SIE EXAM

1/165

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

166 Terms

Par Value

Arbitrary value for accounting purposes

non marginable and marginable securities

Marginable: exchange listed securities, US government securities, OTC securities listed on the fed marginable securities list

Non marginable: options, mutual fund shares, new issues that have been publicly traded for less than 30 days, and penny stocks

Authorized stock

Fixed number of shares that may be issued when a corporation is formed

Issued shares

Authorized shares that have been sold

Treasury stock is considered issued shares that have been repurchased by the company and are not considered outstanding.

Outstanding shares

Total number of shares in circulation

Outstanding shares = issued shares - treasury stock

Aggregate value

Outstanding shares x Par value = aggregate value

Preemptive rights

Distributed to shareholders when a company is issuing new shares. Short term securities that give the owner the option to buy shares at a reduced price.

Only common stock gets pre emptive rights

Have a life of about 4-8 weeks. Not redeemable

Stock split

Can be forward or reverse. Must adjust par, so $1 par would go to $.5 after (2:1) split.

assume x:y; for price adjustment: y/x

for share adjustment: x/y

Current yield

Annual income / market price

Earnings per common share

Earnings available for common/ common shares outstanding

Treasury stock

Shares repurchased by a corporation after issuance.

treasury stock does not vote or receive dividends

Statutory Voting vs Cumulative

Statutory: Votes must be cast evenly

Cumulative: Can divide total votes as desired. Good for small investors

Preferred stock

Can be callable, cumulative, convertible, and participating.

Cumulative stock is guaranteed dividends.

Convertible stock gives the opportunity for growth- most sensitive to price changes

Participating gives extra dividends.

based on market interest rates

common stockholder

owner in a corporation. common stock is not callable

warrants

give the holder an option to buy stock at a premium of the current market price. usually have a life around 5 years

offered as a sweetener

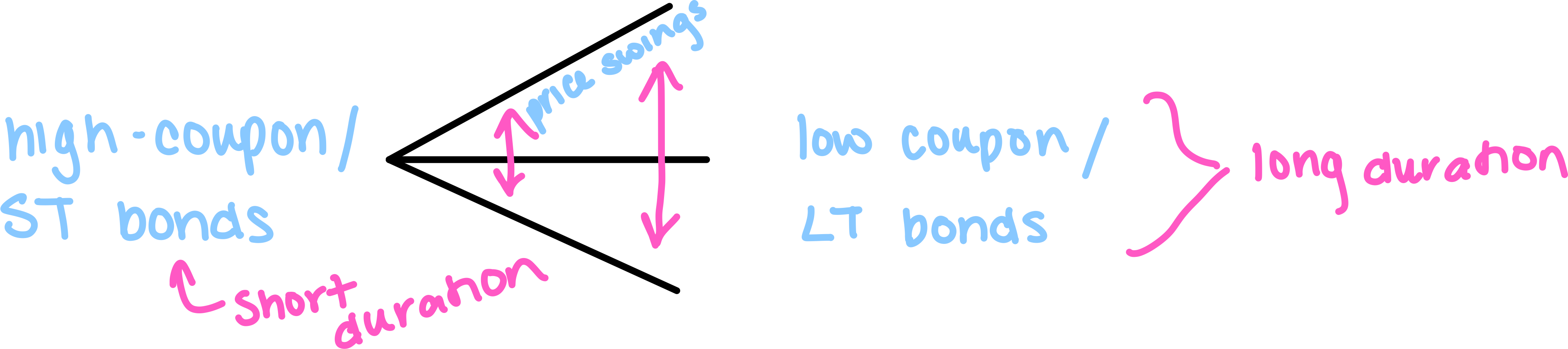

0 coupon bonds

purchase at a discount and receive no interest payments, but receive more at maturity than the purchase price.

no reinvestment risk

serial bond

bond issues with single issue dates and different maturities and interest rates. often used by municipals

series bond

same maturity but have different issuance dates and often pay different interest rates.

bond quotes

if there is no fraction, add a 0 to the quote for $

corporate bonds are 1/8 of par. ex if quoted 80 8/32 =80.25 and move decimal to the right for $802.5

government bonds are 1/32. some are 1/64

term bonds are quoted in % of par. serial bonds are quoted on a yield basis

bid / ask spread

investor pays the dealer the ask when buying and bid when selling.

98.16 ask = 98 and 16/32 cents

basis points

refers to the yield. each % of the yield = 100 bps. 1bps = .0001 or 1/100th of a percent

bond point

1% of par

selling at par

coupon rate = current yield = YTM

selling at a discount

coupon rate < current yield < YTM

below par

most likely to never be called by an issuer

selling at a premium

coupon rate > current yield > YTM

nominal yield

the coupon rate or stated interest

annual income / par

current yield

the return an investor is earning

annual income / market price

term bond

same interest rates and maturities

callable bond

issuer can redeem the bond @ a predetermined price (% of par) before maturity

likely to be called when interest rates drop

issuer buy back

Yield to worst

must be disclosed to client. this is the lesser of the YTC or YTM

YTC > YTM

for a bond trading at a discount

YTM would be yield to worst

YTC < YTM

for a bond trading at a premium

YTC would be yield to worst

put bonds

have lower coupon rates and higher interest rates. benefit to the investor

bondholder buyback

once exercised, the bond price will not fall below the option price if rates rise

bond payouts

adjustable rate bonds

fluctuate with the market. as interest rates drop, the rate on the bond drops

are protected from interest rate risk

call protection

prevents a callable bond from being called the first few years of its life.

benefit is greatest when the bond is most likely to be called (rates are falling / prices are rising)

yield to call

the yield of a callable bond, assuming it is held until its first call date

call premium

price above par where the issuer has the right to call in the bonds from bondholders prior to maturity

trust indenture act of 1939

all corporate issues of $50 mil or more must have a trust indenture, with the exception of munis and government issues

trustee is appointed by the issuer and protects interests of bondholders

bond types

secured - mortgage, equipment trust certifications, collateral trust bonds

unsecured - debentures, junk bonds, guaranteed bonds

other - income bonds. not suitable when seeking income because payments are not guaranteed

convertible bonds

conversion ratio = par/ conversion price

conversion value = conversion ratio x market price

parity price of stock and bonds

PP of stock = bond mkt value / conversion ratio

PP of bonds = conversion ratio x market price of common

treasury securities

Tbills: > 1 yr. $100-$5mil. no interest. quote in yield

Tnote: 2-10 yr. $100-5mil. semiannual interest. quoted as 1/32

Tbond: 10-30 yr. $100-5 mil. semiannual interest. quoted as 1/32

unqualified muni

a muni with an unconditional affirmation that there are no legal issues

GO bond

muni debt backed by the full faith, credit, and taxing power of the muni

unsecured bonds

ad valorem tax

need voter approval

have statutory debt limits

used for roads, schools, and muni buildings

CAB

capital appreciation bonds. muni zero discount

good for munis close to debt limit

revenue bonds

backed by the revenue from a specific project

higher coupons and riskier

no voter approval, but must do feasibility study

self supporting

used for tolls, hospitals, utility companies

bond tax status

US govt and govt agencies: subject to federal, exempt from state

private govt agency or corporate: subject to federal and state

munis: exempt from both if a resident

money market debt

ST debt and those < 1 yr maturity. large denominations

if maturity is < 270 days, not registered to the SEC

Fed buys MM from primary dealers to increase debt availability since it puts cash into banks

GAN

comes from federal transit funding

RAN

comes from federal highway funding

special tax bonds

backed by taxes other than an ad valorem tax like liquor, gas, cigarette, or sales tax.

non self supporting

federal funds

overnight loans between member institutions of the federal reserve system

debentures

secured by the full faith and credit of the issuer

3 investment companies

face amount certificate companies (obsolete) management companies, unit investment trust

management corporation

open end (mutual funds) and closed end (publicly traded fund)

open end is only common shares

closed end is negotiable and not redeemable

UIT

fixed UIT (fixed trust) and non fixed UIT (variable annuity)

fixed is mainly bonds but also stocks'

non fixed is only mutual funds

mutual funds

established by a sponsor and shares are sold by the fund distributor.

offers professional money management and diversification. must have 75-5-10 diversification (securities - per issuer- voting)

always require a prospectus

largest expense is the management fee

can easily be redeemed (liquid). must pay redemption proceeds within 7 days

LT gain is taxed at preferential rate, ST is at ordinary

load fund

MF with a sales charge

sales charge can’t exceed 8.5% of POP

POP

NAV + sales charge

12-b1 fund

max sales charge can be 7.25%

12-b1 fee can’t exceed 1% of average annual net assets

of the 1%, .75% can be used for marketing and distributing, and .25% for admin expenses

MF Class A

NAV: NAV + sales charge

sales charge: front end with breakpoints

12b-1: low

good for: large / LT accounts

MF Class B

NAV: NAV

sales charge: back end unless held for long enough

12-b1: high but can convert to class A

good for: 5-7 year hold

MF Class C

NAV: NAV

sales charge: none

12-b1: very high

good for: 1-2 year hold

expense ratio

total expenses / total net assets

ETFs

traded on an exchange like a stock, but are usually registered as open-end

linked to a specific index

nontraditional ETFs are okay for short term investing

private REITs

not listed on exchanges and aren’t registered with the SEC. not liquid

95% REITs income must be RE related income

Registered non-listed REITs

registered with the SEC but not on an exchange. not liquid

listed REITs

registered with SEC and on an exchange or OTC. very liquid and can use margin and short

no load fund

MF that markets and sells their own shares

12-b1 can not exceed .25% of net assets

passively managed

oil and gas programs

exploratory: find where gas likely is - 100% deduction for intangible and tangible drilling costs

developmental: find properties near producing oil and gas wells - deduction for intangible and tangible drilling costs

income: purchase existing producing wells - oil depletion allowance

breakpoint sale

when a customer buys just beneath the breakpoint level so they didn’t get the benefit of the lower sales charge

NAV

(total assets - liabilities) / # of outstanding shares

increases when fund receives dividends or interest and when liabilities decrease.

figured using forward pricing

MF types riskiest —> least risky

-special situation fund (bankruptcy, takeover)

-sector / specialty fund (1 industry or area)

-growth fund ( growing common stocks)

-balanced (bonds and pref stock)

-value (blue chip common stocks)

-income (large cap/ blue chip pref stocks and bonds)

-money market fund (Tbills, BAs, commercial paper)

dividend dates (DERP)

declaration date- when company declares dividend

Ex-dividend- 1st day a stock trades and purchaser will not receive upcoming dividend

record date- purchasers of stock must settle no later than the record date to receive dividend

payable date- the actual day checks will be sent

**ex dividend date is the same as the record date

cost basis

purchase price (including commissions or markups) x number of shares

**only includes amount paid for the securities. excludes commission price when selling

TIPS

Tnotes and Tbonds whose interest adjusts based on inflation (uses real interest rate)

no purchasing power risk

STRIPS

government 0 coupon bonds

no reinvestment risk

trading markets

primary (IPOs) and secondary

Secondary:

first market- exchanges

second market- OTC

third market- OTC trading of listed securities

fourth market- institutional trading systems

broker vs dealer

broker (agent):

charges commission

no inventory is held

no risk to firm

dealer (principal):

markup / markdown

inventory is held

risk to firm

**firm can’t be the broker and dealer on the same transaction

**markups can not exceed 5%. exceptions: MFs max is 8.5% and Munis are exempt but have similar rules

SLOBS and BLUSS

Sell Limits over the market Buy Stop (SLOBS)

Buy Limit under the market Sell Stops (BLUSS)

-cash dividends adjust these orders on the ex-date

**Stops are to “stop the pain”. You would be happy to take profits at a limit because it is an opportunity for the client

** Stock splits and dividends affect all order (# of shares inc, price dec)

-new shares = share x (1+div%)

-new price = price / (1+div%)

types of orders

market orders: filled immediately

limit orders: filled at specific price

stop orders: turns into a market order when price is hit

stop limit: turns into limit order when price is hit

buy call

right to buy

profit = unlimited

loss = premium

breakeven = strike + premium

sell call

obligation to sell

profit = premium

loss= unlimited

breakeven = strike + premium

buy put

right to sell stock

profit= strike price - premium

loss = premium paid

breakeven = strike price - premium

sell put

obligation to buy

profit = premium

loss = strike price - premium

breakeven = strike price - premium

premium =

IV + time value

new account form

name and address, if legal age, registered rep, principal signature, and if a corporation, the name who will transact business

must be sent 30 days of account open and every 3 years to update

customer signature nor education need to be included, unless margin account then signature is needed

KYC

must make an effort to obtain financial status, tax status, investment objectives

suitability questionnaire rules

must obtain:

investment objective

investment experience

age

financial needs

tax status

investment time horixon

liquidity needs

risk tolerance

**must be updated every 36 months

Regulation S-P

can’t disclose nonpublic personal info with 3rd parties

Regulation BI

best interest

disclosure obligation requires written disclosure of material facts before or when a recommendation is made

can never be waived

does not apply to institutions

Reg T

initial margin: 50%. must be at least $2,000

min maintenance margin: long = 25% short = 30% of the closing price of the security that day

covers borrowing between customers and brokers

an extension request gives a customer 2 additional business days to pay for a securities purchase

FRB determines if an OTC stock is marginable

equity value =

market value of security - amount owed broker

equity % =

equity value / market value of security

Reg U

covers borrowing between banks and brokers

fiduciary account

ONLY the fiduciary can trade. cash accounts only

revocable vs irrevocable trust accounts

revocable: can be eliminated by the trustor

irrevocable: permanent and assets aren’t included in tax purposes

living vs testamentary trust accounts

testamentary accounts are initiated upon death

charitable trust

can give assets to charity upon death

can deduct the fair market value of the securities as long as they have been held for 12 months