Personal Finance & Economic Indicators: Key Concepts and Processes

1/64

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

65 Terms

Personal Finance

the Study of Personal & family resources considered important in achieving financial Success

Financial Literacy

Knowledge of facts, concepts, Principals, & tools of Money Management

Financial capability

ability to handle day-to-day financial Matters

Financial Well-being

the degree to which we can fully Meet current & ongoing financial obligations and feel secure in our financial future & be able to make Choices that allow us to enjoy life

Financially responsible

accountable for your future financial Well-being & Strive to make good decisions in Personal finance

5 steps in the financial planning process:

1. Evaluate our financial health relative to current lifestyle and career choice.

2. Define our financial goals.

3. Develop a plan of action to achieve our goals.

4. Implement spending and saving plans to monitor and control progress toward goals.

5. Review our financial progress and make changes as appropriate.

Financial success

achievement of financial aspirations that are desired, planned, or attempted

Financial security

comfortable feeling that our financial resources will be adequate to fulfill any needs we have as well as most of our wants

Financial happiness

experience we have when we are satisfied with our money matters

Current consumption

Spending on goods & Services

Savings

Income not spent on current consumption

Investments

assets Purchased with the goal of Providing additional future income from the asset itself

Standard of living

Where we'd like to be

Level of living

where we actually are in the Moment

Economy

system of Managing the productive resources of a country, State or community

Capitalism

A country's trade & industry are controlled by private owners who seek profit

Economic growth

Condition of increasing production (business activity) and consumption in the economy

Consumer spending accounts for

about 70% of the total U.S. economy

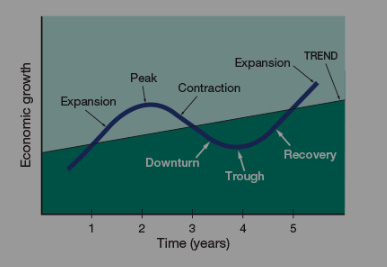

Business cycle

Process by which the economy grows and contracts over time

Deleveraging

a time period when credit use shrinks in an economy instead of expanding as during normal economic times

Recessions

recurring period of decline in total output, income, employment, and trade

Economic indicator

any economic statistic (unemployment rate, GDP, inflation rate) that suggests how well the economy is doing or how well the economy might do in the future

Procyclical economic indicator

moves in the same direction as the economy

Procyclical economic indicator examples

retail sales, industrial production, new orders for durable goods (housing starts), # of employers on nonagricultural payrolls, & the GDP.

Gross Domestic Product (GDP)

the market value of all the goods & services produced in the country. Best example of procyclical indicator

GDP <2%

Very low growth (not enough to create jobs for job market college graduates)

GDP =3%

growth occurring at a Safe Speed that doesn't induce excessive inflation

GDP >4%

fears of rising Prices or inflation

Counter cyclical economic indicator

Moves in the opposite direction from the economy

Counter cyclical economic indicator examples

Unemployment rate (GDP = 2.5% to prevent Unemployment rate rising)

Leading economic indicators

indicators that Change before the economy changes

Leading economic indicators examples

Stock Market, # of new building Permits, existing home sales, home Prices, jobless claims, & the CCI

Consumer Confidence index

gauges how consumers feel about the economy & their personal finances

The Conference Board Leading Economic Index (LEI)

Composite index reported Monthly that suggests the future direction of the US economy

Inflation

rise in the general level of Prices

Stagflation

Stagnant economic growth & high unemployment accompanied by rising Prices

Consumer Price Index (CPI)

broad measure of Changes in the Prices of all goods & Services Purchased for consumption by urban households.

Real Income

income Measured in constant Prices relative to some base time Period

Nominal Income

income that hasn't been adjusted for inflation & decreasing Purchasing power

Purchasing Power

the amount of good's & services that one's income Will buy

Rule of 70

A formula to determine how long it will take for the Value of a dollar to decline by one-half

Deflation

broad, sustained decline in Prices of goods & Services

Interest

Price of borrowing money, Most often reported as an Annual Percentage of the amount borrowed

Fed (Federal Reserve Board)

an agency representing the central banking system of the United States.

Federal Funds Rate

Short-term rate at which banks lend funds to other banks overnight

Opportunity cost

the value of the next best alternative that must be forgone

Trade-offs

giving up one thing for another

Utility

the ability of a good or service to satisfy a human want

Marginal Utility

extra satisfaction derived from having one more incremental unit of a product or service

Marginal Cost

the additional cost of one more incremental unit of Some item

Marginal tax rate

the tax rate at which our last dollar earned is taxed

Tax-exempt income

income from an investment whose earnings are free or exempt from taxation

Tax-exempt income examples

interest on Municipal bonds issued by agencies of state & local governments

Tax deferred income

When a Person does not make a current Payment on income taxes now & instead Pays the tax at a future point in time

Tax deferred income examples

401(k) retirement Plan

Time Value of Money (TVM)

Method by Which one can compare cash flows across time

Simple Interest

i = p x r x t where

p = is the Principal,

r = is the rate of interest,

t = is the time in years

Compound Interest

return earned when previous investment earnings are reinvested into the same investment

Future Value

the value of an asset projected to the end of a particular time period.

FV Equation

(Present Value of Sum money )(1.0+i)^n

Rule of 72

formula for figuring the # of years it takes to double the Principal using compound interest.

Rule of 72 Formula

72 / interest rate = time

Annuity

a stream of payments to be over time at fixed intervals, typically annually

Present Value

the current value of an asset that will be received in the future.

PV Formula

PV = (Future Value of Sum of Money) / (1.0 + i)^n