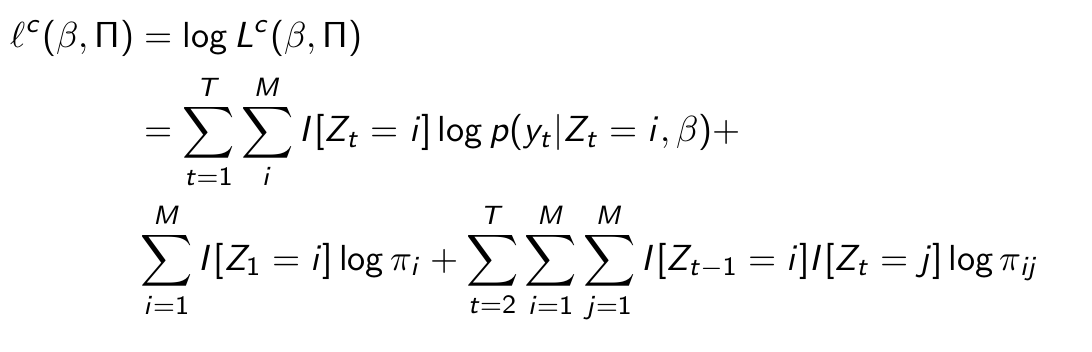

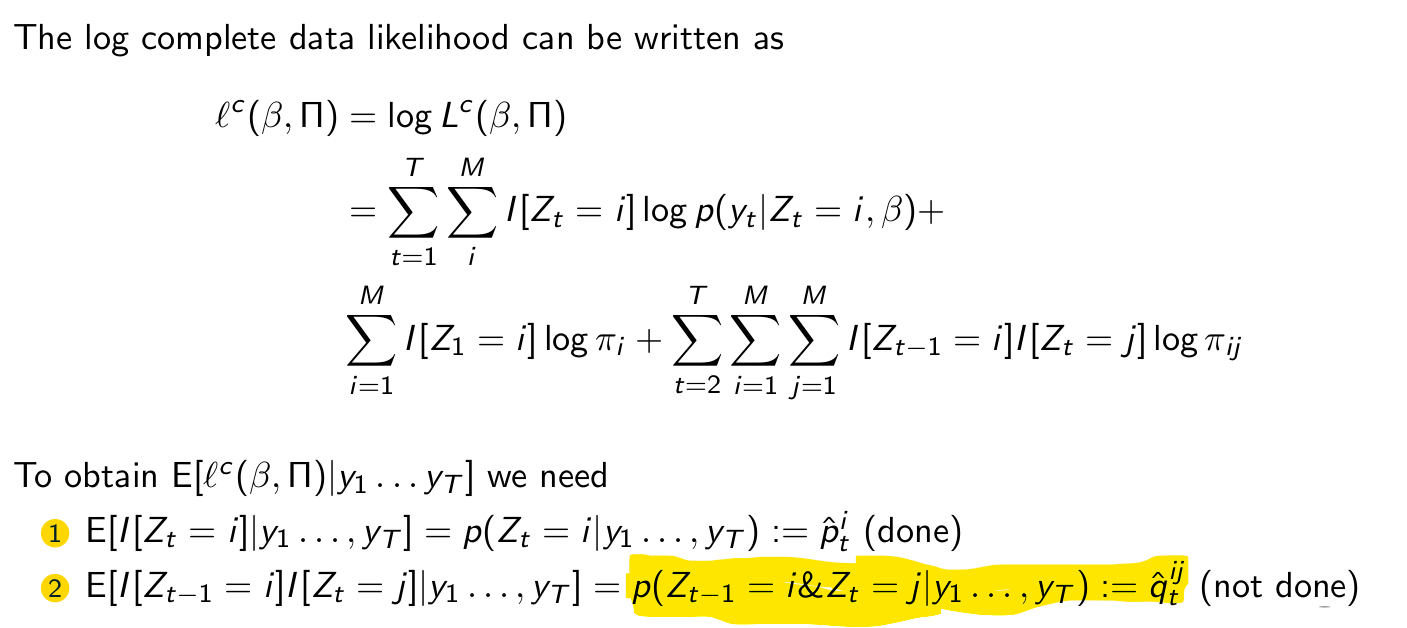

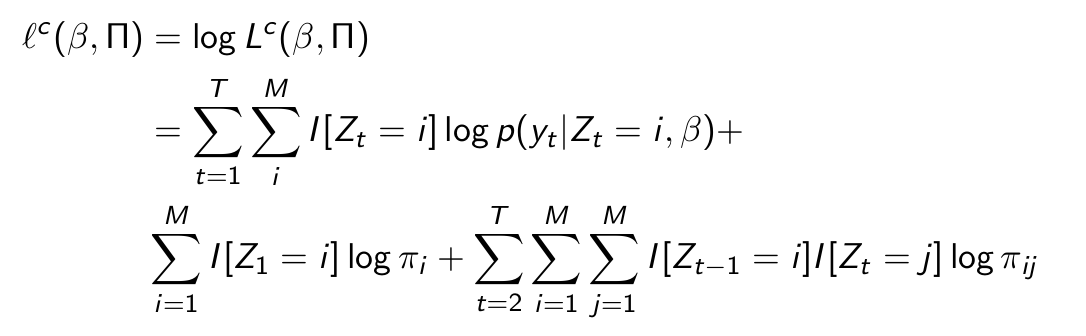

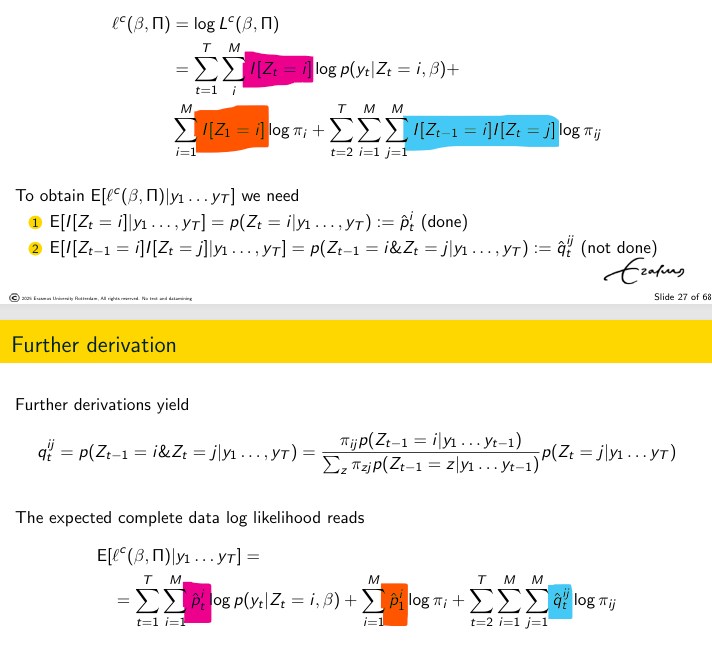

What is the LOG complete data likelihood?

Write this out further.

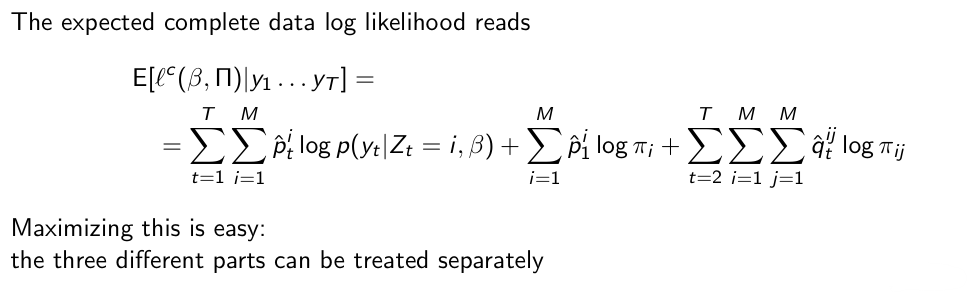

What is the expectation of this conditional on all the data?

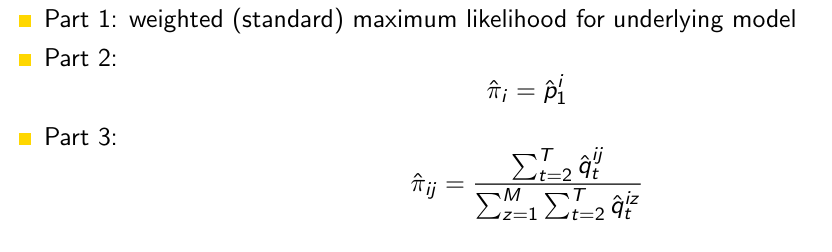

What do the three parts give us?

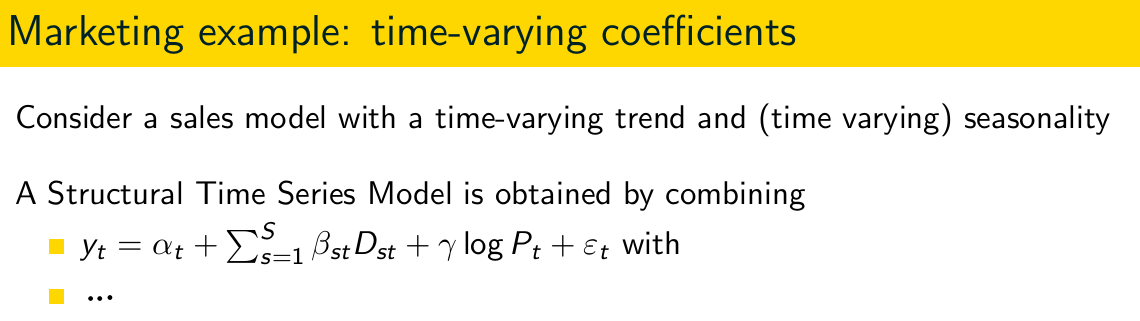

In a structural time series model, the time series can be decomposed into …

What can we say about these components? What does this imply for the model?

Components are unobserved, but have a direct interpretation! They may change over time —> Models often imply non-stationarity

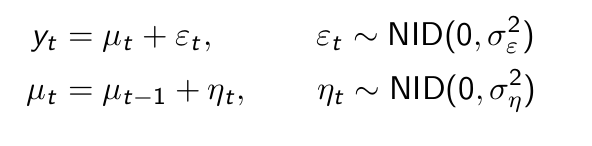

What is the most simple STSM?

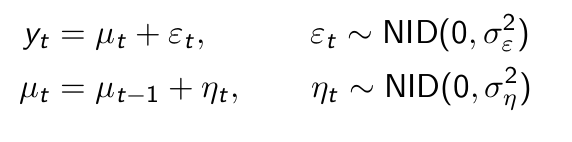

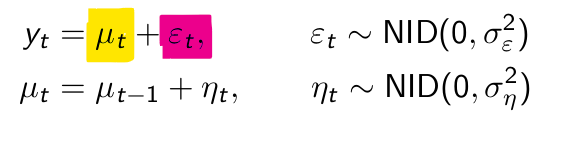

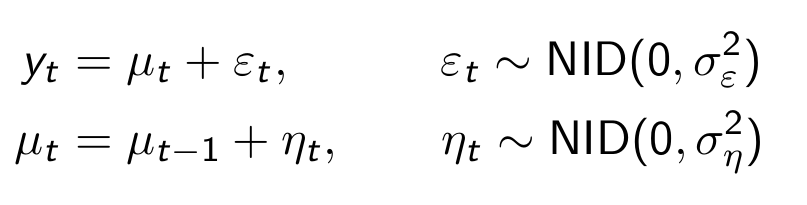

Local level model

What are these called?

The local level and the irregular component

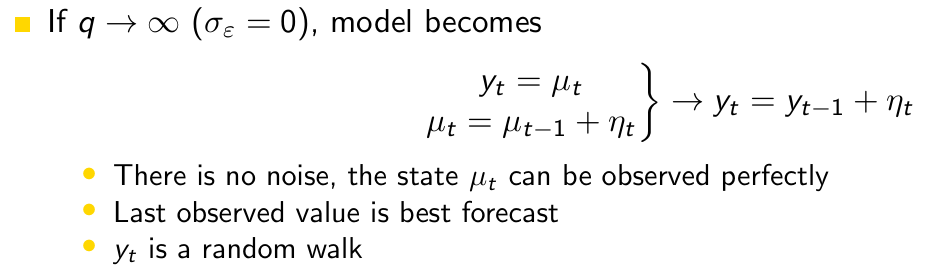

What is the best forecast for yt if the signal to noise ratio is 0?

What is the best forecast for yt if the signal to noise ratio is really, really large?

What is the best forecast for yt for a regular value of the noise ratio?

For less extreme signal-to-noise ratios the forecast becomes a weighted average of the previous values (the “local level”).

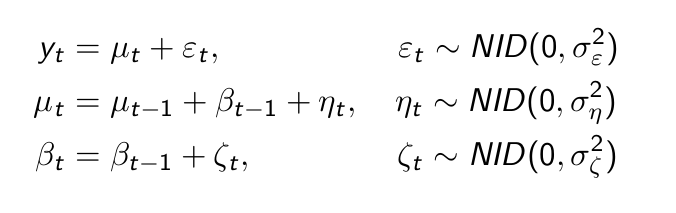

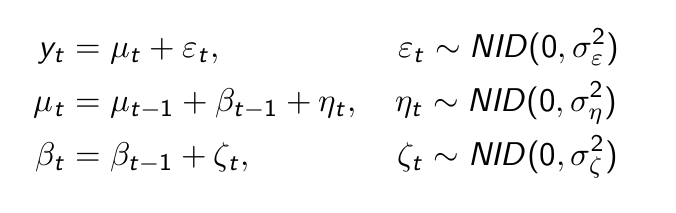

Augment the local level model by allowing for a trend that can change over time.

When does this model become a deterministic trend?

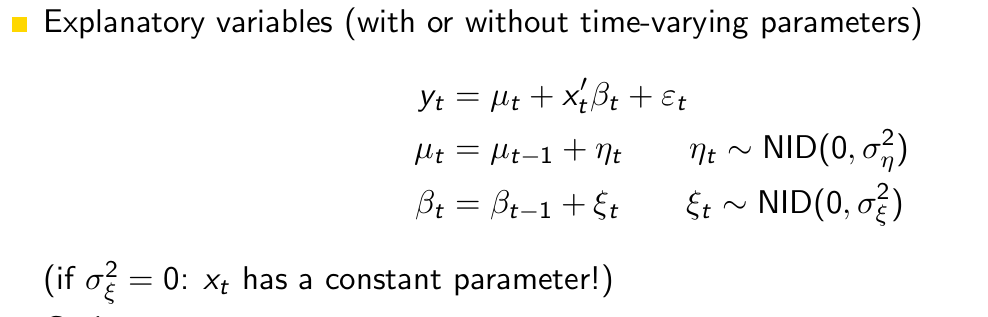

How would the model look if we added explanatory variables?

In what other ways could we extend the local level model except a trend and explanatory variables?

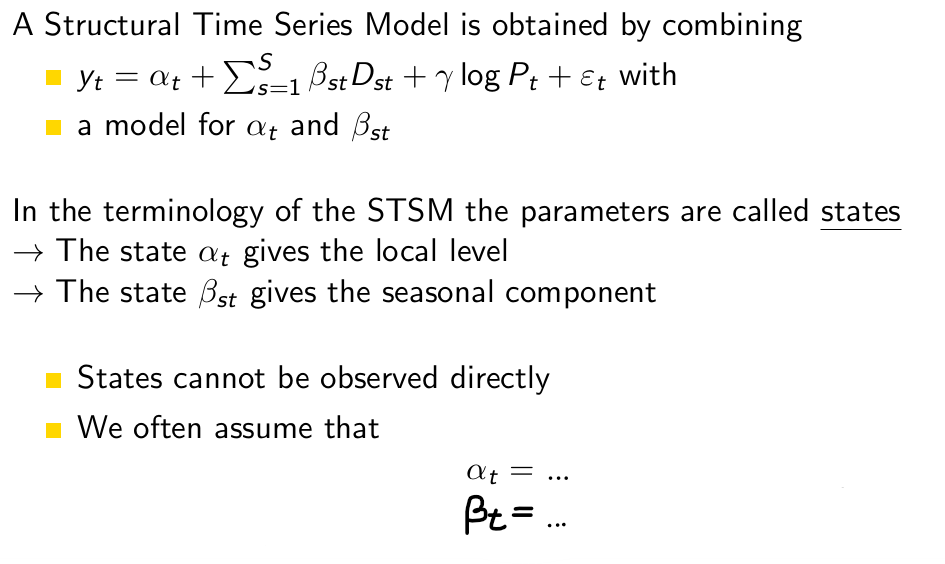

In the terminology of the STSM the parameters are called …

states

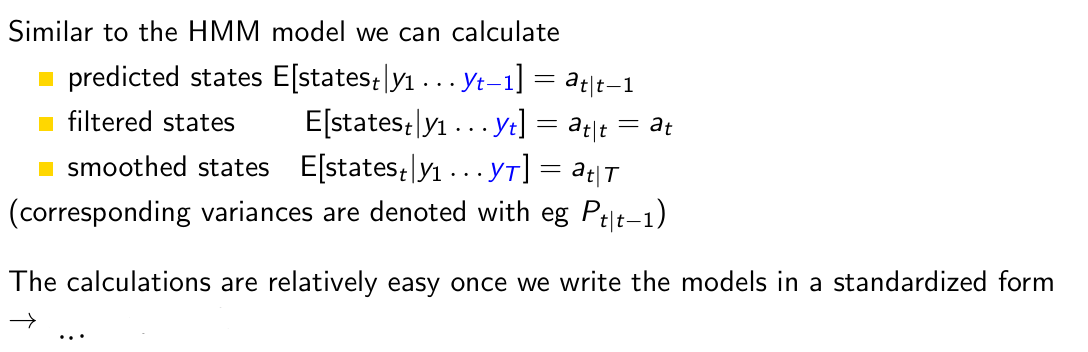

state space form

One of the main tools for state space models is the …

Kalman Filter