module 8 - costs

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

total revenue

the amount a firm receives for sale of its output

total cost

the market value of all inputs a firm uses in production

profit

total revenue - total cost (goal is to max this)

opportunity costs

the cost of something is what you get up to get it.

firm’s cost of production includes all the opporunity costs of making its output of goods and services

explicit costs

input costs that require an outlay of money by the firm

implicit costs

do not require an outlay of money by the firm (ignored by accountants)

economic profit

total revenue - total cost (explicit and implicit costs)

smaller than accounting profit

accounting profit

total revenue - total explicit cost

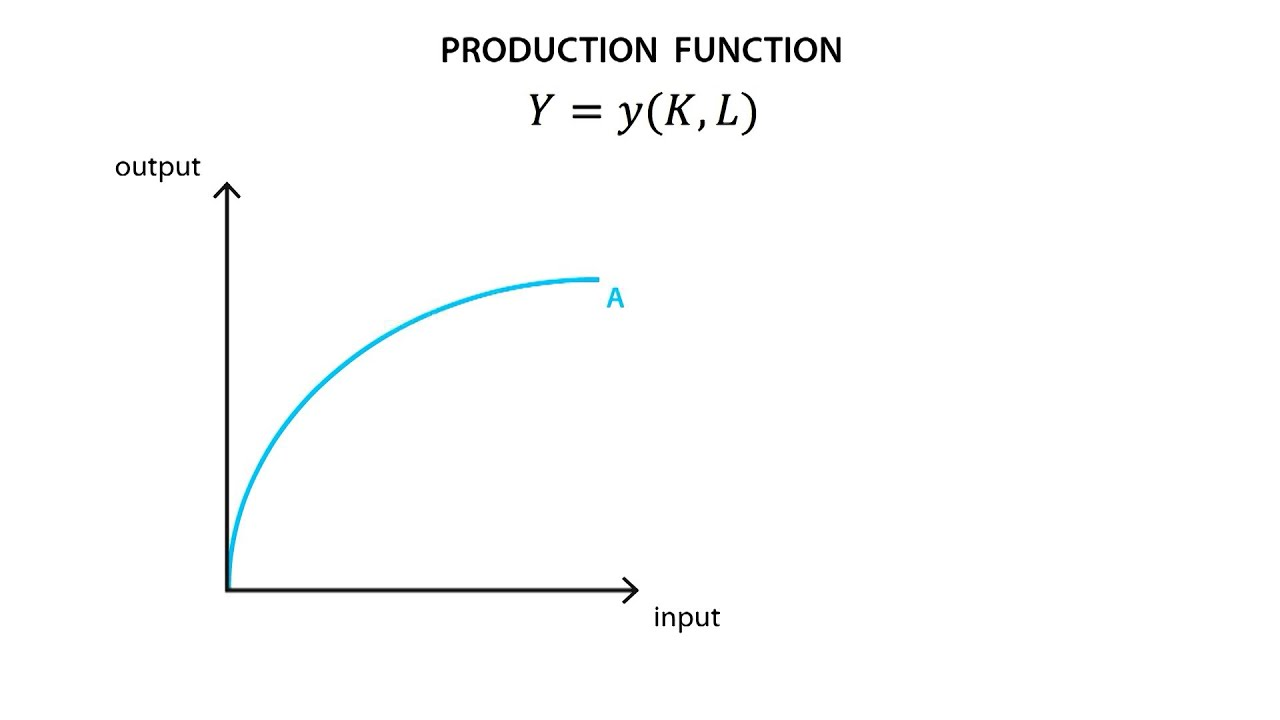

production function

relationship between the quantity of inputs used o make a good and the quantity of output of that food

typically gets flatter as production rises

marginal product

the increase in output that arises from an additional unit of input

slope of production function

diminishing marginal product

property whereby the marginal product of an input declines as the quantity of the input increases

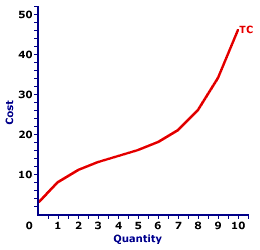

total cost curve

relationship between the quantity produced and the total costs

gets deeper as the amount produced rises due to diminishing marginal product

fixed costs (fc)

do not vary with the quantity of output produced

in short run

variable costs (vc)

vary with the quantity of output produced

applicable in the long run

average fixed cost

fixed cost/quantity of output

fc/quantity always declines as output rises

average variable cost

variable cost/quantity of output

typically increases as output increases

average total cost

total cost/quantity of output

also equals avc + afc

curve is typically U shaped

marginal cost

the increase in total cost arising from an extra unit of production

change in total cost/change in quantity

efficient scale

the quantity of output that minimizes average total cost (atc)

relationship between mc and atc

mc < atc, average total cost is falling

mc > atc, average total cost is rising

marginal cost crosses average total cost curve at minimum

long-run cost curves

differ from short run cost curves, because firms have greater flexibility in the long run (all costs are variable)

much flatter than short run cot curves and lie on or above the short-run cost curves

economies of scale

occur when long run average total cost falls as the quantity of output increases, often due to increasing specialization among workers

constant returns to scale

occur when long run average total cost stays the same as the quantity of output changes

diseconomies of scale

occur when long run average total cost rises as quantity of output increases, often due to increasing coordination problems