ATAR Economics - Microeconomics: Chapter One and Two

1/26

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

27 Terms

Law of Demand

There is an inverse relationship between price and quantity. As price goes up, quantity demanded goes down and vice versa.

Movement Along the Demand Curve

A contraction or expansion will occur only when price change for the product or factor (constant income). The demand curve does not move ** note the degree or extent

Influence of Non-price Factor: Demand

Demand will either increase or decrease, the demand curve will either shift left or right.

Factors Affecting Demand

Levels of Disposable Income

The Price of Substitutes

Tastes and Preferences

Expectations

Population Factors

Other Factors: Advertising

Law of Supply

a higher price will lead producers to supply a higher quantity to the market. Because businesses seek to increase revenue, when they expect to receive a higher price for something, they will produce more of it

Non Price Factor: Supply

Price of Other Goods

Technology

Prices of Resources

Expectations of Products

Number of Sellers

Weather

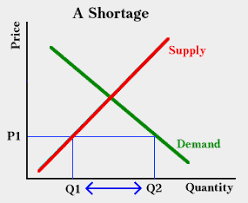

Shortage

A shortage in economics occurs when the quantity demanded for a good or service exceeds the quantity supplied at a given price, leading to a situation where not all consumers can obtain the desired product.

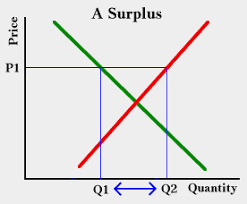

Surplus

A surplus in economics refers to the excess of a product or resource that remains after all needs have been met. It can lead to lower prices or increased consumption.

The Roles Of Market

A market exist when buyers and sellers exchange goods, services, or resources.

Market Consists of…

Buyers (Demand

Sellers (Supply)

Something to Exchange (goods or services)

Product Market

A product market refers to the marketplace where goods and services are bought and sold by consumers. It is where products are offered for sale and consumers make purchases.

Factor Markets

a factor market is where resources like labour, capital, land, and entrepreneurship are bought and sold to produce goods and services.

Competitive Market

According to the intensity of competition in the market

Firms: Price Takers

They must take the price that is established by the market

Firms: Price Settlers

Who have market power and can make their own price

Imperfect Market

Small numbers of firms

Product Differentiation

Price Settlers - Firm

Entry into the market is restricted

Opportunity Cost

Cost of the next best alternative use of money, time, or resources when one choice is made rather than another

Equilibrium Price

The equilibrium price is where the supply and demand for a product are balanced, resulting in a stable price for that product.

Price Mechanism

The tendency to move toward the equilibrium price is known as the market mechanism

Law of Increasing Costs

as the production of a good increases, the opportunity cost also increases, because resources are not of the same quality

Inferior Good

a type of good whose demand decreases when consumer income rises. Examples include generic brands or public transportation.

Two reasons for Law of Demand

Substitution Effect

Income Effect

Market Equilibrium Changes

Market equilibrium increase in demand; P goes up, q goes up

Market equilibrium decrease in demand; p goes down, q goes down

Market equilibrium increase; p goes down, q goes up

Market equilibrium decrease; p goes up , q goes down

Combinations outside of the line:PPF

Impossible to produce since there are inefficient resources

Combinations inside of the line:PPF

Not all resources are being employed or not being used in the most efficient manner

Why is PPF in a negative slope

Law of opportunity cost; one of the two goods available needs to be sacrificed if the economy decides to increase the production of one of the goods, and scarcity of resources as it reallocates resrouces for production

Factors of Production

Land

natural resources used in the production process, such as water, minerals, and land itself. It is one of the essential components alongside labour, capital, and entrepreneurship.

Labour

the physical and mental effort exerted by humans in the production process. It includes the work done by individuals to produce goods and services.

Capital

man-made resources used in the production process, such as machinery, tools, buildings, and technology. It is essential for creating goods and services.

Enterprise

the abilities of individuals to combine other factors (land, labour, capital) to create goods and services.