Economics paper 1

1/100

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

101 Terms

3 main economic groups

Consumers, producers and government

4 factors of production

Land, labour, capital, enterprise

3 key questions for reducing the economic problem

How should goods and services be produced? What should be produced? Who should the goods and services be produced for?

3 types of economies

Market, mixed, controlled

3 sectors

Primary, secondary, tertiary

Benefits of specialisation for producers

Higher output, higher productivity, higher quality, bigger market, economies of scale, saves time and money

Costs of specialisation for producers

Diseconomies of scale, if one part of the process fails the whole production system may stop, may not be able to buy necessary resources or components, movement of workers

Benefits of specialisation for workers

Increased skill (potentially increased wages), increased job satisfaction, increased standards of living

Costs of specialisation for workers

Demotivation, deskilling, unemployment if they are replaced by machines

Benefits of specialisation for regions

Makes best use of its resources, creates nearby jobs for residents, better infrastructure

Costs of specialisation for regions

If demand falls industry may collapse, resources may run out, other region could become better at producing

Benefits of specialisation for countries

Greater efficiency and output, more jobs, international trade with surplus output, improved infrastructure, increased standards of living, government revenue increases

Costs of specialisation for countries

If industry declines unemployment will increase, overspecialisation, over exploitation of resources, negative externalities to the environment

Direction the demand curve slopes

Downward

Movement up the demand curve

Contraction

Movement down the demand curve

Expansion

Causes of shifts in demand

Change in income, marketing, change in taste and fashion, substitutes, complementary goods, expectations of a change in price, population changes, government policies

Impact on demand curve if demand increases

Shifts to the right, price increases, quantity increases

Impact on demand curve if demand decreases

Shifts to the left, price decreases, quantity falls

Formula for PED

Percentage change in quantity/ percentage change in price

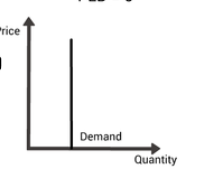

PED value= 0

Perfectly inelastic

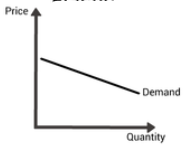

PED value= Between 0 and -1

Inelastic

PED value= -1

Unitary elastic

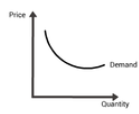

PED value= Between -1 and -infinity

Elastic

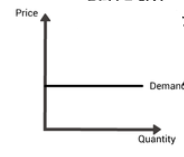

PED value= Infinity

Perfectly elastic

Perfectly inelastic

No change in quantity as price changes

Inelastic

Change in quantity is less than change in price

Unitary elastic

Change in quantity is equal to change in price

Elastic

Change in quantity is more than change in price

Perfectly elastic

An infinite amount can be demanded at a given price, no change in price

PED- What is it?

Perfectly inelastic

PED- What is it?

Inelastic

PED- What is it?

Unitary elastic

PED- What is it?

Elastic

PED- What is it?

Perfectly elastic

Importance of PED for consumers

If a product has inelastic demand they are likely to face price rises and high taxes, allows them to make choices if substitutes available

Importance of PED for producers

Allows producers to maximise total revenue, affects their decision whether to supply the product or not

What direction does a supply curve slope

Upwards

Movement up the supply curve

Expansion

Movement down the supply curve

Contraction

Causes of a shift of the supply curve

Costs of production, taxes and subsidies, new technology, climate change, increase in producers/size of firms, government regulation

Impacts on supply curve if supply increases

Shift to the right, prices fall, quantity increases

Impacts on supply curve if supply decreases

Shift to the left, prices rise, quantity decreases

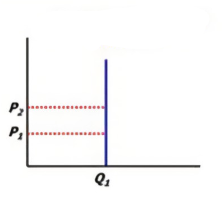

PES value= 0

Perfectly inelastic

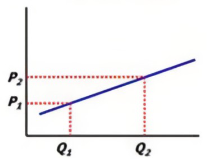

PES value= Between 0 and 1

Inelastic

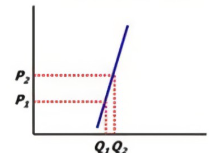

PES value= 1

Unitary elastic

PES value= Between 1 and infinity

Elastic

PES value= infinity

Perfectly elastic

PES- What is it?

Perfectly inelastic

PES- What is it?

Inelastic

PES- What is it?

Unitary elastic

PES- What is it?

Elastic

PES- What is it?

Perfectly elastic

Importance of PES for consumers

If the product has inelastic supply they are likely to face high prices to obtain more, may not be able to get more of a product with very inelastic supply, if a product has elastic supply it is easy to purchase more

Importance of PES for producers

Firms would prefer elastic supply so it is easier to response to prices, elastic supply enables a firm to be more flexible, very inelastic supply means price will depend entirely on demand

3 functions of price

Signalling, transmission of preferences, rationing

Effects on equilibrium price and quantity if demand increases

Price increases, quantity increases

Effects on equilibrium price and quantity if demand decreases

Price decreases, quantity decreases

Effects on equilibrium price and quantity if supply increases

Price decreases, quantity increases

Effects on equilibrium price and quantity if supply decreases

Price increases, quantity decreases

2 types of competition

Price and non-price

3 reasons why producers compete

To: enter a new market, survive in a market, make a profit.

Benefits of competition for producers

Increased efficiency: costs cut, innovating, improving productivity

Costs of competition for producers

Lose consumers, replace workers with technology

Benefits of competition for consumers

Cheaper prices, improved quality of goods/services, innovation, increased consumer sovereignty

Costs of competition for consumers

Innovations may be harmful, quality may fall, marketing may be dishonest

Monopoly- control of prices

Able to set prices

Oligopoly- control of prices

Can influence price but is restrained by the reaction of rivals

Competitive- control of prices

Price is set by market forces

Monopoly- level of price and output

Higher price, lower quantity

Oligopoly- level of price and output

Dependent on how strong competitors are

Competitive- level of price and output

Lower price, greater quantity

Monopoly- efficiency

Not seen as efficient but can be if they gain large economies of scale

Oligopoly- efficiency

Not seen as economically efficient

Competitive- efficiency

Efficient

Advantages of an increase in production

Increase in employment, rise in standard of living, increase in profits, gain larger economies of scale, gain greater market share, economic growth

Disadvantages of an increase in production

Workers replaced by machines, diseconomies of scale, other firms lose market share, environmental problems

Impacts of higher productivity

Lower average costs, increased economies of scale, increased profits, increased output, increased exports

Costs of productivity

Unemployment, fall in GDP

Formula for total cost

Total fixed cost + total variable cost

Formula for average cost

Total cost/quantity

Formula for total revenue

Price x quantity

Formula for average revenue

Total revenue/total quantity

Formula for profit

Total revenue- total cost

9 internal economies of scale

Division of labour, financial, increased dimensions, managerial, marketing, bulk buying, risk-bearing, research and development, technical

4 external economies of scale

Concentration of firms, education and training facilities, location, transport

Reasons for lack of labour mobility

Lack of skills, geographical immobility, personal factors, information failure

Factors affecting demand for labour

Demand for products, wage rates, real wages, productivity of labour, profits of firms, state of the economy

Factors affecting supply of labour

Wage rate, other monetary payments, non-monetary payments, education and training, barriers to entry, size of working population

Role of central banks

Issue bank notes, control monetary policy, manages foreign reserves, bank for the commercial banks, bank for the government

Role of commercial banks

Accept deposits, make payments for customers, make payments by accepting cheques, issue loans, provide foreign currencies, offer safe deposit boxes

Role of investment banks

Help firms: in mergers and takeovers, underwriting share issues, with international trade.

Role of building societies

Provide a limited range of services (mainly savings and mortgages), limited as to how much money can be borrowed from the money market

Importance of credit provision for consumers

Can buy now and pay later

Importance of credit provision for producers

Can borrow money to expand

Importance of credit provision for government

Can run a budget deficit or spend before taxes are collected

Importance of liquidity provision for consumers

Can borrow to pay later

Importance of liquidity provision for producers

Banks will provide overdraft facilities so firms can continue trading while waiting for payments

Importance of risk management for consumers

Allows savers to spread their risk by putting their money into a range of companies

Importance of risk management for producers

Reduces risk of not receiving payment on time