Inventory Control

1/16

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

Inventory control

Why ? Because inventory is money, and its needs to be well utilised

What ? Have the optimum level to minimise the cost of overstocking or stocking out

How ? Understanding better demand and costs

High inventory means …

High cost of carrying inventory - obsolescence, insurance, ect

Low inventory means…

Potential shortage and increasing ordering costs

Why inventory control ?

Inventory is money

Reduces inefficiencies, such as purchasing and sales managers spending more time in following up on orders

inventory is harder to control when:

Demand is unpredictable

Customer demand must be met quickly

Follows made to stock process

Purpose of Inventory

To maintain independence of operations

Each workstation can work at its most efficient schedule, and not depend on incoming material

To meet variation in demand

To allow flexibility in production scheduling

If setup cost is high, it is economical to produce a large number of units

To provide safeguard in variation against supplier's delivery schedule

Supplier cannot produce, or cannot deliver according to required production schedule

To take advantage of economic purchase order size

Dependency

Independent demand (ex: IKEA produces mugs and curtains. Demand for the two are independent)

Dependent demand (ex: IKEA produces frames and slats for beds, demand for both are dependent)

Cost of inventory

Ordering cots

Holding cots

Shortage costs

Holding costs

storage facilites

Breakage obsolescence

Depreciation

Opportunity cost of capital

Ordering costs

Cost of purchasing each order:

Clerical, managerial

calculating order counting quantities

Counting items

Shortage costs

Lost customers

Lost profits

Penalty for late delivery

Penalty for non delivery

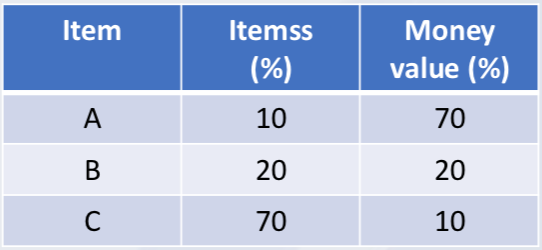

ABC valuation

A ltems:

High usage rate or high cost.

Tight control

B Items:

Less essential

Lower money value

C Items:

Least impact on sales

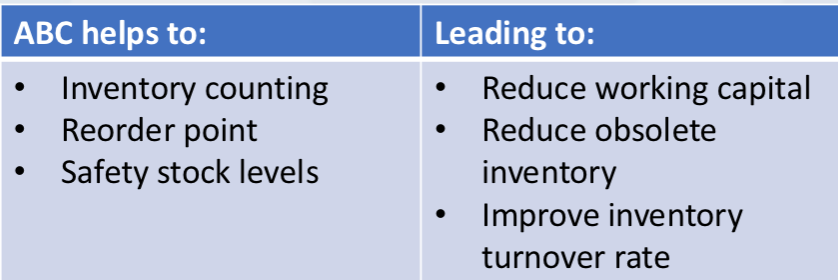

ABC helps to….leading to….

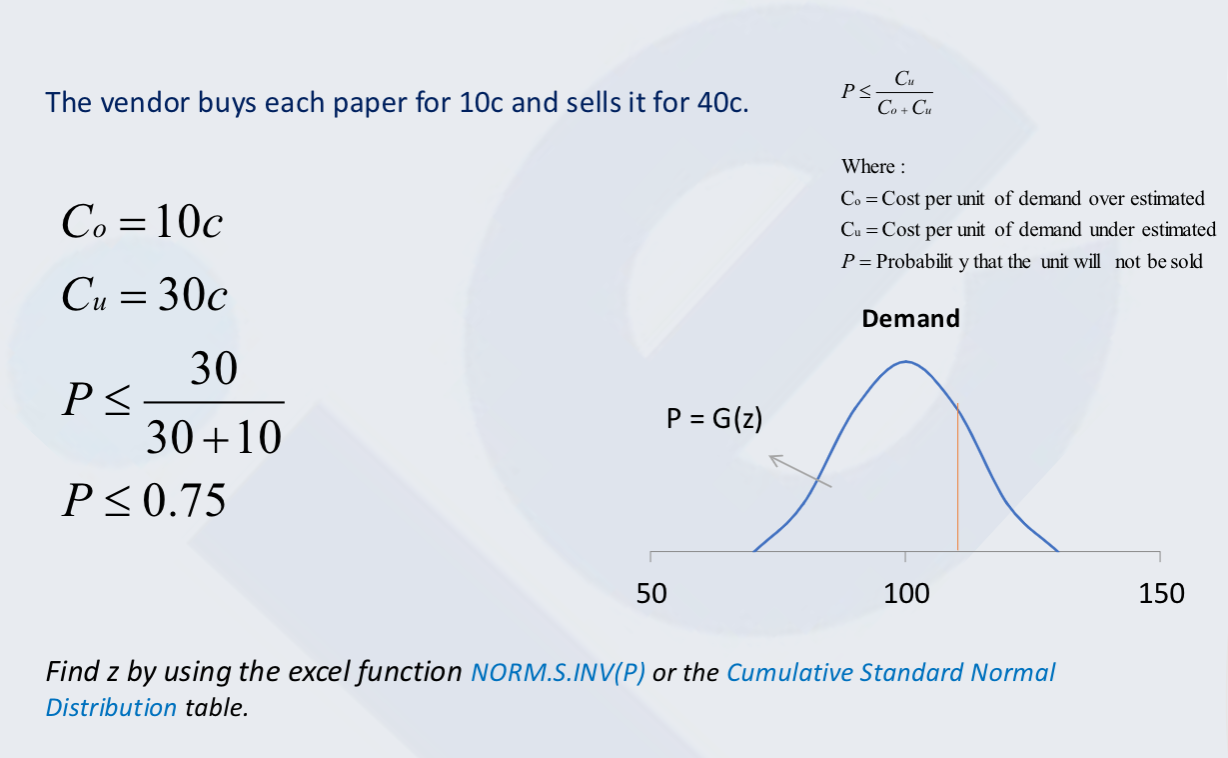

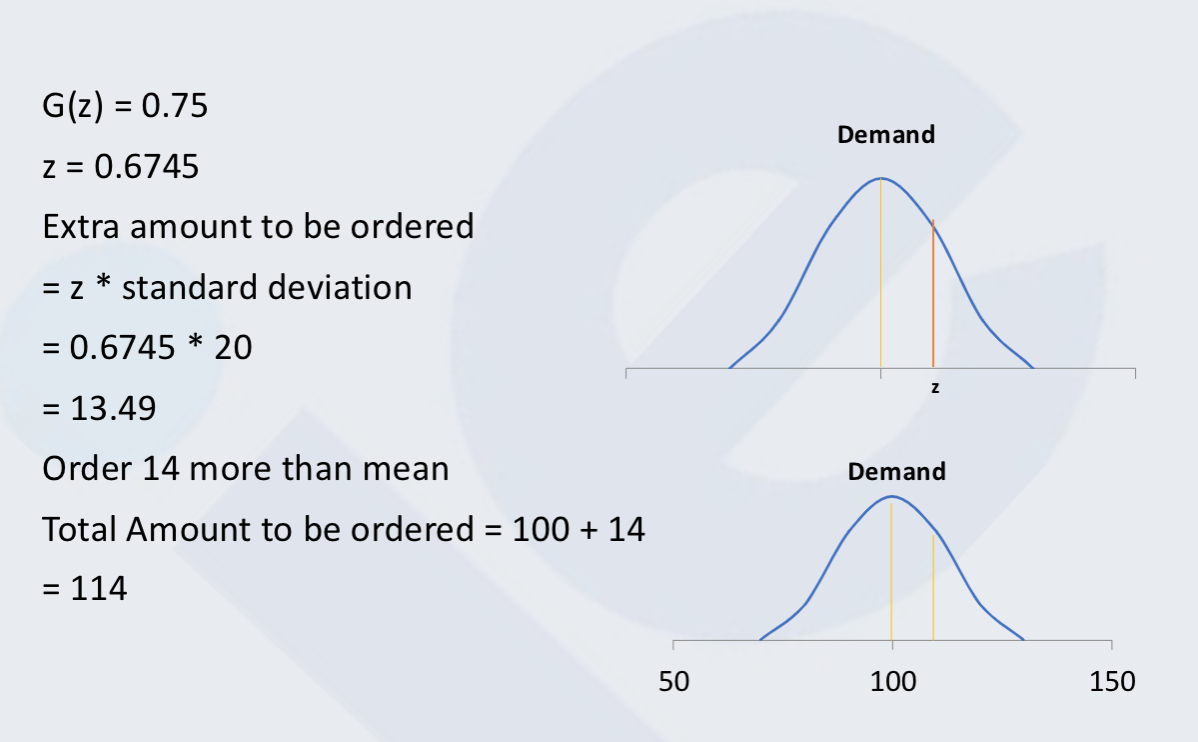

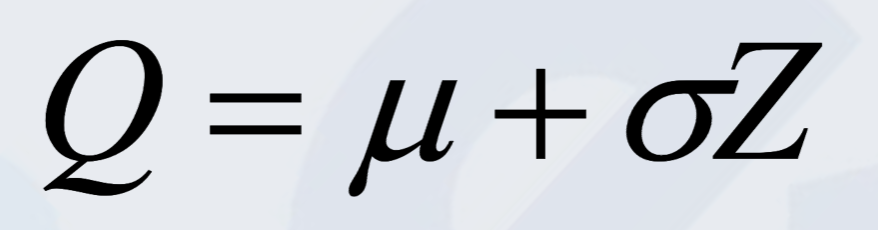

Single Period Inventory Model

One time purchase (ex: Christmas trees, newspapers, airline seat reservation)

Where

Q is Quantity to be Ordered

μ is Average Demand

σ is Standard Deviation

Z is probability of running out of the item

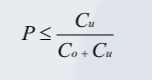

Where :

Co = Cost per unit of demand over estimated

Cu = Cost per unit of demand under estimated

P = Probability that the unit will not be sold